Downloaded 48 times

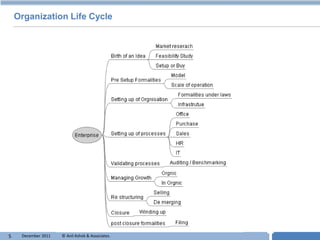

The document defines internal audit as an independent function that appraises an entity's operations and suggests improvements to strengthen governance and controls. It discusses the audit universe, scope of internal auditing, and organization lifecycle. Finally, it lists capabilities needed for internal auditors, including knowledge of standards, audit processes, and personal skills like presentation, negotiation, and time management.

![Approach note on internal audit [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/approachnoteoninternalauditcompatibilitymode-130407035746-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)