Download as PDF, PPTX

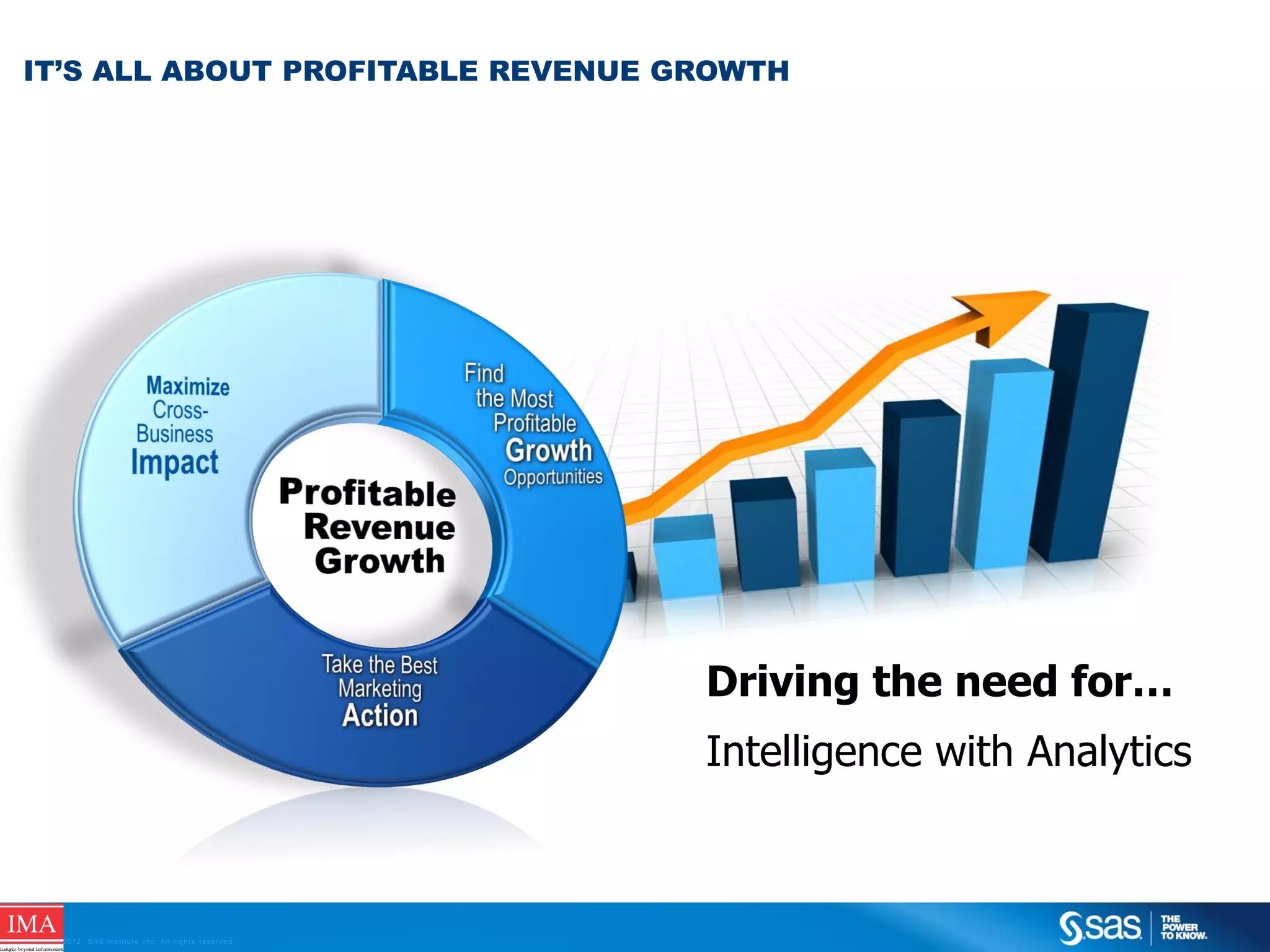

Emerging technologies are reshaping business by driving innovation and optimization, requiring new strategies and the ability to take risks. Analytics and big data are essential for understanding customer behavior and enhancing decision-making, ultimately leading to profitable growth. Organizations must adapt quickly to changing conditions, leveraging insights to stay competitive in a rapidly evolving landscape.