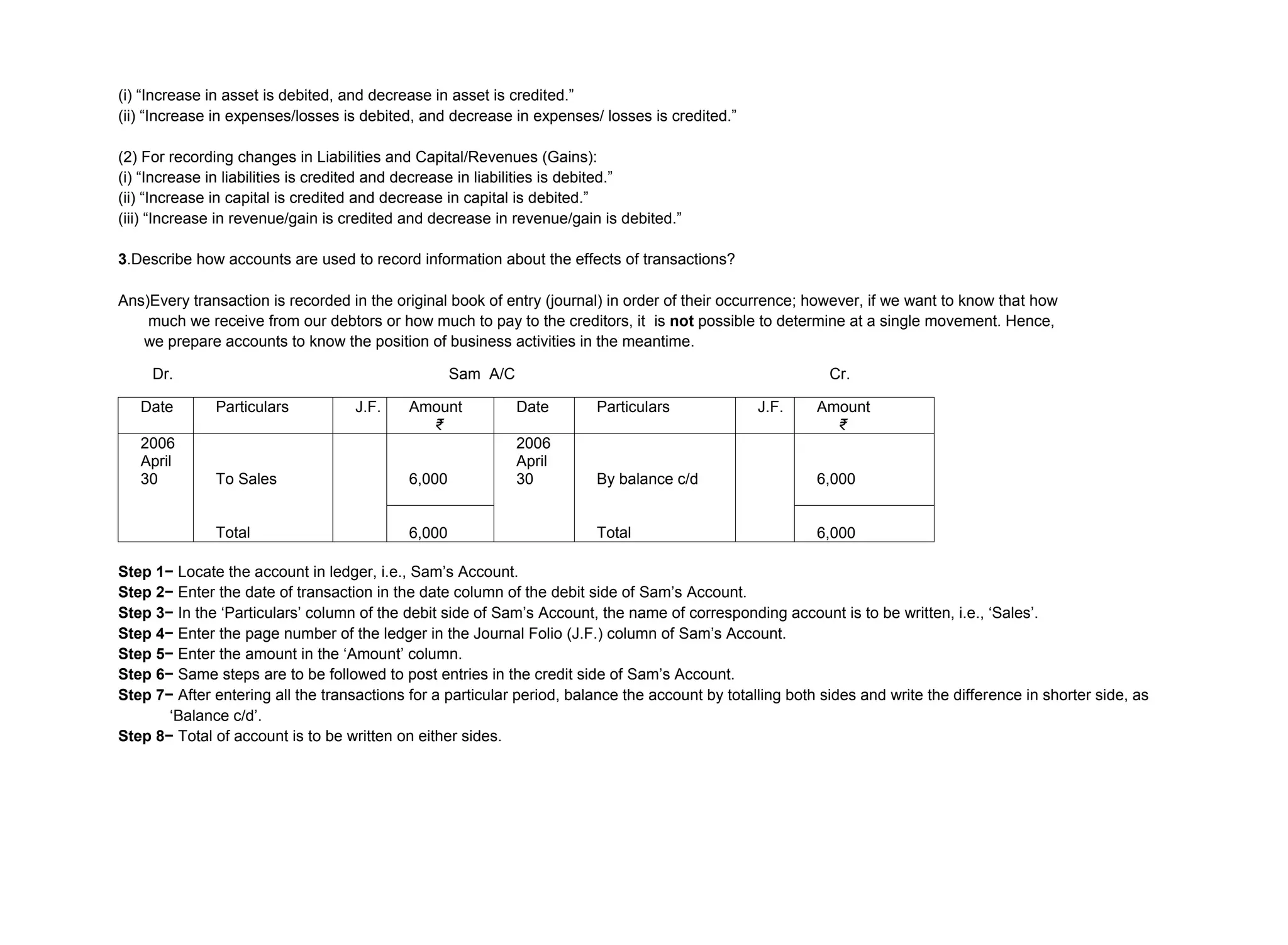

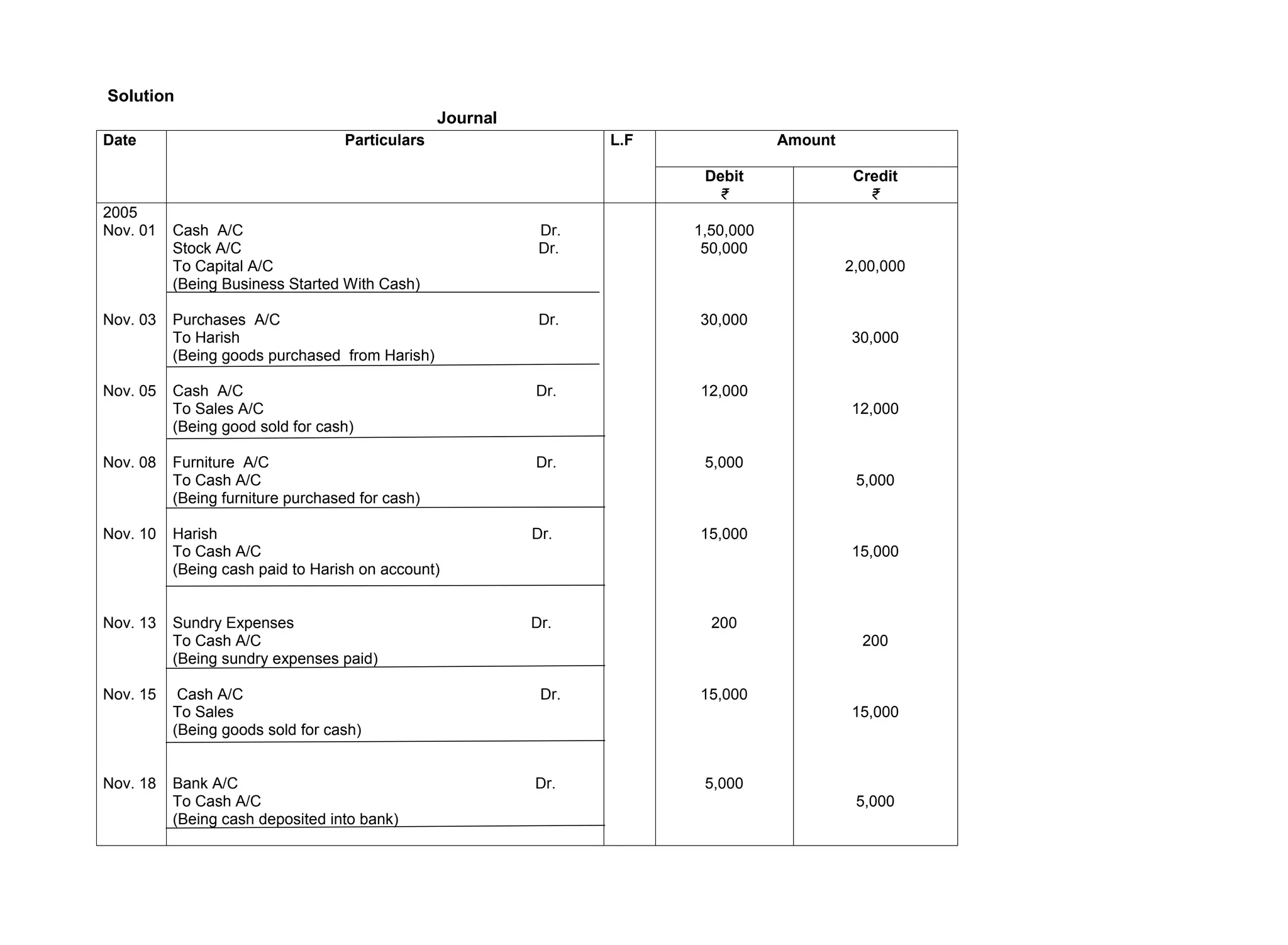

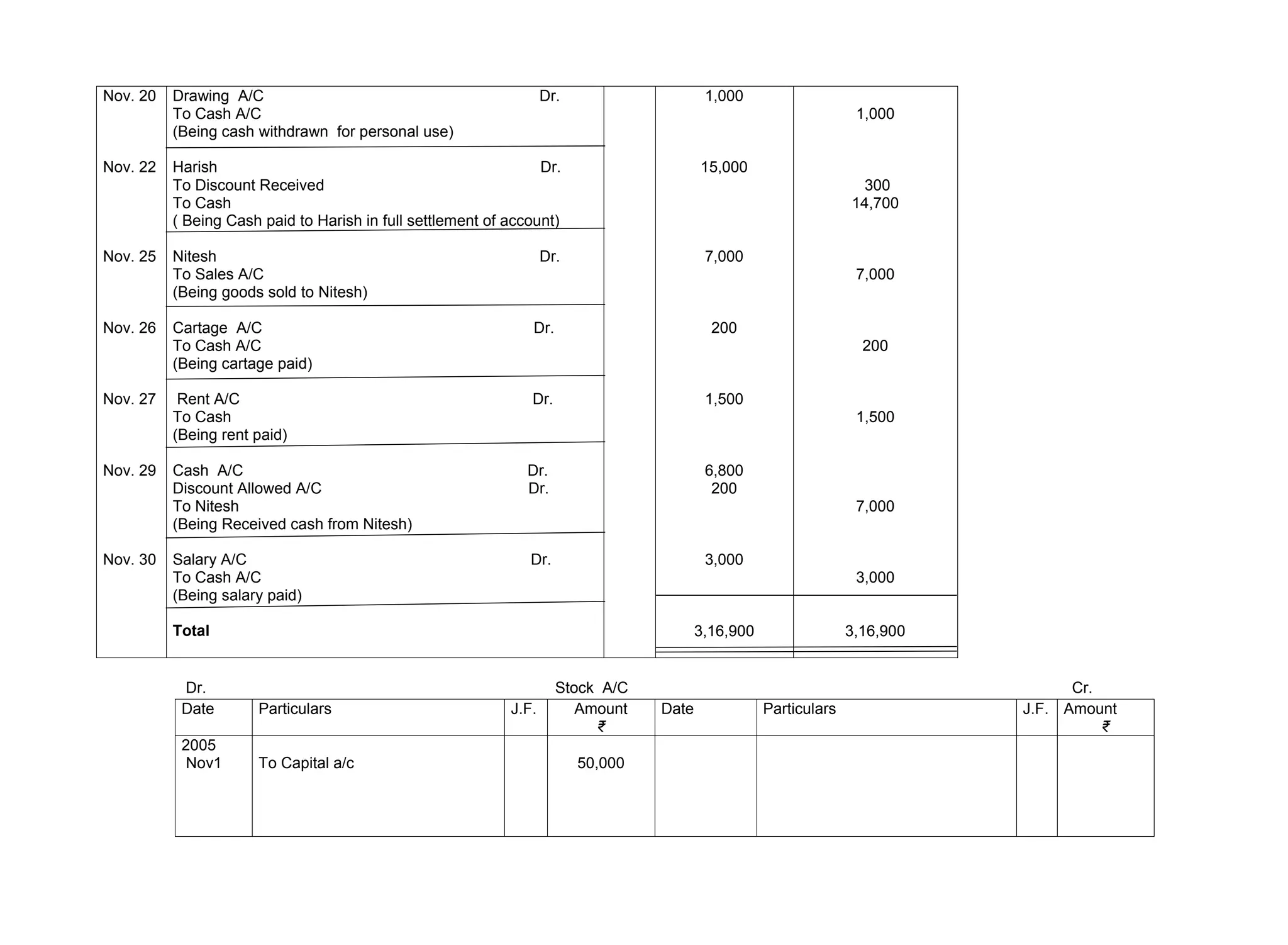

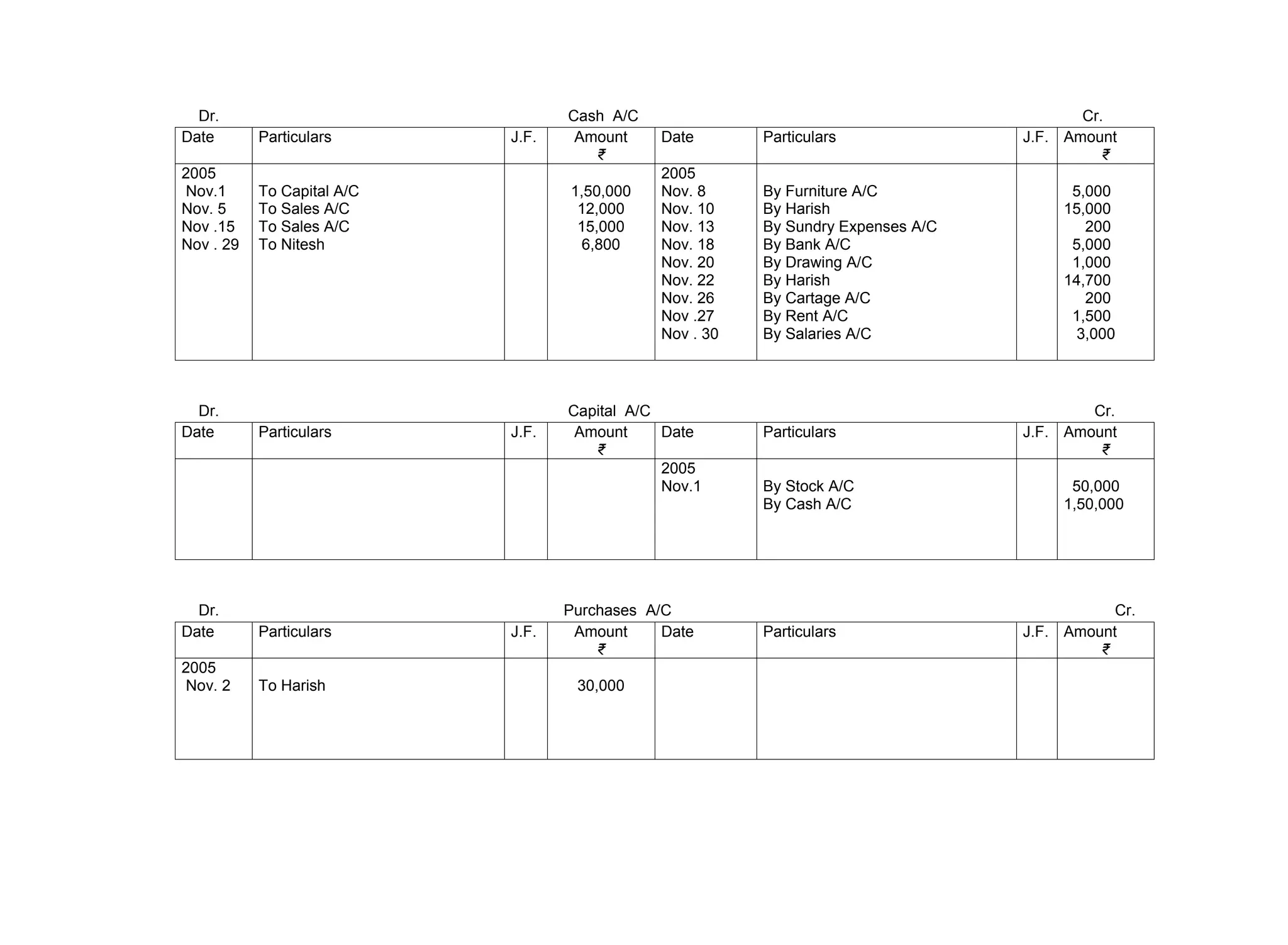

