Downloaded 924 times

The document discusses internal controls and control self-assessment. It begins with definitions of internal control and internal auditing. It then outlines the COSO internal control framework, including the five components and seventeen underlying principles of internal control. The presentation agenda and a case study are also mentioned. Sample templates for evaluating internal controls against the principles are included.

Presentation on internal control concepts and self-assessment by CA Manoj Agarwal. Disclaimer on speaker opinions.

Agenda covers main topics: Internal Control, Control Self Assessment, Case Study, and Q&A.

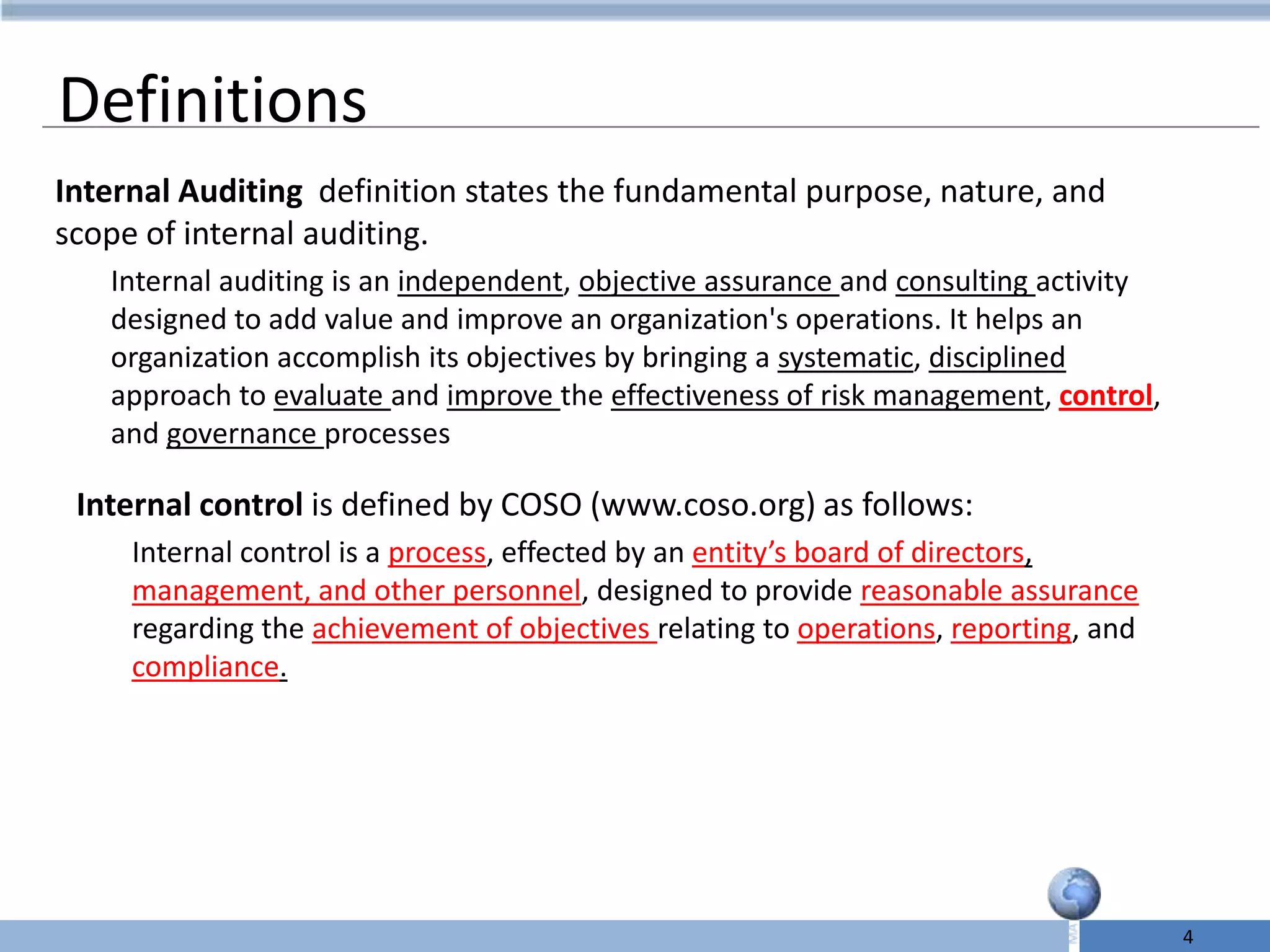

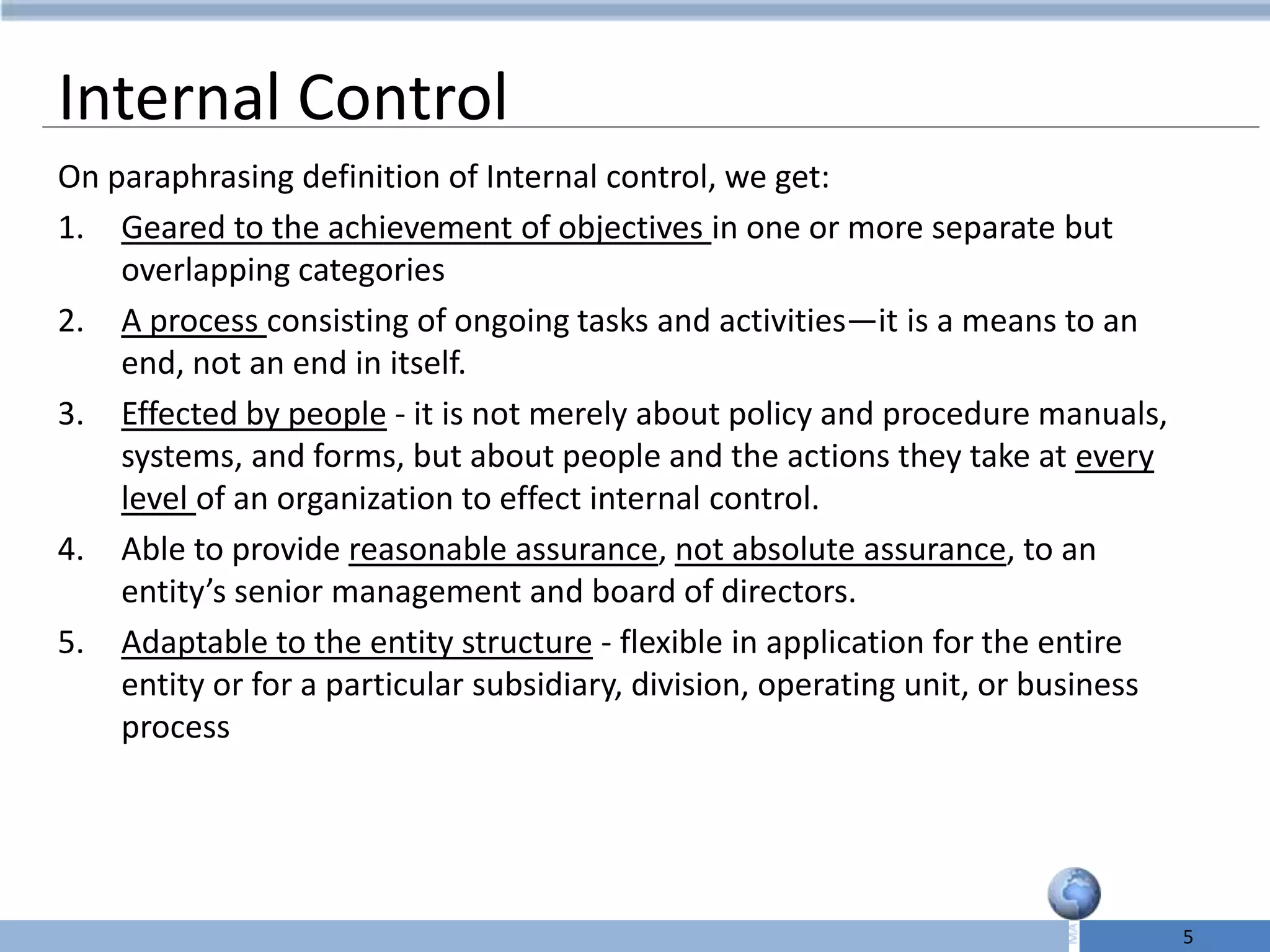

Definitions highlighting internal auditing, its objective, and COSO's definition of internal control, emphasizing assurance and governance.

