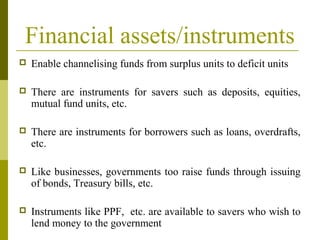

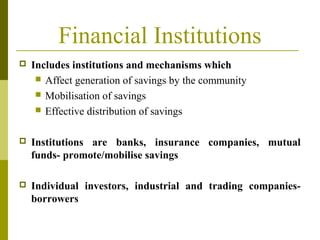

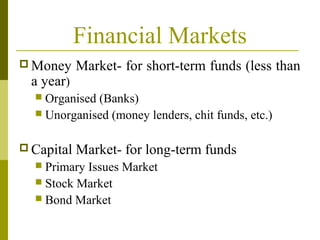

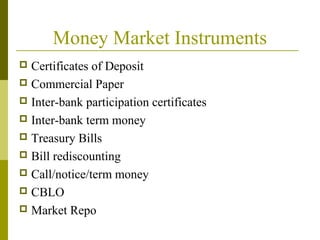

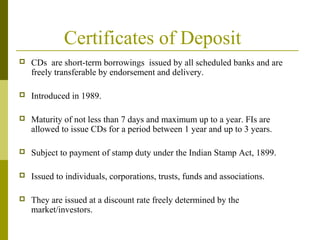

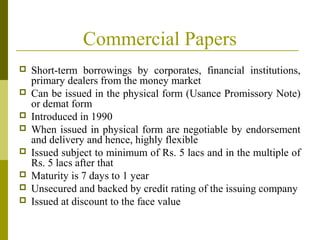

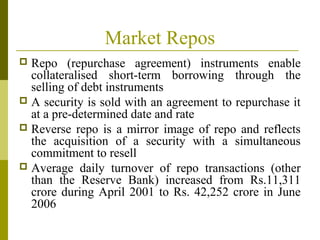

The document provides an overview of the Indian financial system. It discusses the three main parts of a financial system: financial assets/instruments, financial institutions, and financial markets. It then goes on to describe various financial assets like deposits, loans, bonds, and equities. It also discusses important financial institutions like banks, insurance companies, and mutual funds. Key financial markets like the money market, capital market, and foreign exchange market are also outlined. The document provides details on key components of the Indian financial system like money market instruments, commercial banks, cooperative banks, and financial intermediaries.

![Indian financial system[1]](https://cdn.slidesharecdn.com/ss_thumbnails/indianfinancialsystem1-130511123055-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Eco presentation1[2]](https://cdn.slidesharecdn.com/ss_thumbnails/ecopresentation12-120927080734-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)