3

Definitions

• Book offirst entry

Journal

• Separate record showing

increases and decreases in

a specific assets or liability

Account

•A group of accounts for a business

entity

Ledger

•List of account and their balances at

a given time

Trial balance

4.

Analysis of Business

transaction

singleentry system

Old system of accounting

Single effect

Accounting records are not kept strictly

Only cash and person account maintain

Profit not accurate

Two system of accounting

Double entry conceptof

accounting

Based on a simple concept: each party in a

business transaction will receive something

and give something in return.

* The two sides of a coin

* Receive & Give

* Left versus Right

7.

7

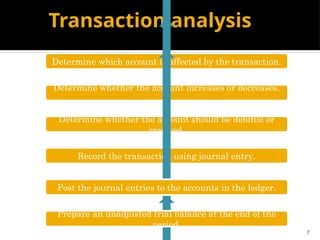

Transaction analysis

Determine whichaccount is affected by the transaction.

Determine whether the account increases or decreases.

Determine whether the account should be debited or

credited.

Record the transaction using journal entry.

Post the journal entries to the accounts in the ledger.

Prepare an unadjusted trial balance at the end of the

period.

Practice example Question

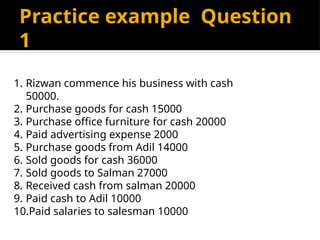

1

1.Rizwan commence his business with cash

50000.

2. Purchase goods for cash 15000

3. Purchase office furniture for cash 20000

4. Paid advertising expense 2000

5. Purchase goods from Adil 14000

6. Sold goods for cash 36000

7. Sold goods to Salman 27000

8. Received cash from salman 20000

9. Paid cash to Adil 10000

10.Paid salaries to salesman 10000

17.

Practice example Question

2

1.Invested 100000 cash, building 75000 and furniture

25000.

2. Purchase goods for cash 44000 subject trade

discount 10%.

3. Purchase goods from Ali 5000

4. Sold goods on account to Zain 8000.

5. Receive cash from Zain 7800, discount allowed 200

6. Paid Ali 4750, discount received 250

7. Goods taken away by the owner 350

8. Paid salaries 1000, Rent 600 and Repairing charges

400

9. Received commission 1500

Journal

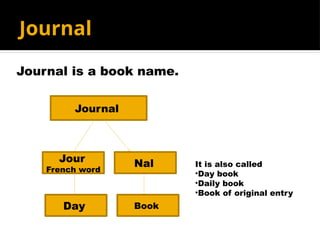

Journal is abook name.

Journal

Jour

French word

Nal

Day Book

It is also called

•Day book

•Daily book

•Book of original entry

20.

20

Journal entries

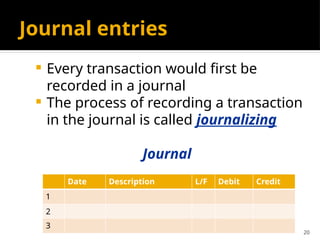

Everytransaction would first be

recorded in a journal

The process of recording a transaction

in the journal is called journalizing

Journal

Date Description L/F Debit Credit

1

2

3

21.

21

Journalizing steps

1. Recordthe date.

2. Record the title of the account debited in

the Description column.

3. Enter the amount in the Debit column.

4. Record the title of the account credited in

the Description column.

5. Enter the amount in the Credit column.

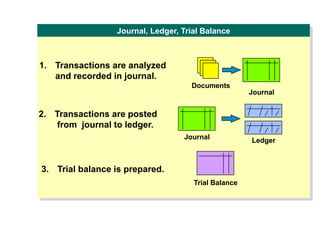

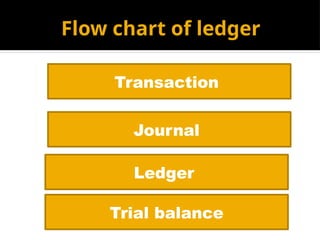

1. Transactions areanalyzed

and recorded in journal.

Documents

Journal

2. Transactions are posted

from journal to ledger.

Journal Ledger

3. Trial balance is prepared.

Journal, Ledger, Trial Balance

Trial Balance

30.

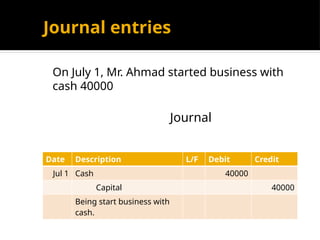

Journal entries

On July1, Mr. Ahmad started business with

cash 40000

Journal

Date Description L/F Debit Credit

Jul 1 Cash 40000

Capital 40000

Being start business with

cash.

31.

On July 5,Mr. Ahmad bought a piece of

land for Rupees 200,000 by paying cash.

Date Description PR Debit Credit

Nov 5 Land 200,000

Cash 200,000

Purchased land for

cash.

