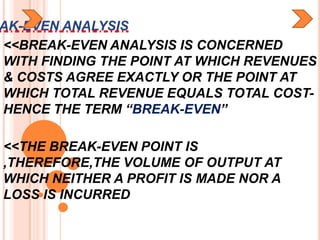

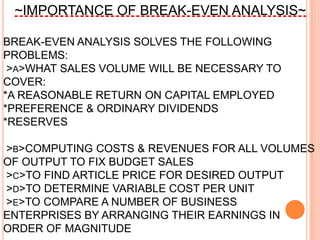

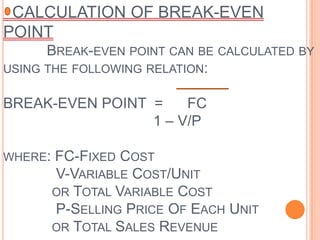

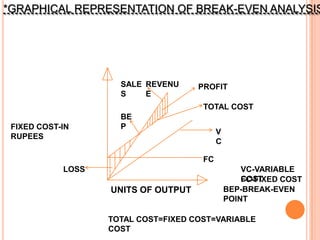

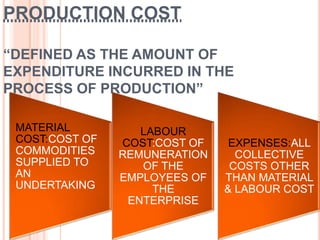

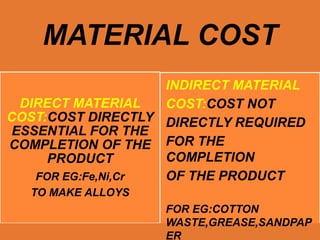

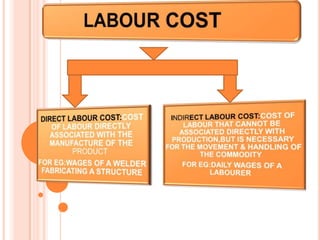

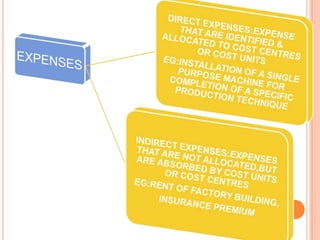

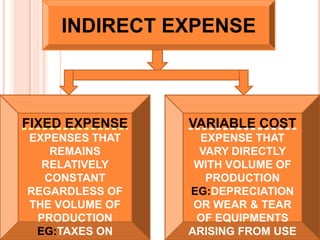

This document welcomes members of the Industrial Engineering & Management team and discusses production cost concepts. It defines production cost as the amount spent in the production process, including material, labor, and other expenses. Material costs are further divided into direct material costs and indirect material costs. Expenses are classified as either fixed or variable. The document also discusses break-even analysis, which finds the point where revenues and costs are equal, resulting in neither profit nor loss. It explains how to calculate the break-even point using a formula and presents a graphical representation of break-even analysis using a chart.

![RIME COST[TOTAL COST]

++

PRIME COST

DIRECT (VARIABL DIRECT

E)DIRECT MATERIA

LABOUR EXPENSE

COST L COST

S](https://image.slidesharecdn.com/industrialengg7managtjoshi-copy-130228071917-phpapp01/85/Industrial-engg-managt-break-even-analysis-10-320.jpg)