Downloaded 14 times

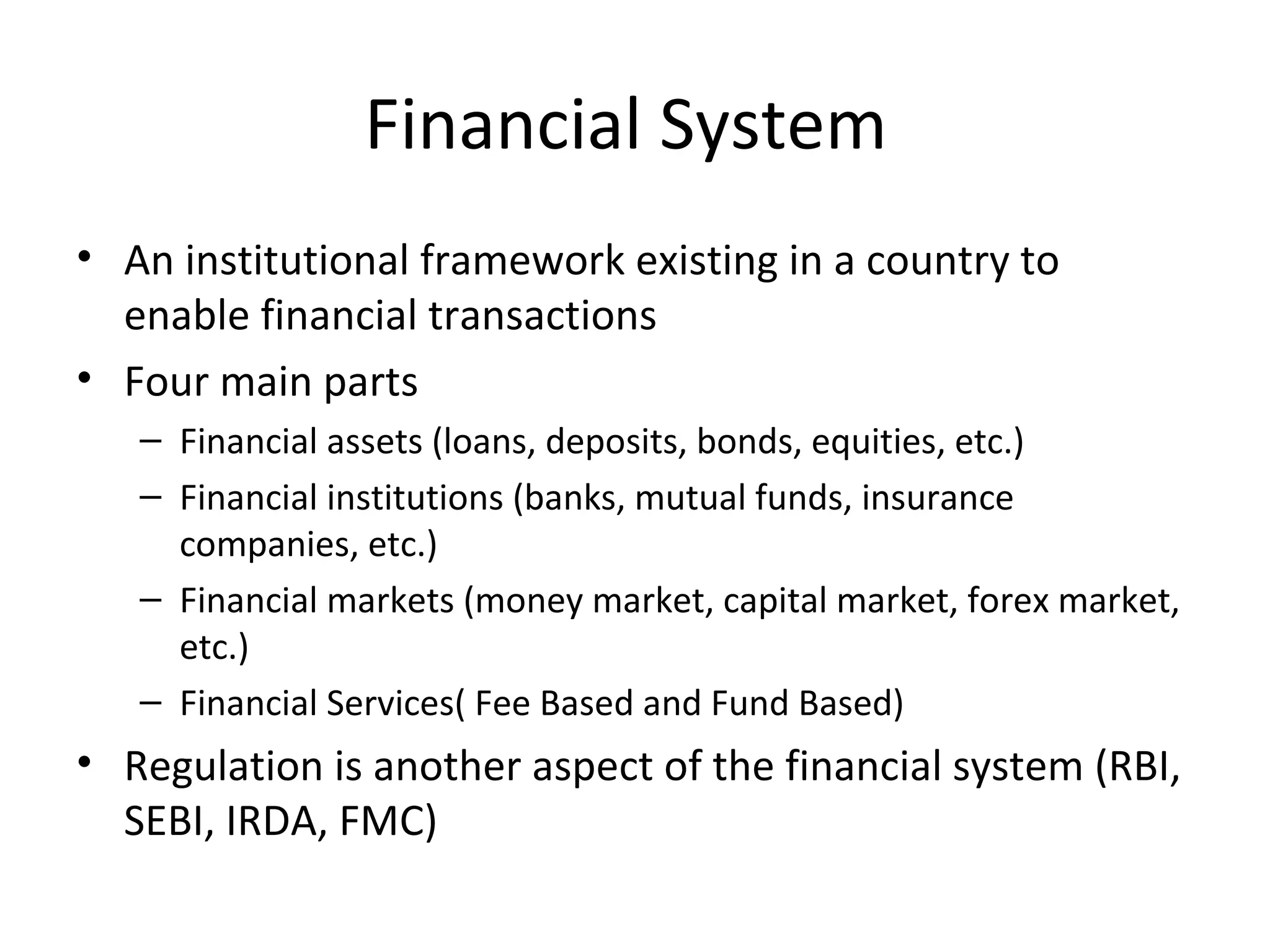

The financial system consists of four main parts: financial assets, financial institutions, financial markets, and financial services. It enables financial transactions through an institutional framework regulated by organizations like RBI, SEBI, and IRDA. The system channels funds from surplus to deficit units through various financial instruments for savers like deposits and bonds, and for borrowers like loans. It mobilizes savings through institutions like banks and invests them in markets like money markets for short-term funds and capital markets for long-term funds.

![Eco presentation1[2]](https://cdn.slidesharecdn.com/ss_thumbnails/ecopresentation12-120927080734-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Indian financial system[1]](https://cdn.slidesharecdn.com/ss_thumbnails/indianfinancialsystem1-130511123055-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)