![Risk Based Audits

22

Risk Based

Audit

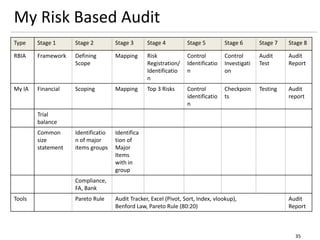

Risk based Internal Audit (RBIA) is an internal methodology which is

primarily focused on the inherent risk involved in the activities or system

and provide assurance that risk is being managed by the management

within the defined risk appetite level.[1] It is the risk management

framework of the management and seeks at every stage to reinforce the

responsibility of management and BOD (Board of Directors) for managing

risk

http://en.wikipedia.org/wiki/Risk_based_audit](https://image.slidesharecdn.com/rbiaandstbcsc20180902v0-180903174817/85/Risk-Based-Internal-Audit-and-Sampling-Techniques-22-320.jpg)

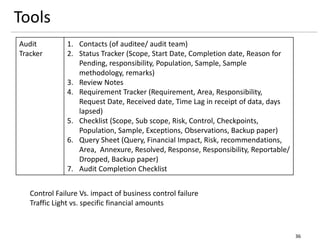

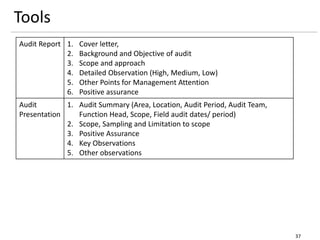

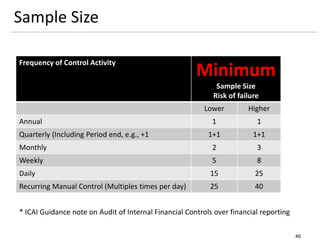

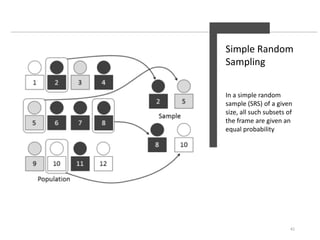

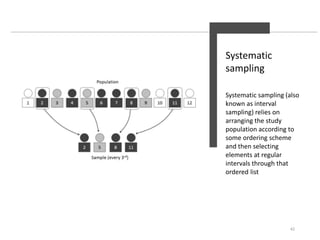

This document discusses risk based internal auditing and sampling techniques. It begins with an agenda and definitions of risk, risk management, and the three lines of defense model. It then covers topics like risk identification, evaluation, scoring, developing a risk based internal audit plan, criteria for rating observations, and tools used for auditing. Sampling techniques discussed include random selection, systematic selection, monetary unit sampling, haphazard selection and block selection. Guidelines are provided for determining appropriate sample sizes based on the frequency of control activities.