1. Ledger accounts are used to summarize transactions related to specific accounts. Each ledger contains one page for each individual account.

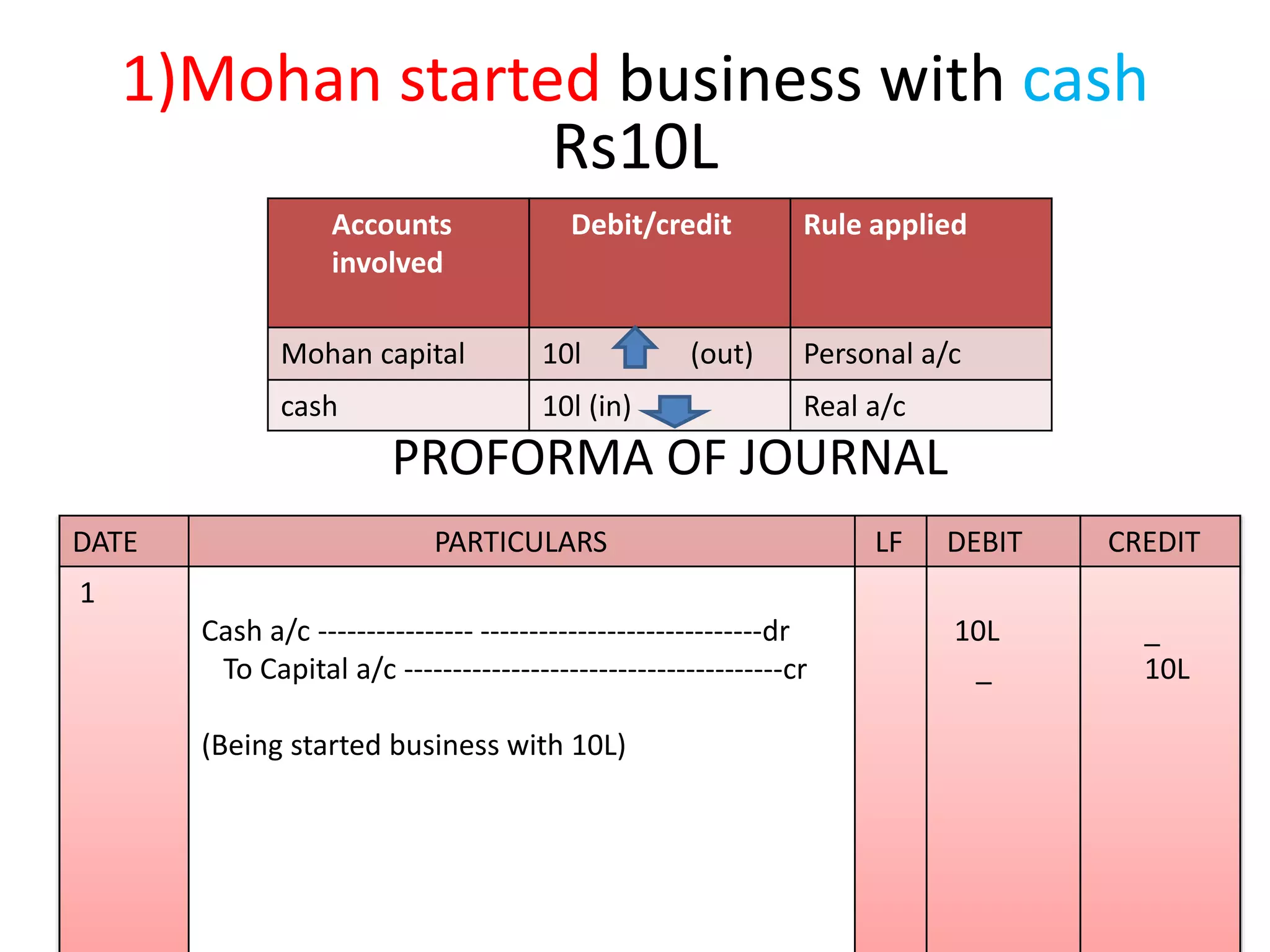