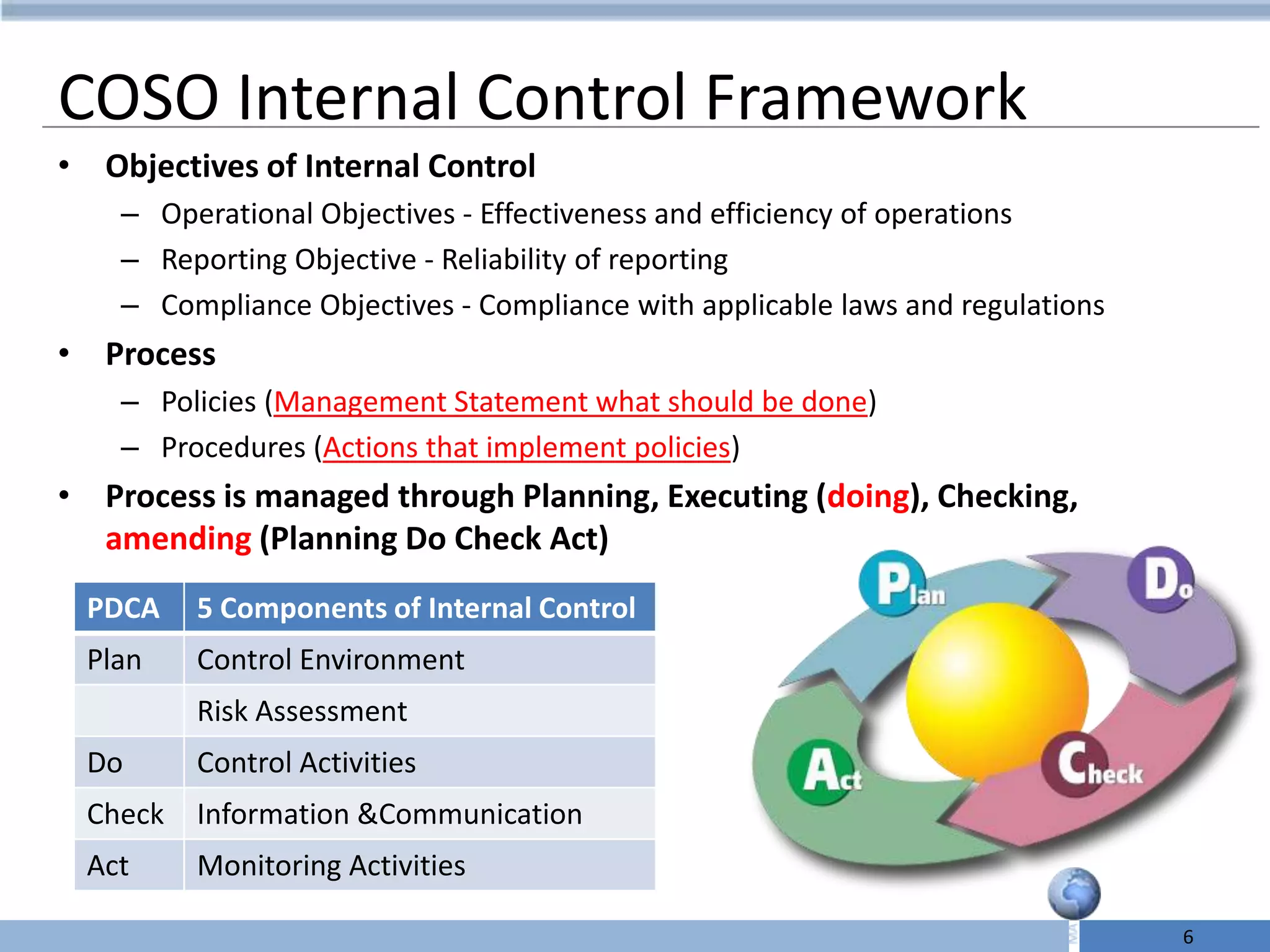

Details internal control's goals (operations, reporting, compliance), processes, and a framework including PDCA with five components.