Dr Cr

Land Dr Cr

Cash

Jul 5 Land 200,000 Jul 5 Cash 200,000

32.

July10, Mr. Ahmadpurchased goods

on account for Rupees 13,500.

Date Description l/F Debit Credit

Jul10 Purchases 13,500

Accounts Payable 13,500

Purchased goods on

account.

Dr Cr

Purchases Dr Cr

A/C Payable

Jul 10 A/C Pay 13,500 Jul 10 Supplies 13,500

33.

July 30, Mr.Ahmad paid to creditors

Rs.9,500.

Date Description PR Debit Credit

Jul 30 Accounts Payable 9,500

Cash 9,500

Paid creditors.

Dr Cr

A/C Payable Dr Cr

Cash

Jul 30 Cash 9,500 Jul 30 A/C Pay 9,500

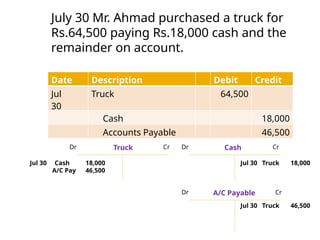

34.

July 30 Mr.Ahmad purchased a truck for

Rs.64,500 paying Rs.18,000 cash and the

remainder on account.

Date Description Debit Credit

Jul

30

Truck 64,500

Cash 18,000

Accounts Payable 46,500

Dr Cr

Truck Dr Cr

A/C Payable

Jul 30 Cash 18,000

A/C Pay 46,500

Jul 30 Truck 18,000

Dr Cr

Cash

Jul 30 Truck 46,500

35.

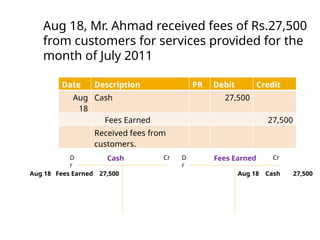

Aug 18, Mr.Ahmad received fees of Rs.27,500

from customers for services provided for the

month of July 2011

Date Description PR Debit Credit

Aug

18

Cash 27,500

Fees Earned 27,500

Received fees from

customers.

D

r

Cr Fees Earned

D

r

Cr

Cash

Aug 18 Fees Earned 27,500 Aug 18 Cash 27,500

36.

Aug 30 incurredthe following expenses:

wages Rs.20,500; and rent Rs3,000 paid by

cash.

Date Description PR Debit Credit

Aug

30

Wages account 20,500

cash account 20,500

Aug

30

Rent account 3,000

Cash account 3,000

D

r

Cr Wages Payable

D

r

Cr

Wages Exp

Aug 30 Wages Pay 20,500 Aug 30 Wages Exp

20,500

D

r

Cr Cash

D

r

Cr

Rent Exp

Aug 30 Cash 3,000 Aug 30 Rent Exp 3,000

37.

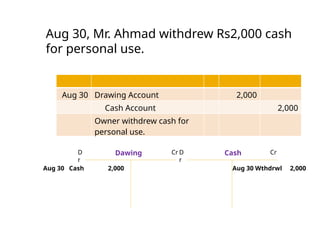

Aug 30, Mr.Ahmad withdrew Rs2,000 cash

for personal use.

Aug 30 Drawing Account 2,000

Cash Account 2,000

Owner withdrew cash for

personal use.

D

r

Cr Cash

D

r

Cr

Dawing

Aug 30 Cash 2,000 Aug 30 Wthdrwl 2,000

38.

Problem No. 2

Introduce cash 148000 and building

20000 as capital.

Purchase goods on account 100000

Purchase Motor vehicle from saleem auto

150000

Sold goods to Imran at list price trade

discount 5% Rs. 5000.

Paid travelling allowance 1000

39.

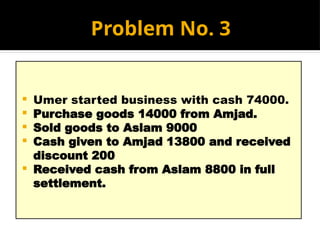

Problem No. 3

Umer started business with cash 74000.

Purchase goods 14000 from Amjad.

Sold goods to Aslam 9000

Cash given to Amjad 13800 and received

discount 200

Received cash from Aslam 8800 in full

settlement.

40.

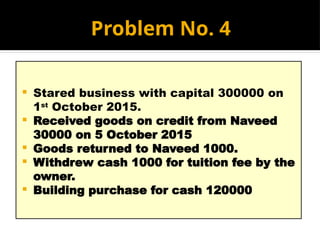

Problem No. 4

Stared business with capital 300000 on

1st

October 2015.

Received goods on credit from Naveed

30000 on 5 October 2015

Goods returned to Naveed 1000.

Withdrew cash 1000 for tuition fee by the

owner.

Building purchase for cash 120000

41.

