Download as PDF, PPTX

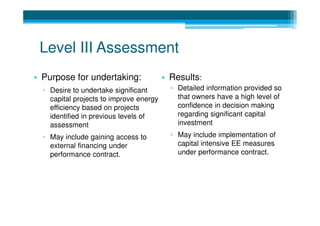

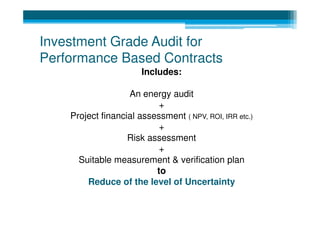

An investment grade audit provides a more detailed analysis than a typical energy audit by evaluating the technical and economic feasibility of potential energy efficiency projects. It establishes an energy baseline, identifies energy saving opportunities, and provides detailed cost-benefit analyses to help customers determine which projects to implement. The audit results can then be used to negotiate a performance-based contract to design, install, commission and monitor the recommended projects over time through measurement and verification of energy savings.