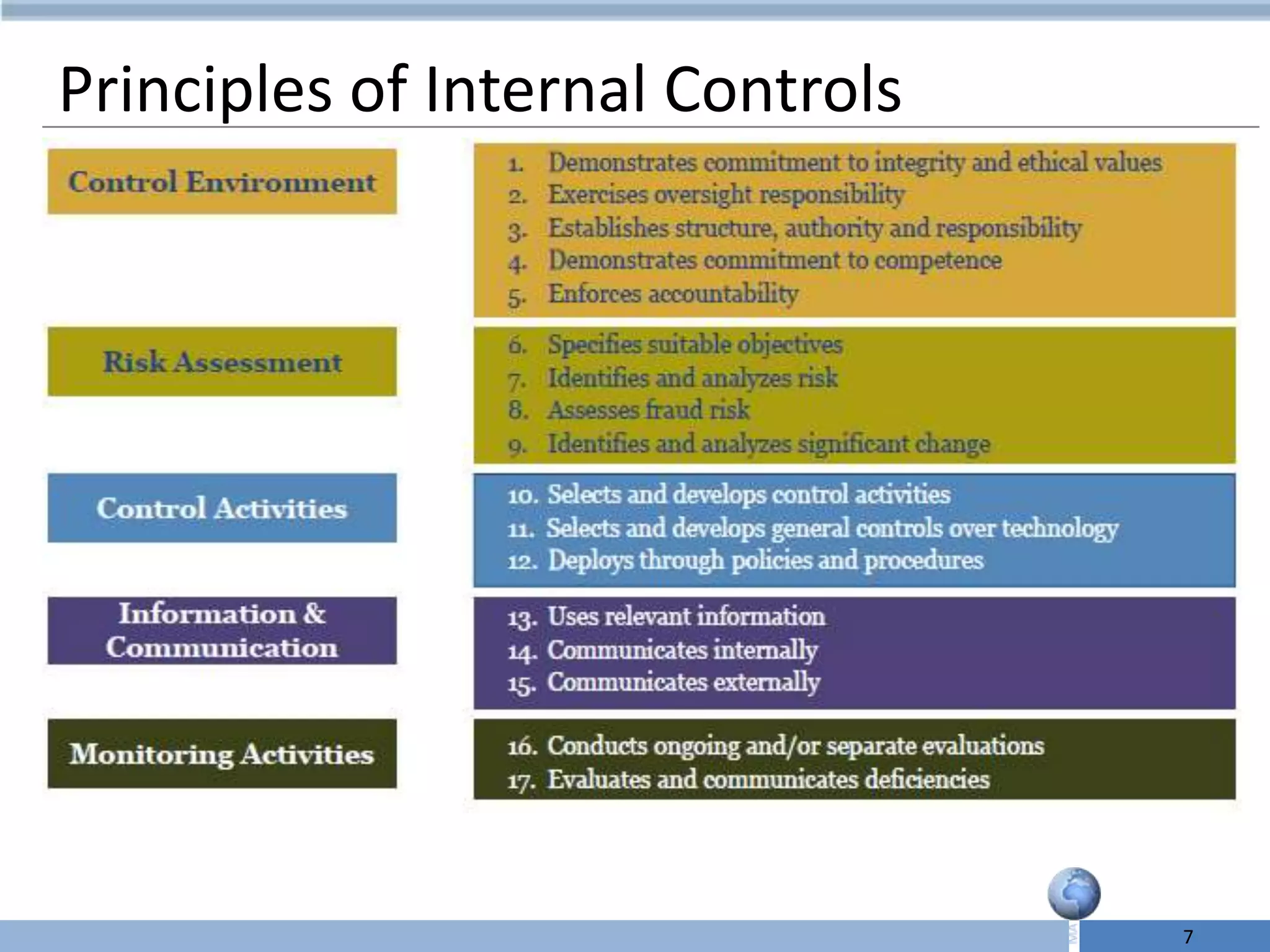

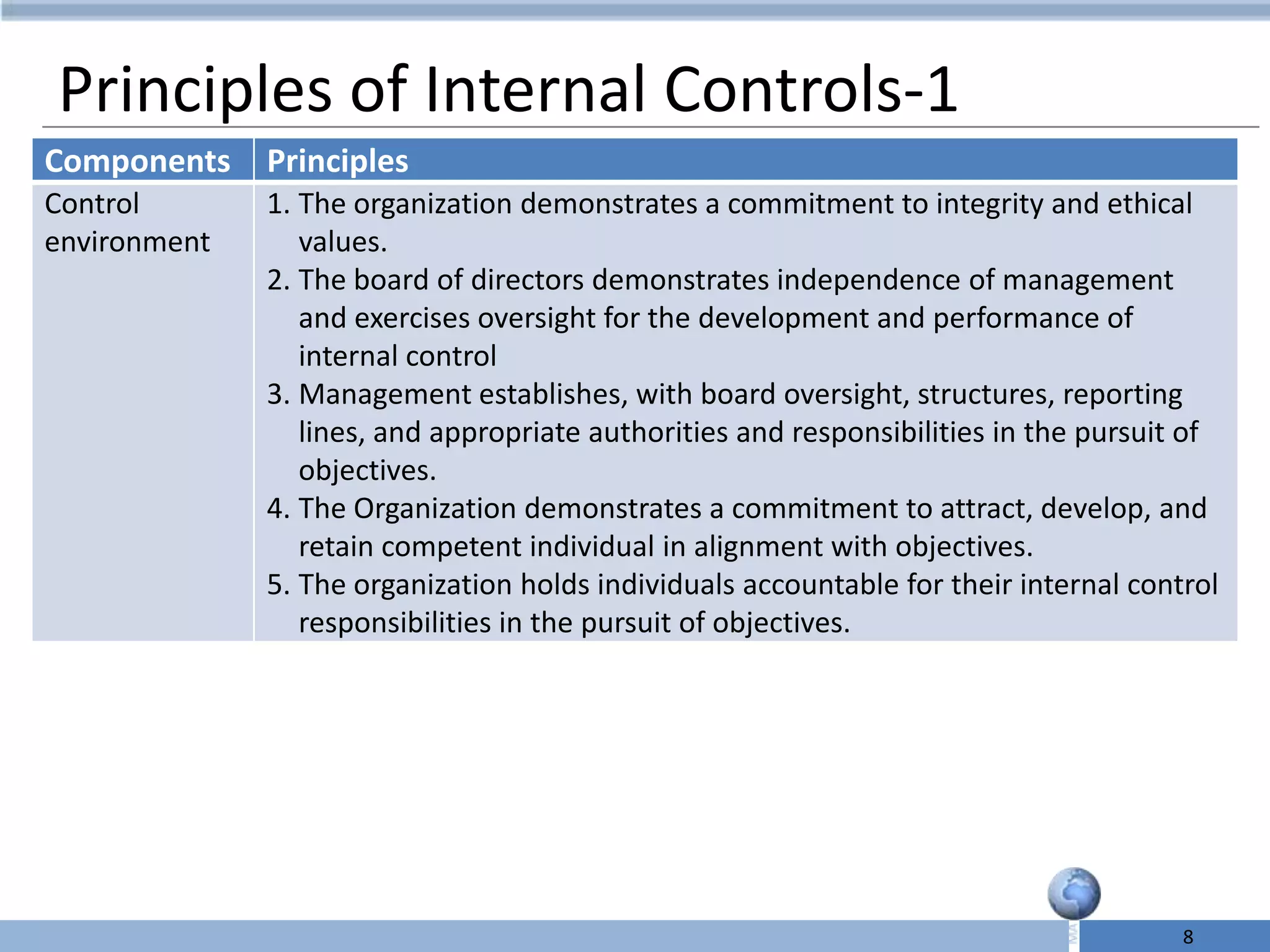

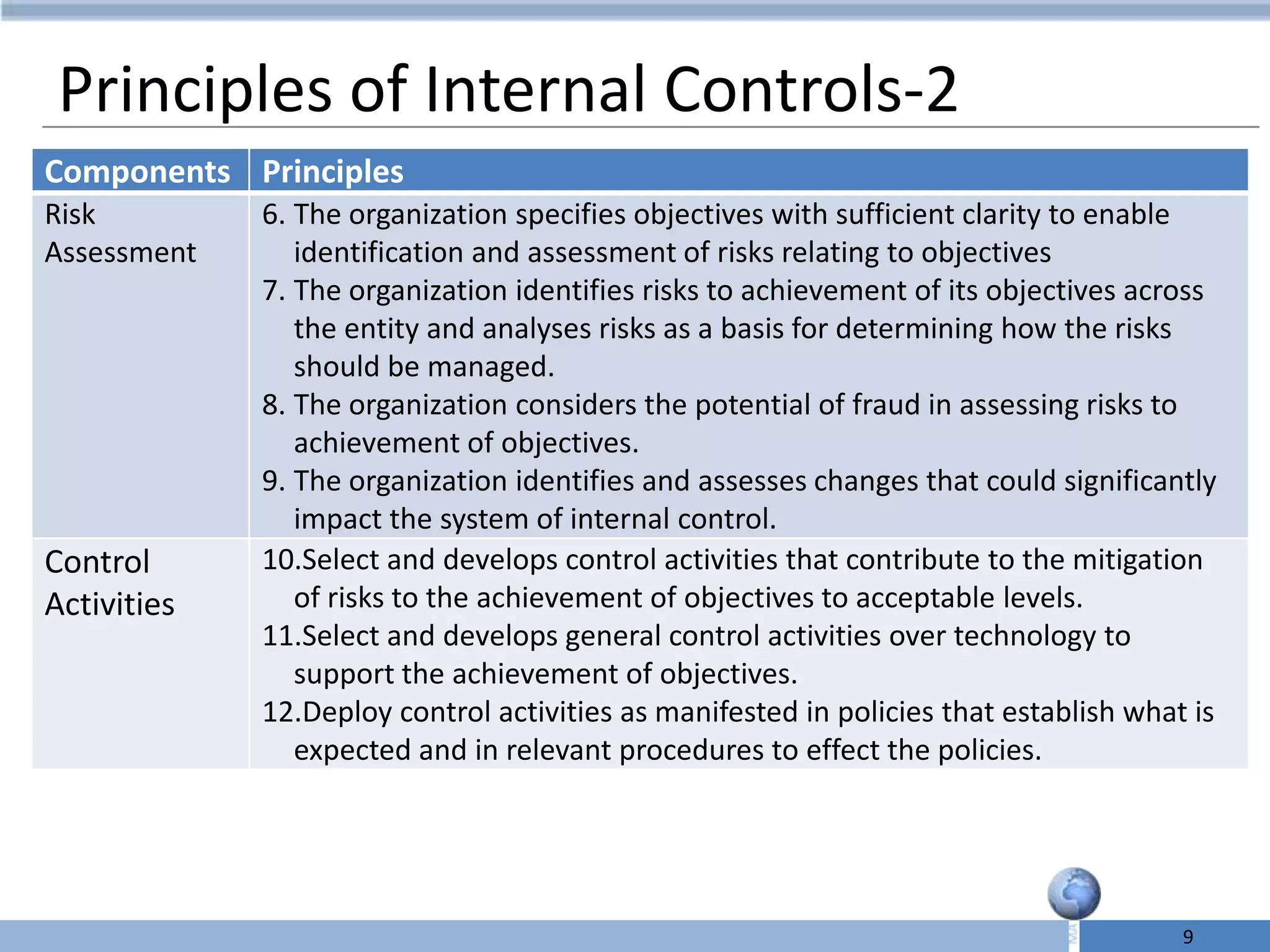

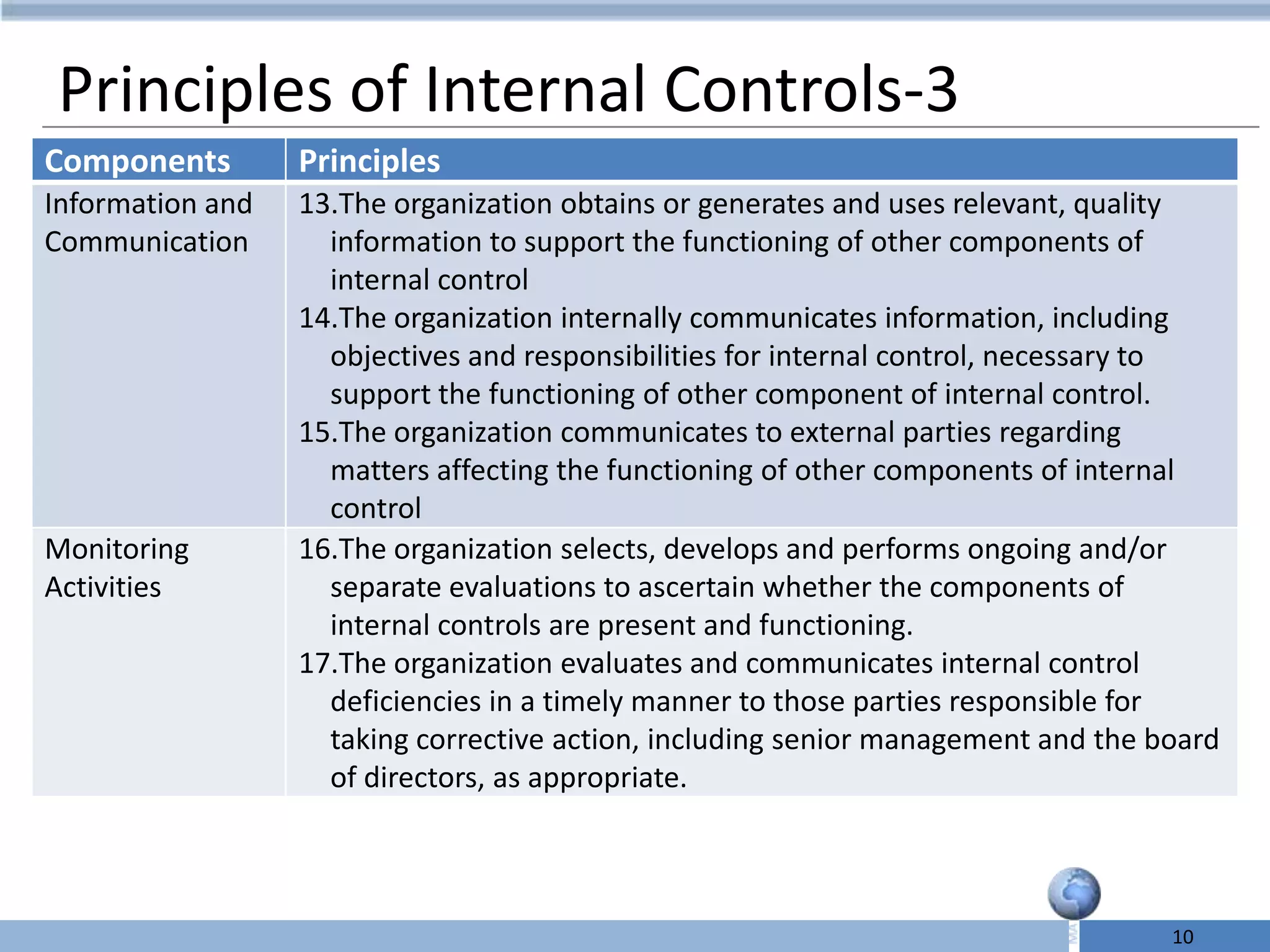

Principles of internal control covering control environment, risk assessment, control activities, communication, and monitoring activities.

