![v Methodware Diagnostic Audit Software Tools Ø Audit Ranking Advisor Risk based Audit Planning Tool where Risk Assessment Criteria is pre-defined Ø Management Advisor Application of COSO Internal Control Frame Work – [Internationally recognized Control parameters] to all the Business Processes Deployment of Automated Audit Management tools for effective functioning](https://image.slidesharecdn.com/3a5Valueaddinginternalaudit-122547729366-phpapp01/75/3a-5-Value-Adding-Internal-Audit-61-2048.jpg)

![ Pro Audit Advisor Risk based Audit Execution based on COSO [Reports on Internal Controls and Governing Processes] and Cadbury Report with automated working papers Ø COBIT Advisor Evaluation of IT processes against the COBIT Frame work. [Control objectives under IT environment] Ø Risk Advisor Capturing Risk Management Standards and developing centralized Risk Register Deployment of Automated Audit Management tools for effective functioning](https://image.slidesharecdn.com/3a5Valueaddinginternalaudit-122547729366-phpapp01/75/3a-5-Value-Adding-Internal-Audit-62-2048.jpg)

![Successful IA Team Effective Communication Appropriate Skill sourcing / Competency Resource Centre [ Knowledge Management System ]](https://image.slidesharecdn.com/3a5Valueaddinginternalaudit-122547729366-phpapp01/75/3a-5-Value-Adding-Internal-Audit-68-2048.jpg)