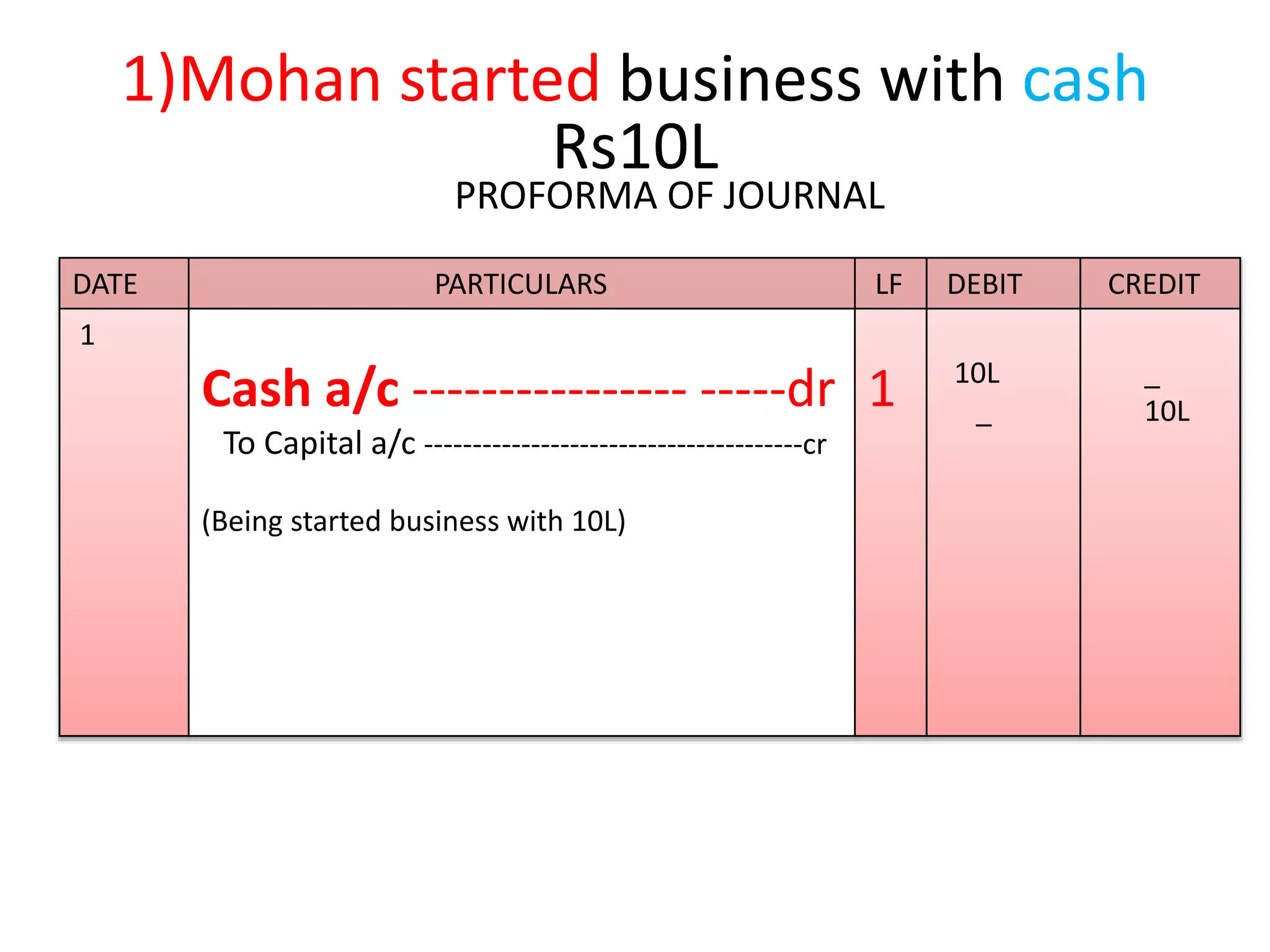

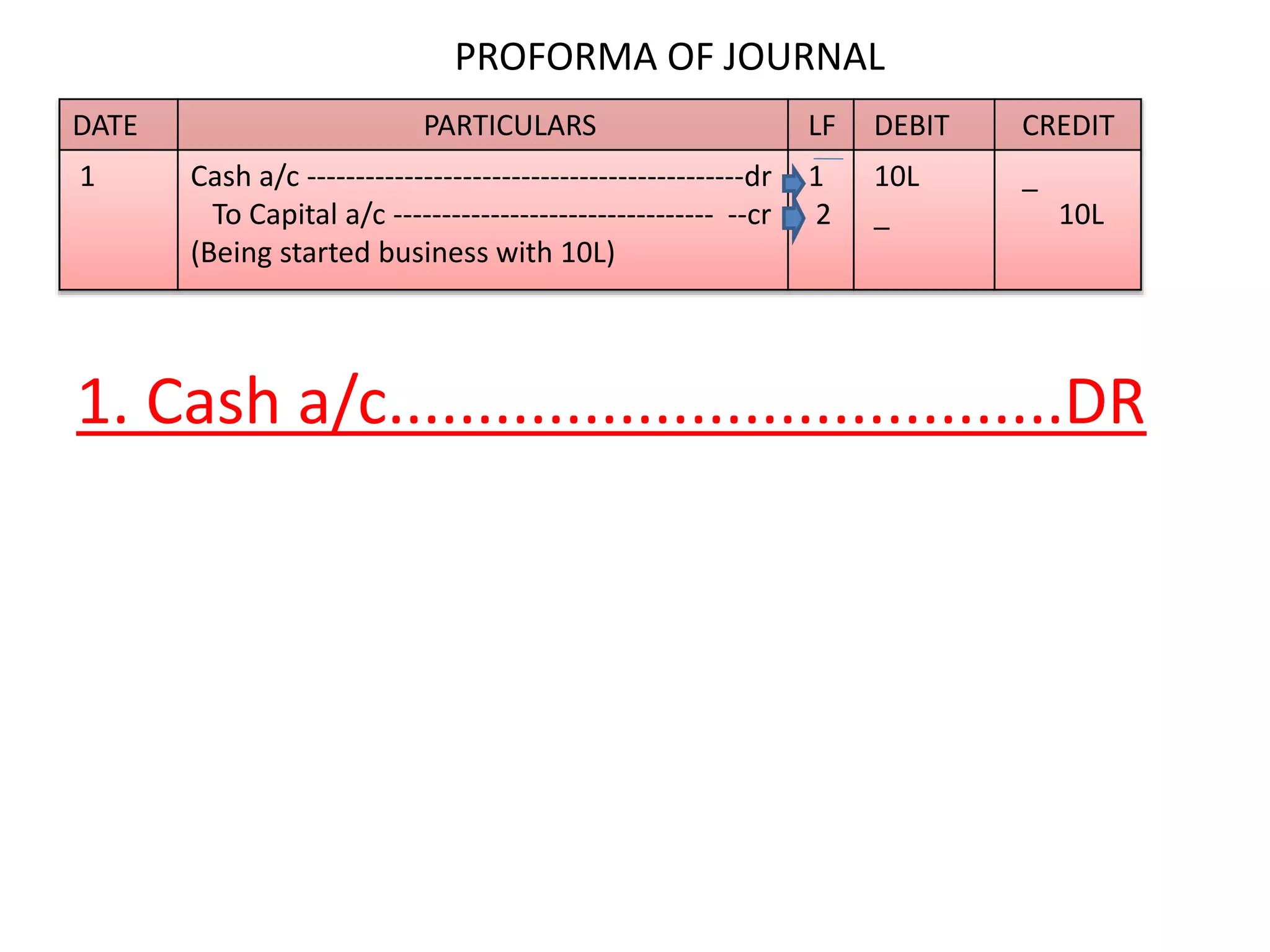

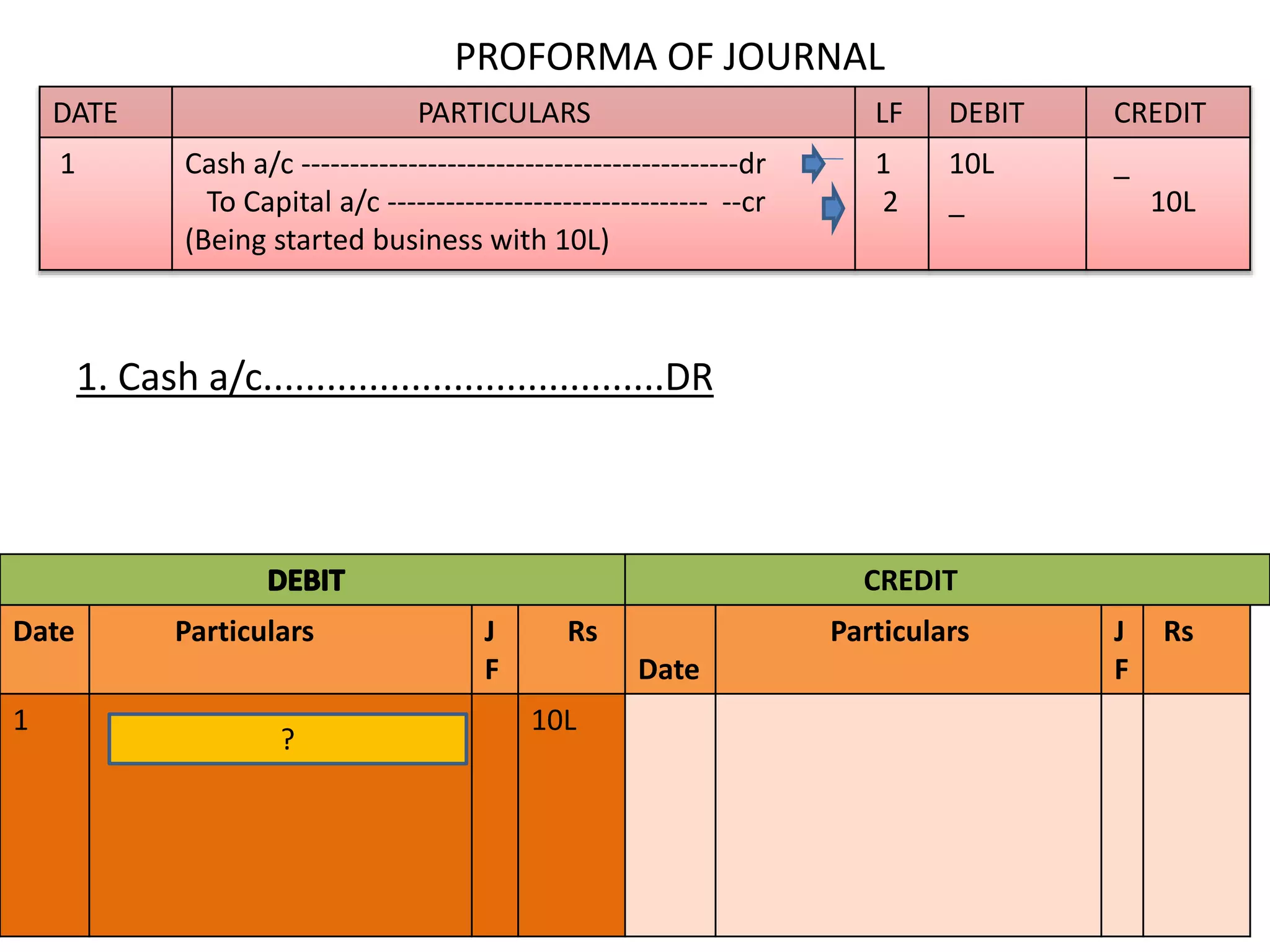

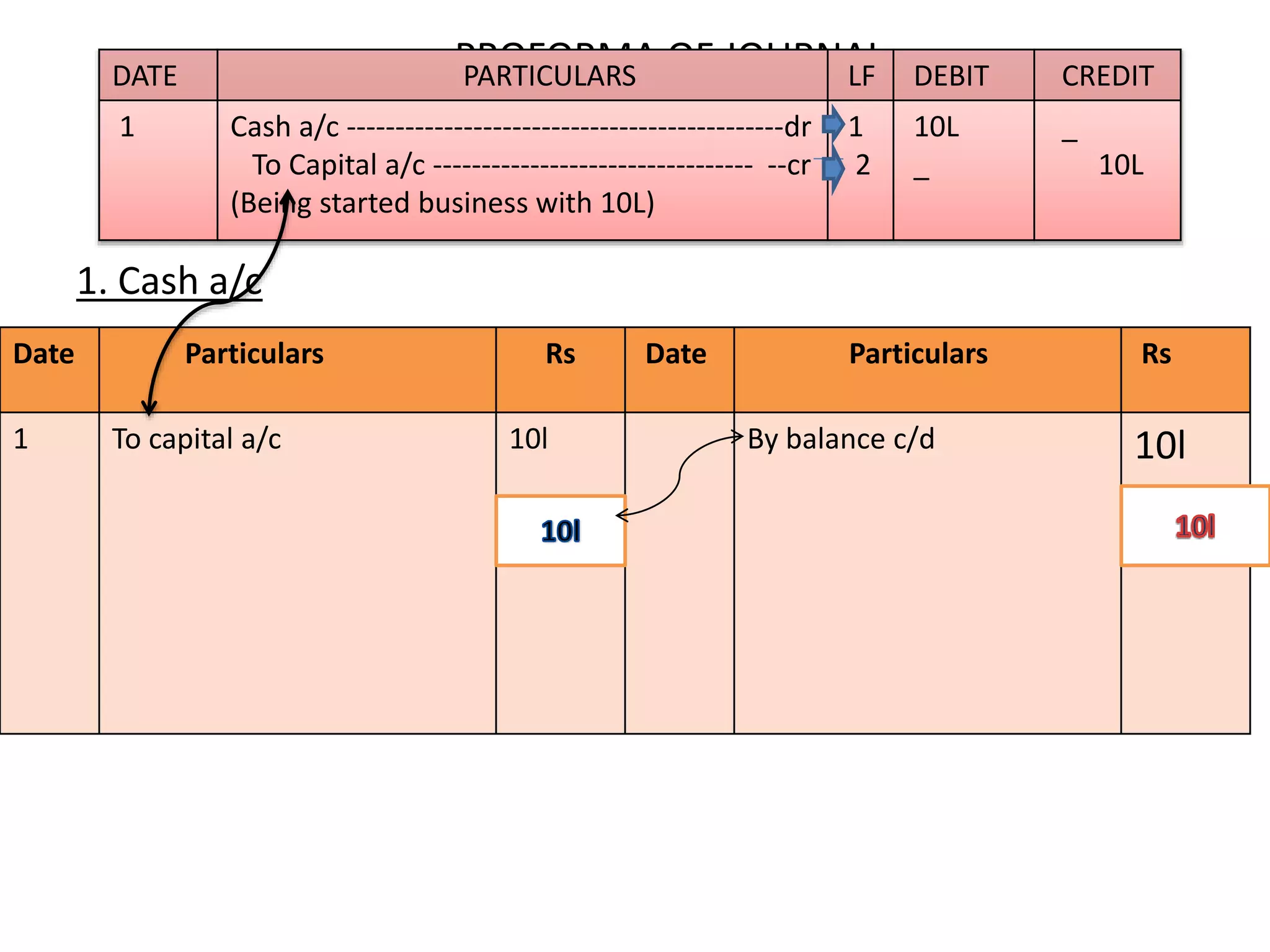