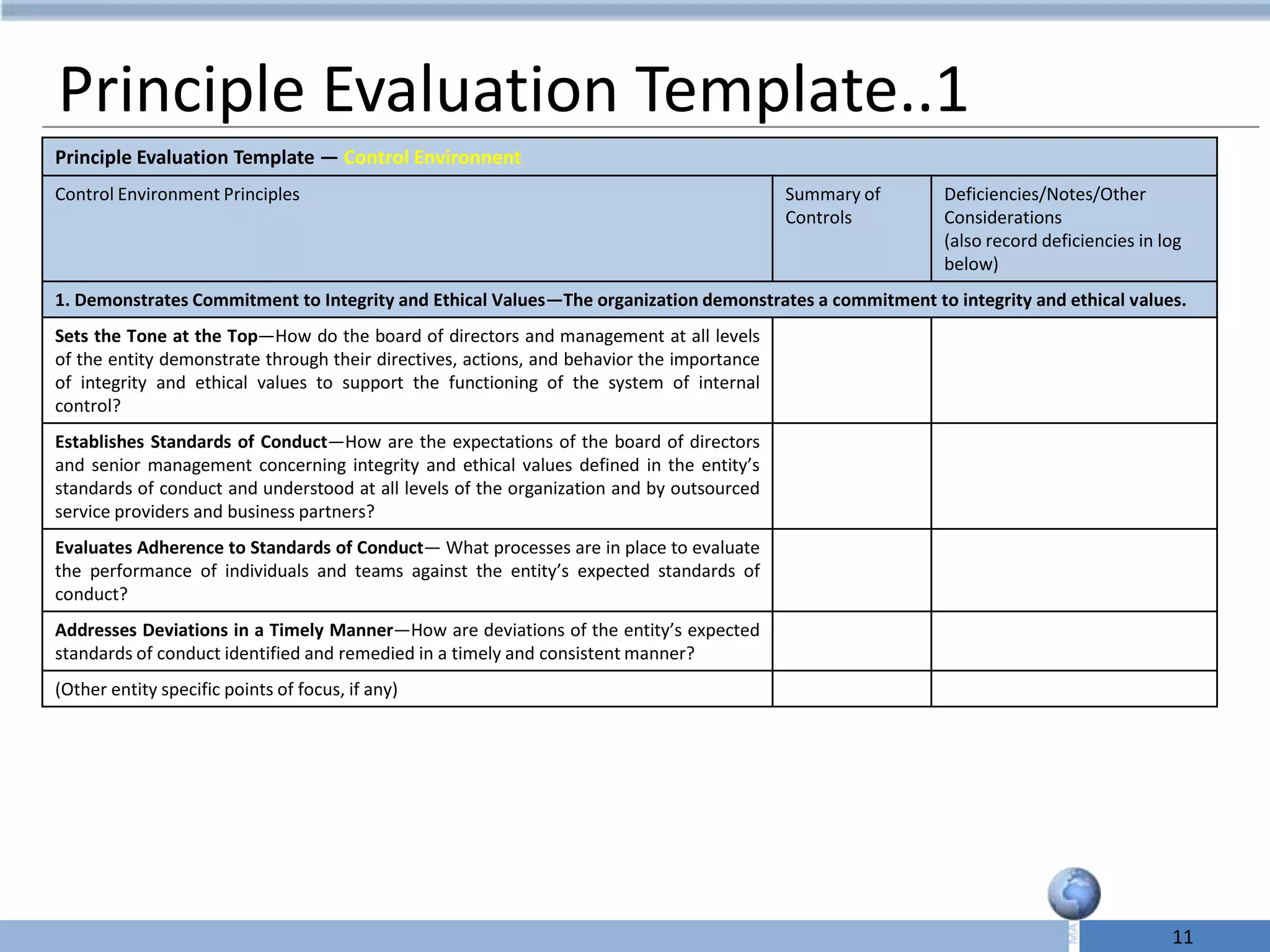

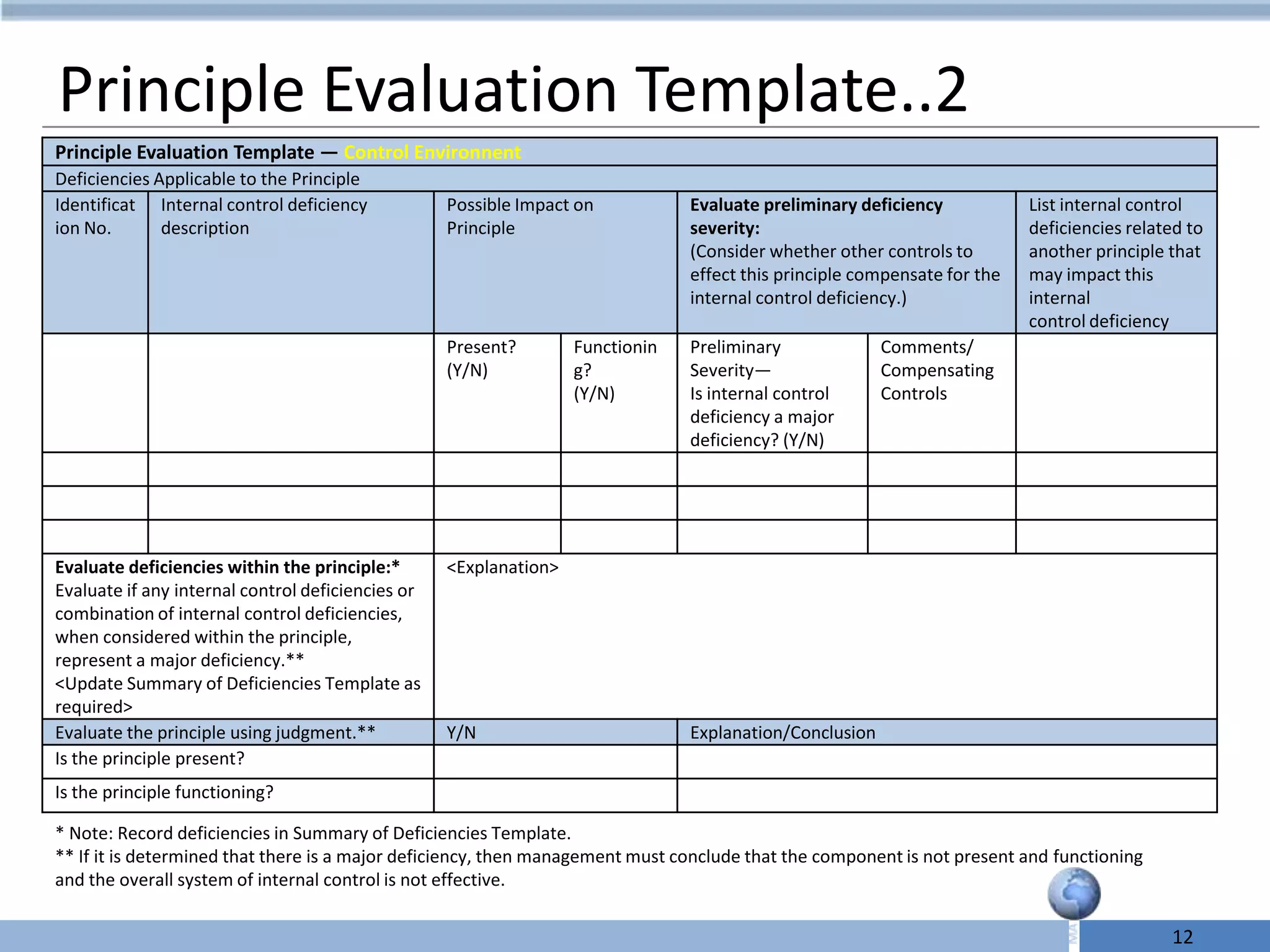

Templates to evaluate control principles, assessing commitment to integrity, ethical values, and adherence to standards.

