Downloaded 36 times

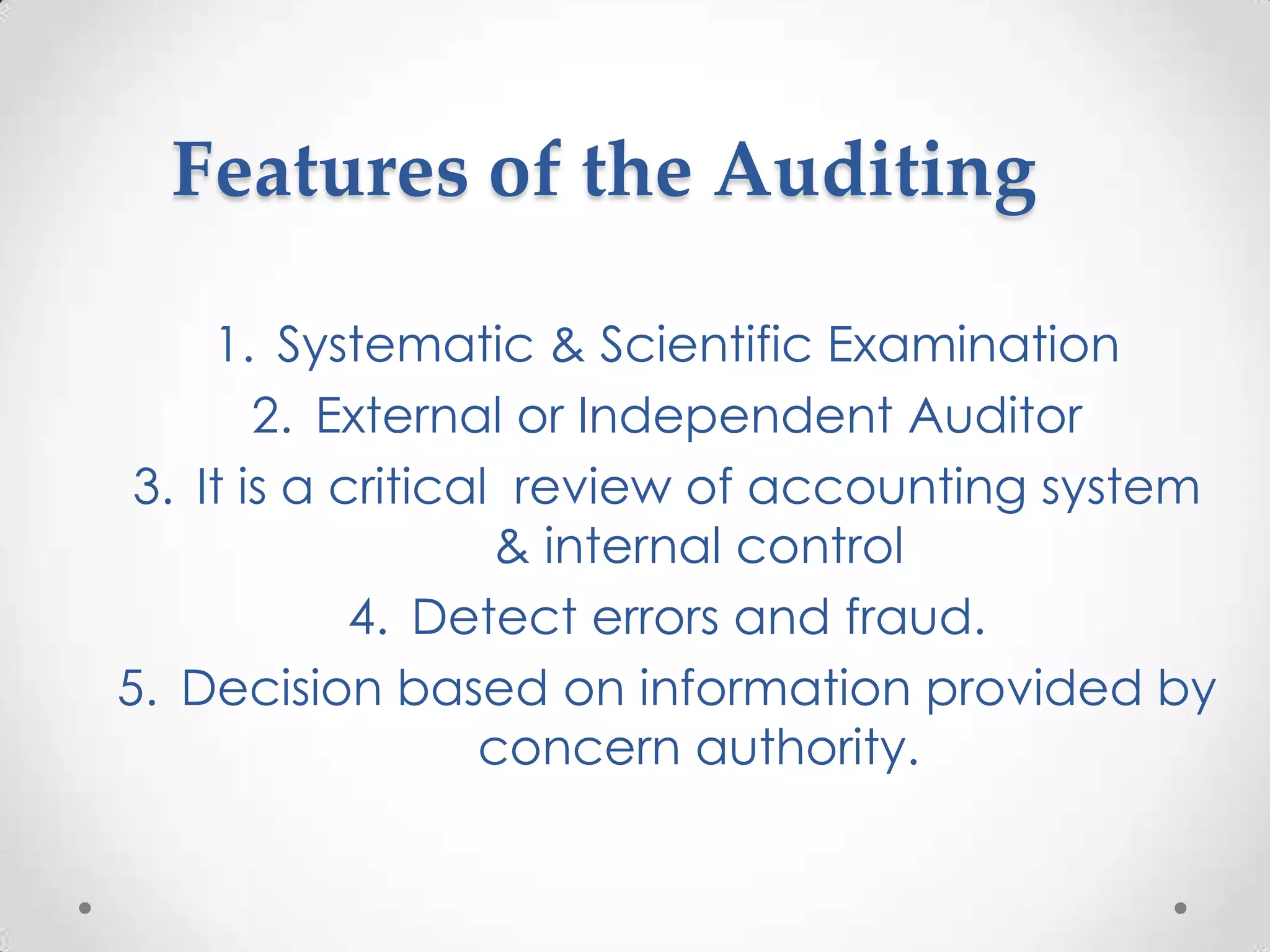

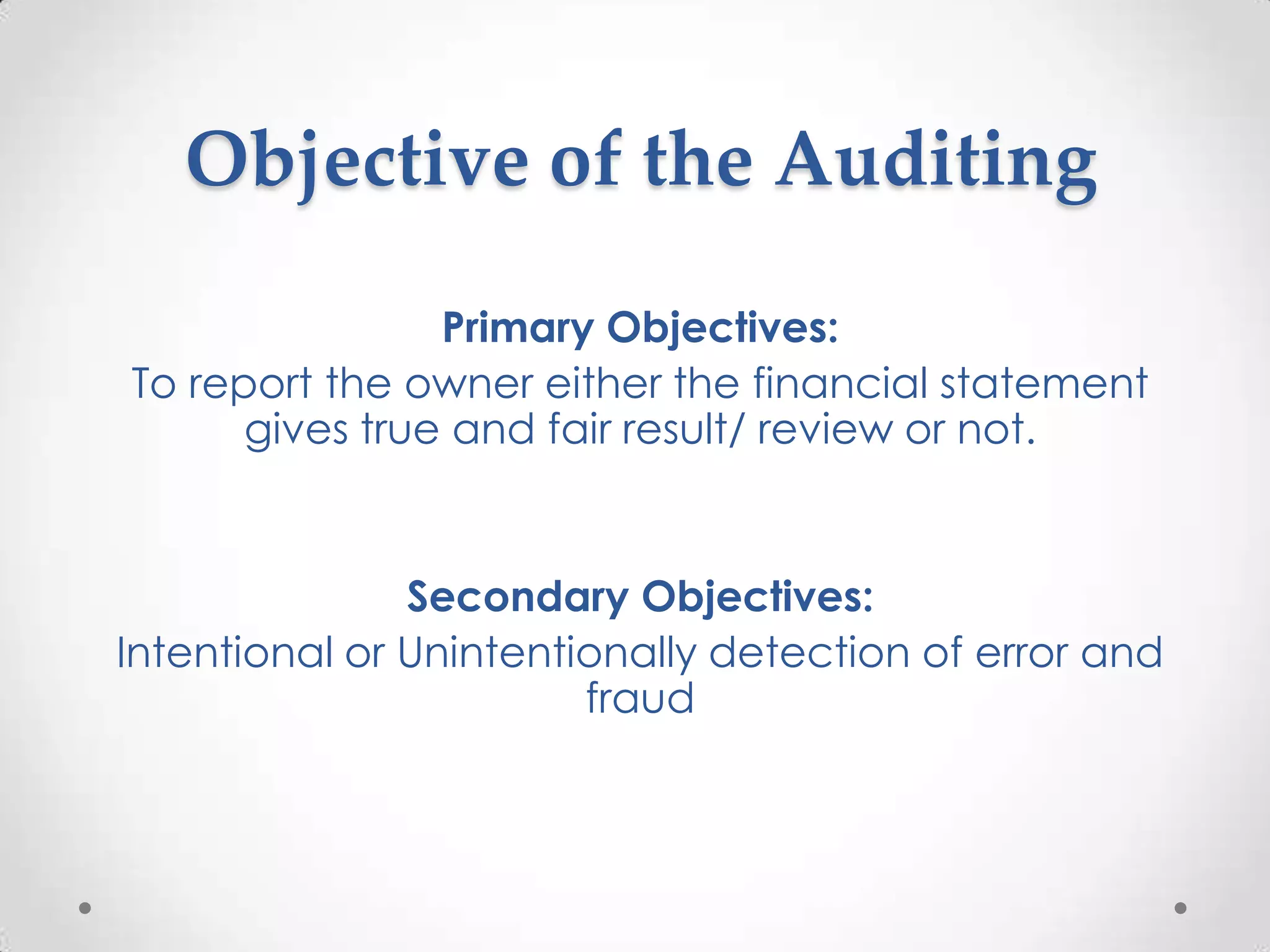

The document provides an overview of auditing, including its history and objectives. Auditing originated from the Latin word "audire," meaning to hear, and its early objectives were to detect errors and fraud. An audit involves examining books, accounts, and business vouchers to determine if they provide a true and fair view of the company. Key features of auditing are that it is a systematic, scientific examination conducted by an external and independent auditor to critically review accounting systems and internal controls, and detect errors and fraud. The primary objective of an audit is for the auditor to report whether the financial statements present a true and fair view or are in accordance with generally accepted accounting principles.