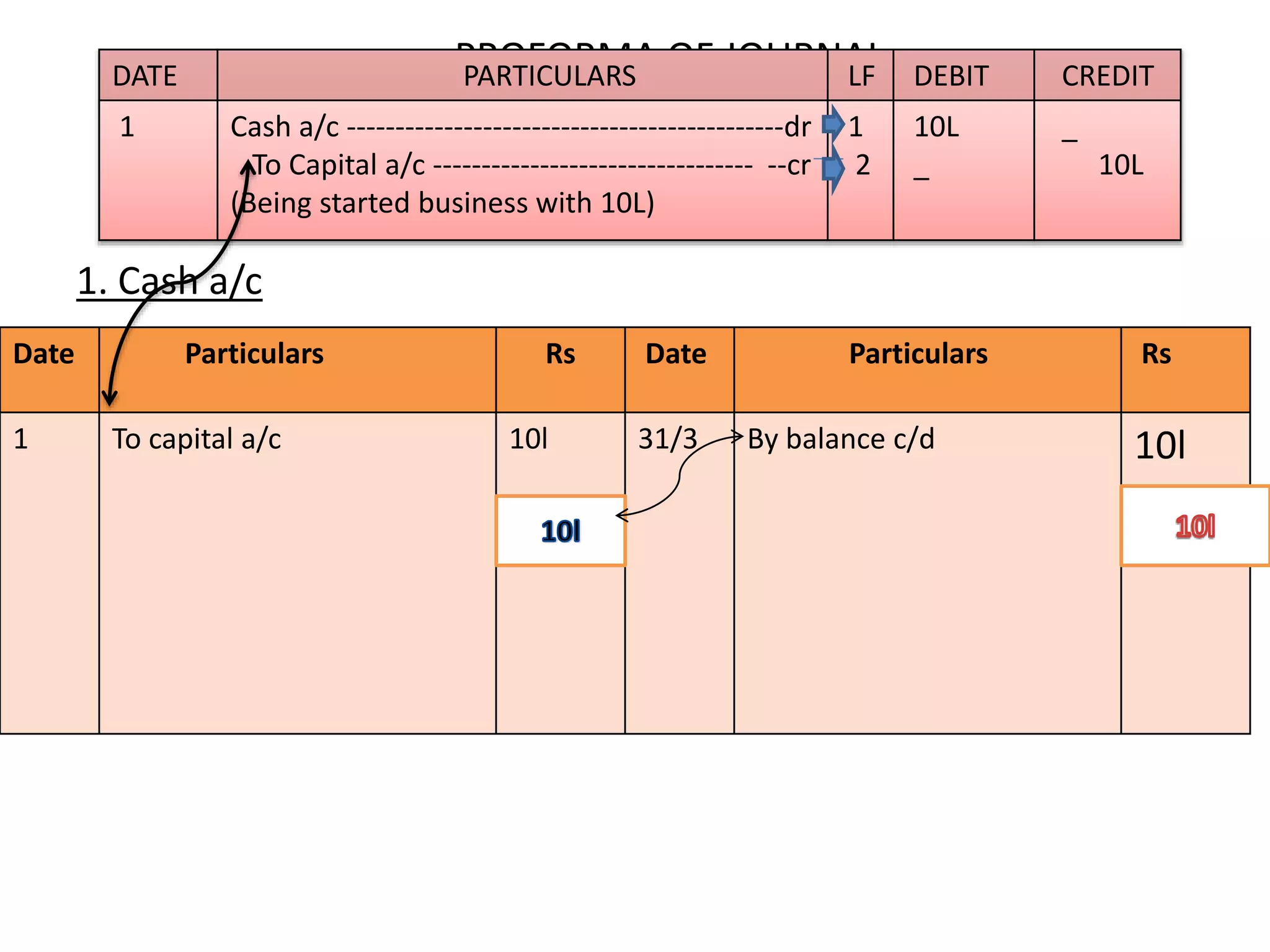

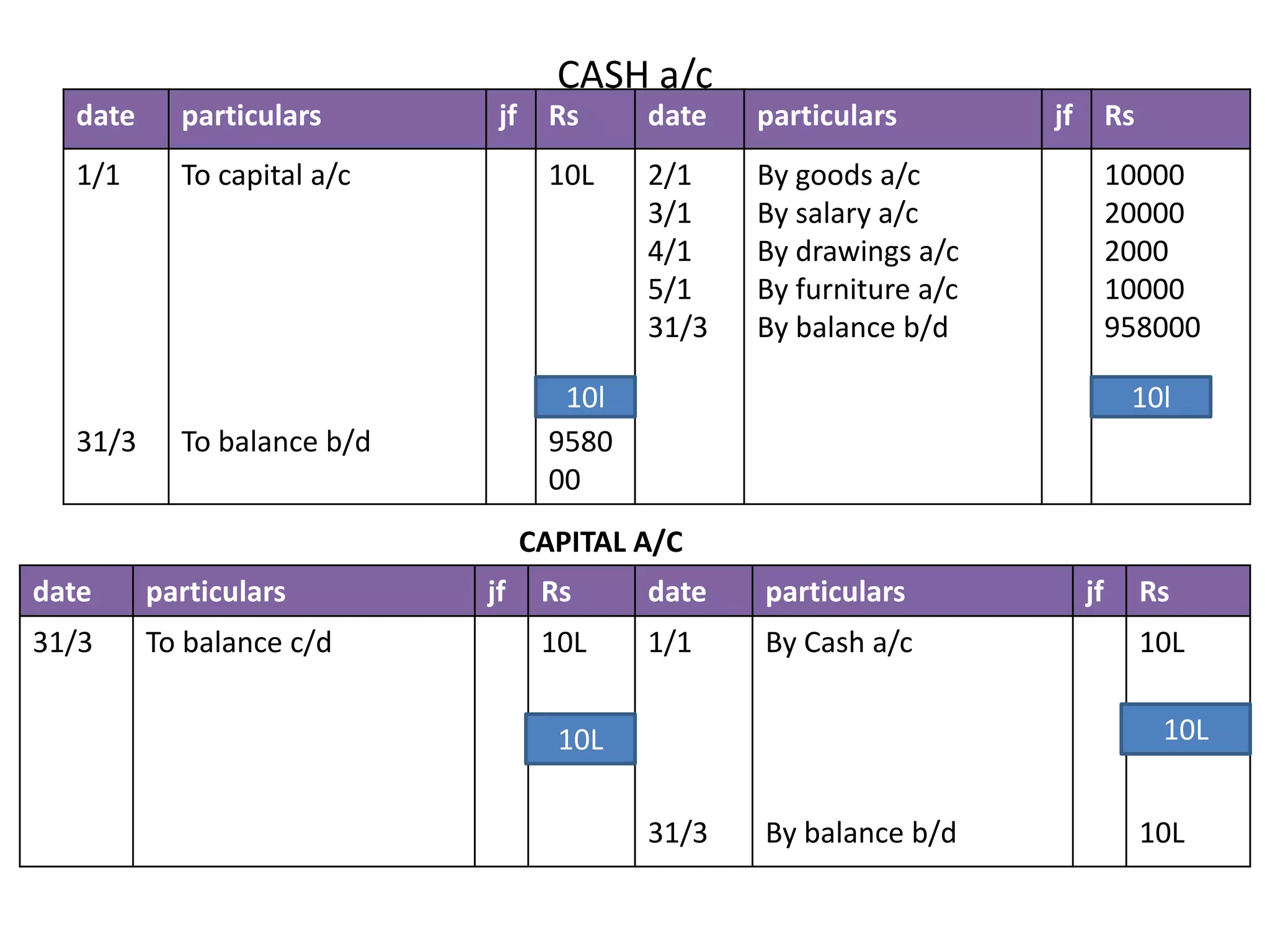

2. Transactions are first recorded in a journal, then posted to the relevant ledger accounts. For example, when Mohan started his business with Rs. 10 lakh cash, the journal entry recorded Cash A/c being debited and Capital A/c being credited.

