Downloaded 145 times

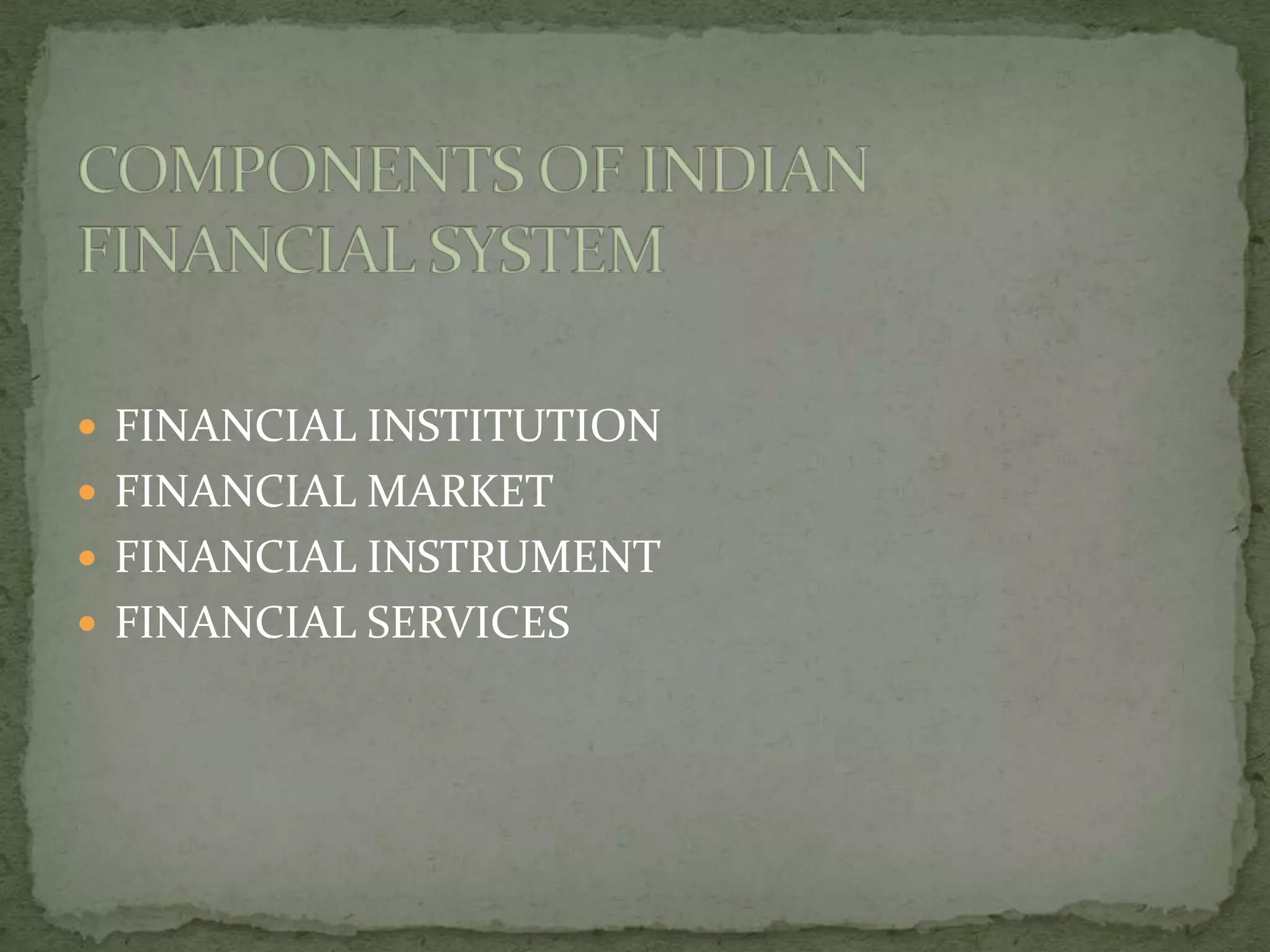

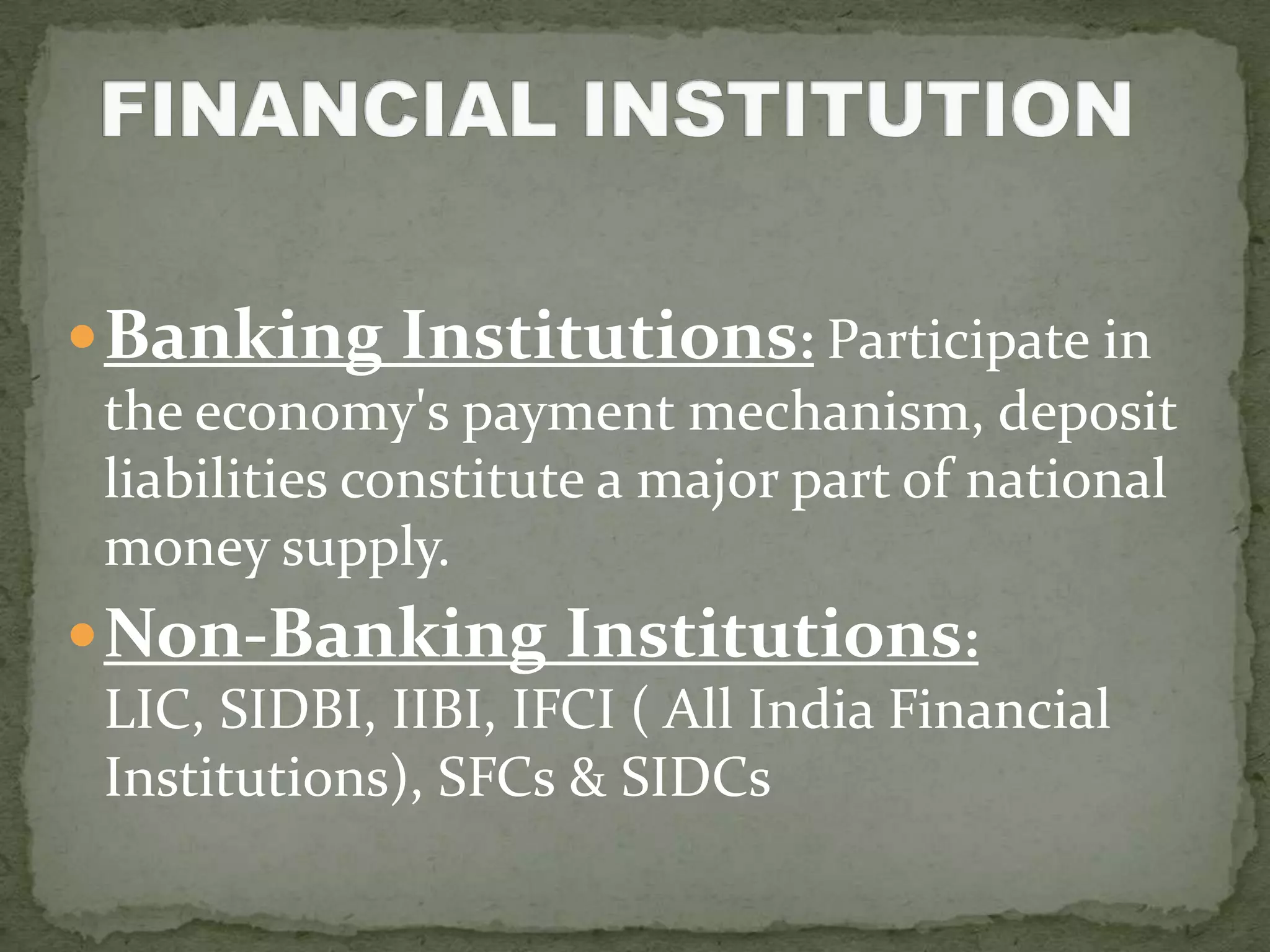

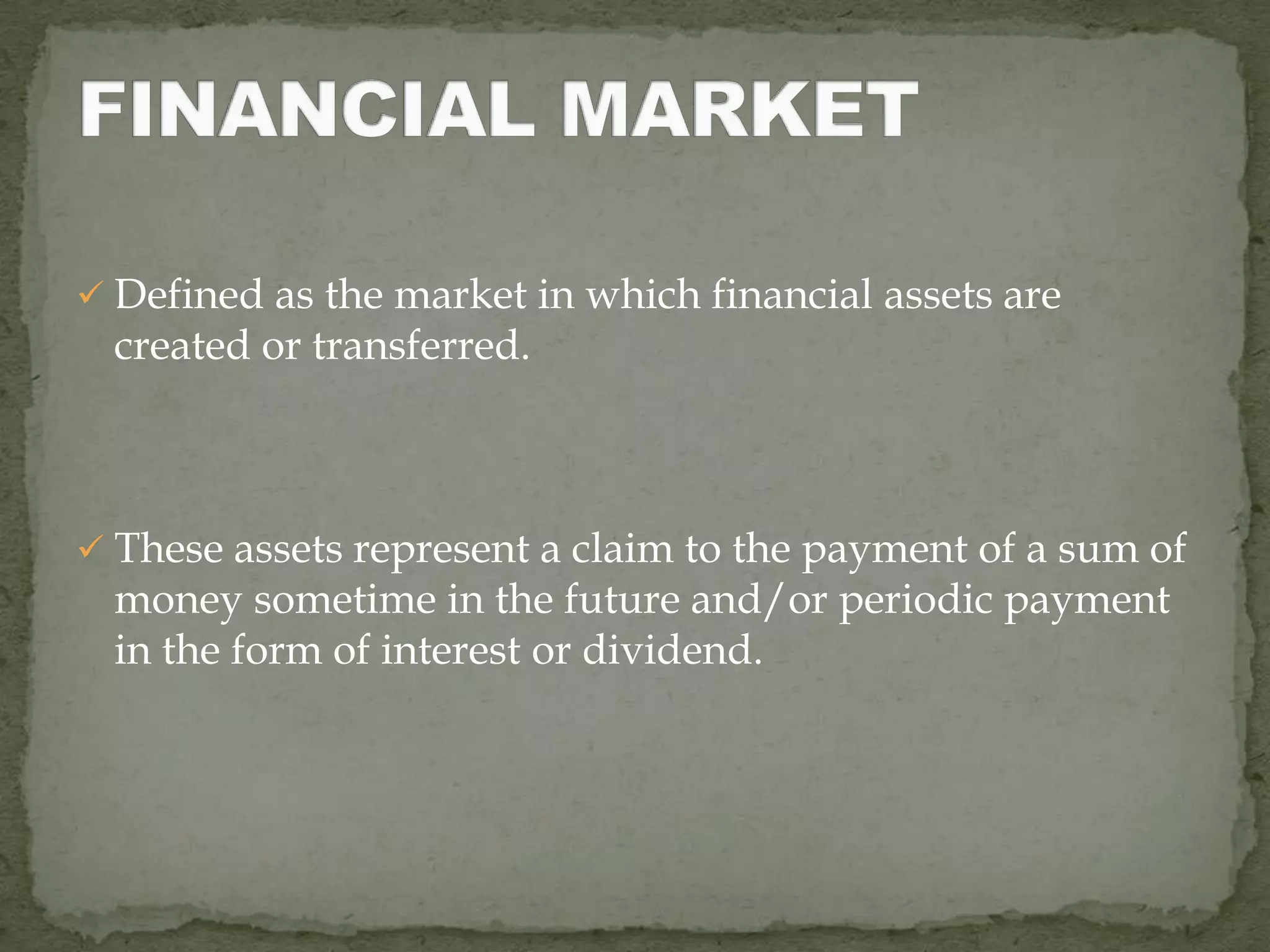

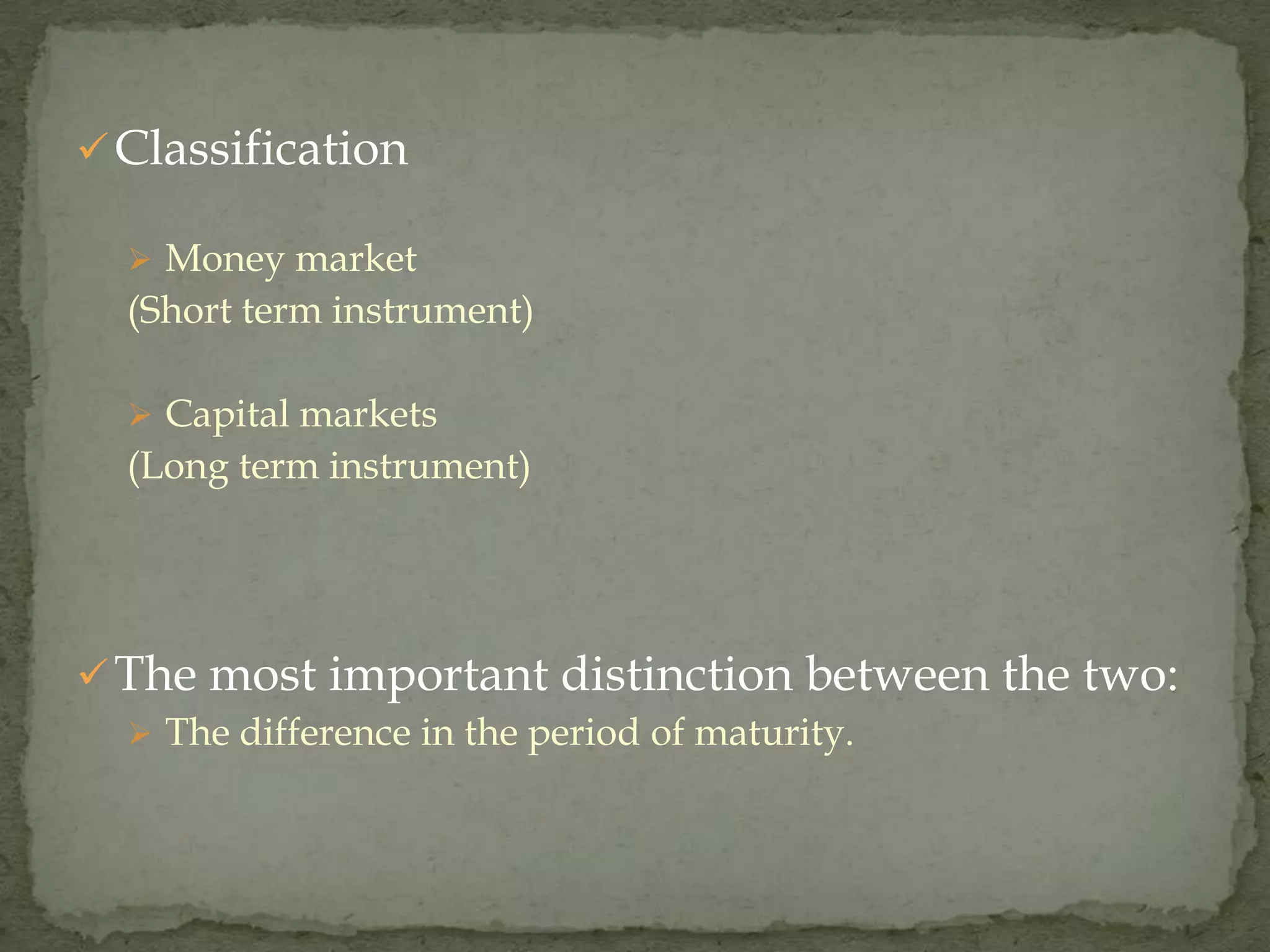

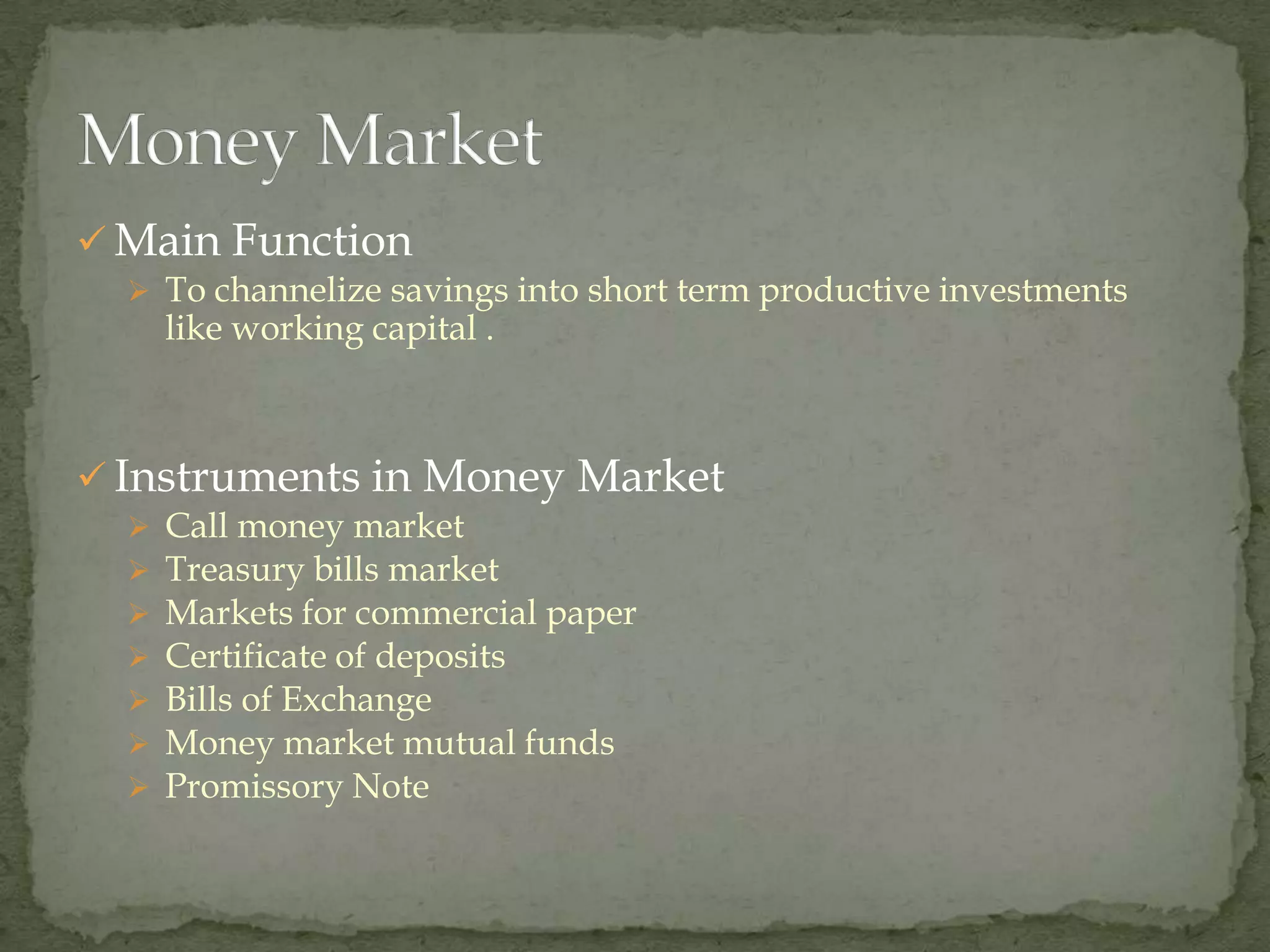

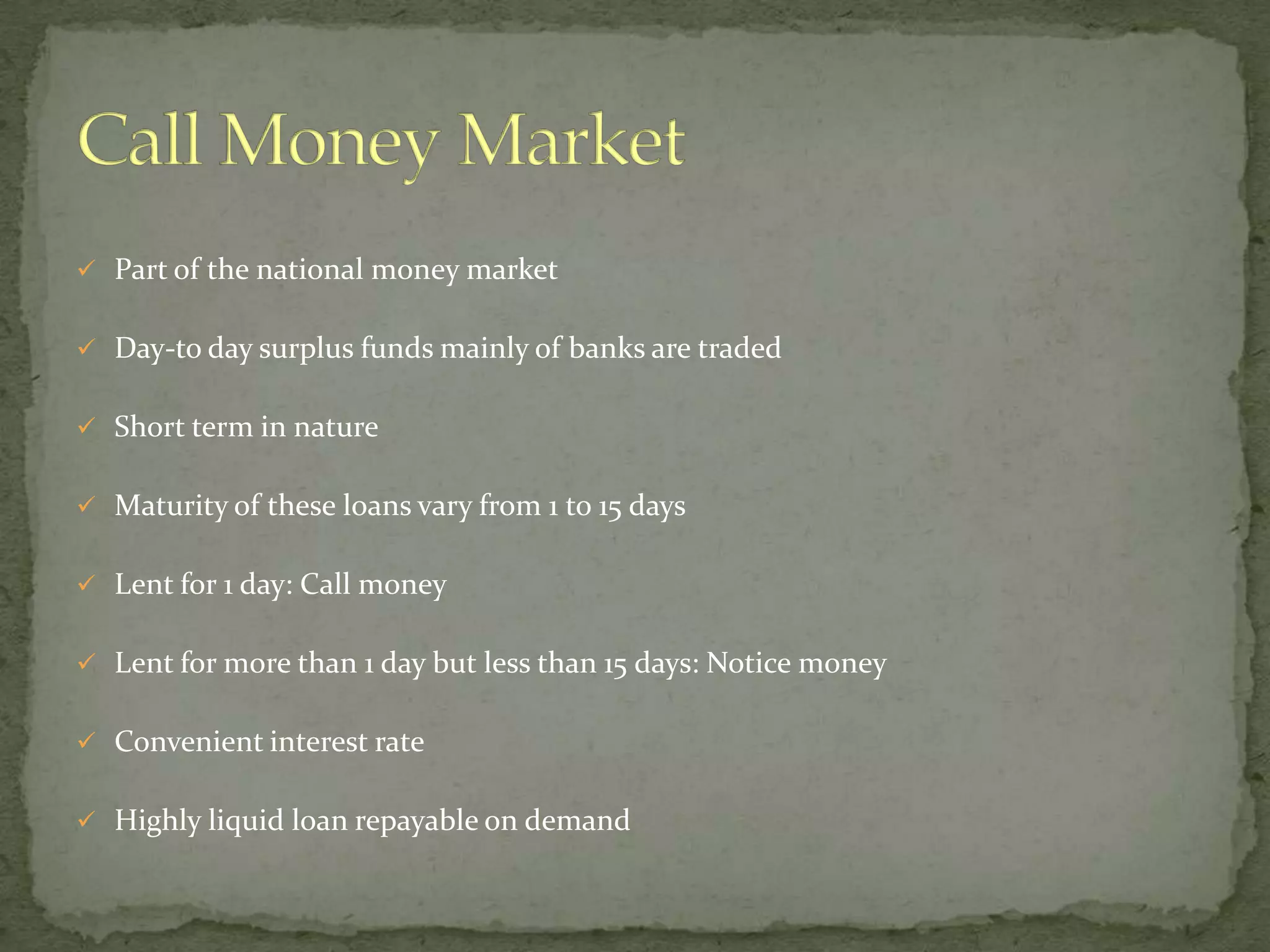

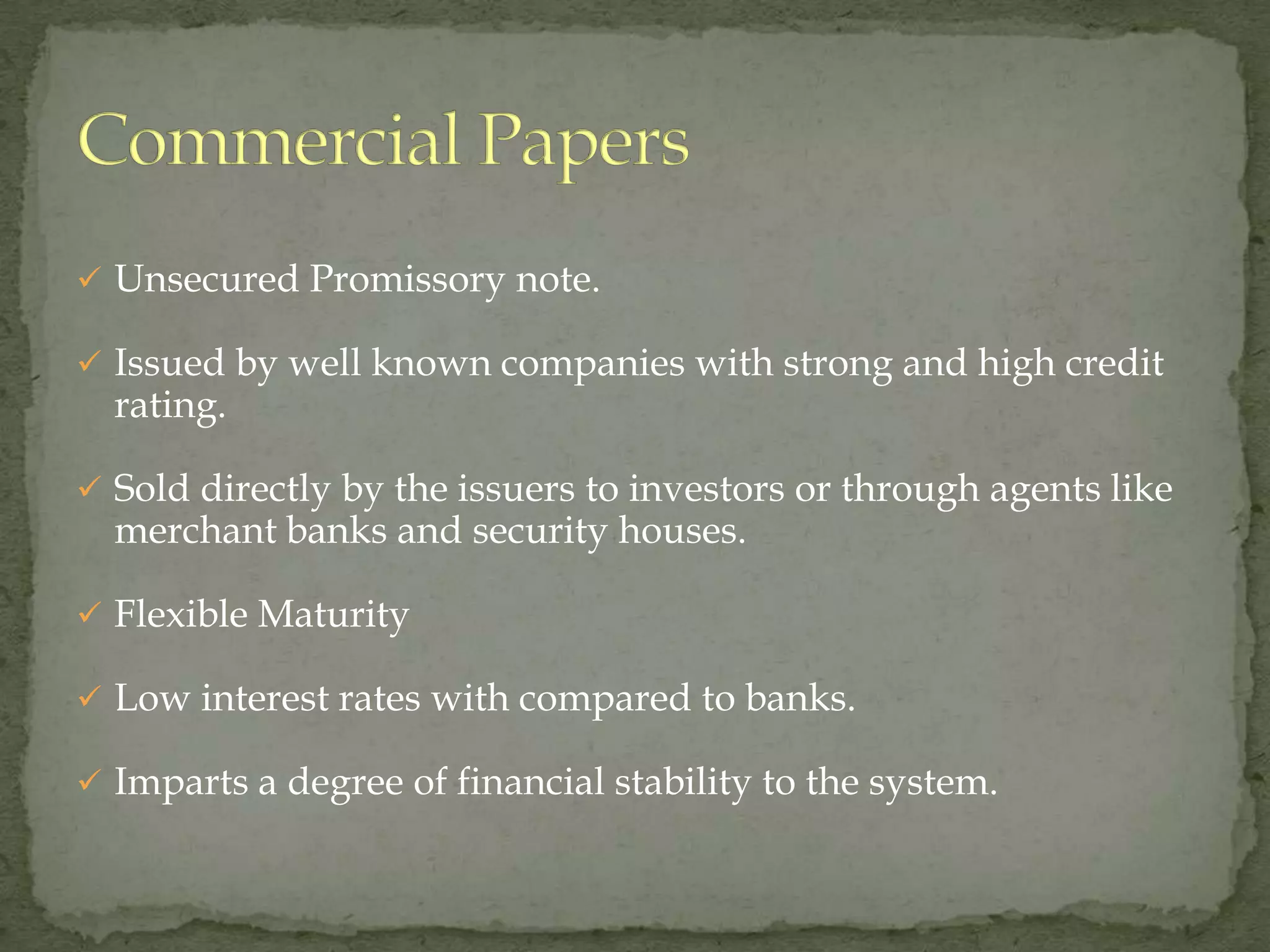

The financial system in India has seen significant changes since independence, facilitating faster economic development. The system links savers and investors through various financial institutions and markets. It provides necessary financial inputs for production through intermediation of funds. The major components of the financial system are banking institutions, non-banking financial institutions, financial markets, and financial instruments. Financial markets include money markets for short-term funds and capital markets for long-term funds. Money markets deal in short-term debt instruments like treasury bills, commercial paper, certificates of deposit, and promissory notes. Capital markets facilitate resource mobilization through primary and secondary markets.

Post-independence economic progress, reliance on voluntary markets, need for efficient financial systems.

