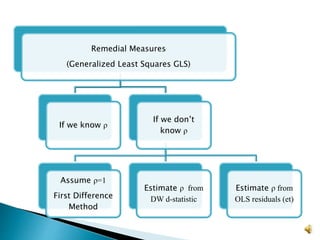

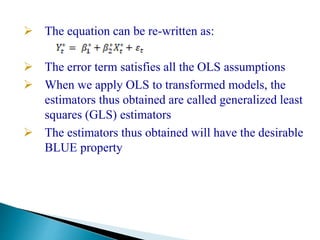

This document discusses remedies for autocorrelation in regression analysis. There are three main methods:

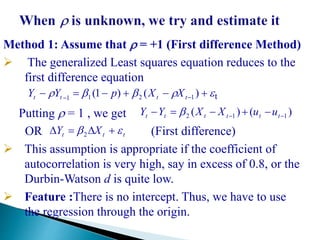

1. Assume ρ=1 and use first differencing to remove the autocorrelation.

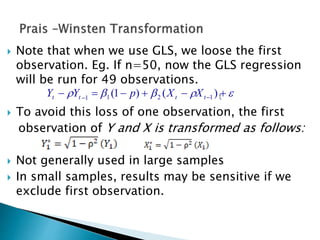

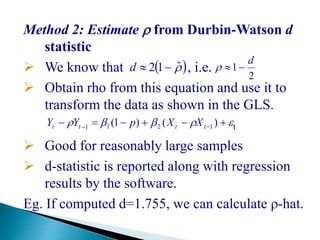

2. Estimate ρ from the Durbin-Watson statistic and use it to transform the data in the generalized least squares (GLS) model.

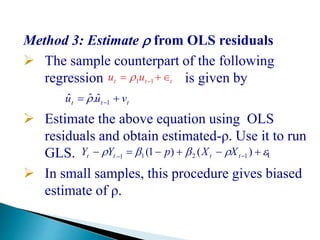

3. Estimate ρ from the OLS residuals and use it to run GLS, though this may be biased in small samples.

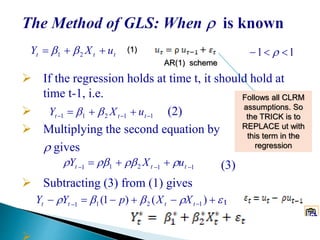

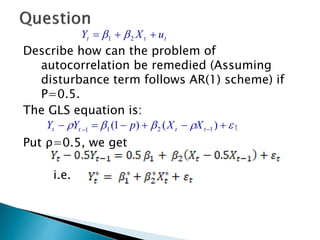

The document also provides an example of applying GLS if the autocorrelation coefficient ρ is estimated to be 0.5.