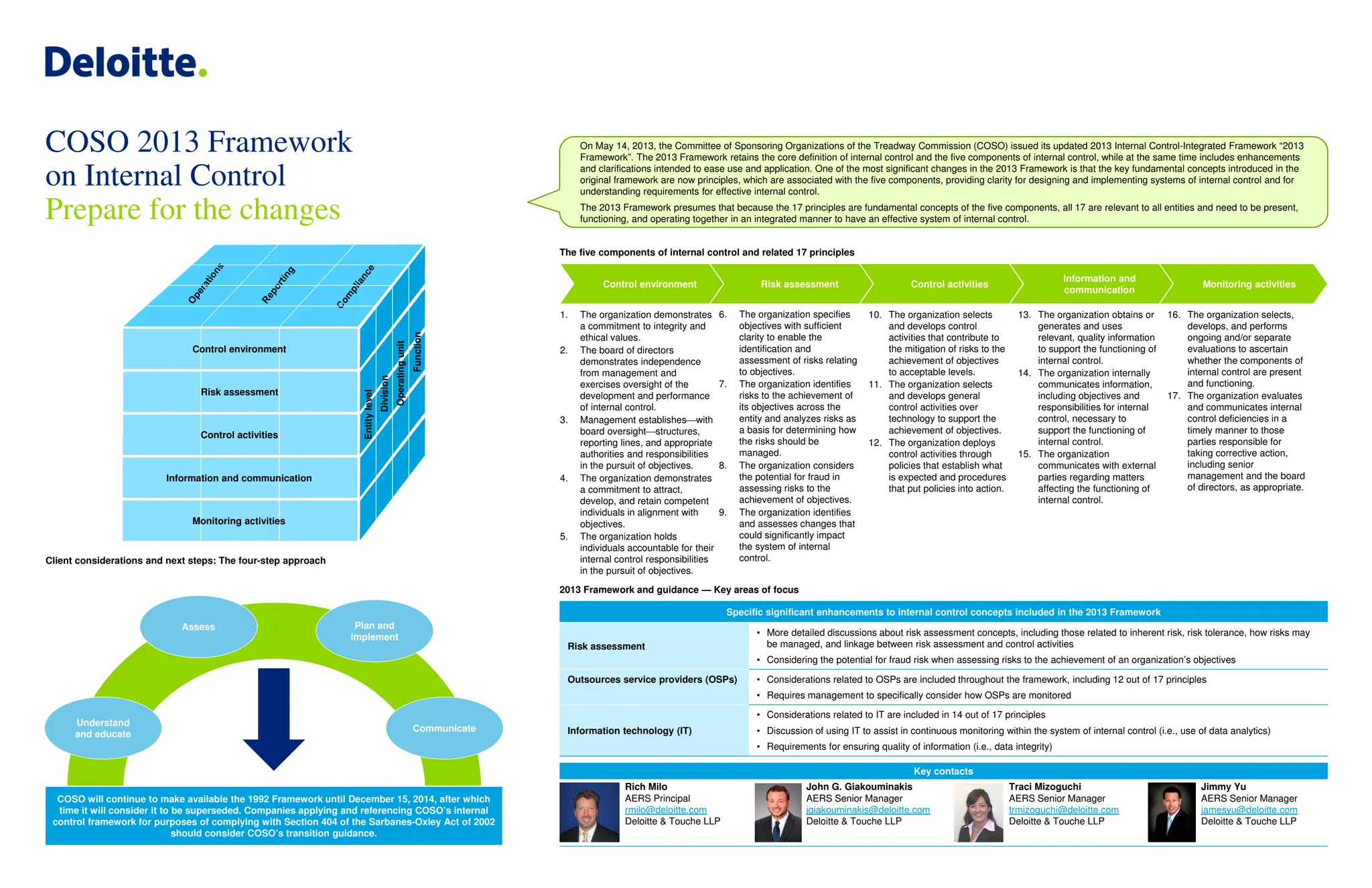

The document summarizes the updated 2013 COSO Internal Control-Integrated Framework, which retains the core definition and five components of internal control from the original framework but includes enhancements and clarifications. The key changes are that the original framework's fundamental concepts are now principles associated with the five components, and all 17 principles must be present and functioning for an effective system of internal control. The document also provides an overview of the 17 principles and related points of focus within the five components of internal control framework.