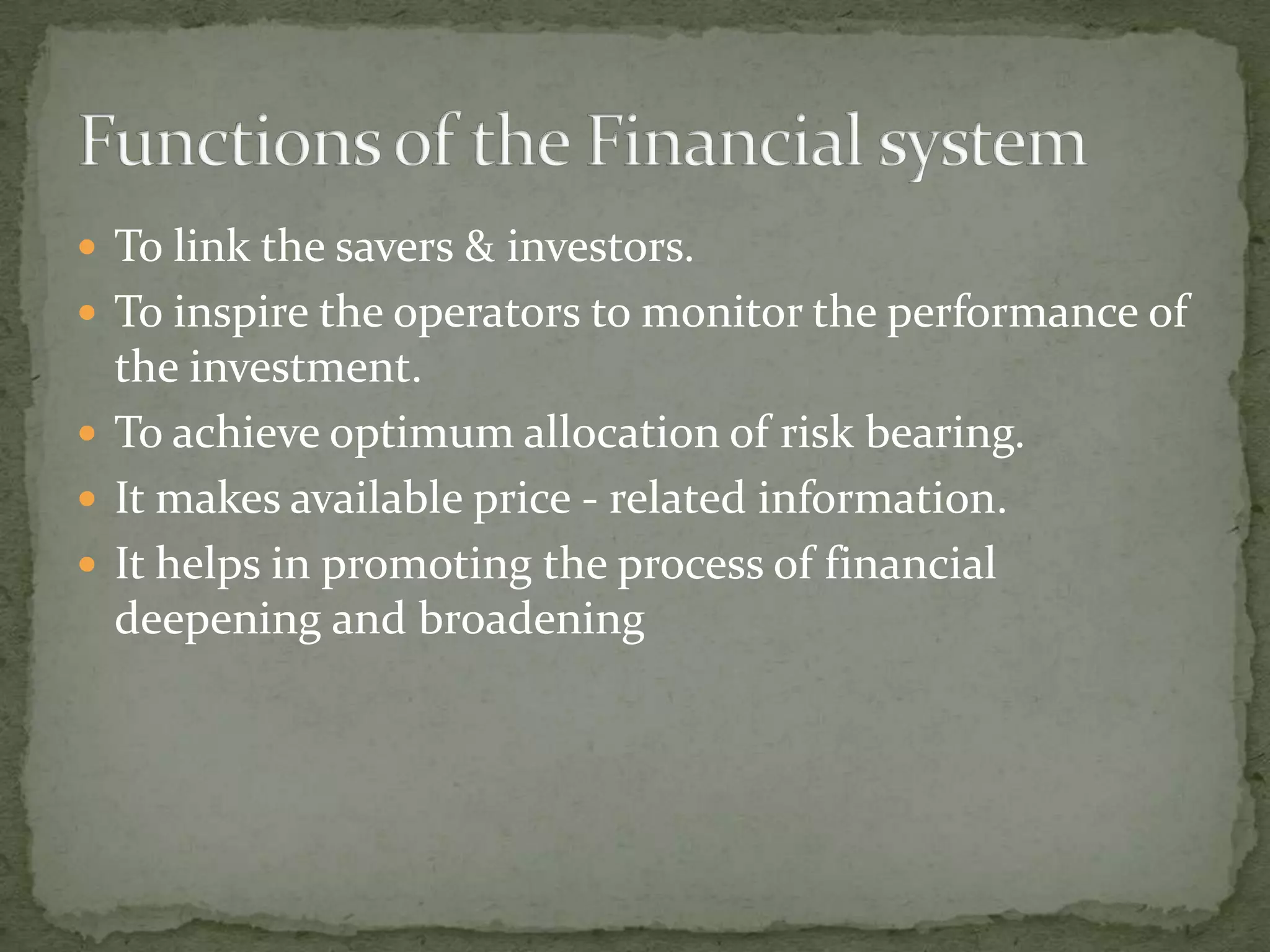

Definition of financial system, includes markets and institutions, aids in the production of goods/services.

Mobilizes savings for investments, promotes economic development, helps in risk allocation and financial deepening.

Includes financial institutions, markets, instruments, and services essential for the economy.

Banking institutions manage payment mechanisms; non-bank institutions include LIC and various All India Financial Institutions.

Markets where financial assets are created or transferred, classified as money market (short-term) and capital market (long-term).

Facilitates short-term investment and liquidity; includes various instruments like T-bills, commercial papers.