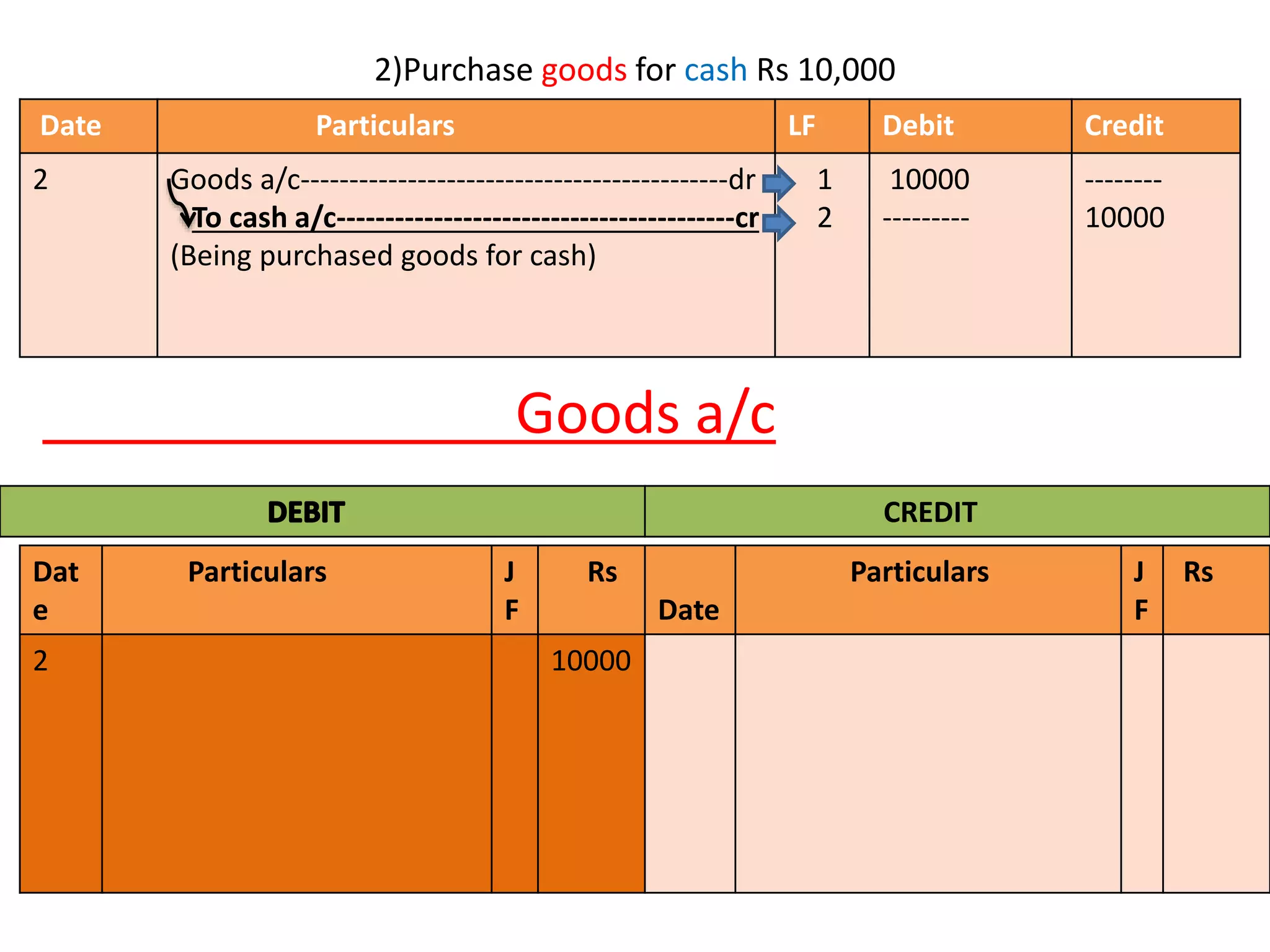

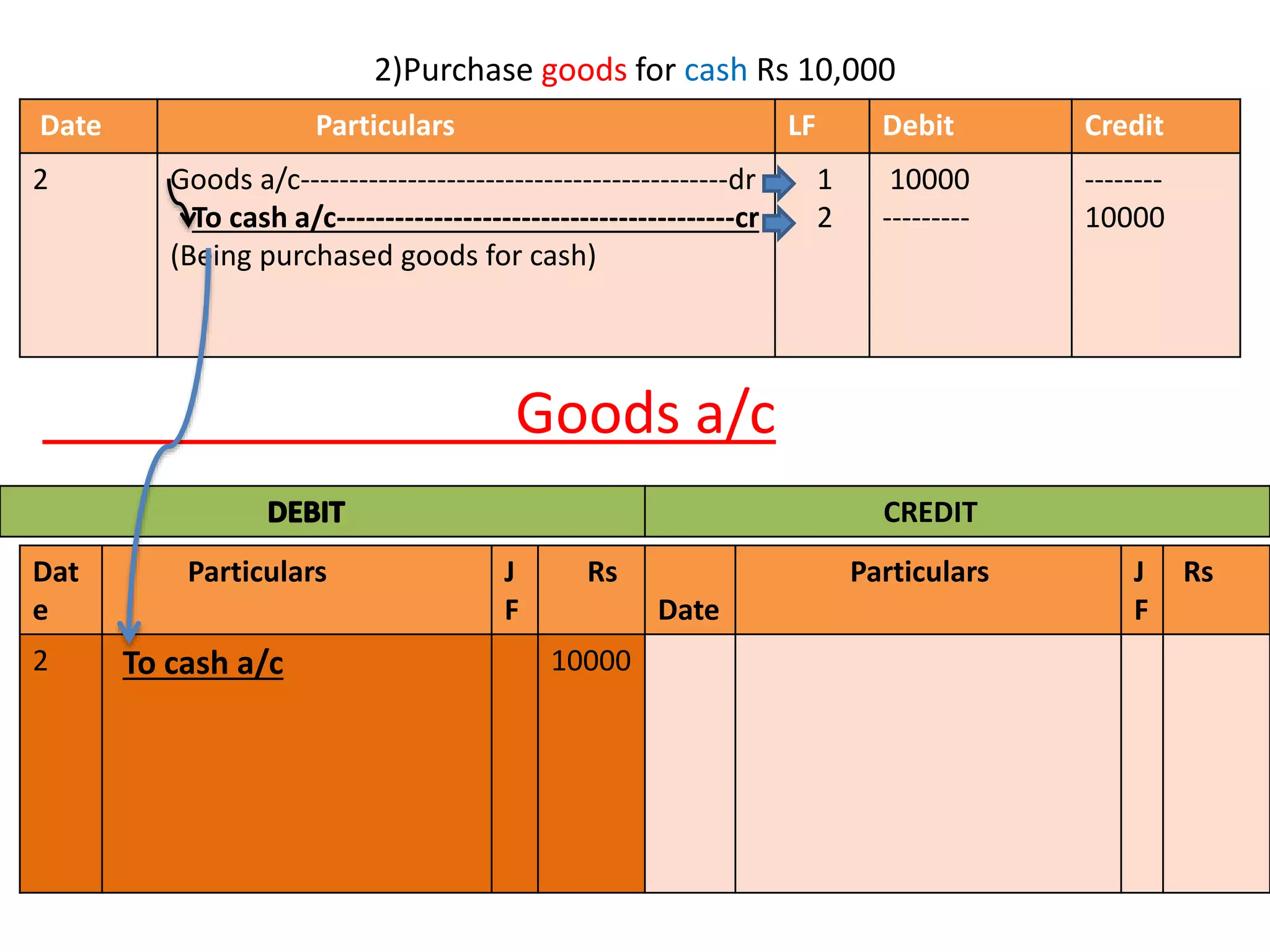

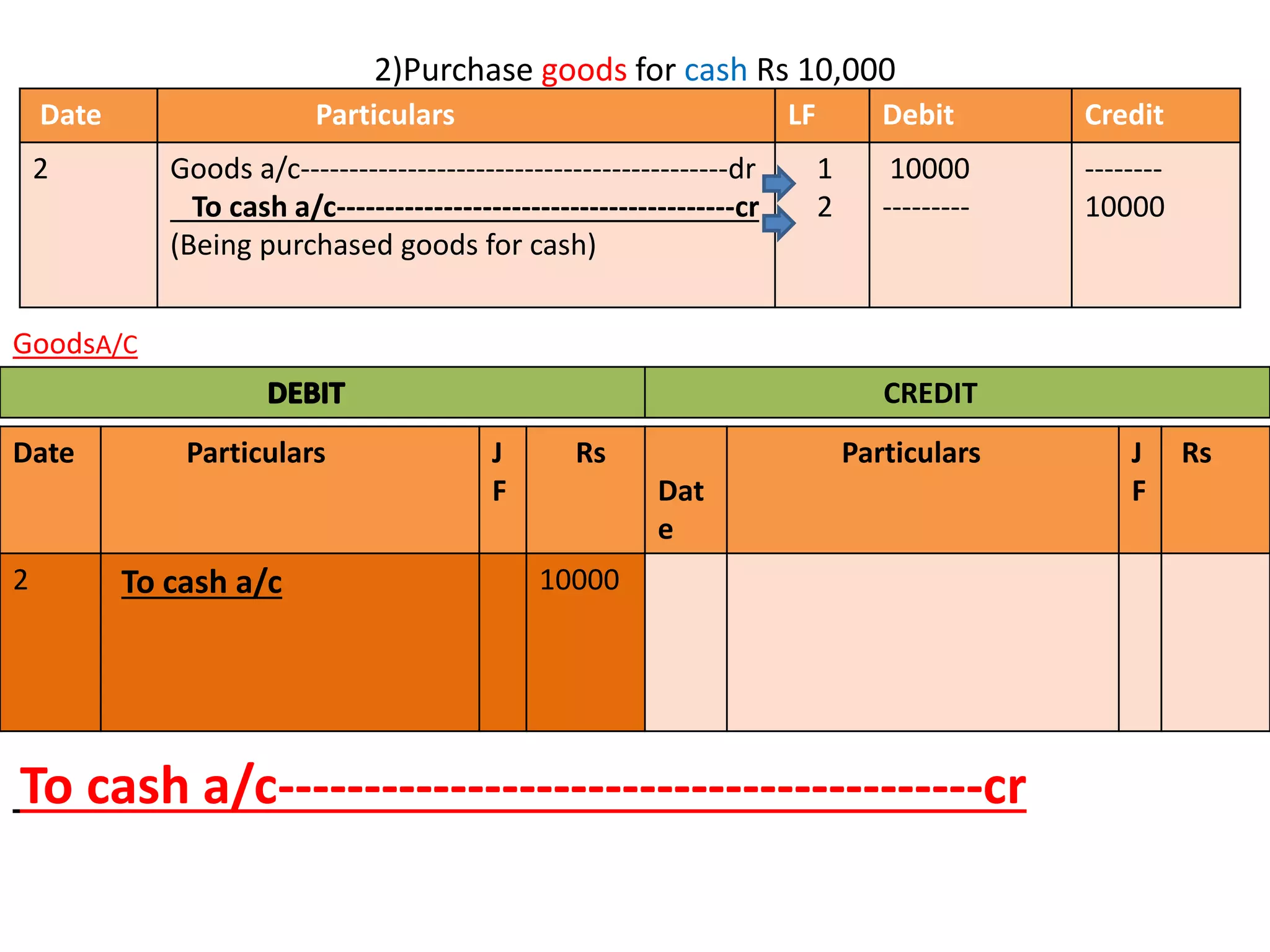

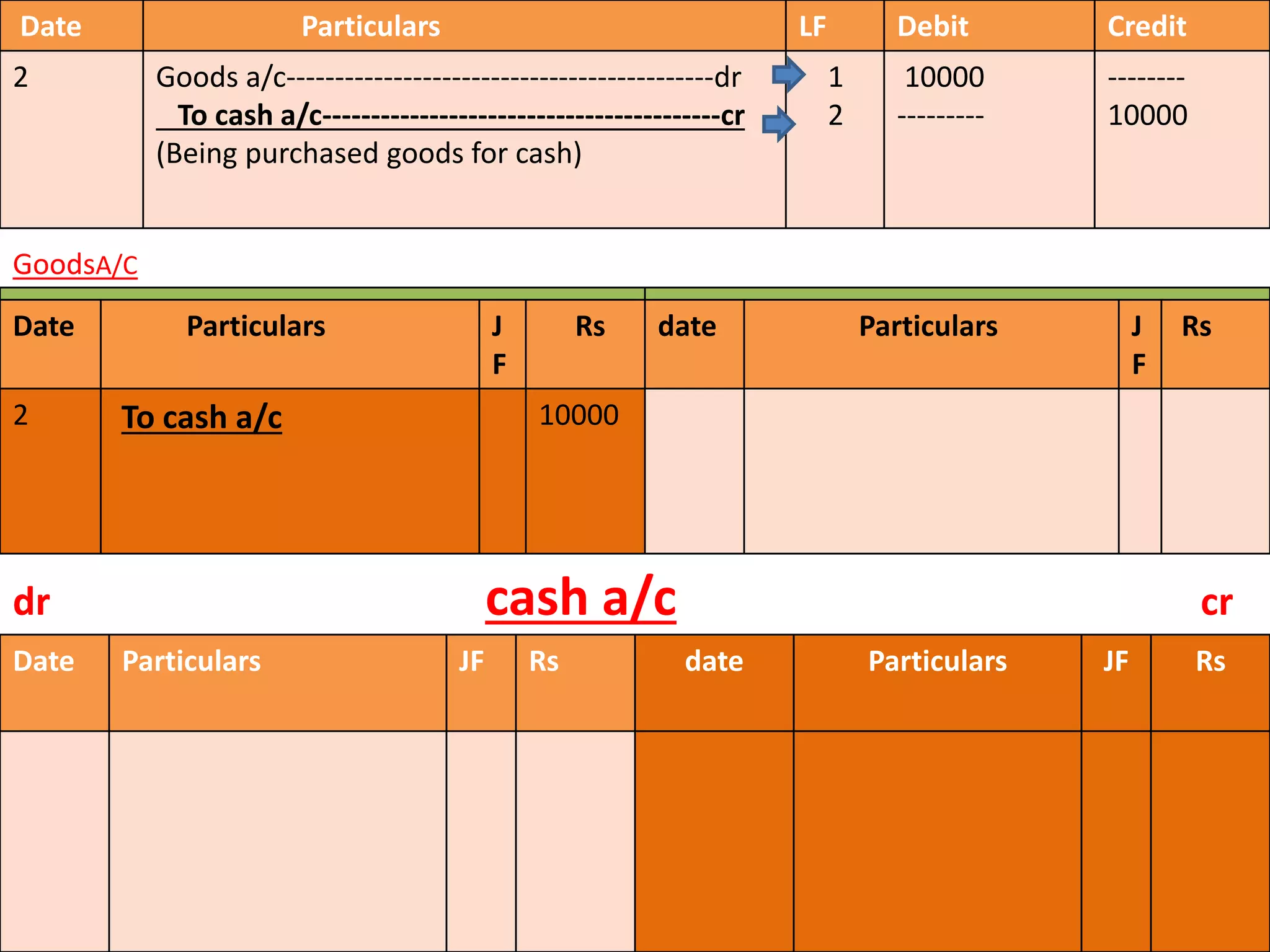