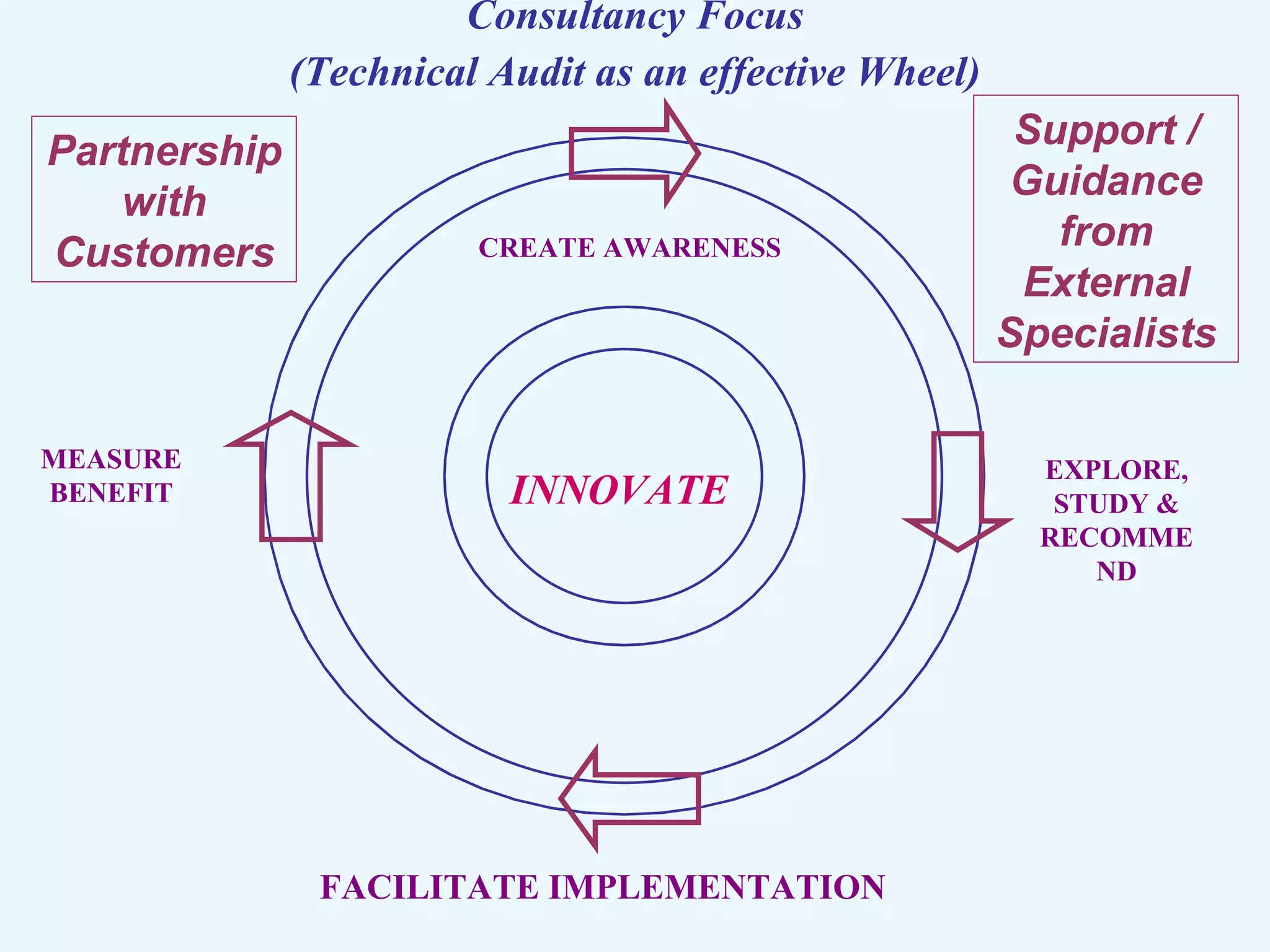

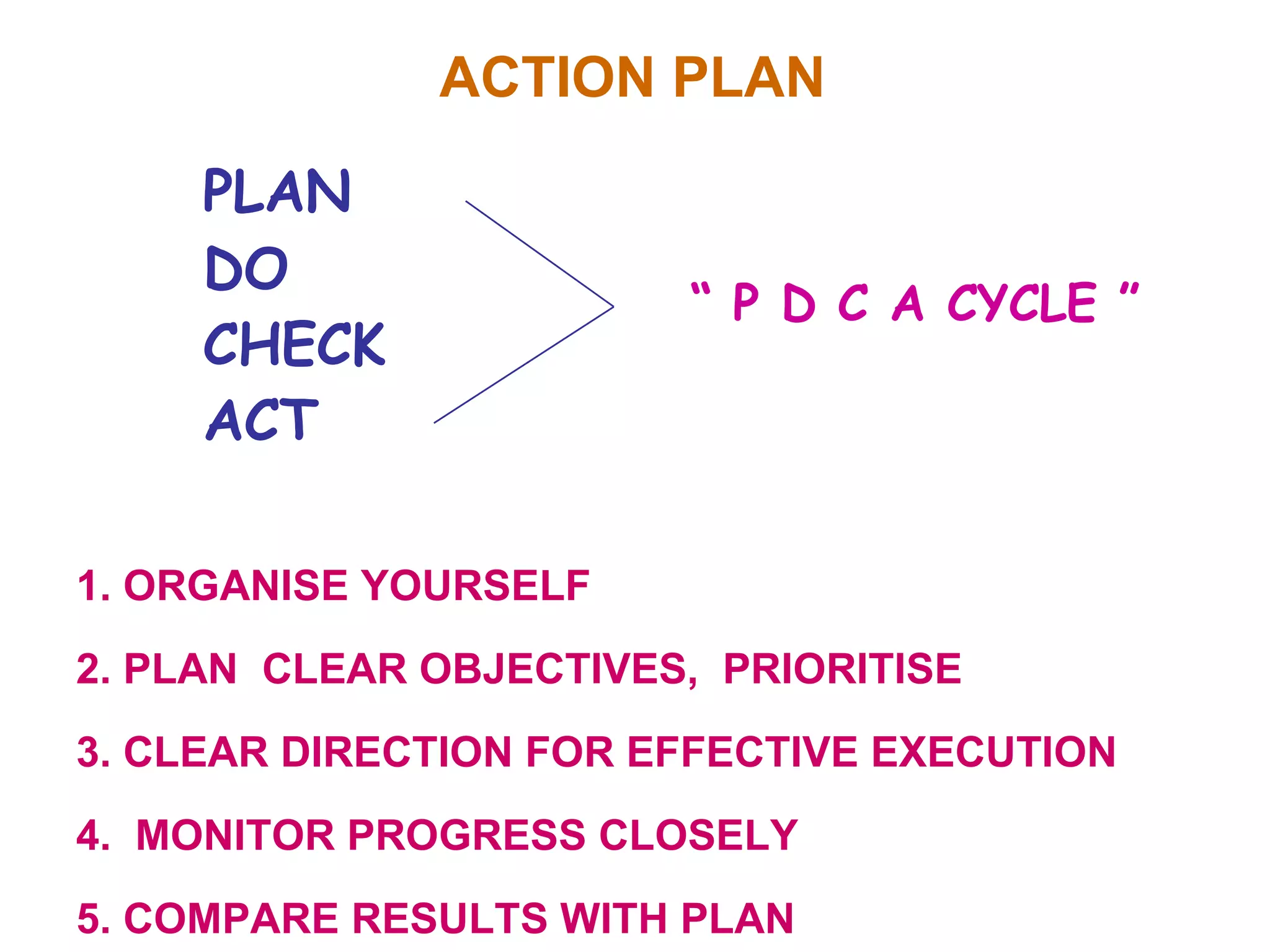

The document outlines the evolving role of internal auditing in enhancing organizational operations through value addition and effective risk management practices. It emphasizes the importance of continuous improvement, professional standards, and collaboration with management to achieve operational excellence, efficiency, and compliance. Additionally, the document highlights the challenges faced by internal audit functions and the need for a proactive, consultative approach to fulfill their objectives effectively.