Internal Controls forRecipients

of ARPA/SLFRF Funds

Albany Law School Community Economic Development Clinic

Matt DeLaus

2.

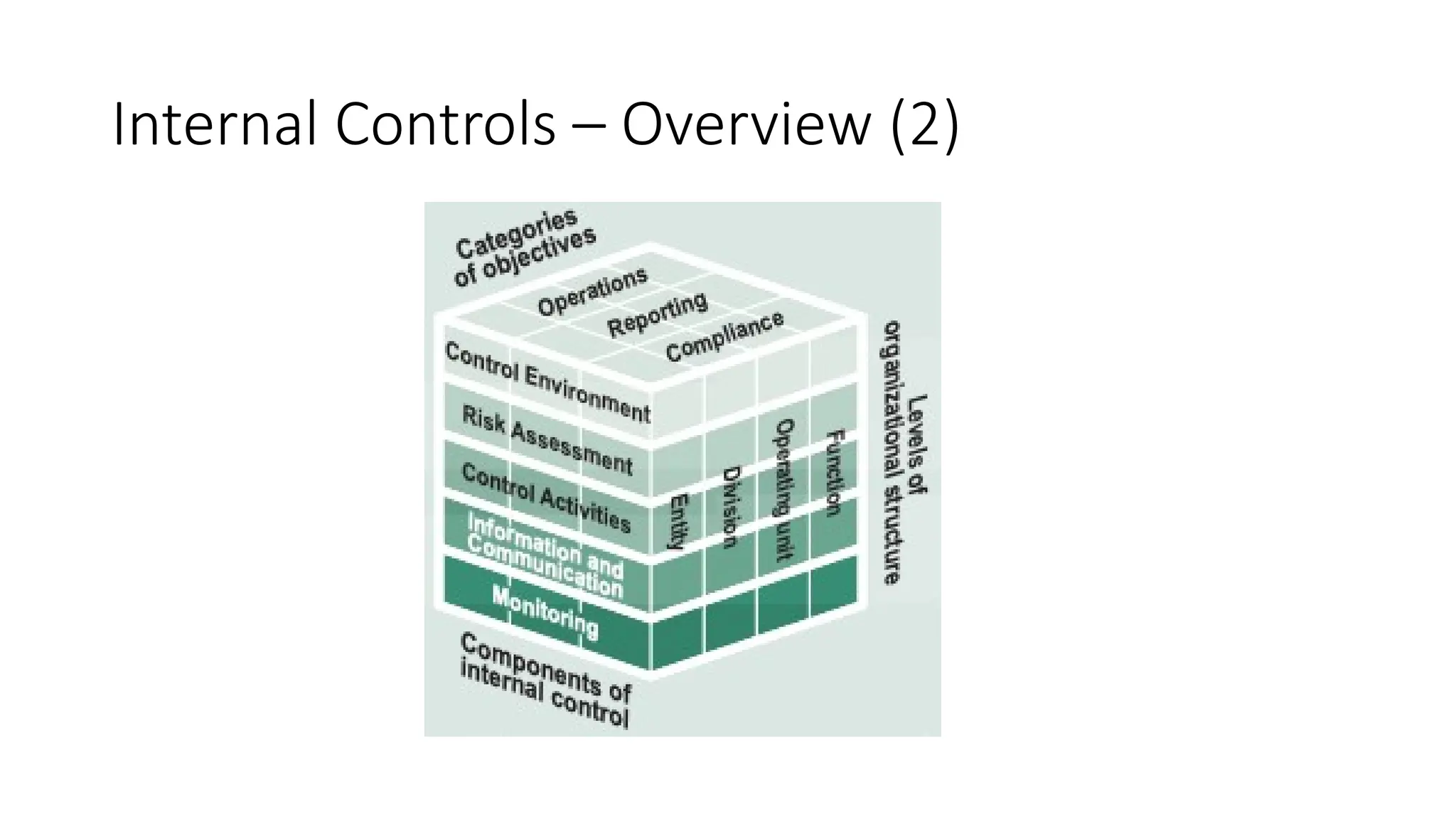

Internal Controls –Overview

• Internal control is a process effected by an entity’s oversight body,

management, and other personnel that provides reasonable

assurance that the objectives of an entity will be achieved

• “Standards for Internal Control in the Federal Government” issued by

the Comptroller General of the United States

• Made up of five components, which are each made up of several principles

• Informs the high-level, as well as day-to-day, operations of the

Organization

Component 1: ControlEnvironment

• The “foundation” for an internal control system

• Setting the tone at the top

• Strong control environment is characterized by:

• High ethical standards;

• Management’s commitment to competence;

• Clear assignment of authority and responsibility;

• Effective communication channels; and

• Accountability for performance

5.