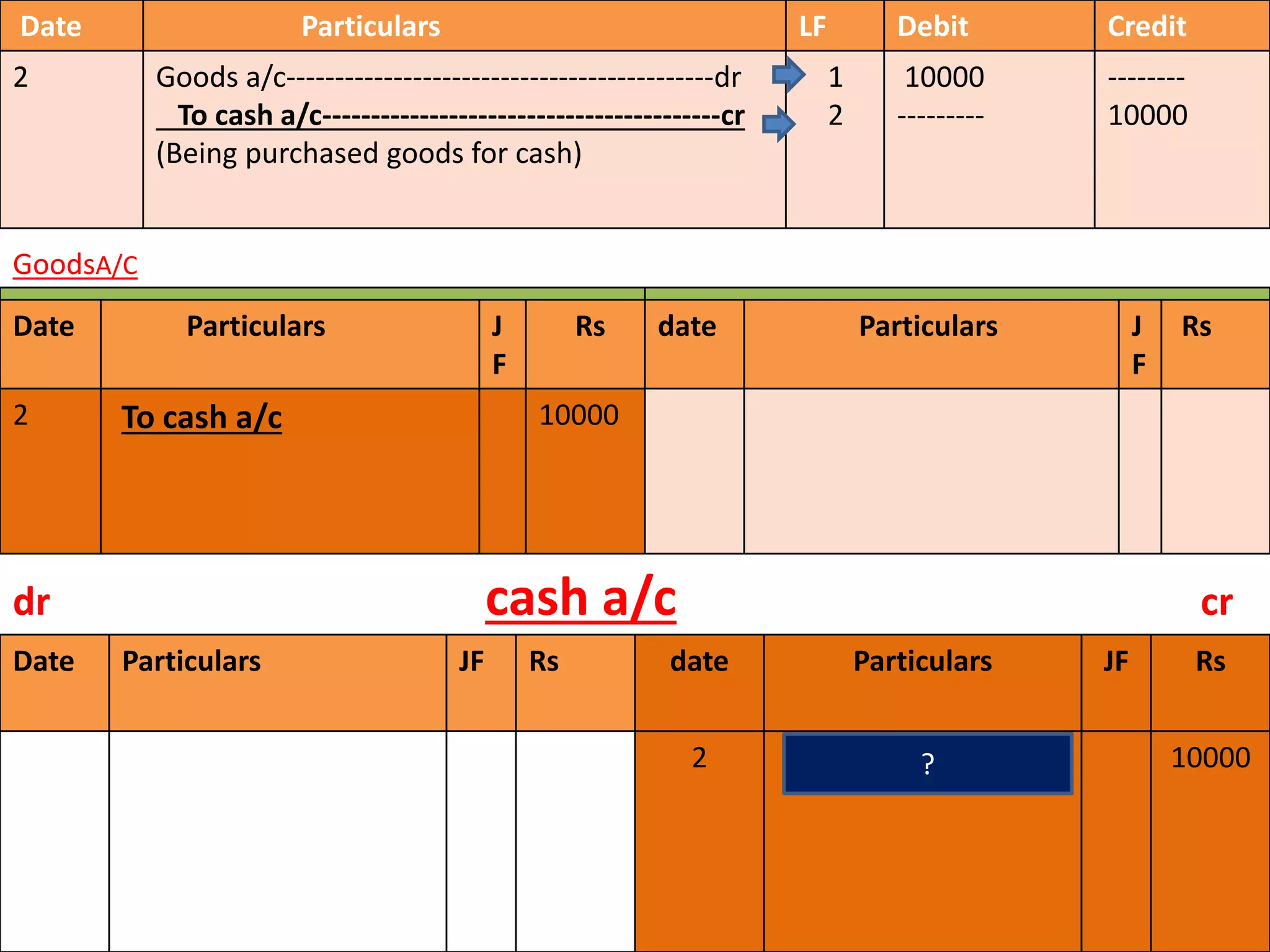

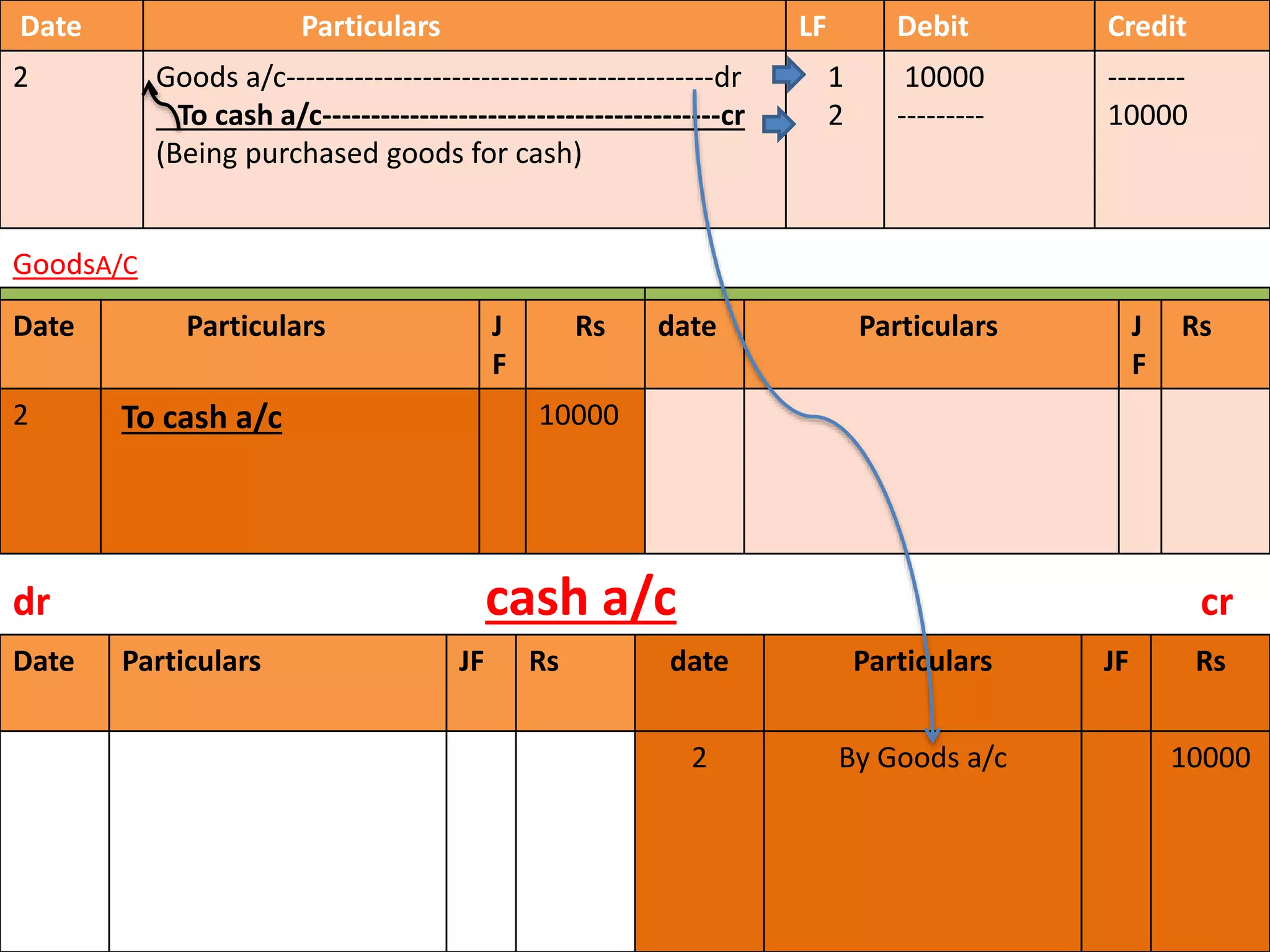

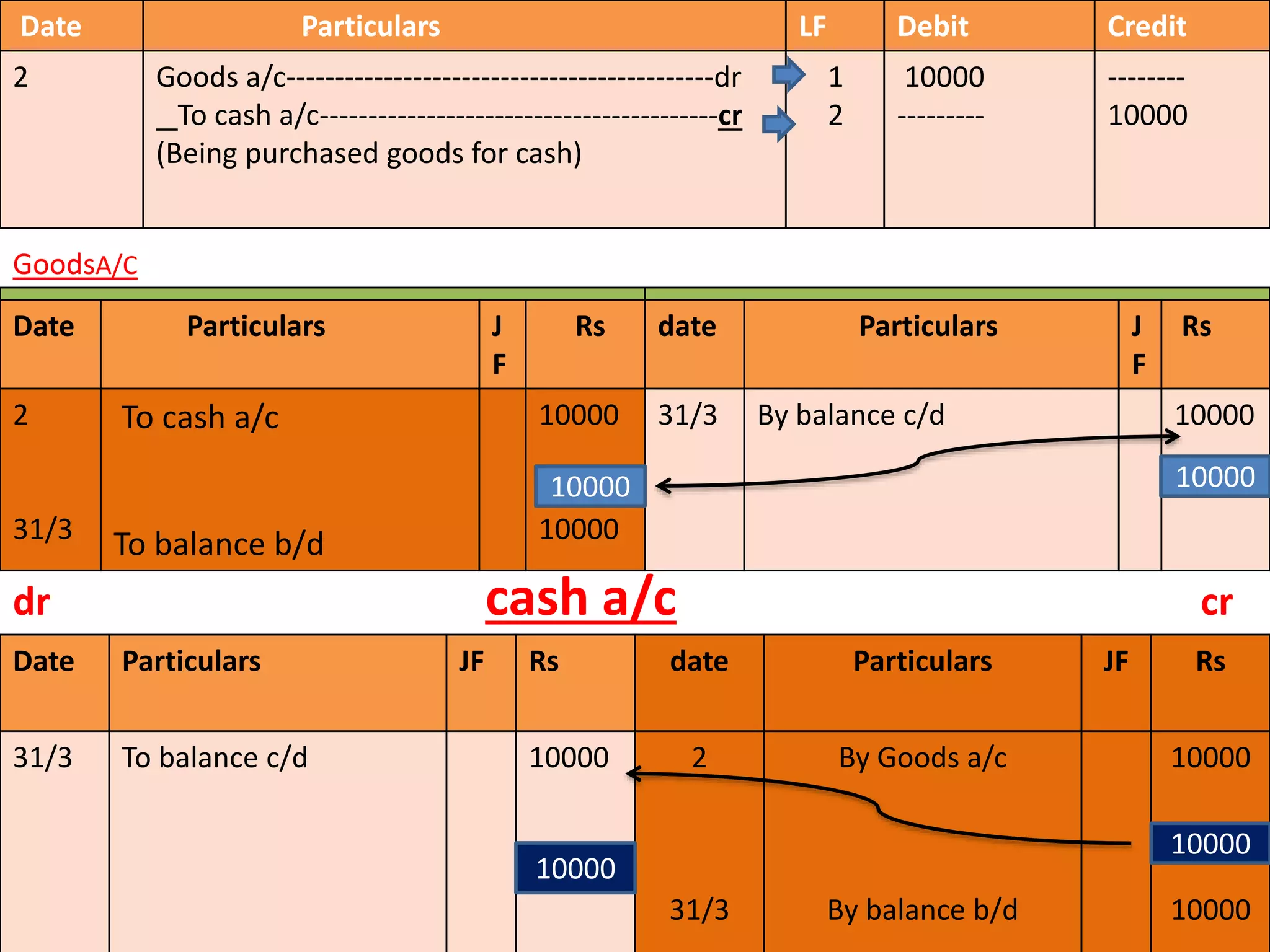