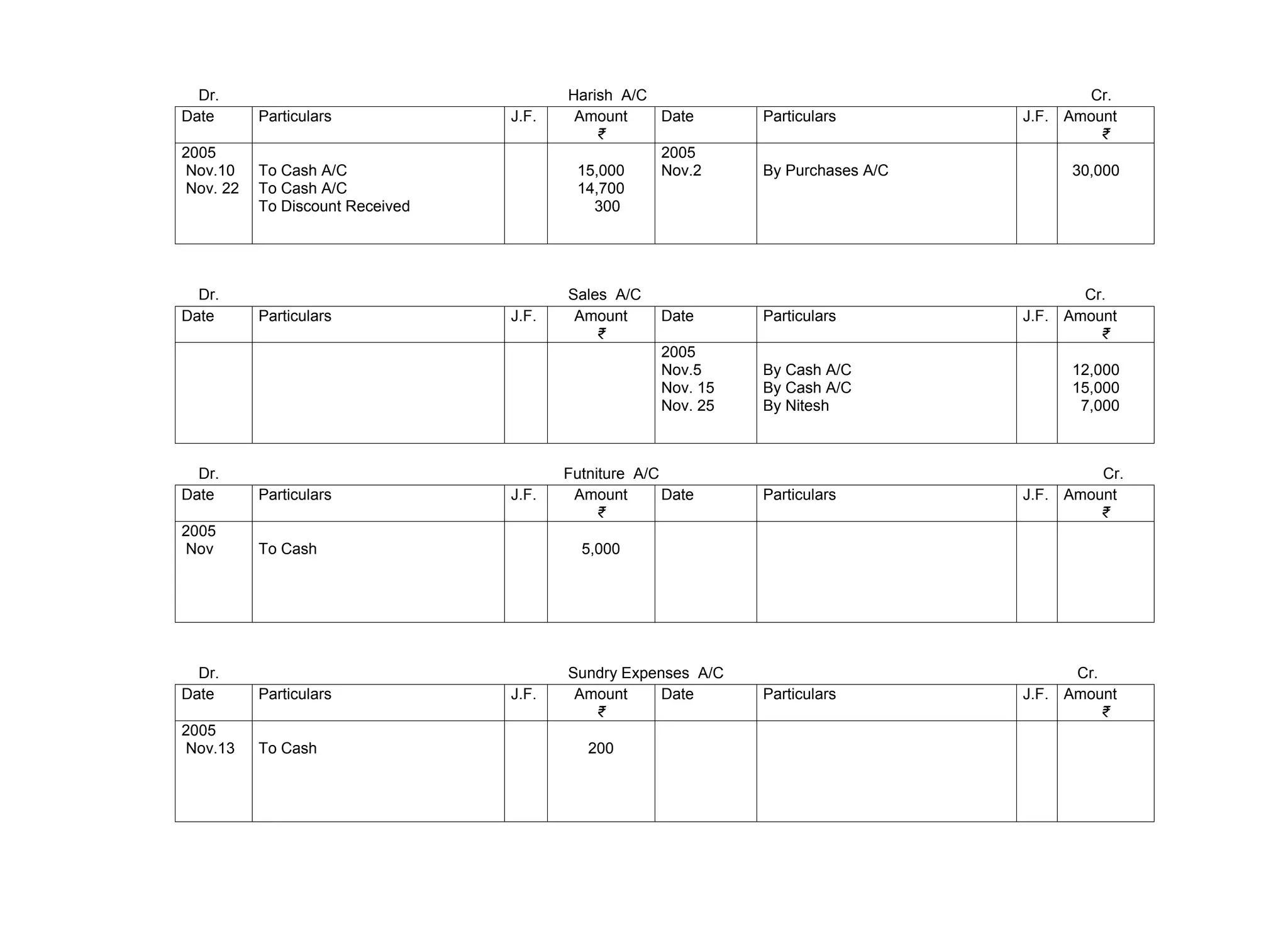

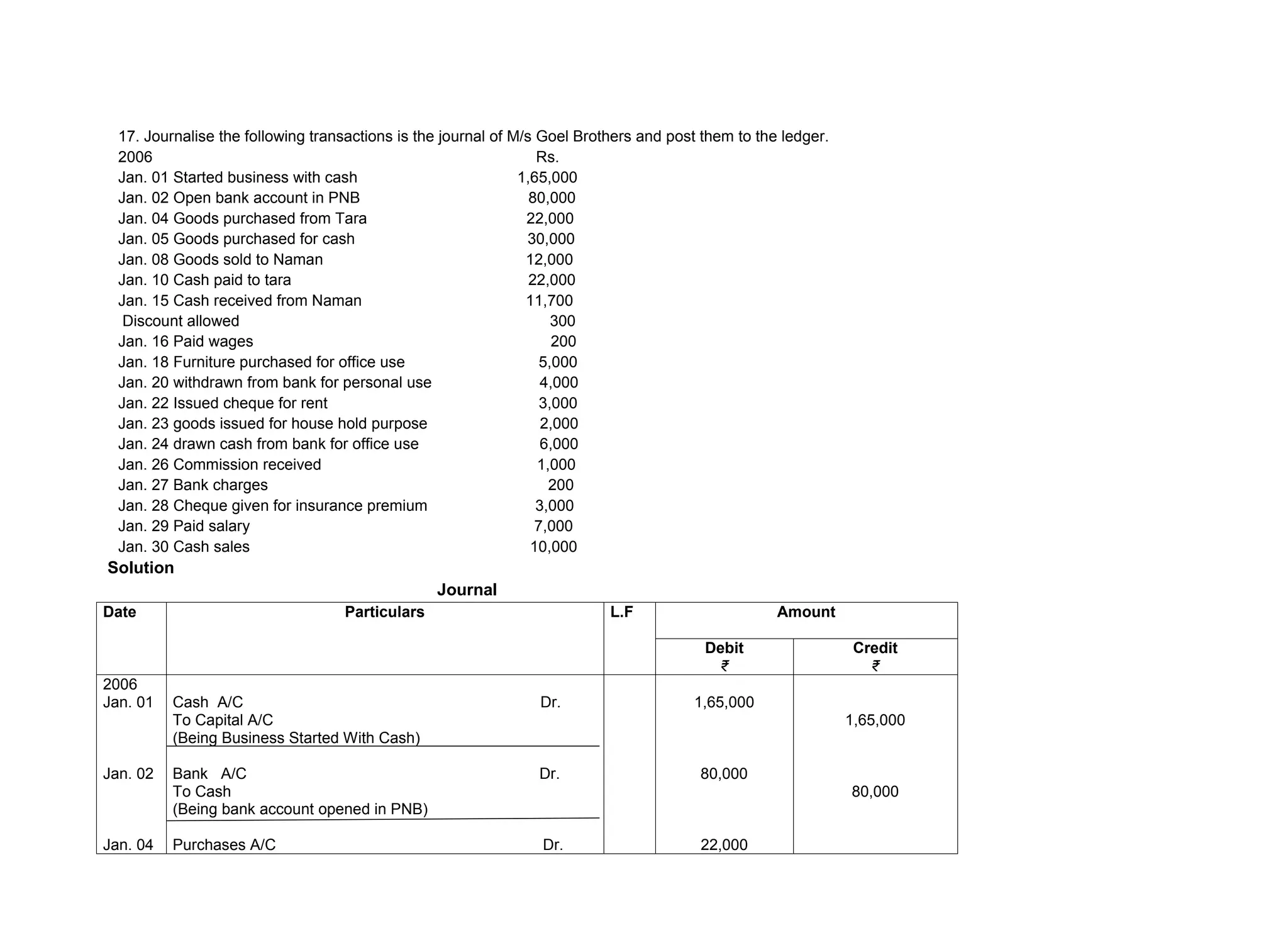

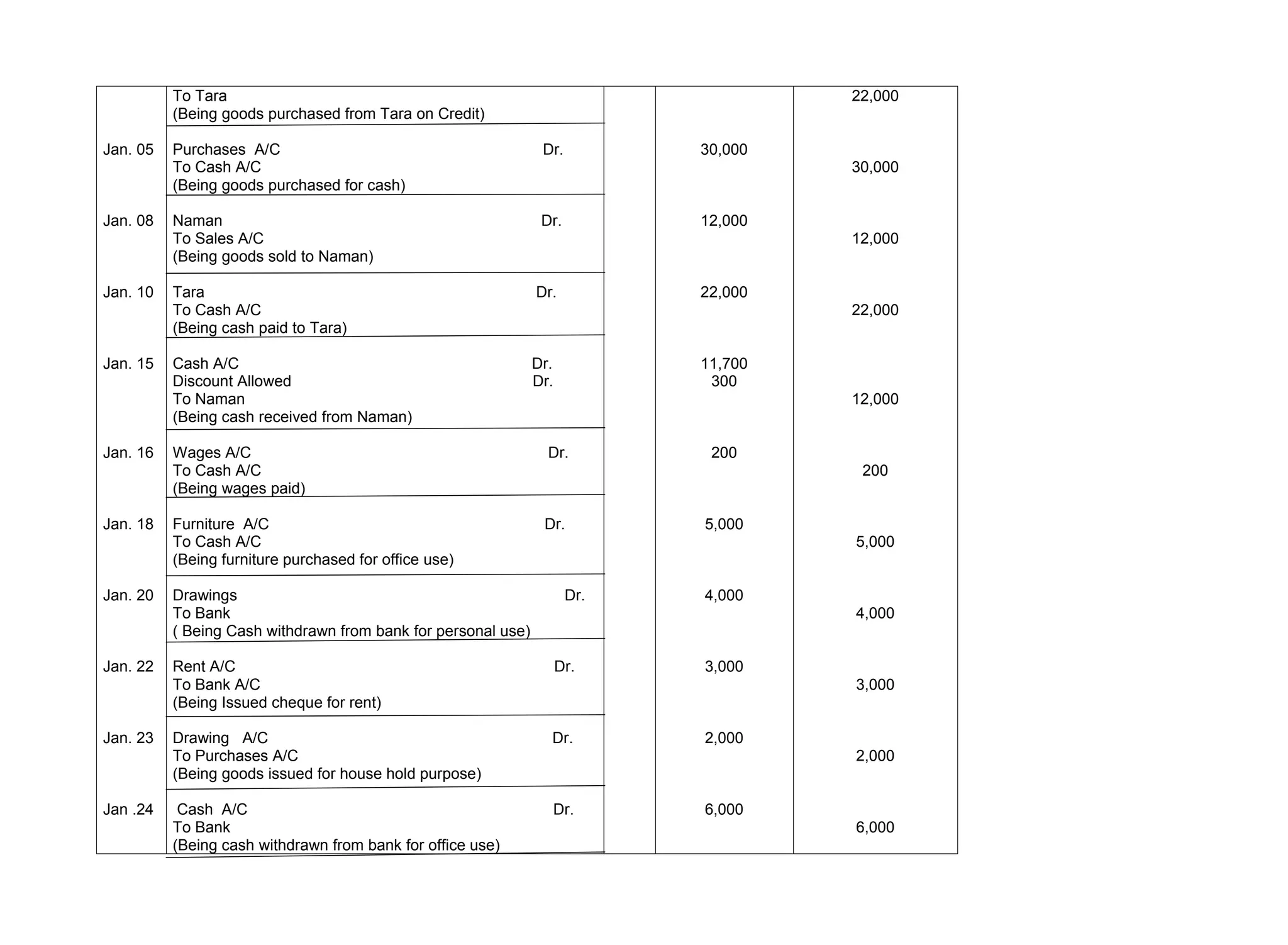

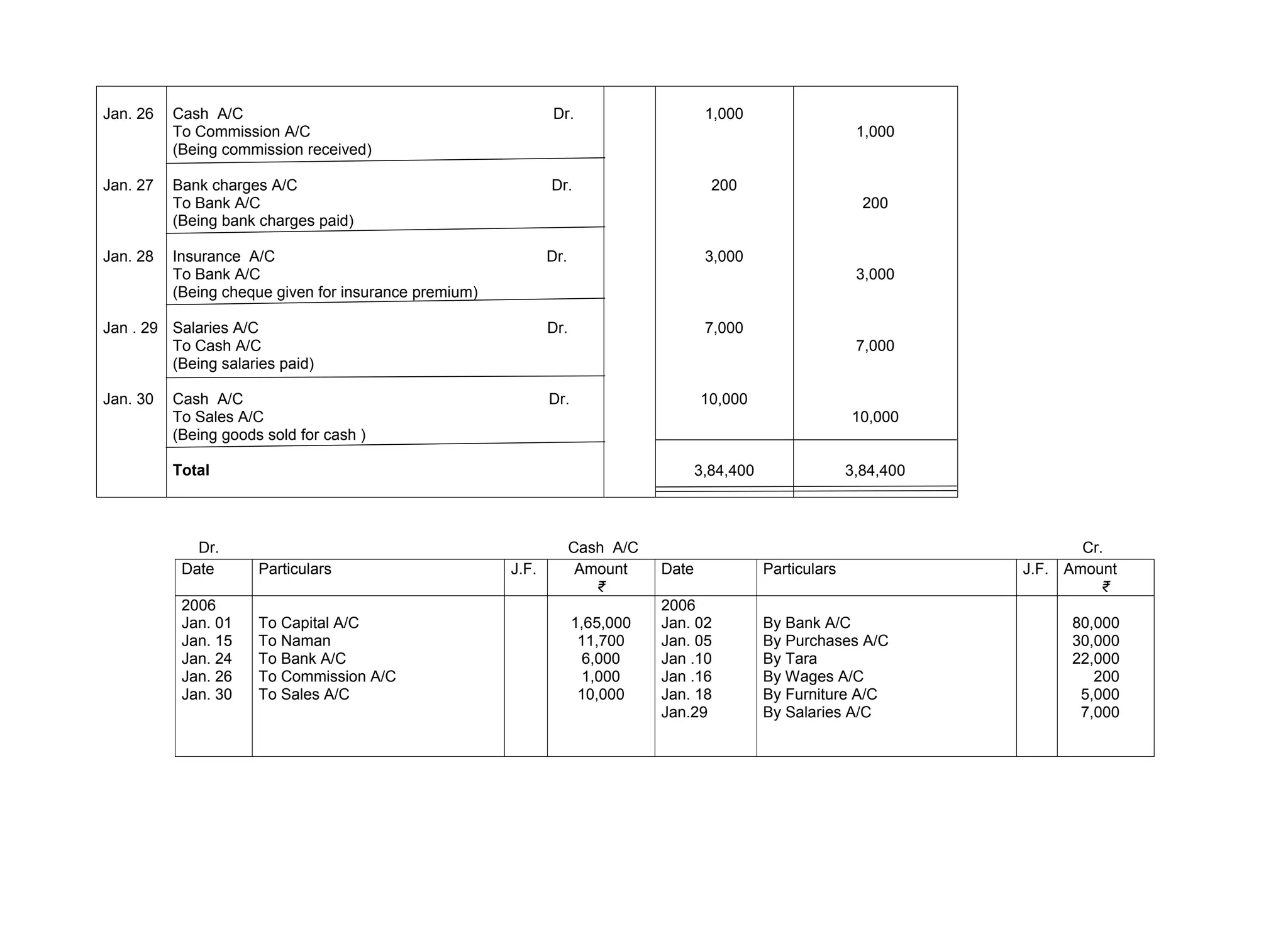

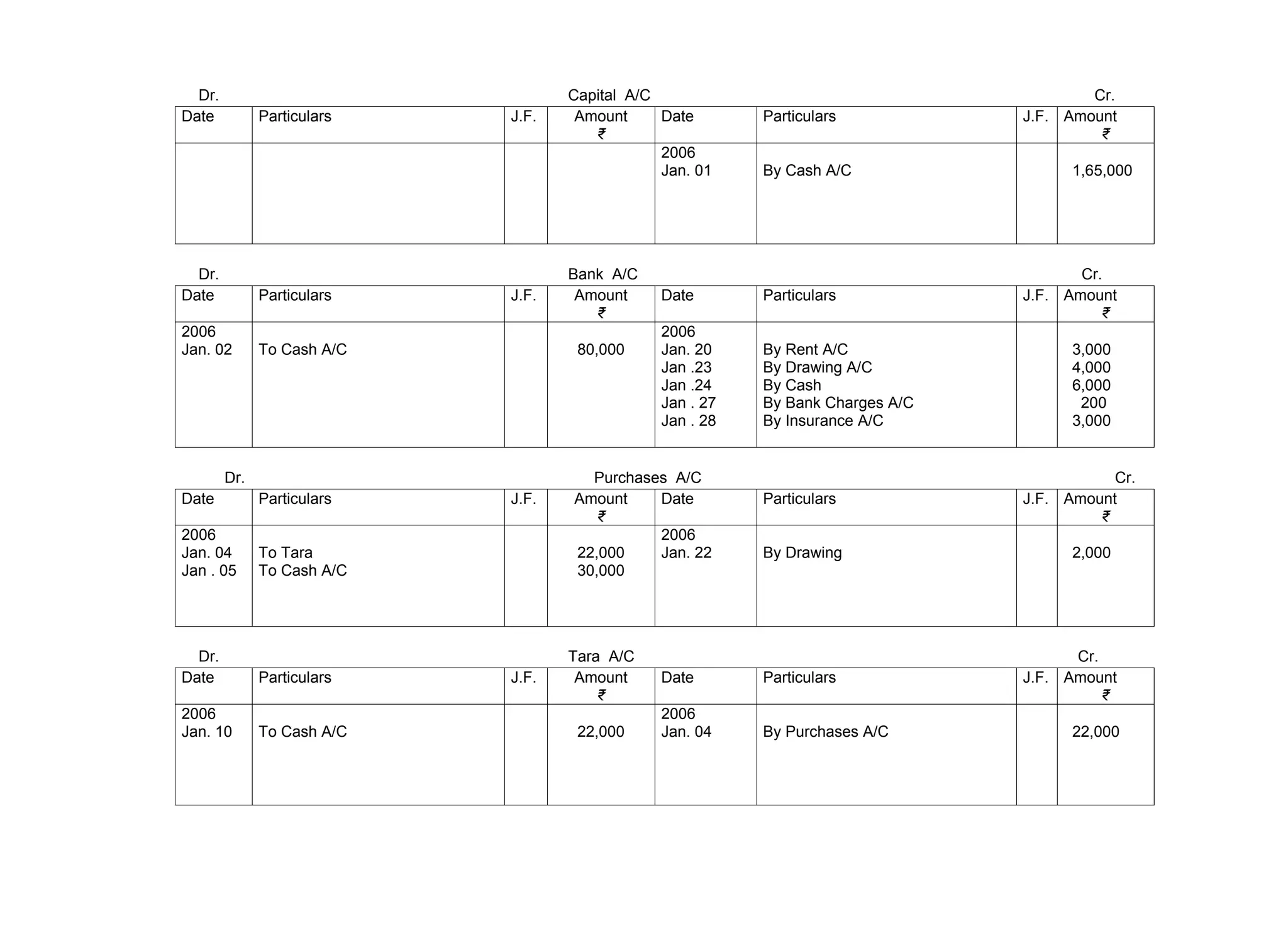