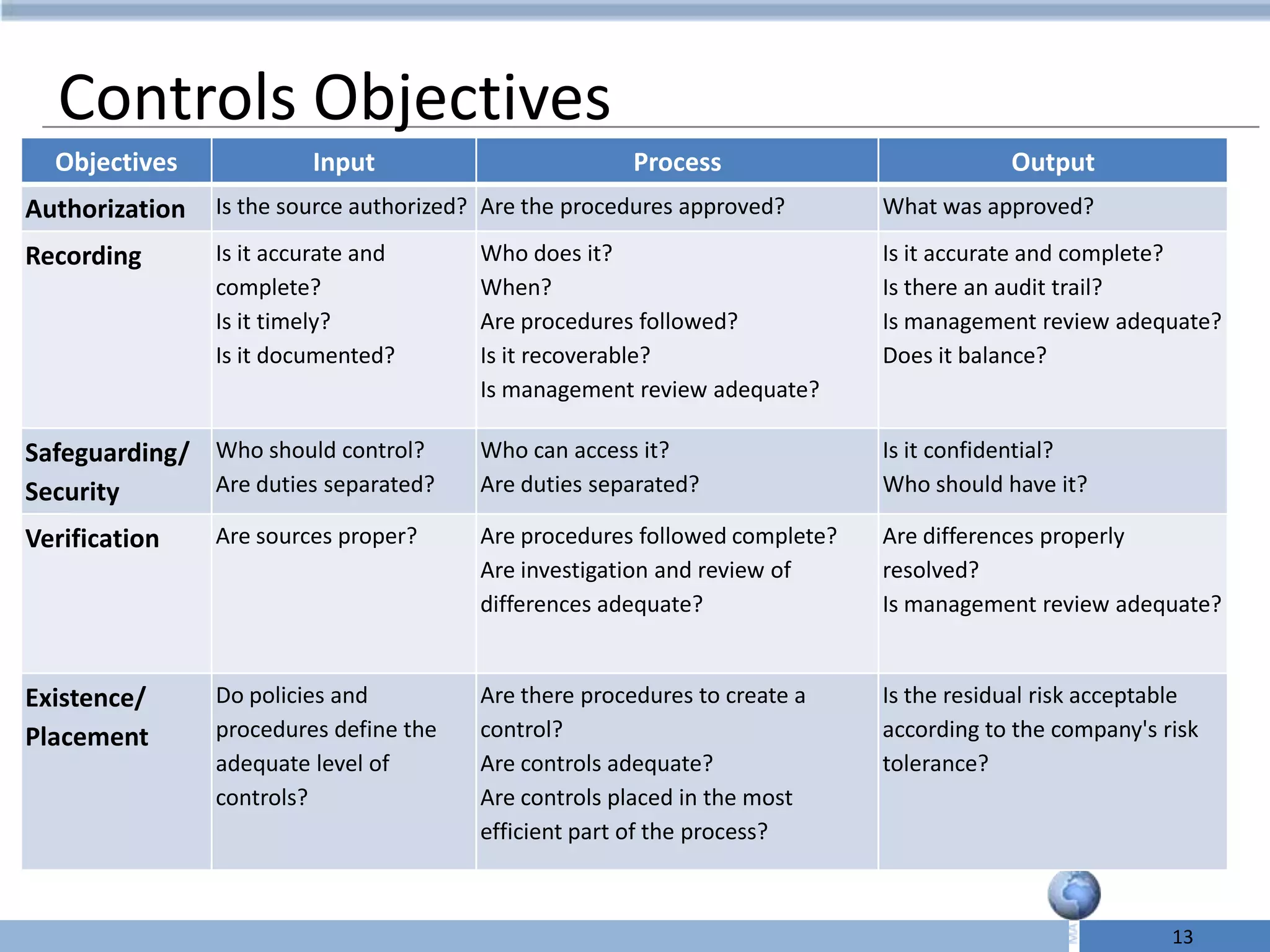

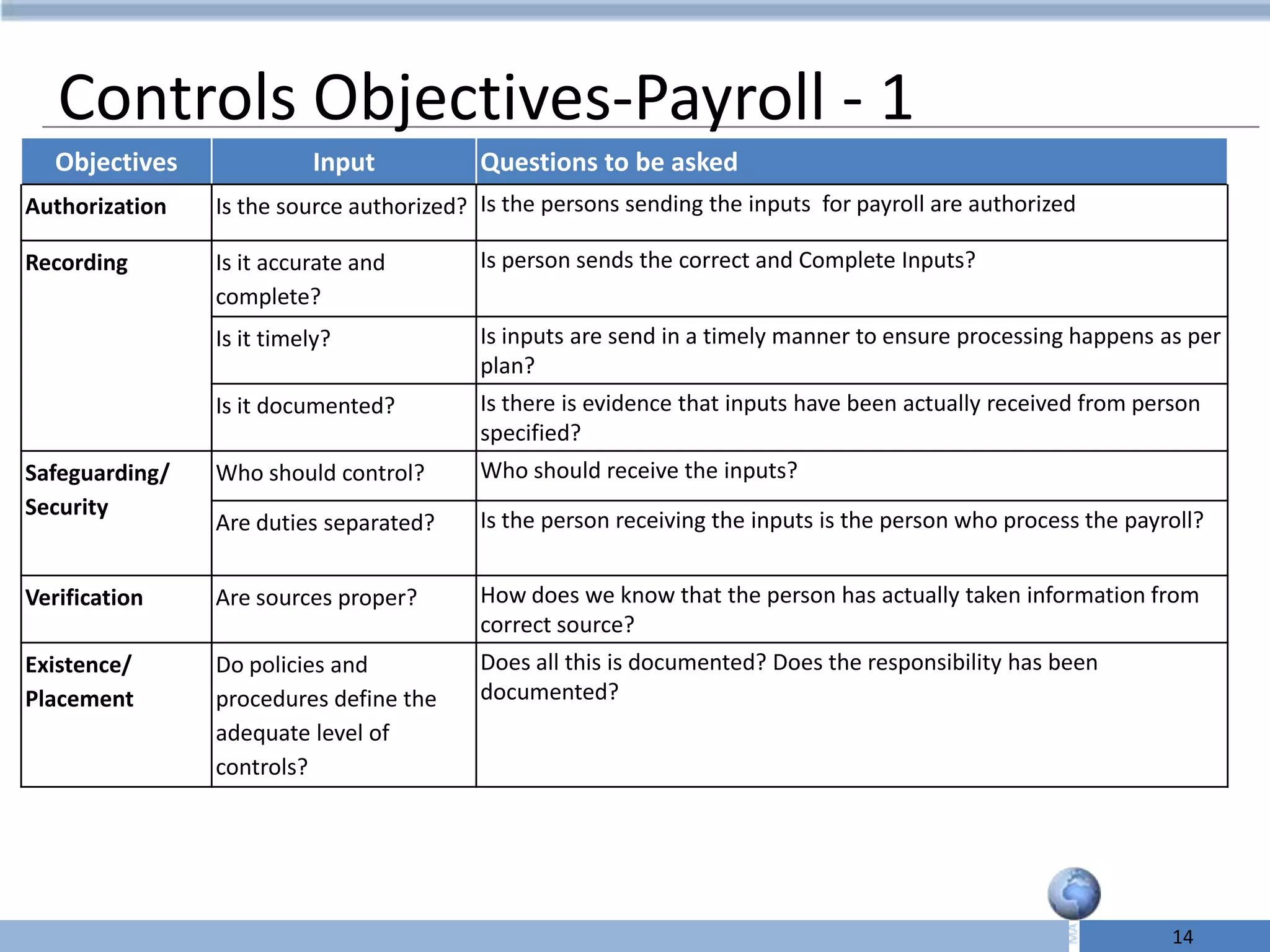

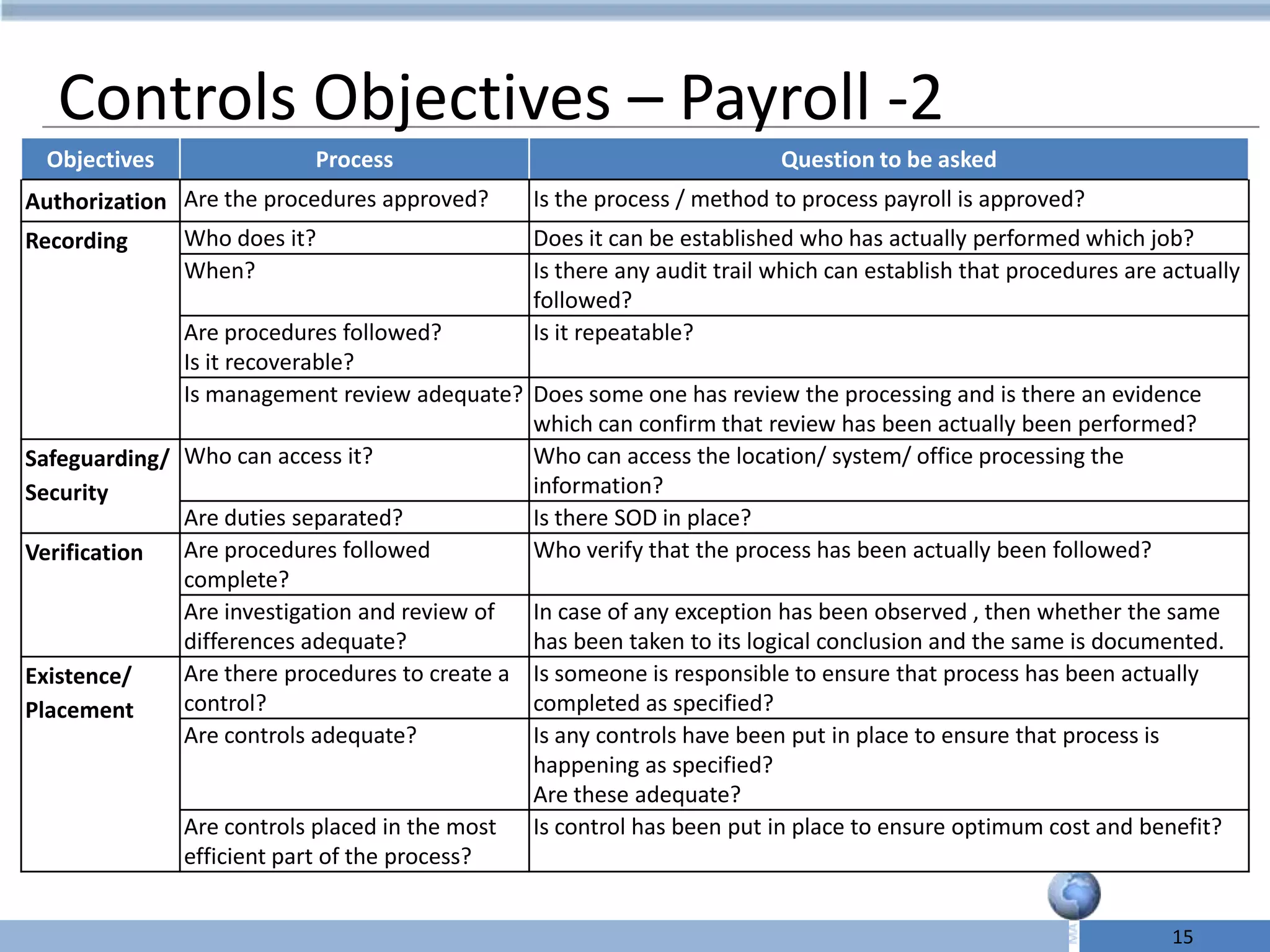

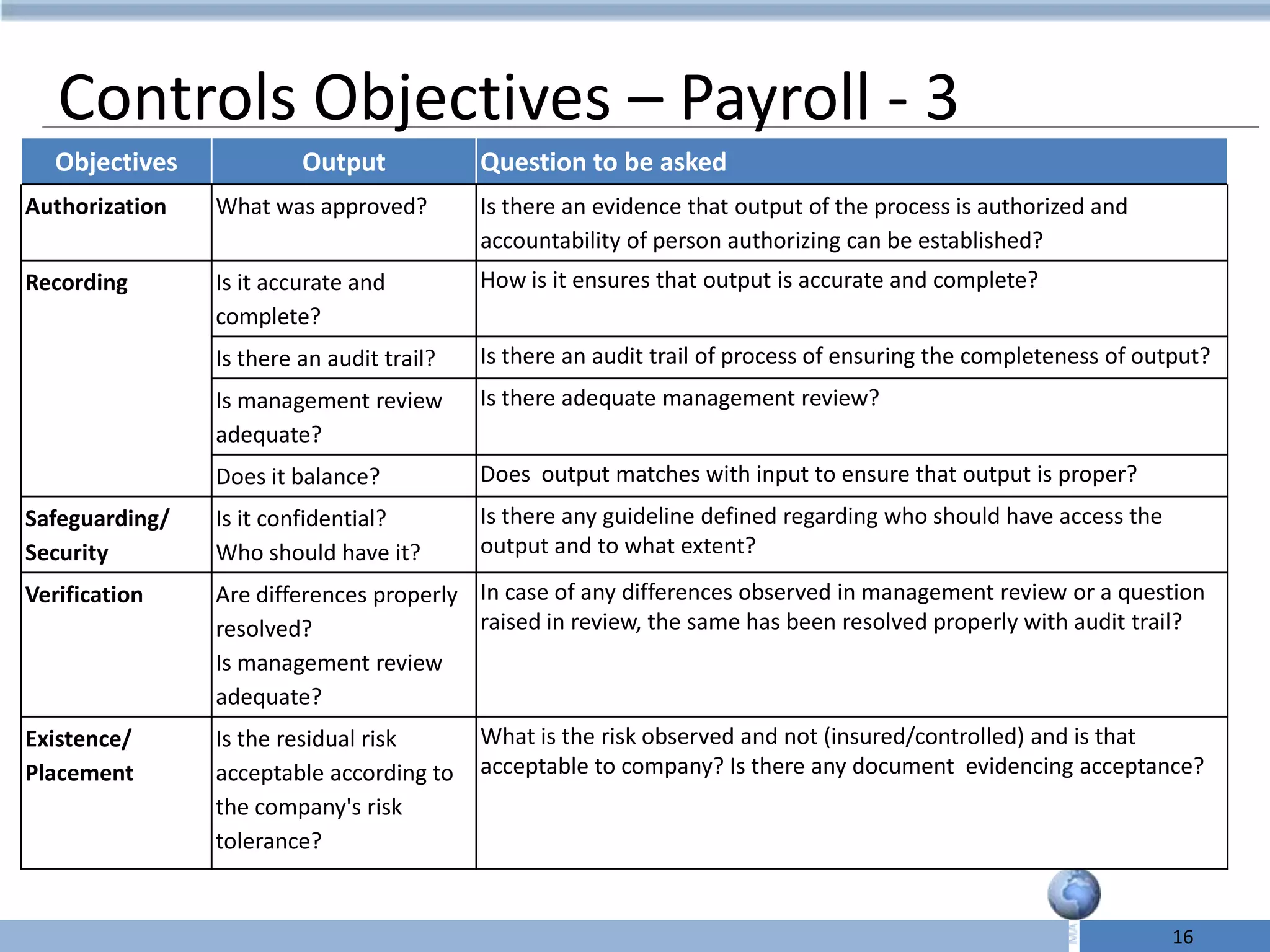

Control objectives in processes such as payroll, including