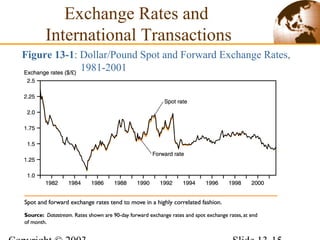

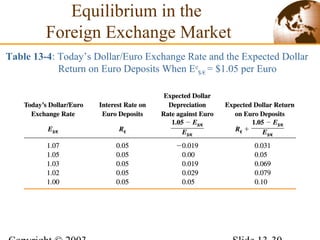

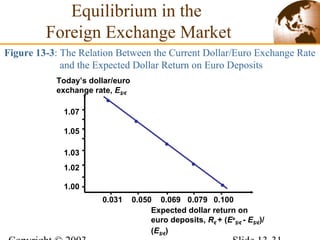

Downloaded 89 times

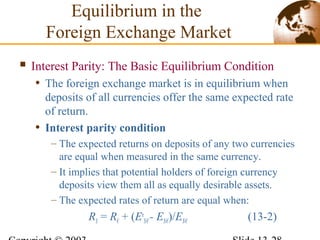

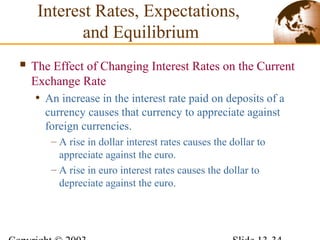

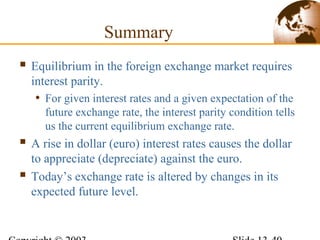

![• The expected rate of return difference between dollar

and euro deposits is:

R$ - [R€ + (Ee

$/€ - E$/€ )/E$/€ ]= R$ - R€ - (Ee

$/€ -E$/€ )/E$/€ (13-1)

where:

R$ = interest rate on one-year dollar deposits

R€ = today’s interest rate on one-year euro deposits

E$/€ = today’s dollar/euro exchange rate (number of

dollars per euro)

Ee

$/€ = dollar/euro exchange rate (number of dollars per

euro) expected to prevail a year from today

The Demand for

Foreign Currency Assets](https://image.slidesharecdn.com/internationaleconomicch13-160602143733/85/International-economic-ch13-24-320.jpg)

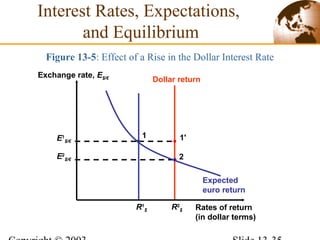

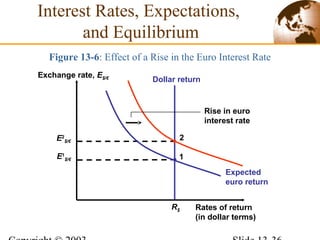

This document summarizes key concepts about exchange rates and the foreign exchange market from an asset approach perspective. It discusses how exchange rates are determined by supply and demand in the foreign exchange market, and how interest rates, expectations of future exchange rates, and relative prices affect equilibrium in the market. Equilibrium requires interest rate parity, where expected returns are equal across currency deposits when measured in the same currency. A rise in a currency's interest rate causes its appreciation, while a rise in expected future exchange rates causes the current rate to rise as well.