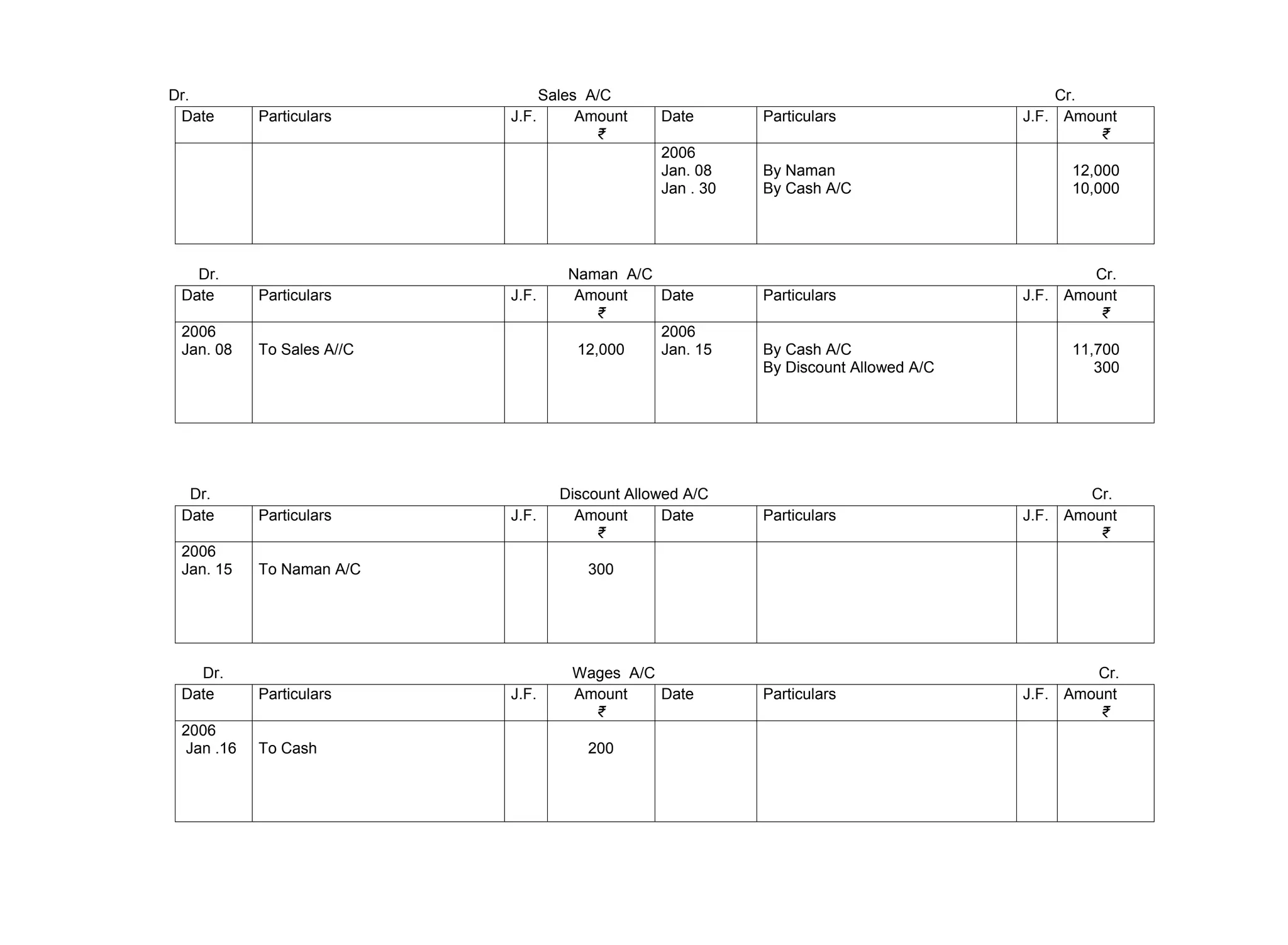

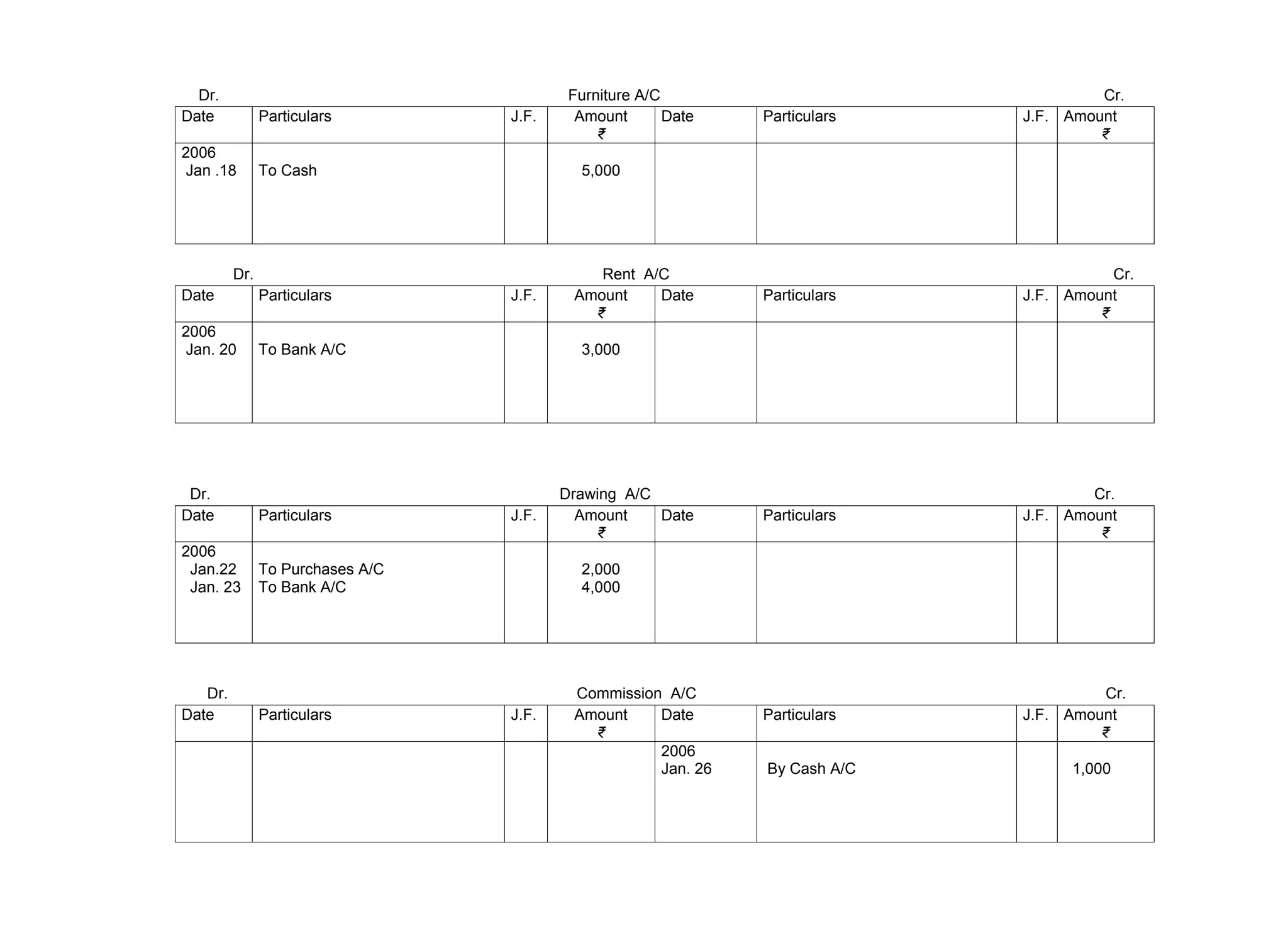

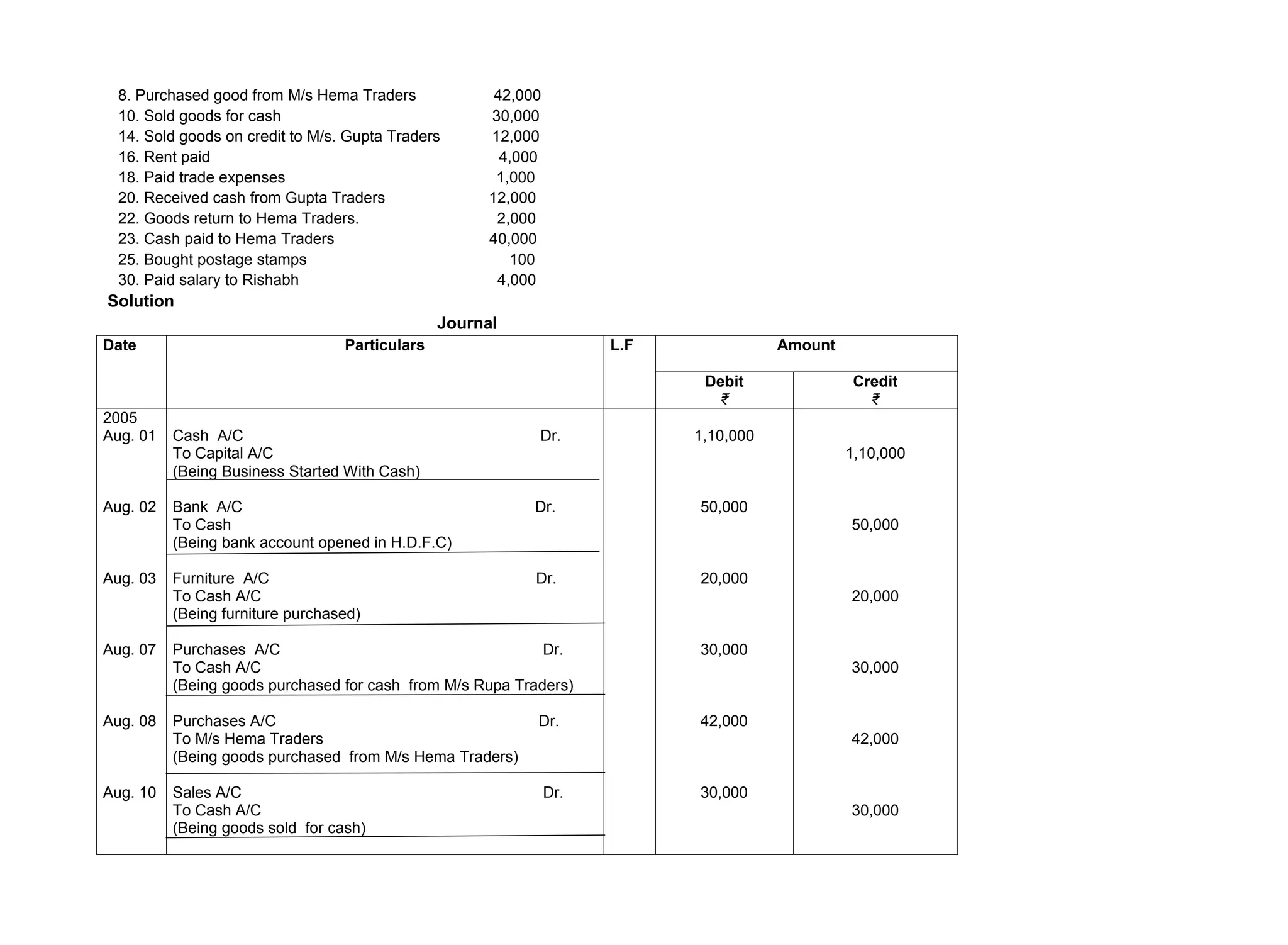

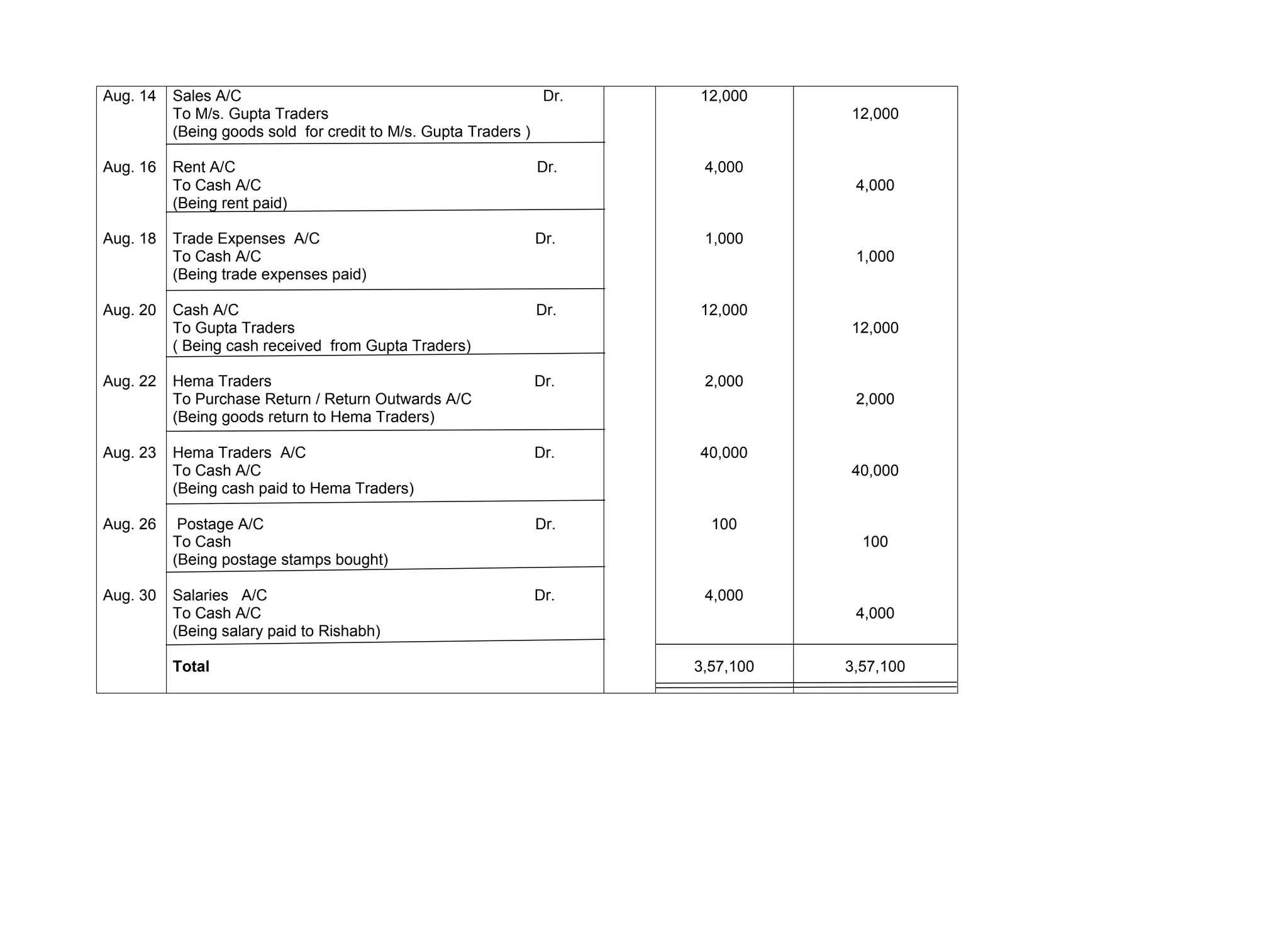