authorization, recording, safeguarding, verification, and existence.

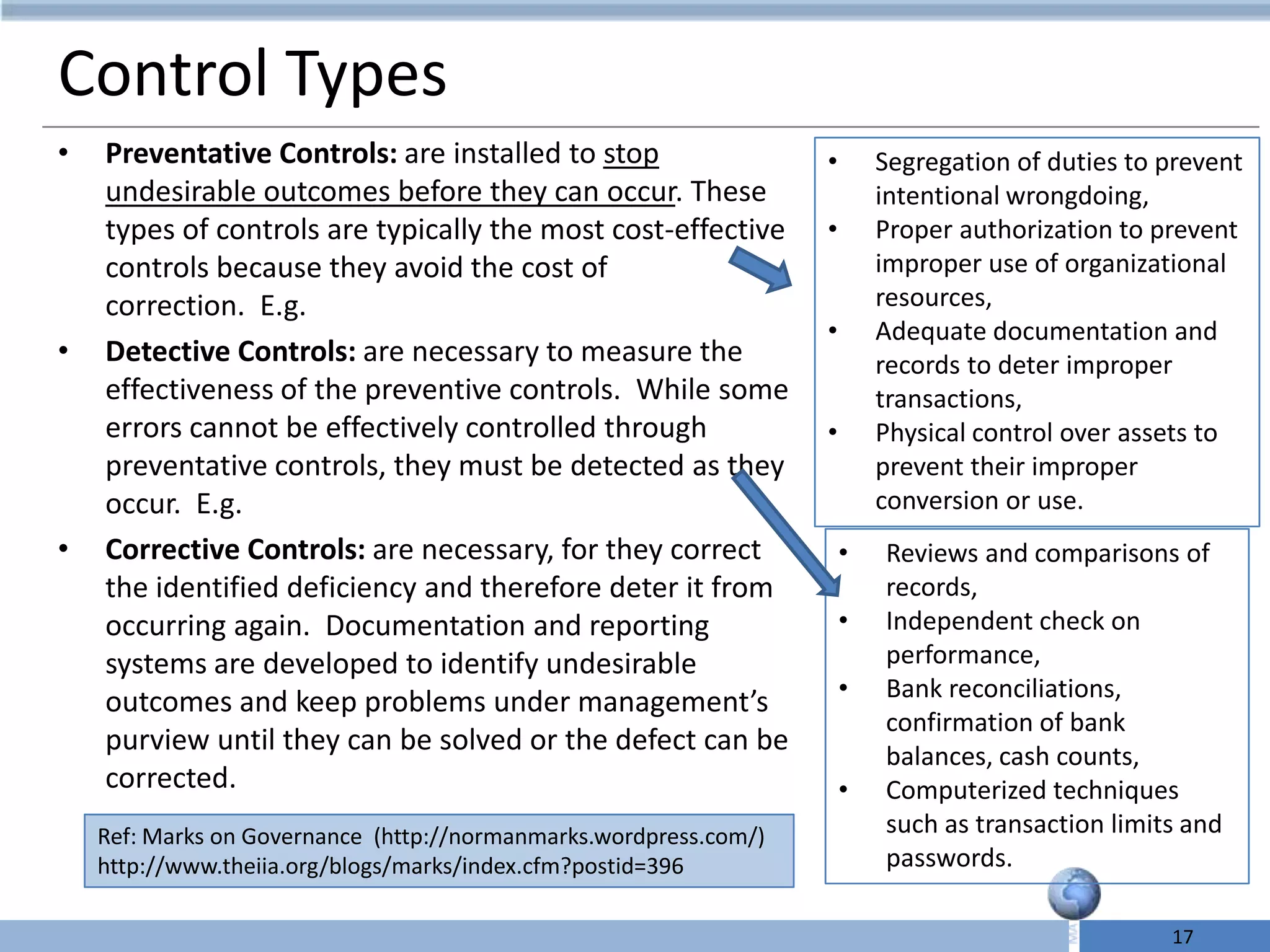

Explanation of preventative, detective, and corrective controls, including practical examples and references.