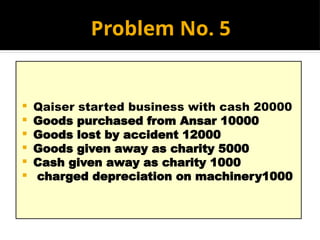

Problem No. 5

Qaiser started business with cash 20000

Goods purchased from Ansar 10000

Goods lost by accident 12000

Goods given away as charity 5000

Cash given away as charity 1000

charged depreciation on machinery1000

42.

Problem No. 7

Started business with cash 60000

Deposit cash into bank 400000

Goods bought by cheque 150000

Purchased goods for cash 10000 and on

credit 5000 from Ali.

Sold goods for cash 12000 and on account

6000 to Aslam.

Ali’s account settled by receiving 200 as

discount

Aslam’s account settled by allowing 200 as

discount

43.

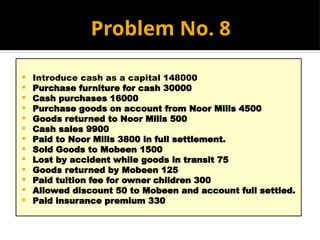

Problem No. 8

Introduce cash as a capital 148000

Purchase furniture for cash 30000

Cash purchases 16000

Purchase goods on account from Noor Mills 4500

Goods returned to Noor Mills 500

Cash sales 9900

Paid to Noor Mills 3800 in full settlement.

Sold Goods to Mobeen 1500

Lost by accident while goods in transit 75

Goods returned by Mobeen 125

Paid tuition fee for owner children 300

Allowed discount 50 to Mobeen and account full settled.

Paid insurance premium 330

44.

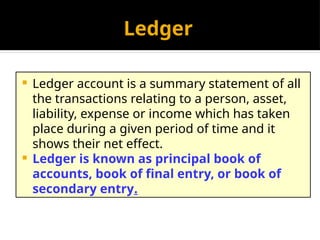

Ledger

Ledger accountis a summary statement of all

the transactions relating to a person, asset,

liability, expense or income which has taken

place during a given period of time and it

shows their net effect.

Ledger is known as principal book of

accounts, book of final entry, or book of

secondary entry.

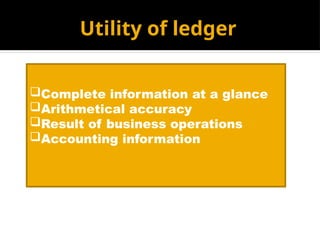

Utility of ledger

Completeinformation at a glance

Arithmetical accuracy

Result of business operations

Accounting information

47.

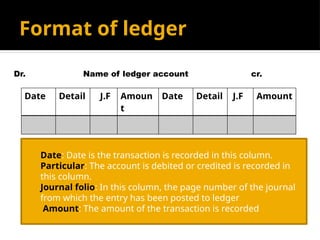

Format of ledger

Date:Date is the transaction is recorded in this column.

Particular: The account is debited or credited is recorded in

this column.

Journal folio: In this column, the page number of the journal

from which the entry has been posted to ledger

Amount: The amount of the transaction is recorded

Date Detail J.F Amoun

t

Date Detail J.F Amount

Name of ledger account

Dr. cr.

48.

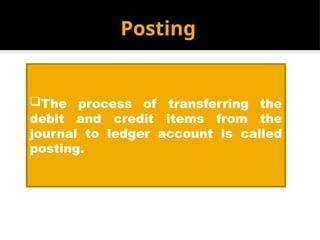

Posting

The process oftransferring the

debit and credit items from the

journal to ledger account is called

posting.

49.

Balancing of ledger

Balancingis the difference between

the total debits and the total credit of

an account.

When the posting is done, many accounts may have entries on

their debit side as well as credit side. The net result of such

debits and credits is an account is the balance.

Balancing means the writing of the difference between of the

two sides in the lighter (smaller total) side, so that the grand

total of two sides become equal.

50.

Significance of balancing

Thereare three possibilities while

balancing an account duing a given

period. It may be a debit balance or

credit balance or a nil balance

depending upon the debit total and

the credit total

51.

Trial balance

Atrial balance is a report that lists the

balances of all general ledge account of

a company at a certain point of time.

52.

Objective of trialbalance

To establish arithmetical accuracy of

books

To provide a base for preparation of

financial statements.

To summaries the ledger account.

53.

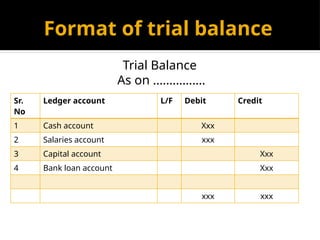

Format of trialbalance

Sr.

No

Ledger account L/F Debit Credit

1 Cash account Xxx

2 Salaries account xxx

3 Capital account Xxx

4 Bank loan account Xxx

xxx xxx

Trial Balance

As on …………….

54.

Format of trialbalance

Sr.

No

Ledger account L/F Debit Credit

1 Cash account Xxx

2 Salaries account xxx

3 Capital account Xxx

4 Bank loan account Xxx

xxx xxx

Trial Balance

As on …………….