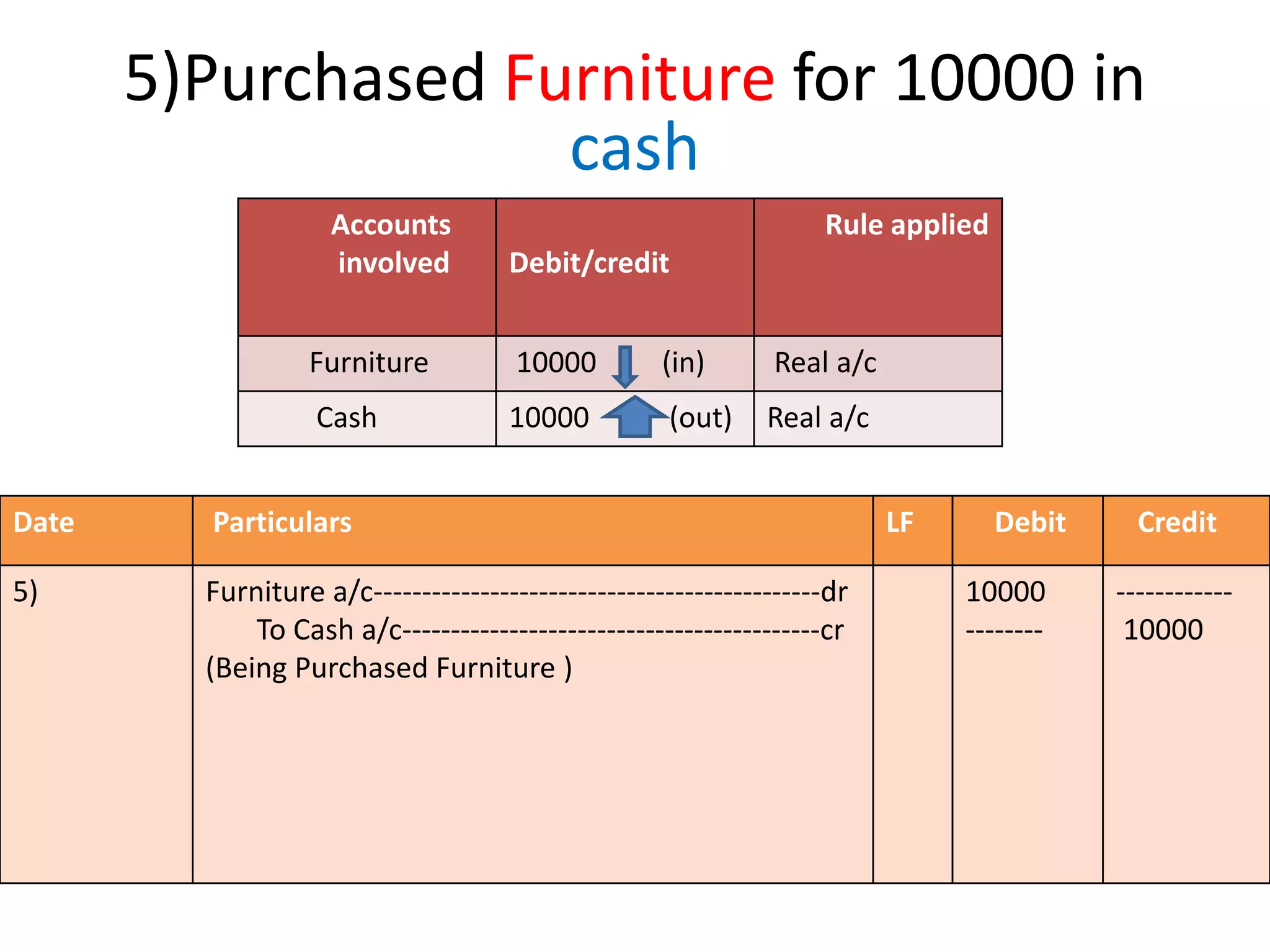

3. The document then provides examples of journal and ledger entries for various business transactions like purchasing goods for cash. It illustrates how transactions are recorded in journals and then posted to the debit and credit sides of the relevant ledger accounts.