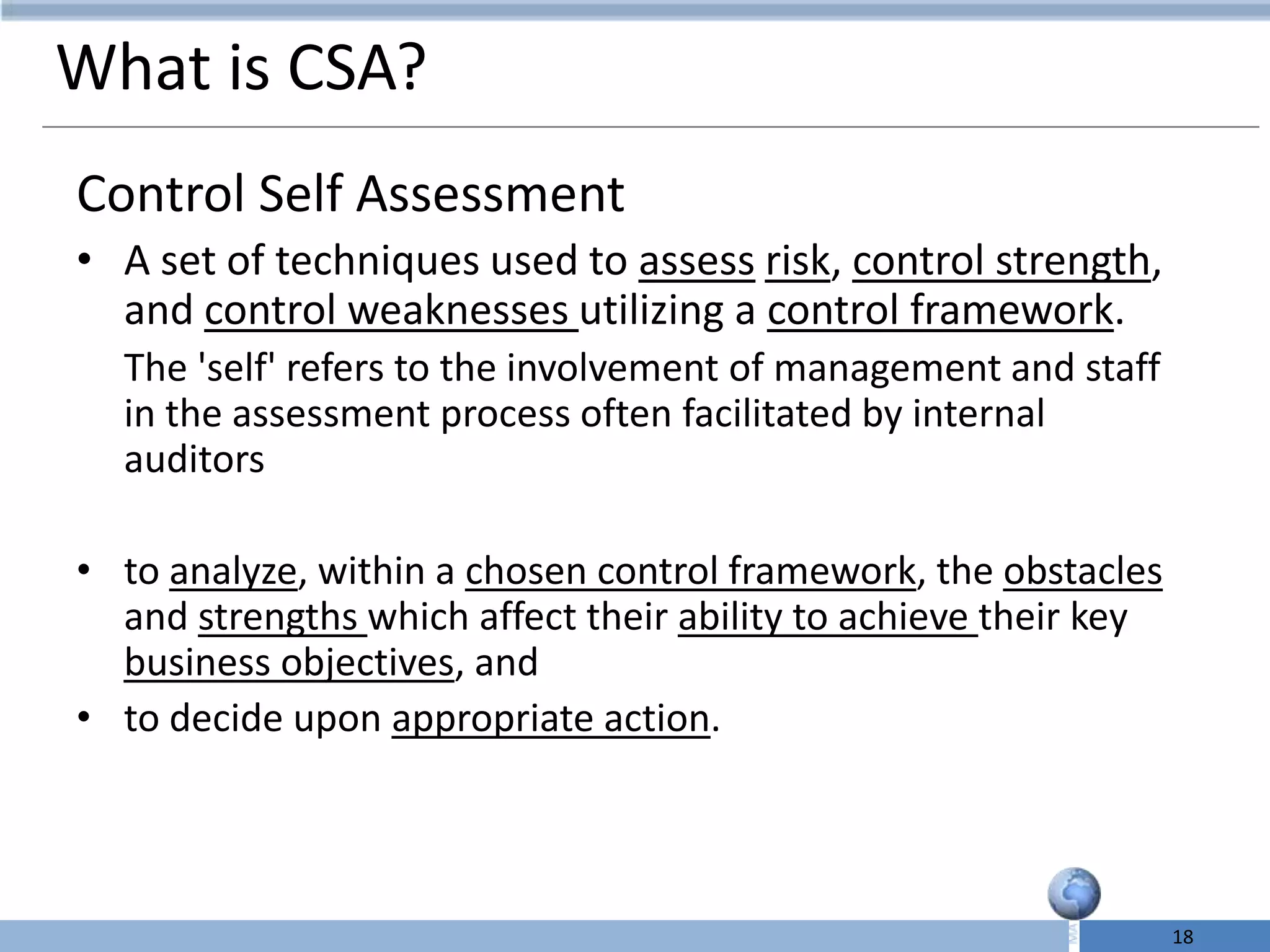

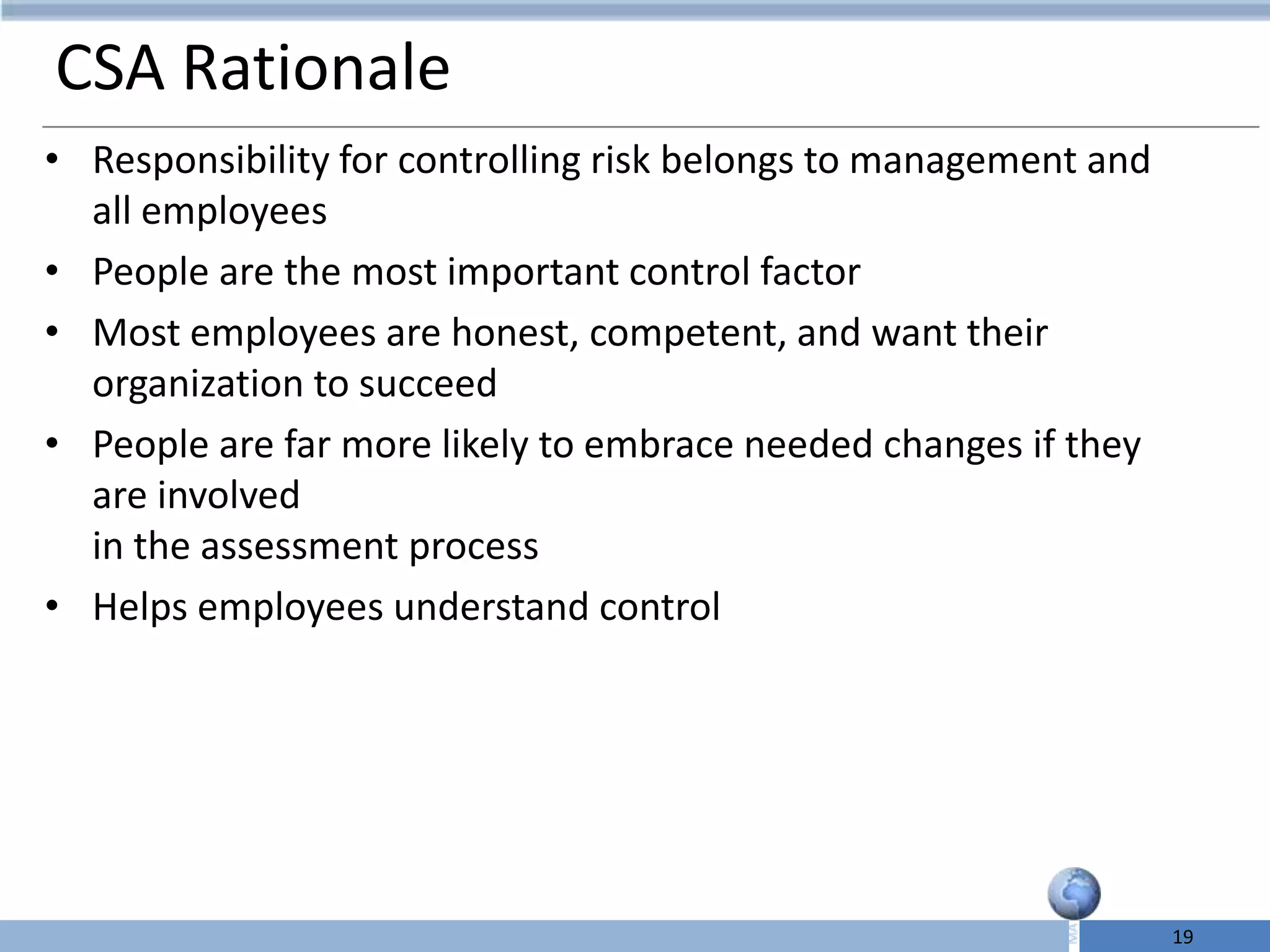

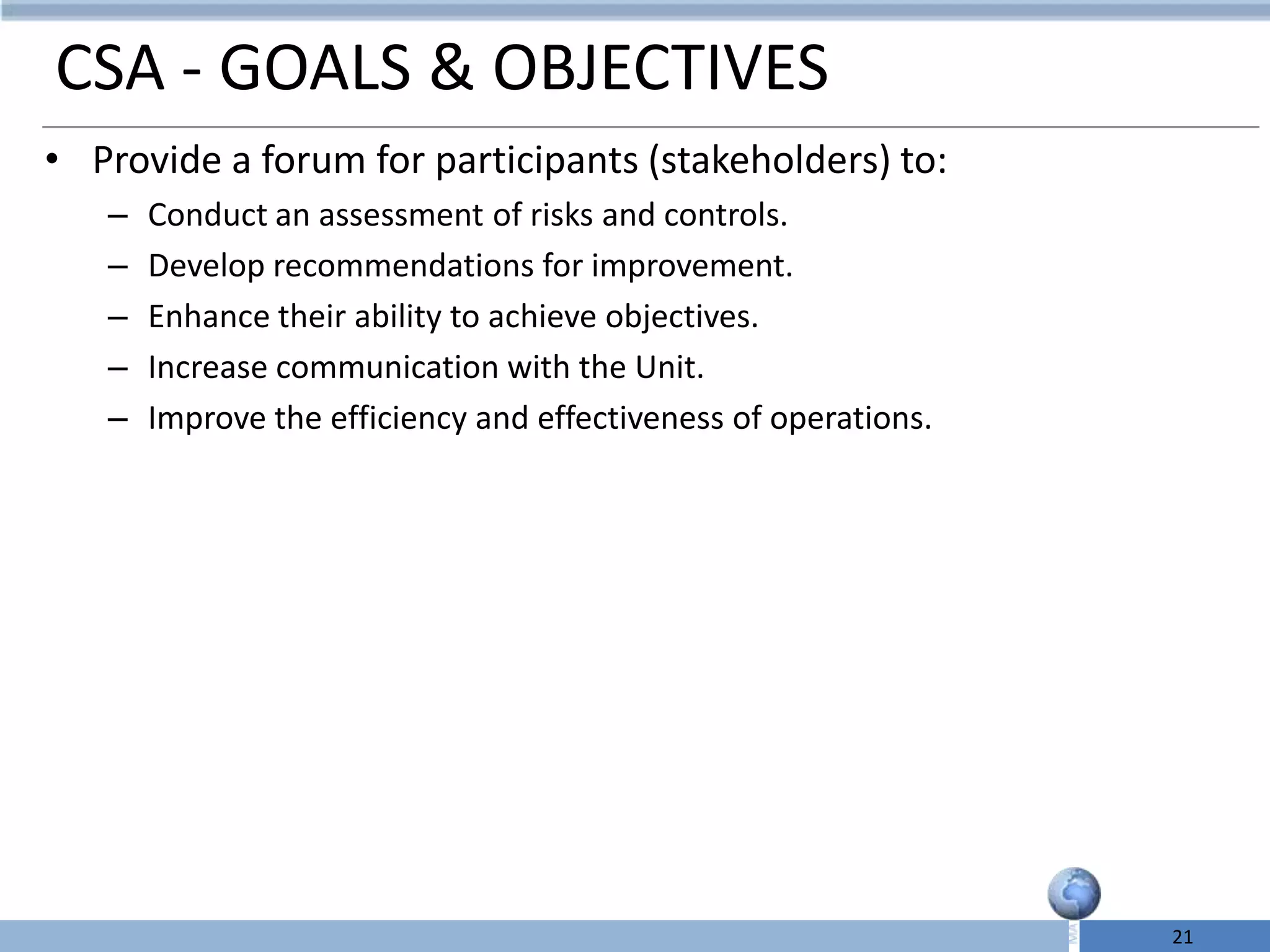

Control Self Assessment's purpose in risk and control evaluation, highlighting employee involvement and management responsibilities.