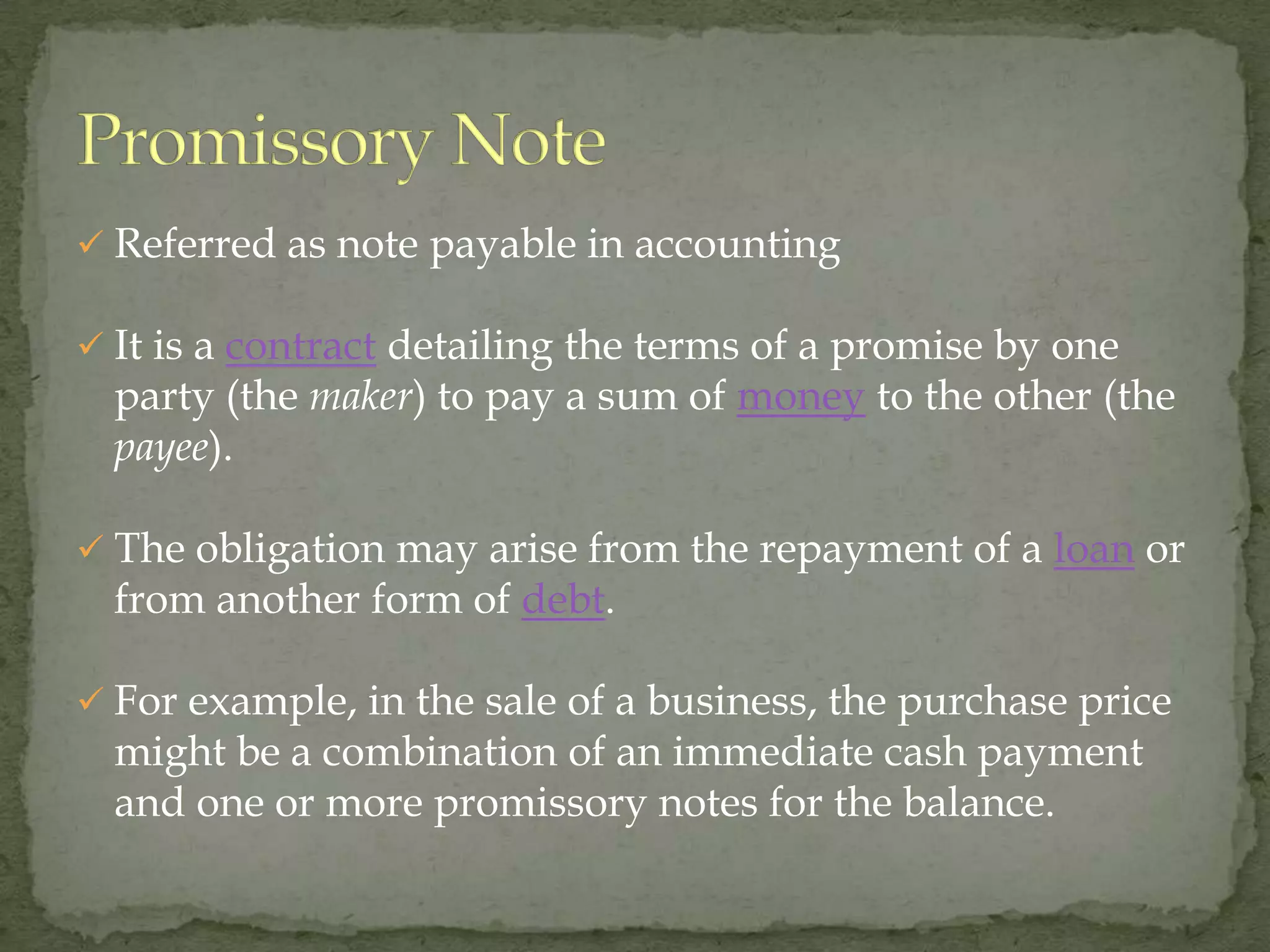

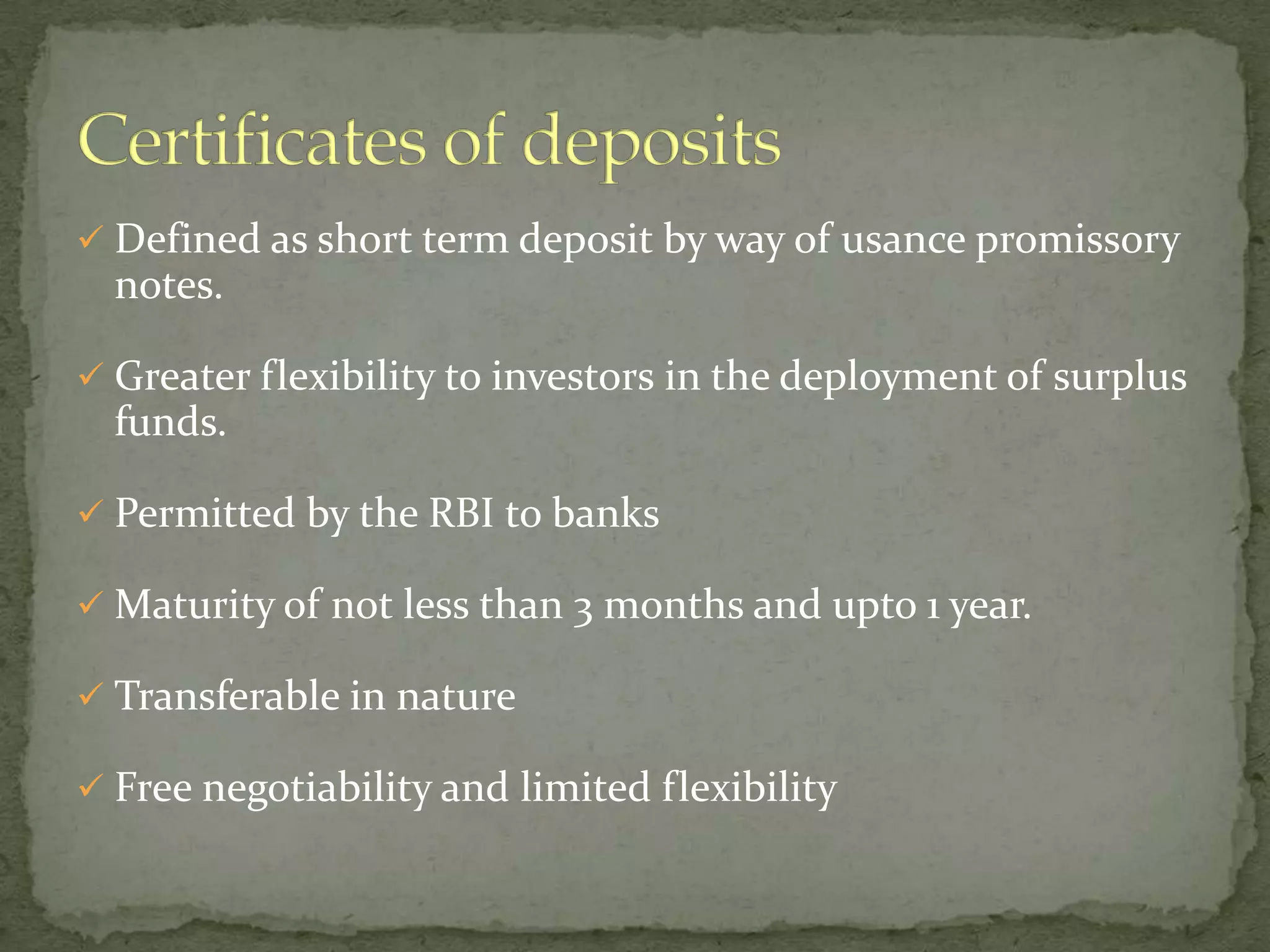

Details on unsecured promissory notes, their features, and the mechanics of usance promissory notes.