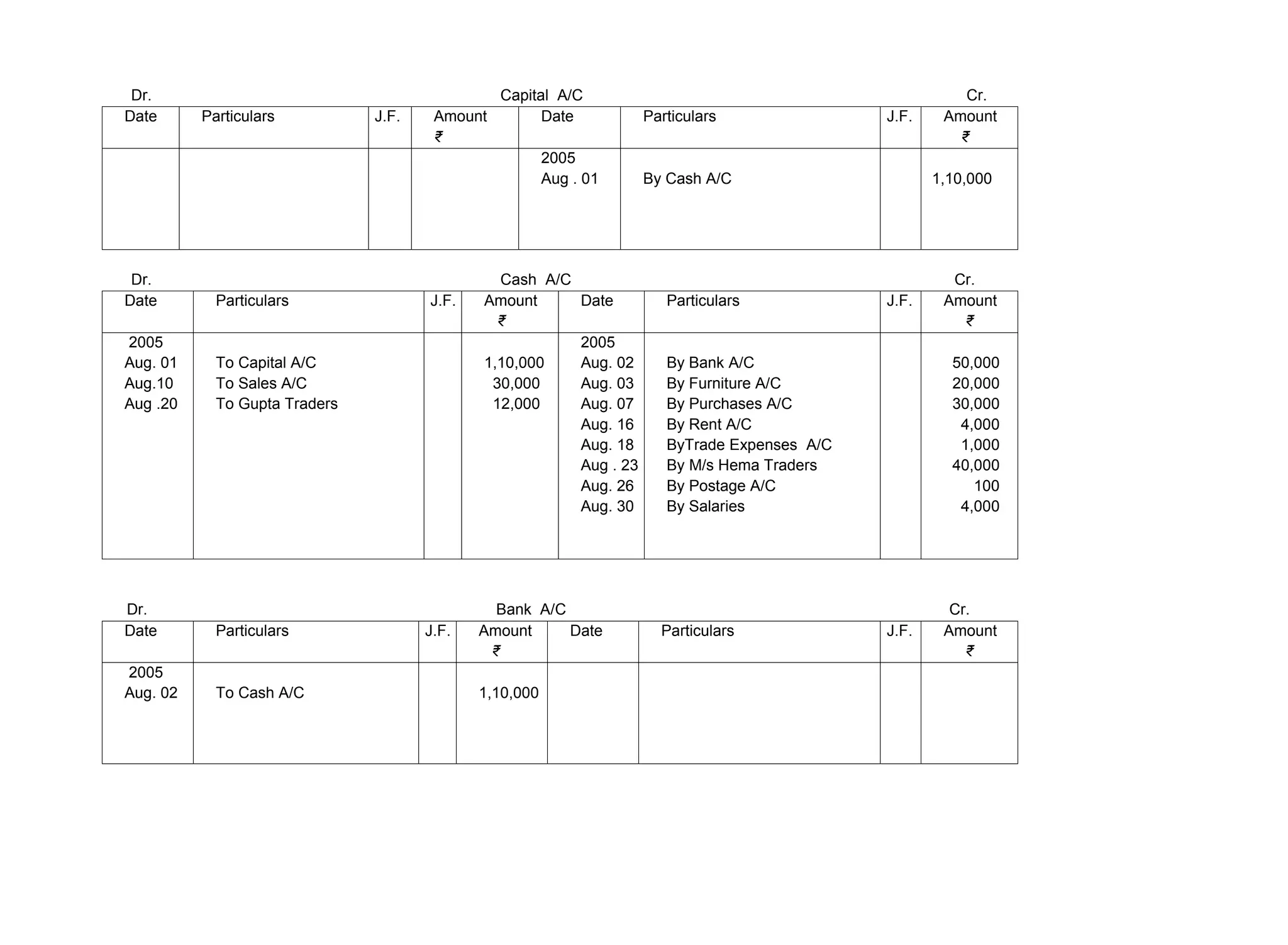

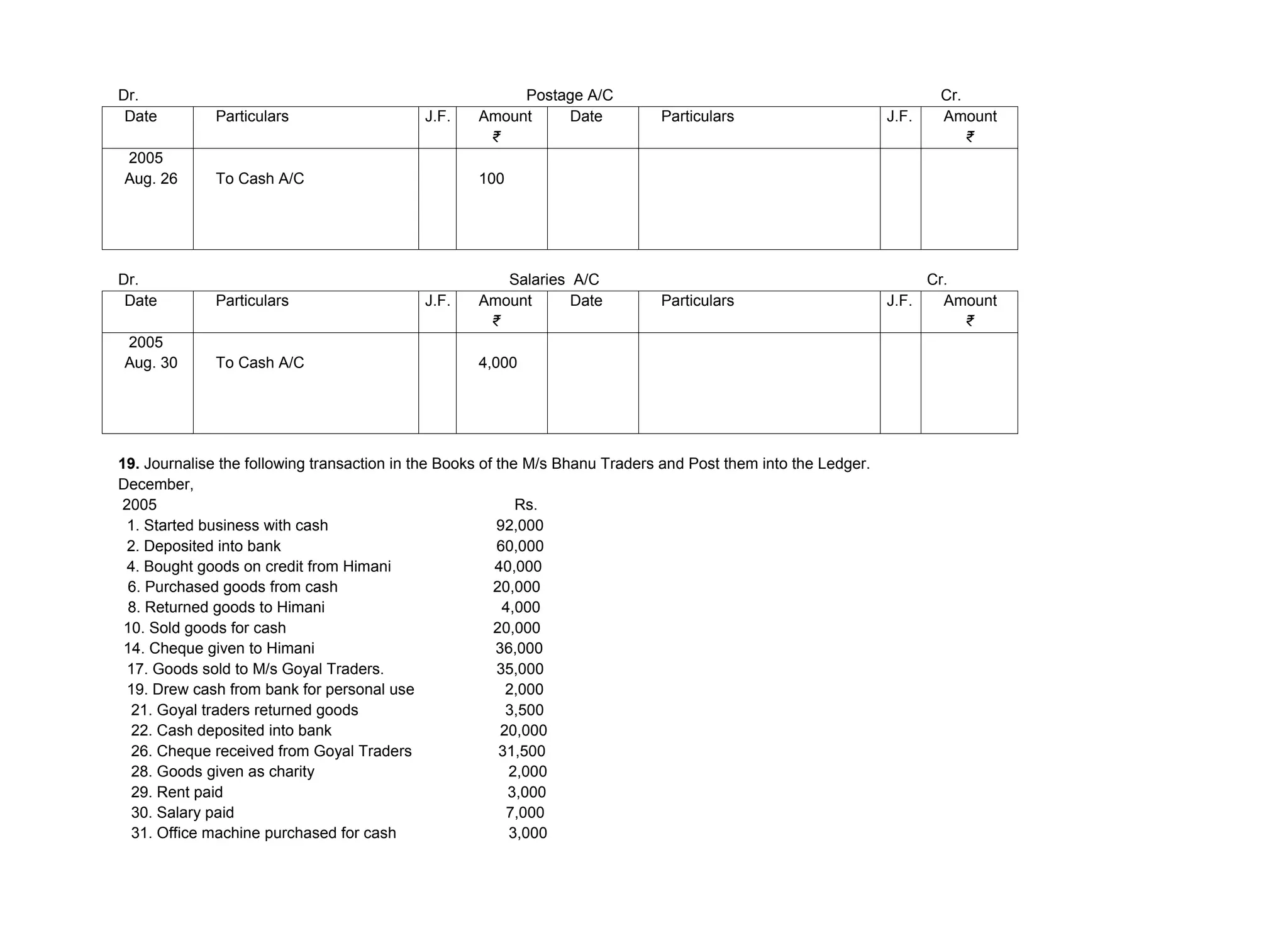

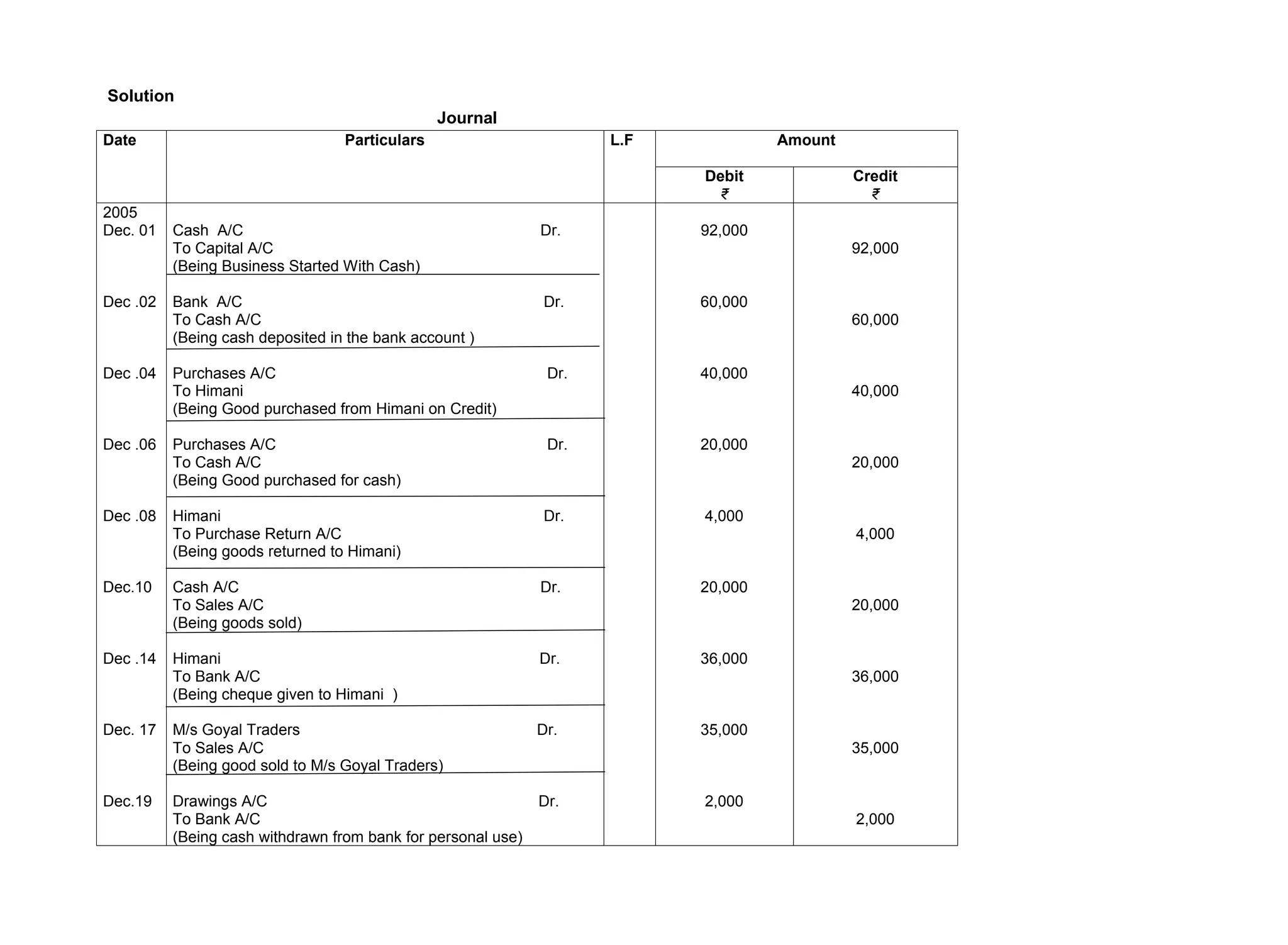

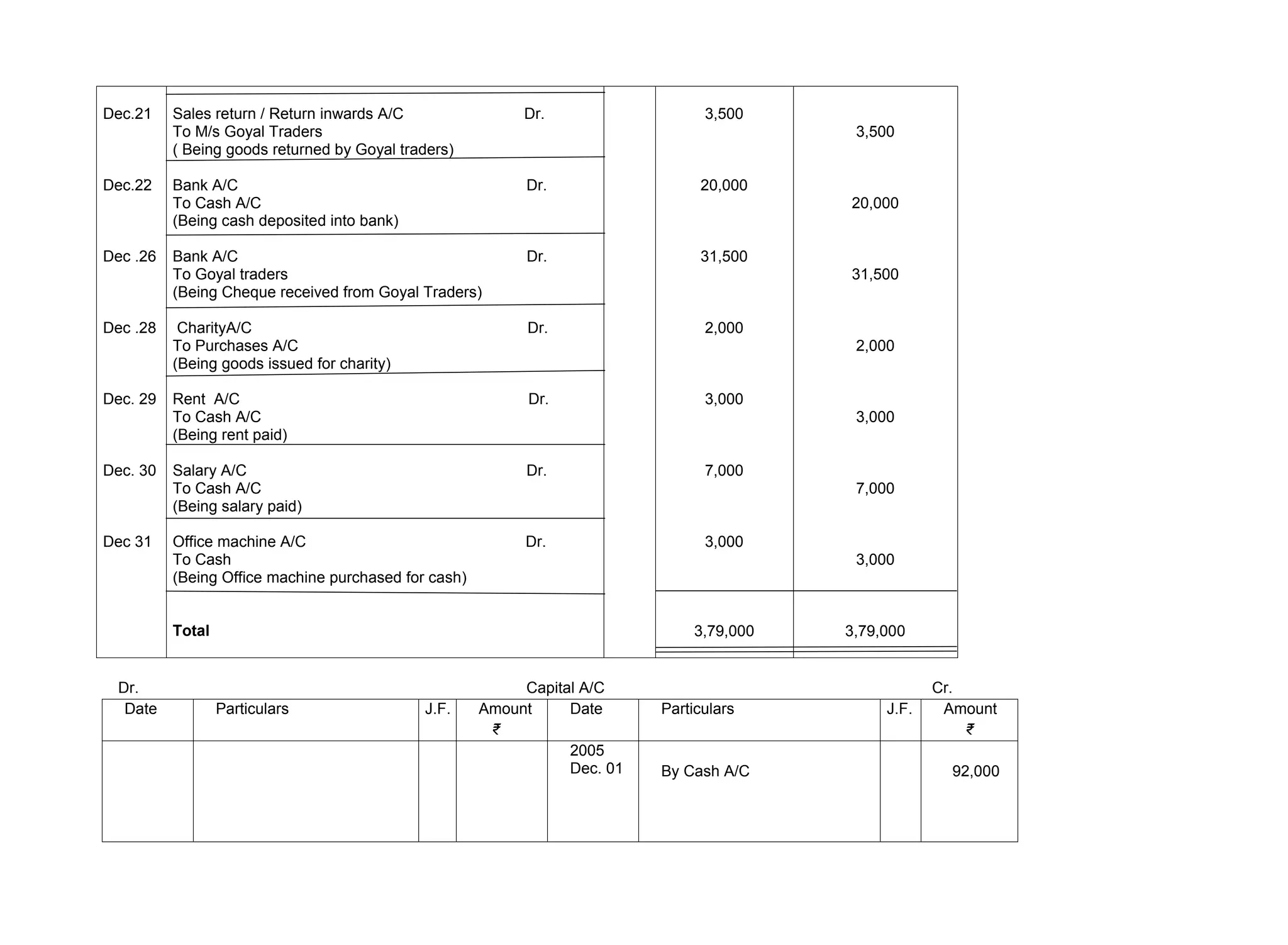

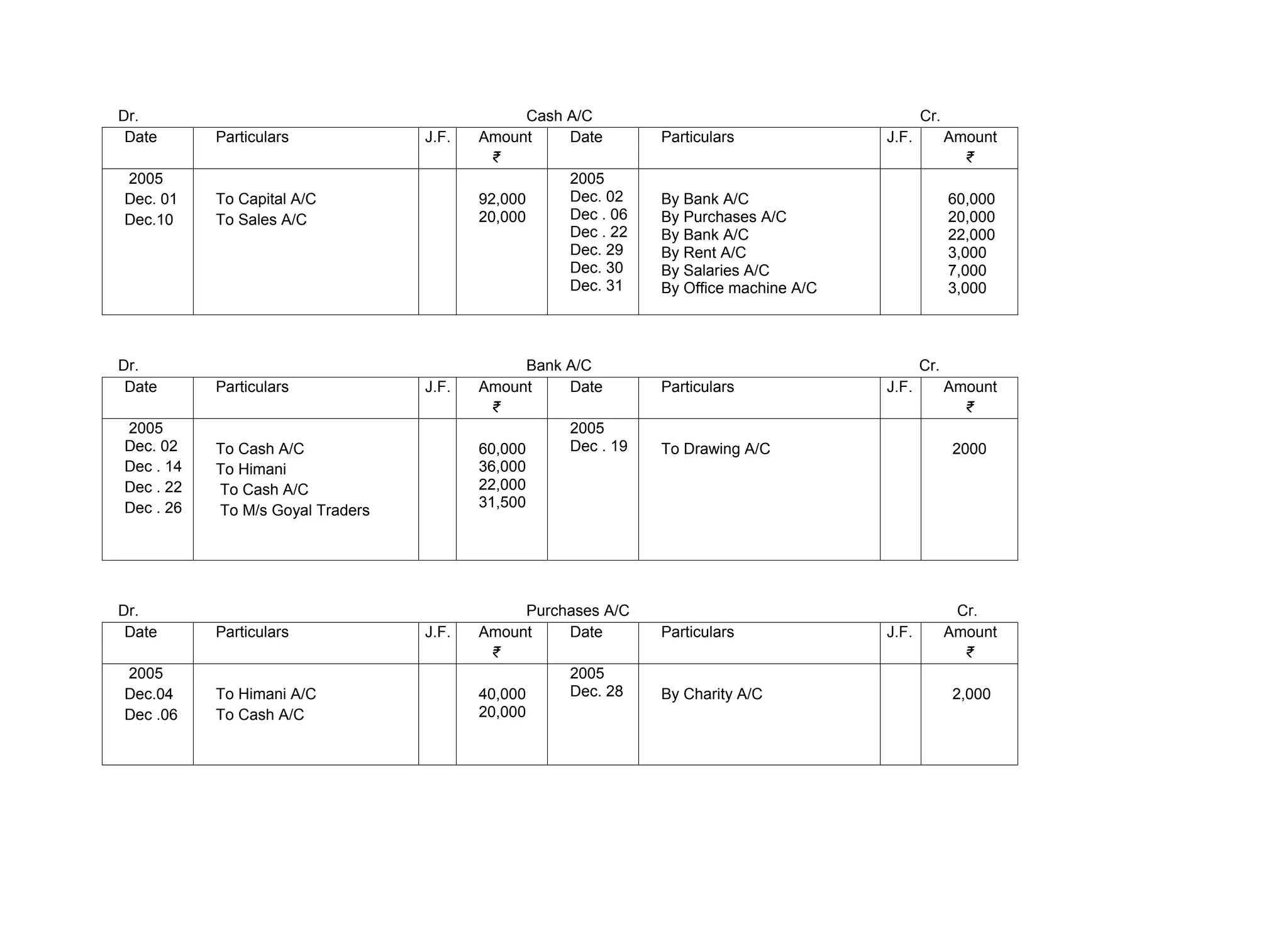