Principle 1 –Demonstrate Commitment to

Integrity and Ethical Values

• “The oversight body and management should demonstrate a

commitment to integrity and ethical values”

• The commitment comes from the top, and compliance comes from all

parties

• Illustrative Controls:

• A code of conduct is developed, documented, communicated and periodically

updated

• A code of conduct explicitly prohibits inappropriate management override of

established controls

• Conflict of interest statements are obtained periodically from those charged

with governance (TCWG) and key management

6.

Principle 2 –Exercise Oversight Responsibility

• “The oversight body should oversee the entity’s internal control system”

• Illustrative Controls:

• Process in place to provide effective oversight pertaining to federal award compliance

issues and related risk

• TCWG periodically review ethical and moral conduct violations including stakeholder

complaints regarding issues of federal award compliance with senior management

• A whistle blower submission process exists to receive and evaluate concerns by employees

regarding questionable practices inclusive of issues impacting federal award

compliance/non-compliance

• An audit committee is enabled by the organization’s bylaws

• TCWG have effective two-way communication with external and internal auditors

• TCWG review risk assessments including the risks of fraud for impact on federal compliance

objectives

7.

Principle 3 –Establish Structure,

Responsibility, and Authority

• “Management should establish an organizational structure, assign

responsibility, and delegate authority to achieve the entity’s

objectives”

• Illustrative Controls:

• Policies, procedures and organizational charts provide for segregation of

duties within and among processes and controls

• Policies and procedures are in place to ensure that compliance responsibilities

are assigned to particular positions

8.

Principle 4 –Demonstrate Commitment to

Compliance

• “Management should demonstrate a commitment to recruit, develop,

and retain competent individuals”

• Illustrative Controls

• Job descriptions include appropriate knowledge and skill requirements

• Appropriate training is provided that is relevant to responsibilities over

compliance objectives

• Personnel with federal award compliance responsibilities are properly trained

on their responsibilities

9.

Principle 5 –Enforce Accountability

• “Management should evaluate performance and hold individuals

accountable for their internal control responsibilities”

• Illustrative Controls:

• Appropriate performance evaluations are provided that establish goals,

accountability, and feedback

• Violations of the Non-Profit policies result in remedial actions to deter others

• Consequences for noncompliance with the Non-Profit policies are

communicated and enforced

• Penalties for inappropriate and/or discriminatory behavior, as well as

harassment, are adequate and publicized

10.

Component 2: RiskAssessment

• Assessing potential risks from internal and external sources in order

to develop appropriate risk responses

• Systematic and ongoing process to identify, analyze, and manage risks

that could prevent Organization from achieving its objectives

• Proactive risk management

11.

Principle 6 –Define Objectives and Risk

Tolerances

• “Management should define objectives clearly to enable the

identification of risks and define risk tolerances”

• Illustrative Controls:

• Management identifies key compliance objectives for types of compliance

requirements

• Management identifies and evaluates risk tolerances related for controls over

compliance

12.

Principle 7 –Identify, Analyze, and Respond to

Risks

• “Management should identify, analyze, and respond to risks related to

achieving the defined objectives”

• Management analyzes and identifies compliance risks

• TCWG have oversight over significant areas of risks

• Employees receive appropriate training to address identified risks

• Risk mitigation strategies are implemented by management

13.

Principle 8 –Assess Fraud Risk

• “Management should consider the potential for fraud when

identifying, analyzing, and responding to risks”

• Illustrative Controls:

• Management reviews audit findings to identify fraud risks

• If an internal audit function exists, it reviews fraud risks and the internal

control structure Compliance Supplement 2020 6-8

• Management reviews the internal control structure for potential fraud risks

• TCWG periodically review a report of the potential fraud risks identified and

actions taken in response to those risks during the period

14.

Principle 9 –Identify, Analyze, and Respond to

Change

• “Management should identify, analyze, and respond to significant changes

that could impact the internal control system”

• Illustrative Controls:

• Management identifies changes such as new personnel, new technology, expanded

operations, rapid growth, or changes in the operating environment and adjusts risk

assessments to address those changes

• Management analyzes compliance requirement modifications to properly adjust

risk

• A communication process with regulators is in place to identify changes in

compliance requirements

• Changes in philosophies or employee turnover are evaluated by management for

any potential impact on related controls

15.