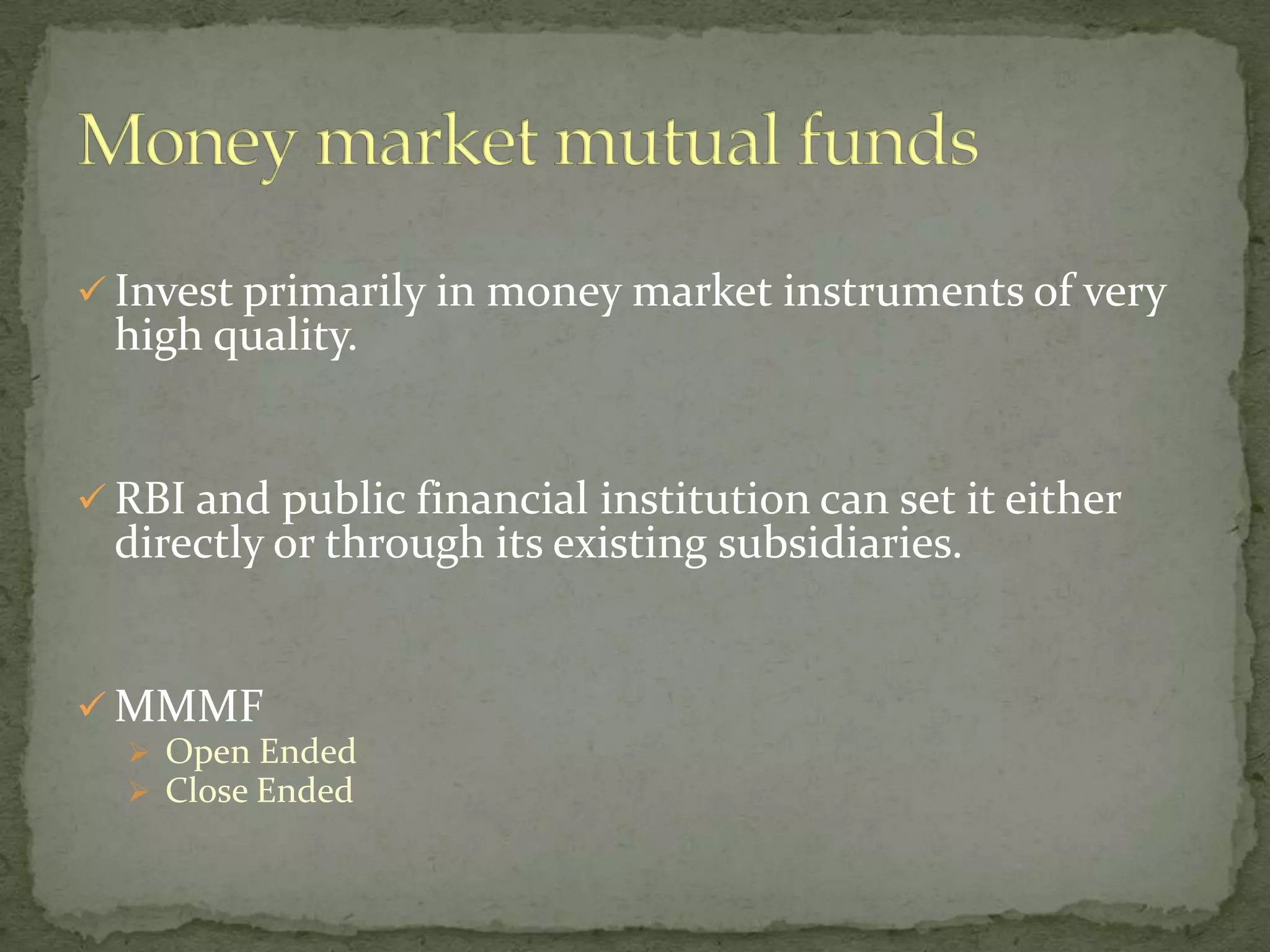

Investment in high-quality money market instruments, types of MMMFs, and their operation.

Provides funding for medium and large-scale industry activities, emphasizing expansion and investments.

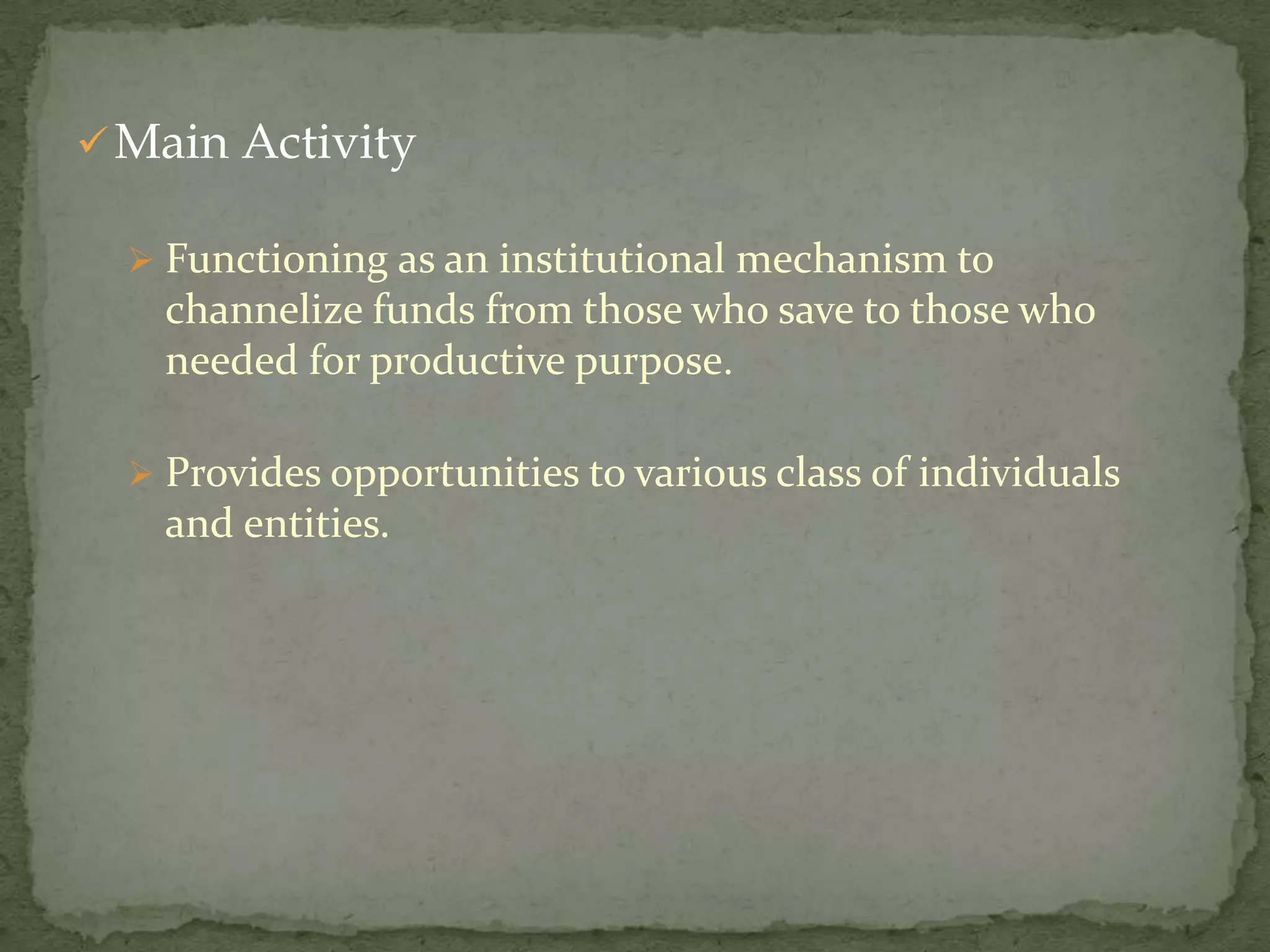

Mechanism for channeling funds from savers to productive uses, opportunities for various stakeholders.