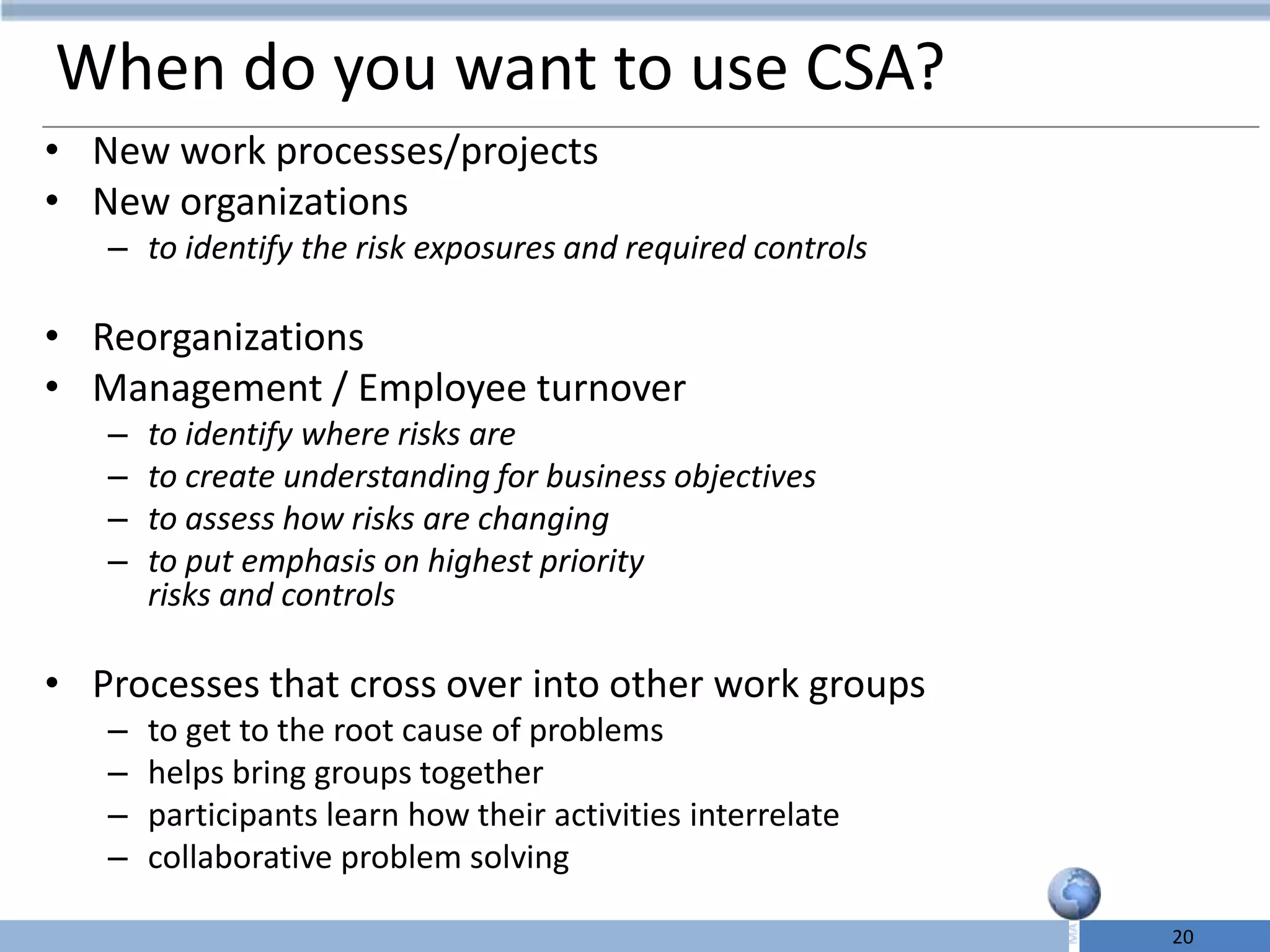

CSA applications in various contexts (new processes, reorganizations) and its goals for assessing risks and enhancing communication.

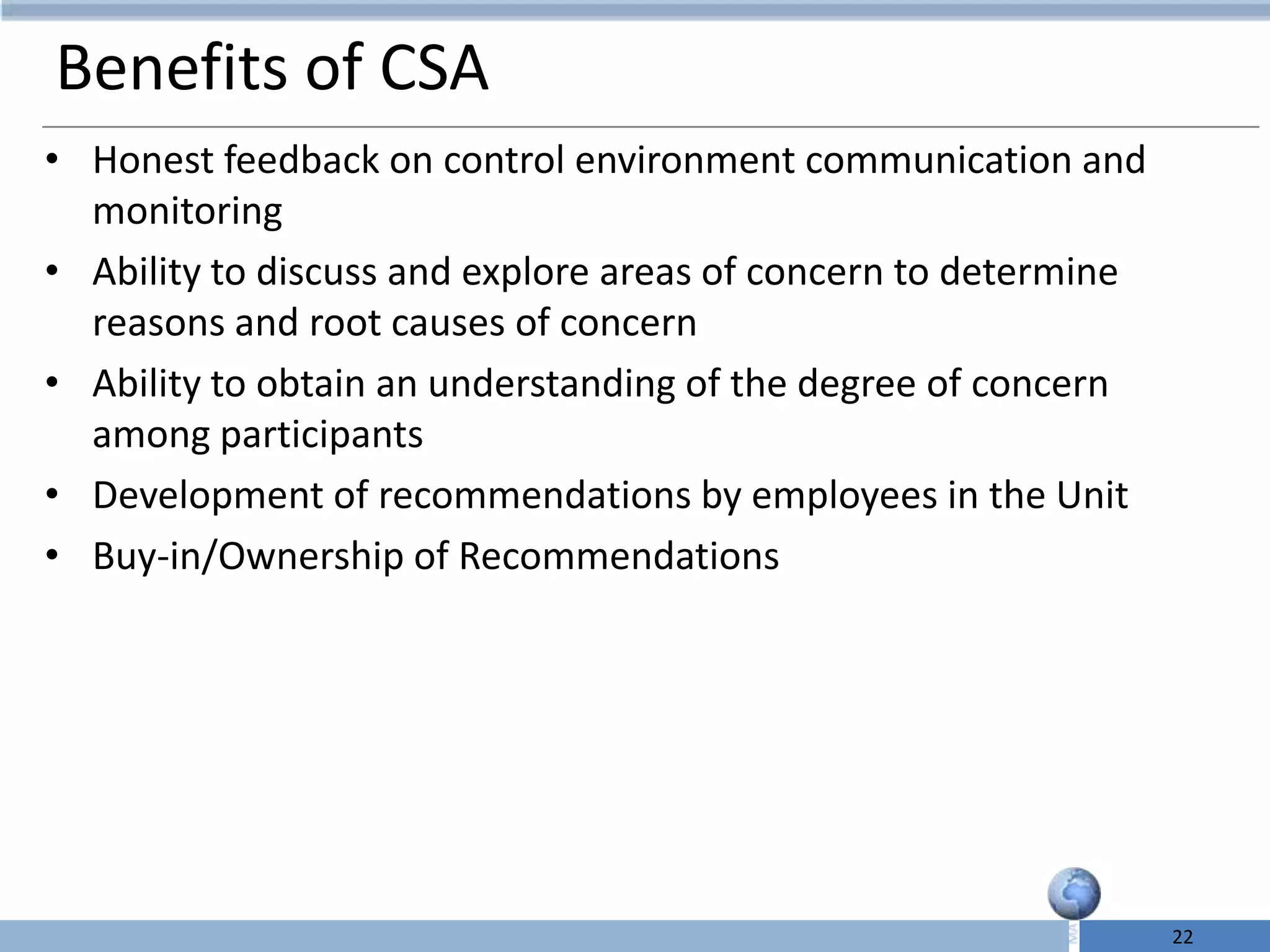

Benefits include honest feedback, exploration of concerns, understanding among participants, and ownership of recommendations.

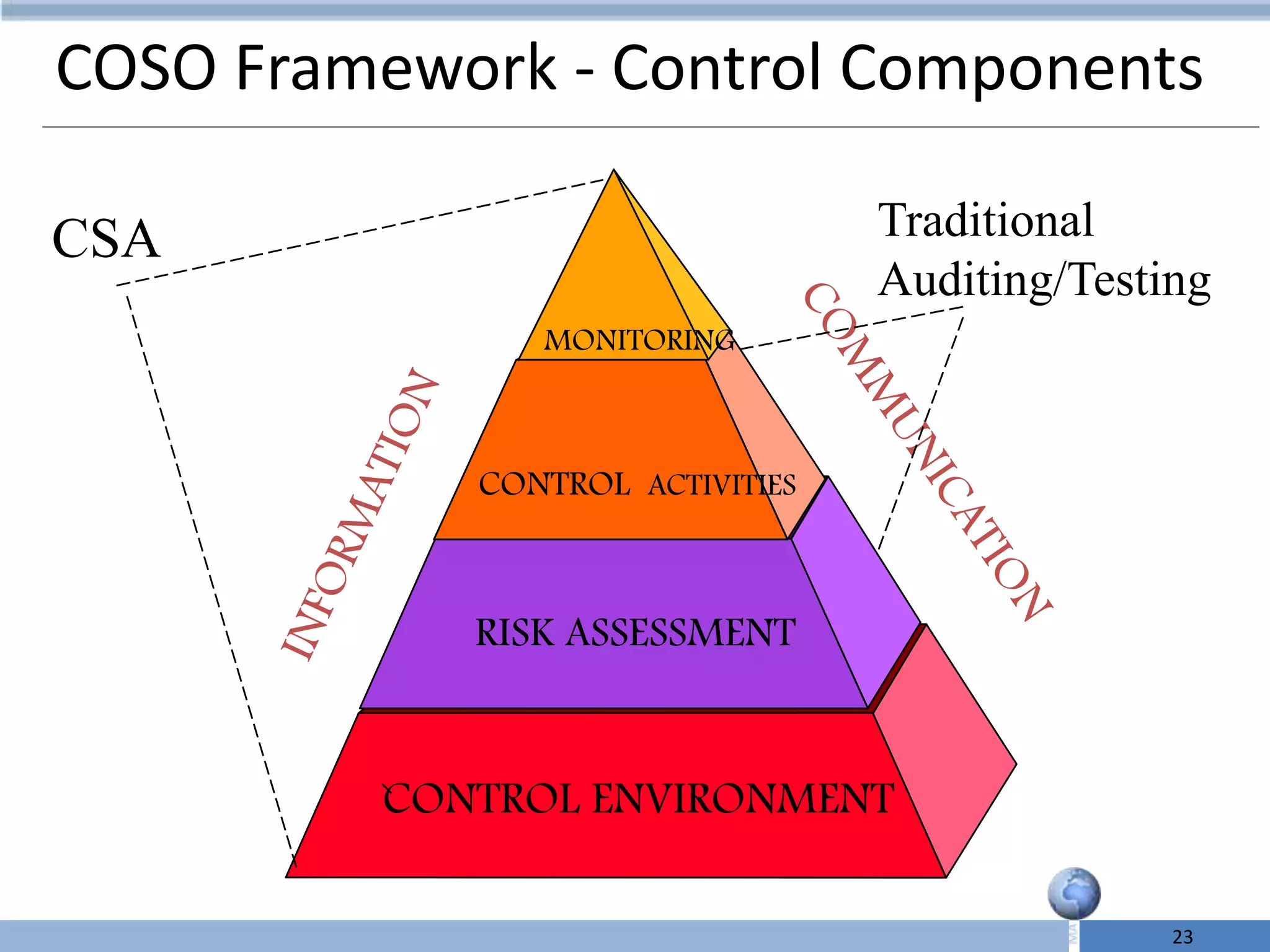

Comparison of CSA components to traditional auditing/testing methods within the COSO internal control framework.

Introduction to a practical case study relevant to internal controls.

Closing of the presentation with a Q&A session for audience interaction.