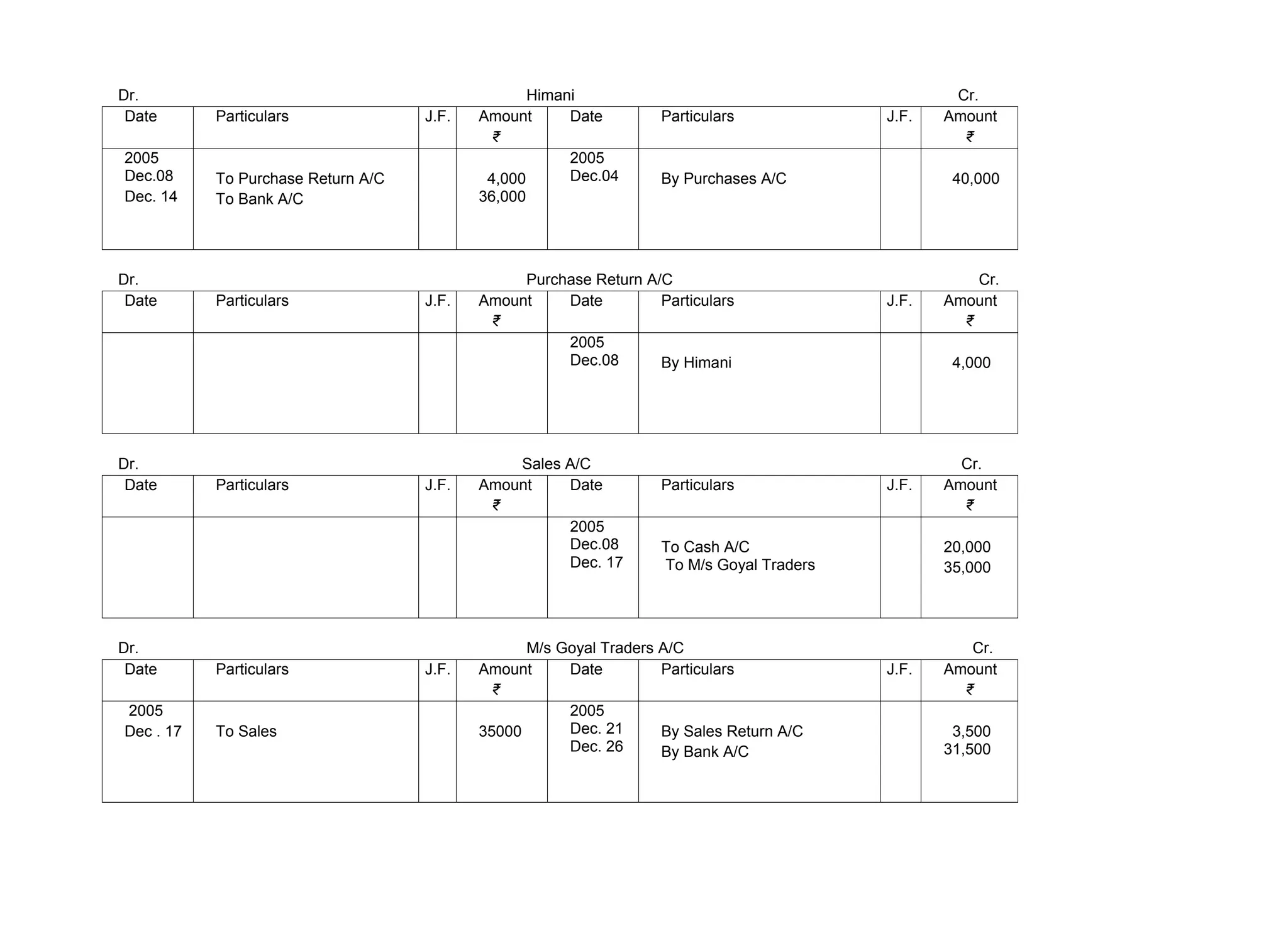

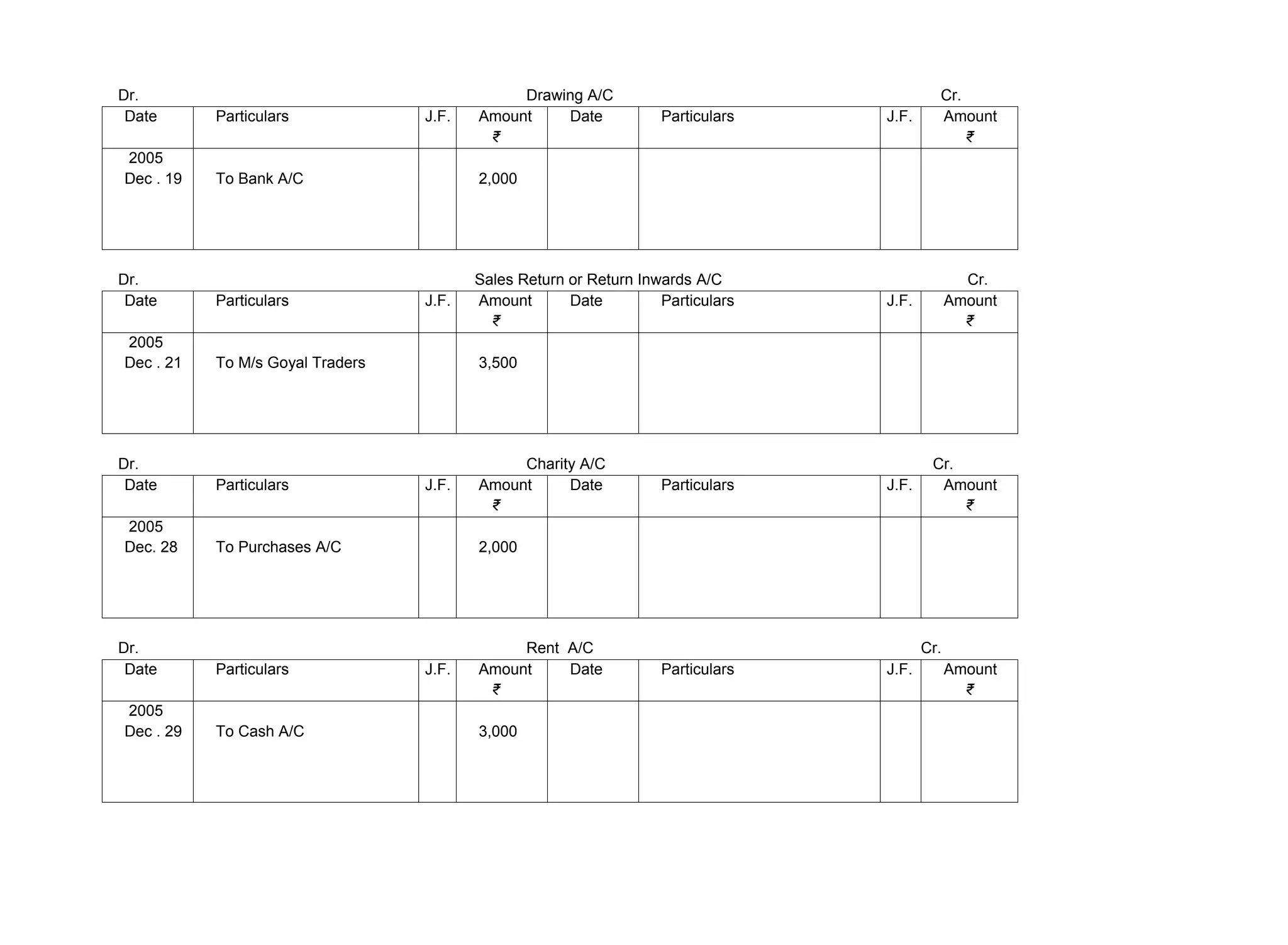

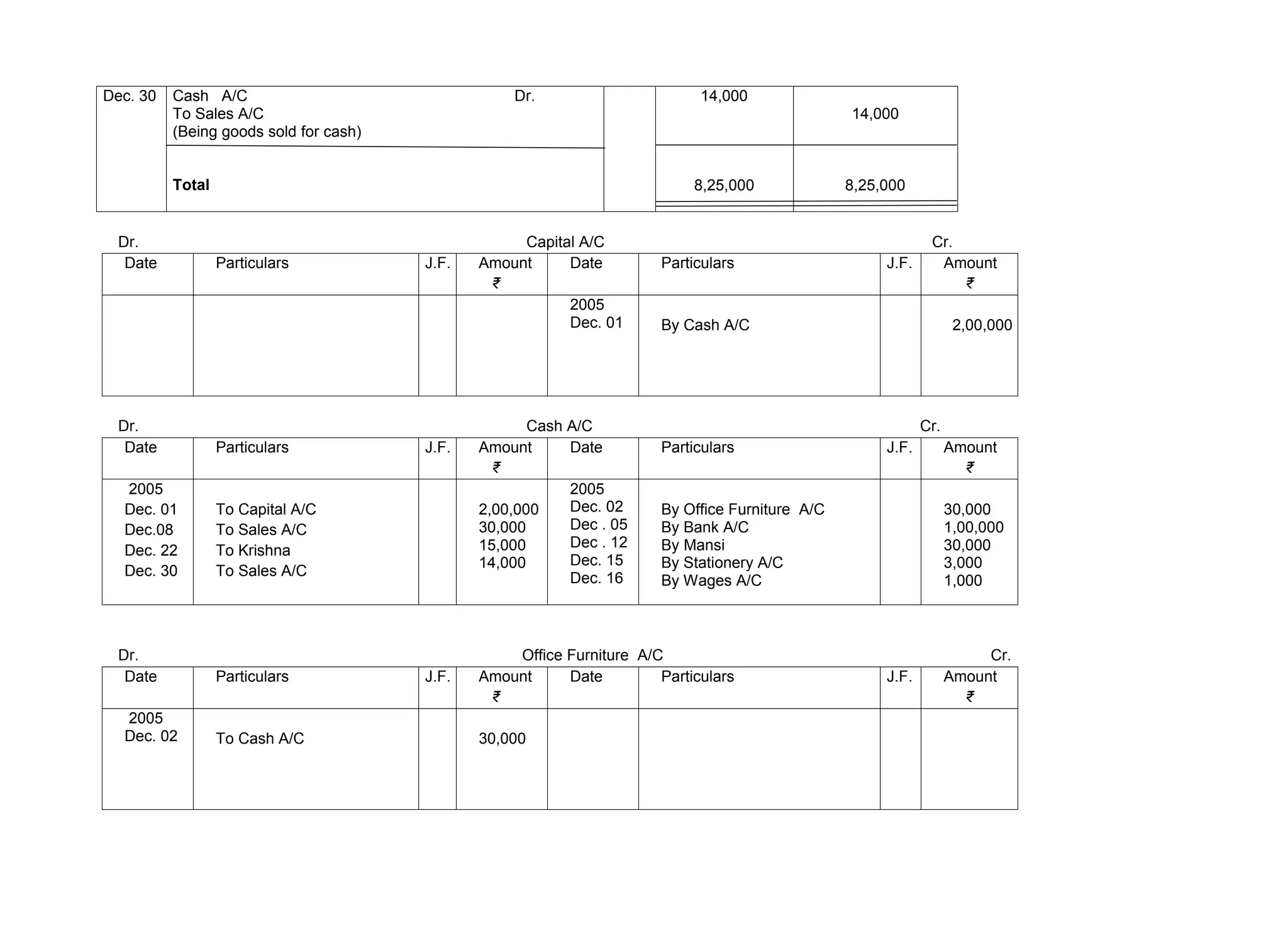

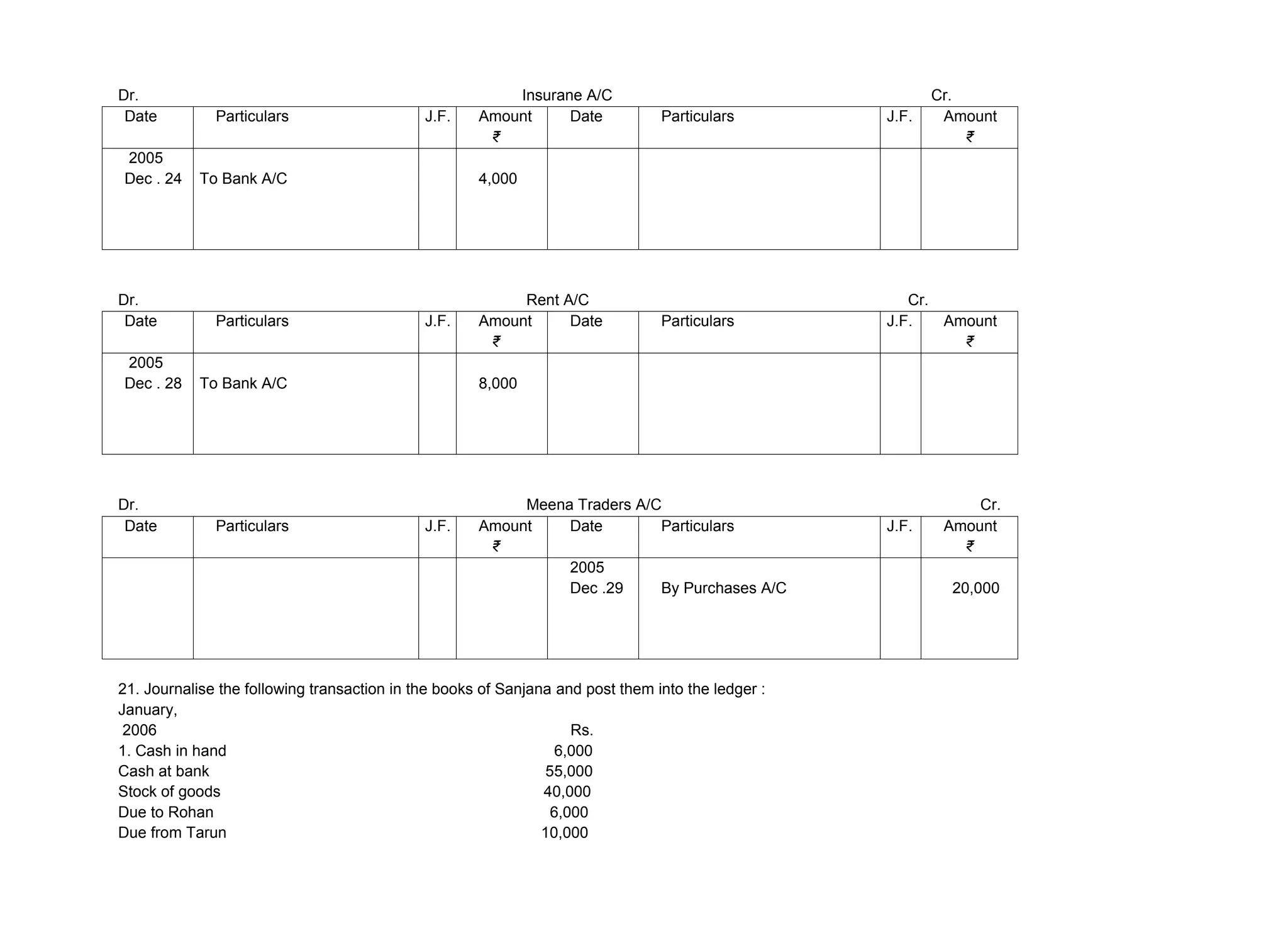