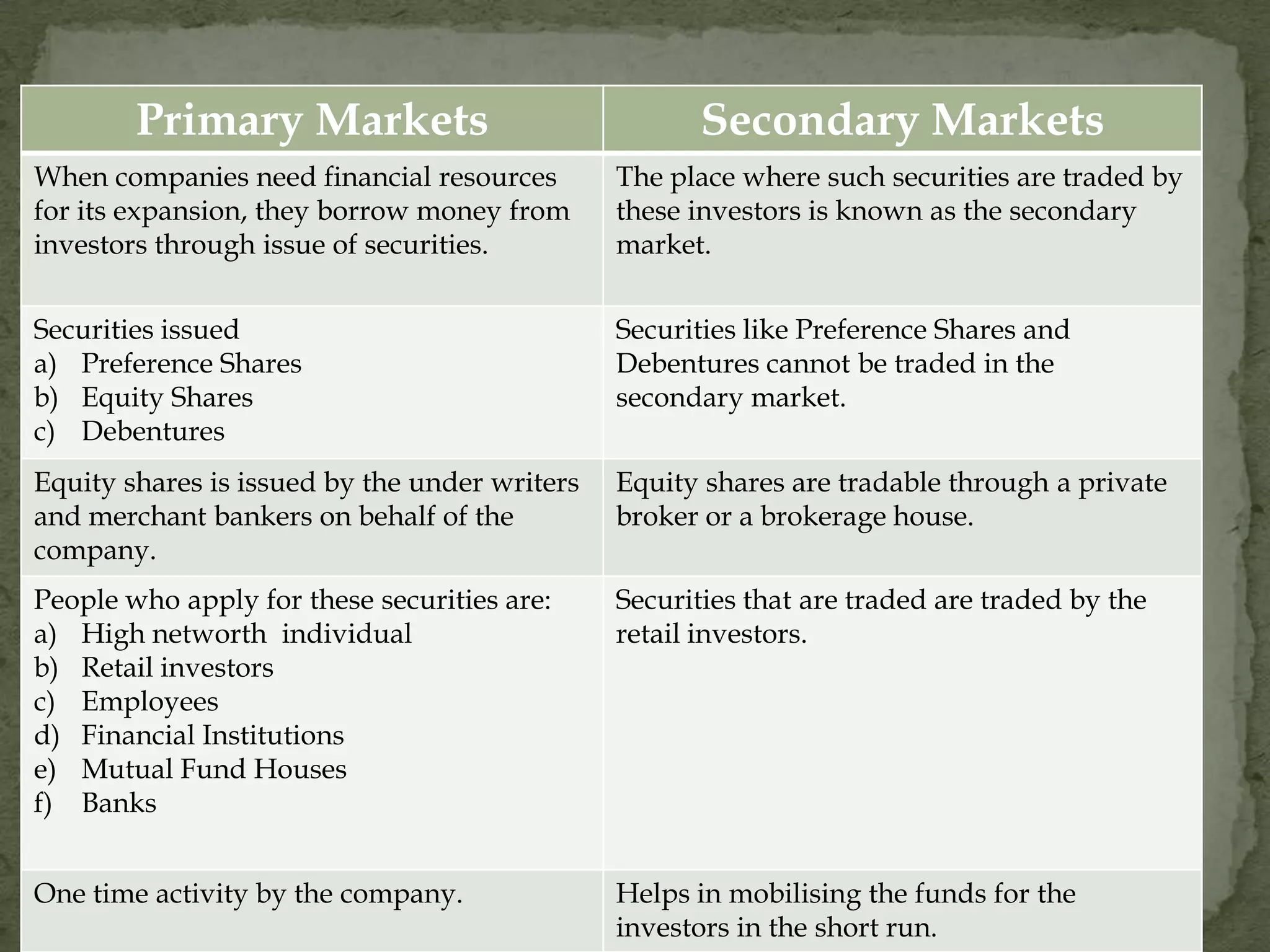

Distinction between primary markets for issuing securities and secondary markets for trading them.

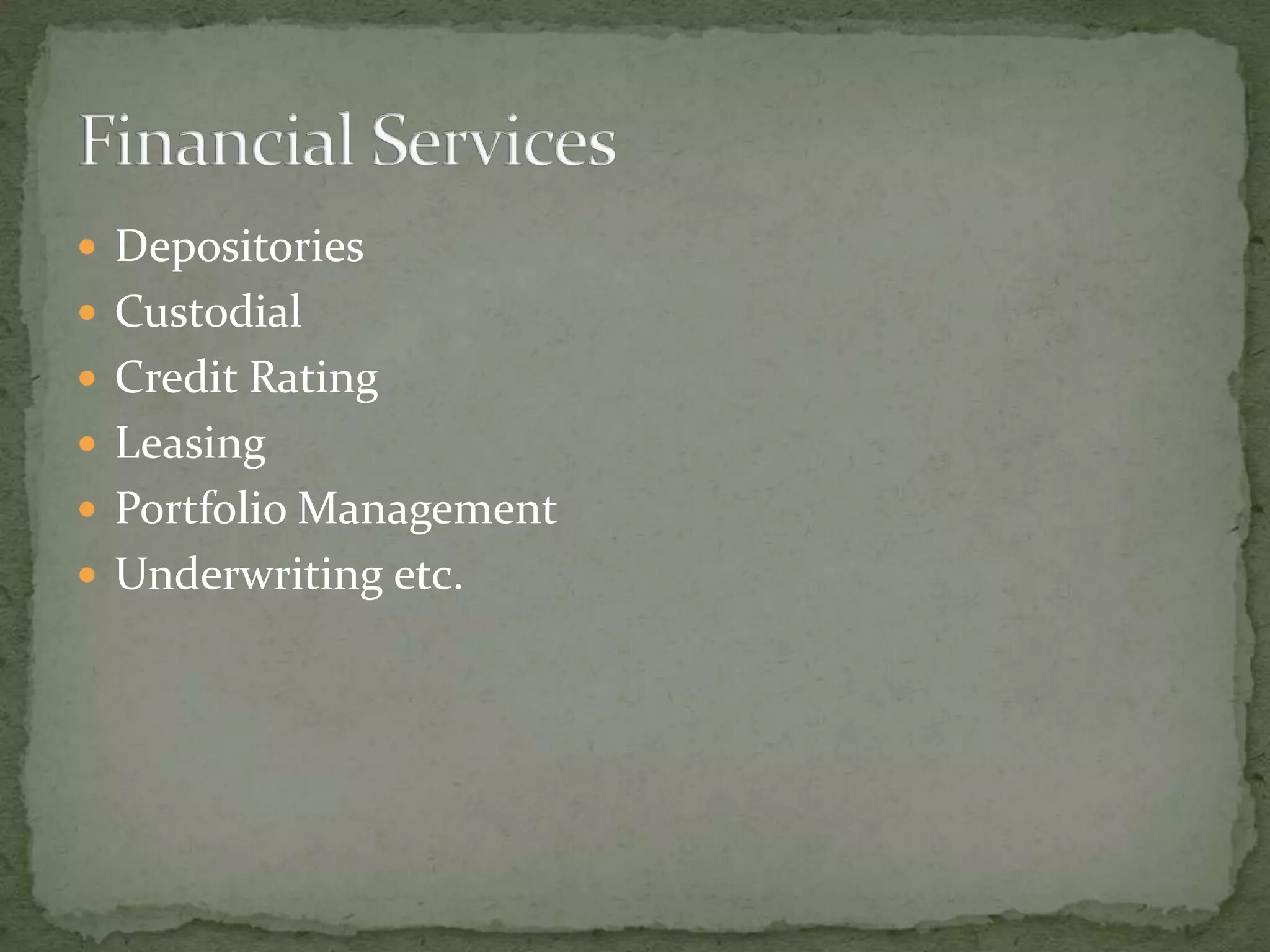

Services supporting financial markets such as depositories, custodial services, credit rating, and leasing.

Thank-you note, concluding the presentation.

![Where to Buy LinkedIn Accounts_ [12 Best Sites] (2).pdf](https://cdn.slidesharecdn.com/ss_thumbnails/wheretobuylinkedinaccounts12bestsites2-251124191348-c246988b-thumbnail.jpg?width=640&height=640&fit=bounds)