Component 3: ControlActivities

• Actions which management establishes through policies and

procedures to achieve objectives and respond to risks in the internal

control system

• Procedures that are part of other processes (e.g., procurement) that

are put in place to ensure risks are being managed and goals are

being achieved

16.

Principle 10 –Design Control Activities

• “Design Control Activities – management should design control activities to achieve

objectives and respond to risks”

• Illustrative Controls:

• Top-level reviews of actual performance

• Reviews by management at the functional or activity level

• Management of human capital

• Controls over information processing

• Physical control over vulnerable assets

• Establishment and review of performance measures and indicators

• Segregation of duties

• Proper execution of transactions

• Accurate and timely recording of transactions

• Access restrictions to and accountability for resources and records

• Appropriate documentation of transactions and internal control

17.

Principle 11 –Design Activities for the

Information System

• “Design Activities for the Information System – management should

design the entity’s information system and related control activities

over technology to achieve objectives and respond to risks”

• Illustrative Controls:

• Management designs the entity’s information system to respond to the

entity’s objectives and risks

• Management designs the entity’s information system to gather relevant data

that is complete, accurate, and valid

• Management continues to evaluate changes in the use of information

technology and designs new control activities when these changes are

incorporated into the entity’s information technology infrastructure

18.

Principle 12 –Implement Control Activities

• “Implement Control Activities – management should implement

control activities through policies”

• Illustrative Controls:

• Management communicates to personnel the policies and procedures so that

personnel can implement the control activities for their assigned

responsibilities

• Management periodically reviews policies, procedures, and related control

activities for continued relevance and effectiveness in achieving the entity’s

objectives or addressing related risks

19.

Component 4: Information& Communication

• Quality information is available for management and employees, who

use it in their decisionmaking

• Information is automatically captured and either communicated or

made available effectively and efficiently

20.

Principle 13 –Use Quality Information

• “Management should use quality information to achieve the entity’s

objectives”

• Illustrative Controls:

• Financial and programmatic systems capture, accurately process, and timely

report pertinent information

• The accounting system provides for separate identification of federal and non-

federal transactions

• Adequate source documentation exists to support amounts and items reported

• Reports are provided timely to managers for review and appropriate action

• Management verifies the sources and reliability of information used in making

management decisions and executes monitoring controls

21.

Principle 14- CommunicateInternally

• “Management should internally communicate the necessary quality

information to achieve the entity’s objectives”

• Illustrative Controls:

• Relevant internal and external information is communicated and delivered to

employees responsible for federal award compliance on a timely basis

• Effective channels for communication throughout the organization exist

22.

Principle 15 –Communicate Externally

• “Management should externally communicate the necessary quality

information to achieve the entity’s objectives”

• Illustrative Controls:

• Relevant information is communicated to external parties including

subrecipients, vendors, federal granting agencies, and third-party processors

on a timely basis

• Effective channels exist for communications with federal granting agencies,

oversight agencies and cognizant agencies

23.

Component 5: Monitoring

•Activities management establishes and operates to assess the quality

of performance over time and promptly resolves the findings of audits

and other reviews.

• Monitoring activities should be ongoing and designed to identify and

address changes

• Should reflect changes in laws, regulations, policies, procedures, and

the Organization’s structure and operations

• Crucial to ensuring internal controls system remain effective over time

24.

Principle 16 –Perform Monitoring Activities

• “Management should establish and operate monitoring activities to

monitor the internal control system and evaluate the results”

• Illustrative Controls:

• Management monitors the effective operation of critical control activities

• Management monitors the use of effective self-review procedures in critical

compliance areas

• Management monitors the effective review of timely and reliable metrics or

key performance indicators, including reconciliation with data from financial

or other reporting systems to ensure its accuracy and completeness

25.

Principle 17 –Evaluate Issues and Remediate

Deficiencies

• “Management should remediate identified internal control deficiencies

on a timely basis”

• Illustrative Controls:

• Findings, recommendations and other observations by independent auditors,

internal auditors, and federal auditors are distributed and reviewed by those

individuals responsible for compliance with federal requirements.

• Control deficiencies and instances of noncompliance are reported to and

evaluated by management and TCWG, if applicable, for resolution on a timely

basis

• Management periodically monitors the corrective action plans related to known

noncompliance and control deficiencies and the organization’s progress to

remediating the findings

#6 Examples:

The board of directors reviews and approves the organization's annual budget.

The board of directors reviews and approves the organization's financial statements and audit reports.

The board of directors establishes an audit committee to provide independent oversight of the organization's financial reporting and internal controls.