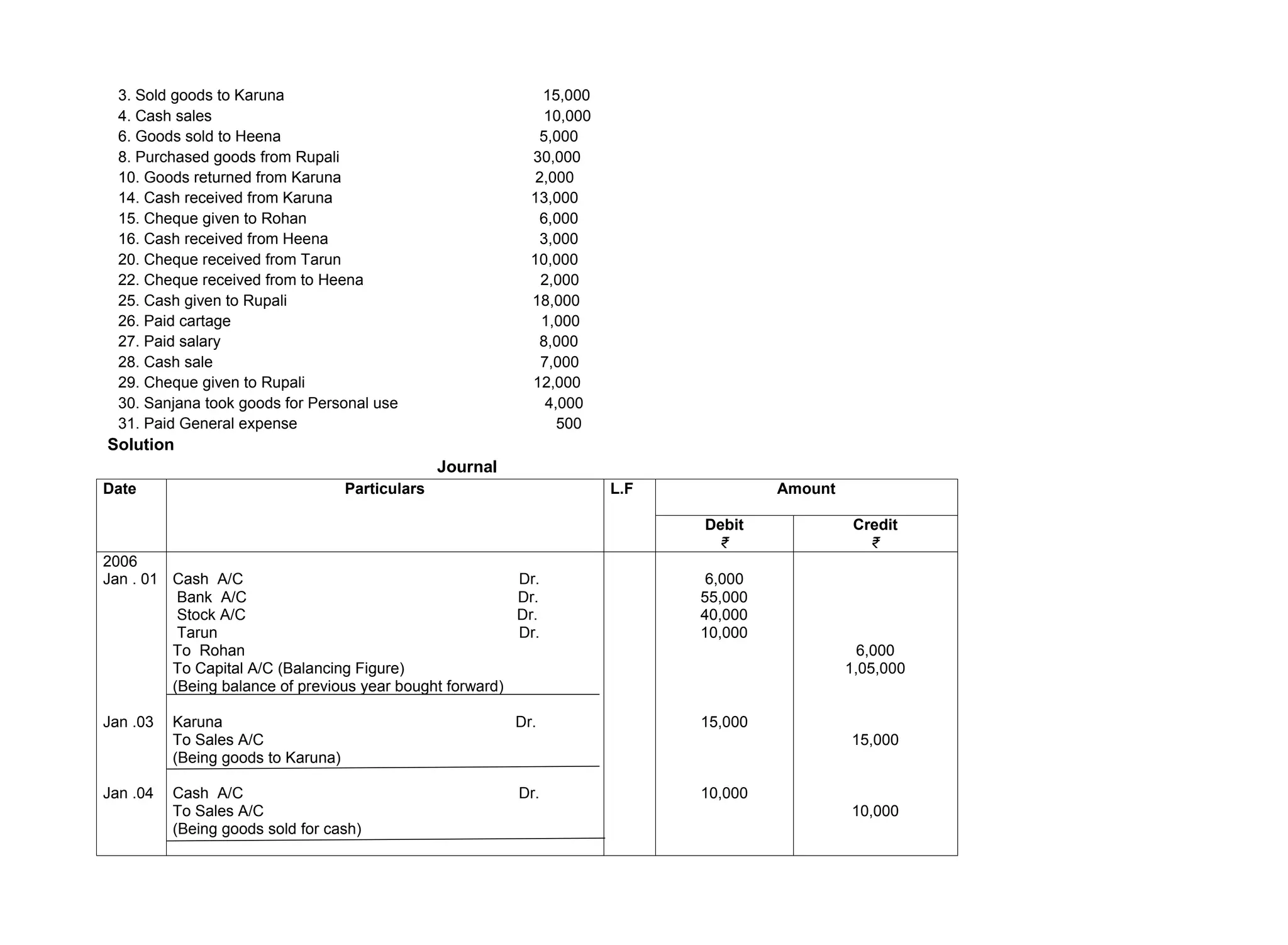

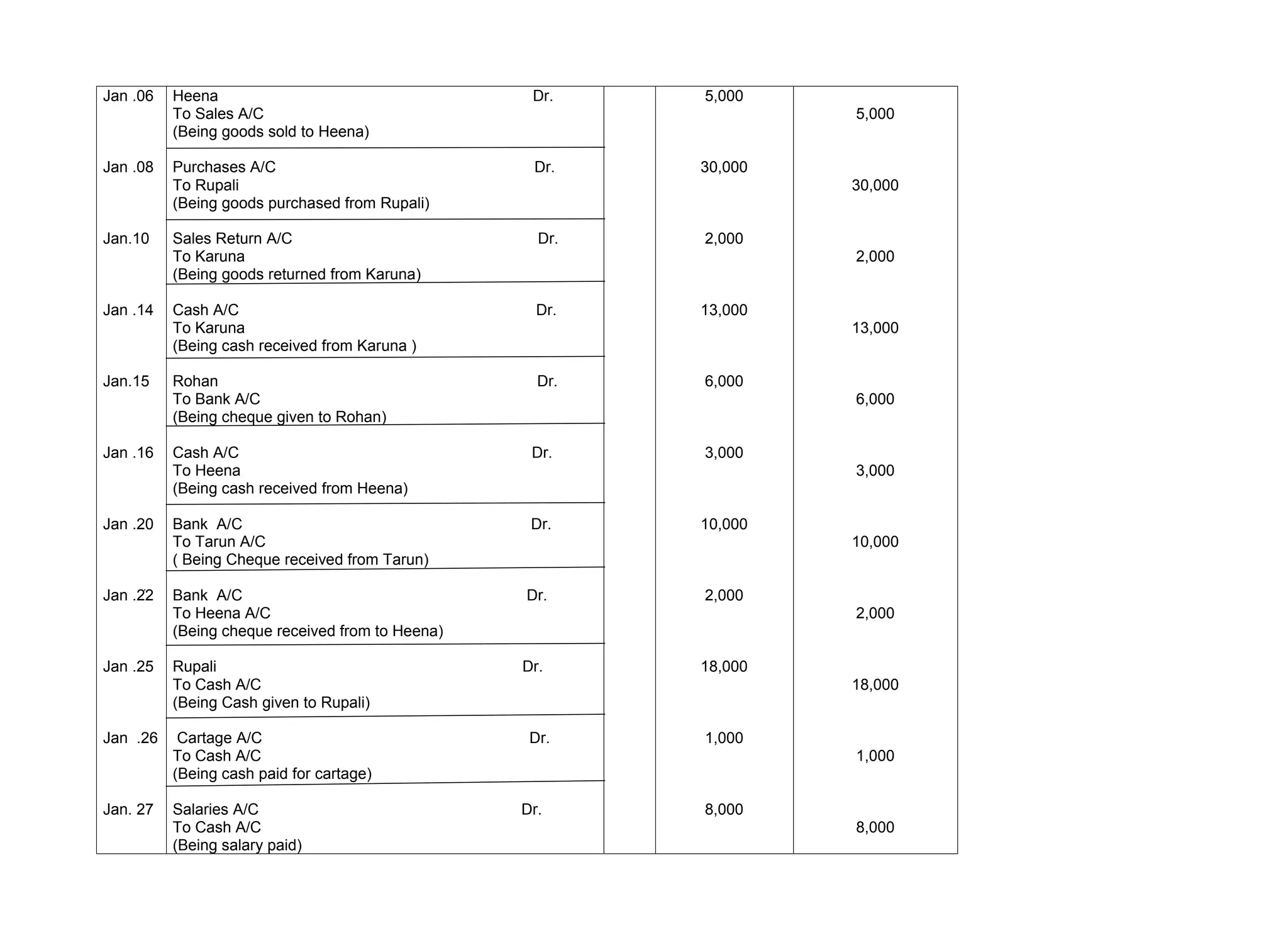

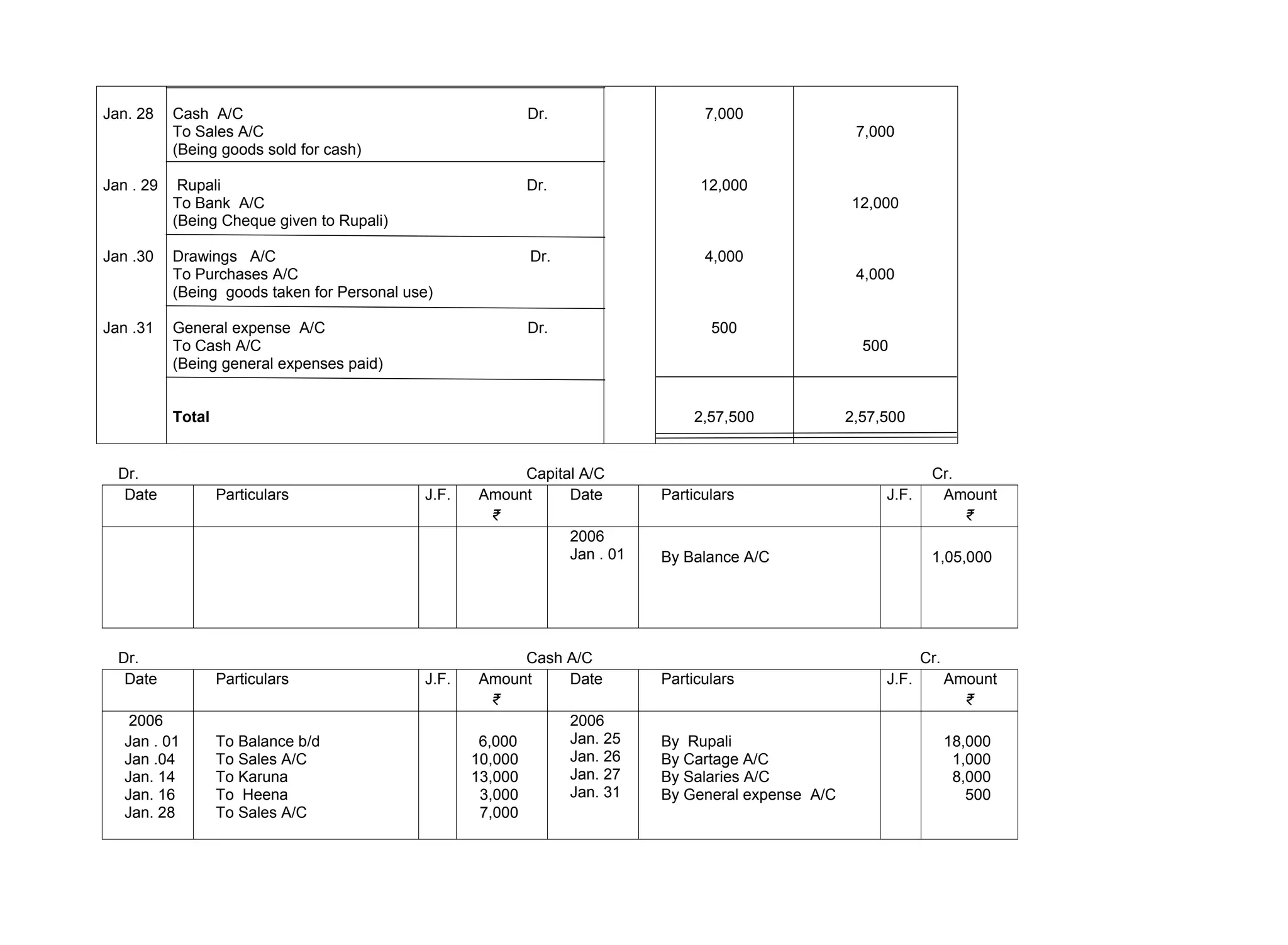

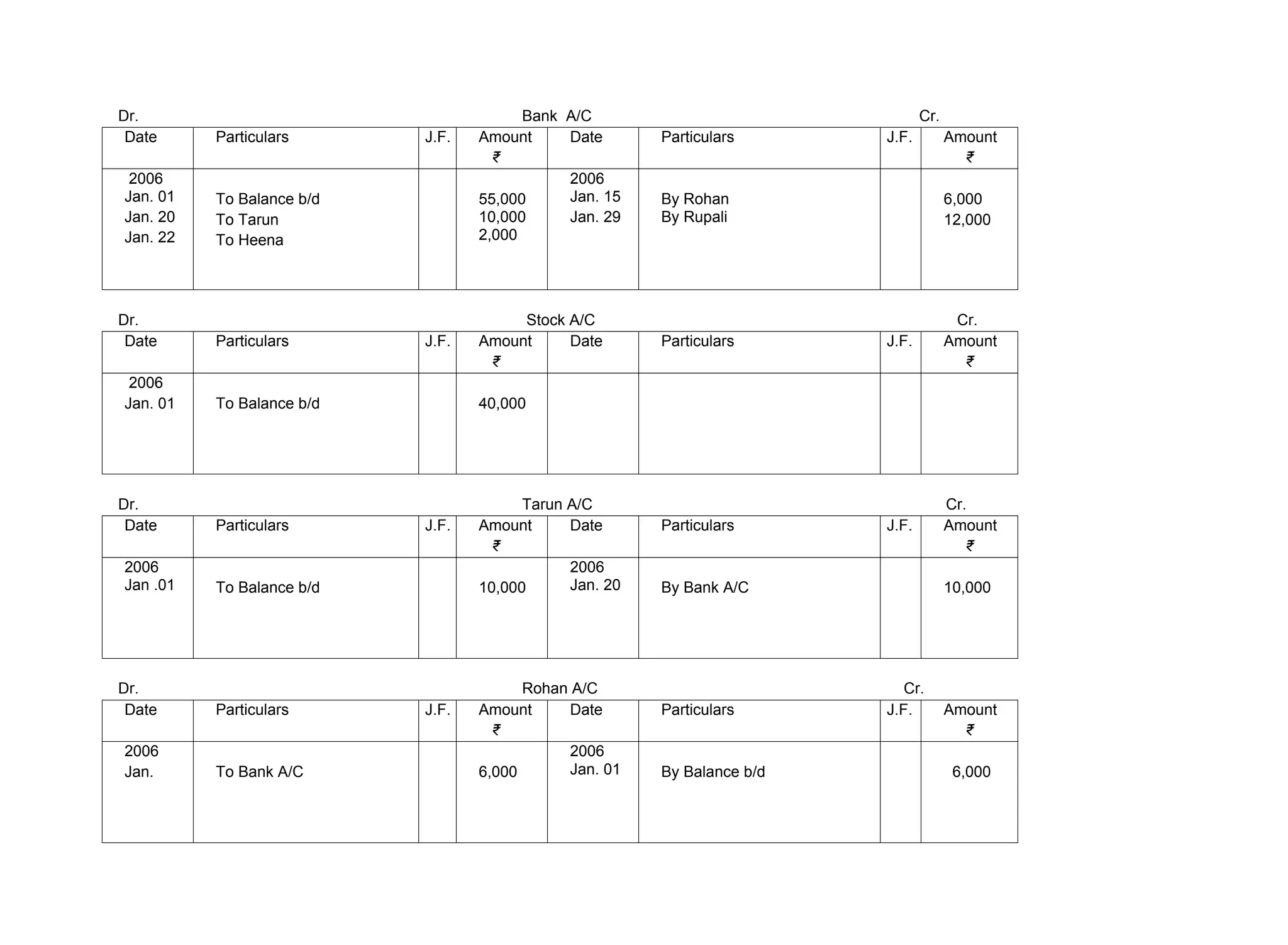

The document provides examples of journal entries and explains the accounting process. It discusses how transactions are first recorded in journals before being posted to individual accounts. Debits are listed before credits in journal entries and credits are indented. Accounts record the effects of transactions by showing increases or decreases to asset, liability, equity, expense and revenue accounts.