Downloaded 191 times

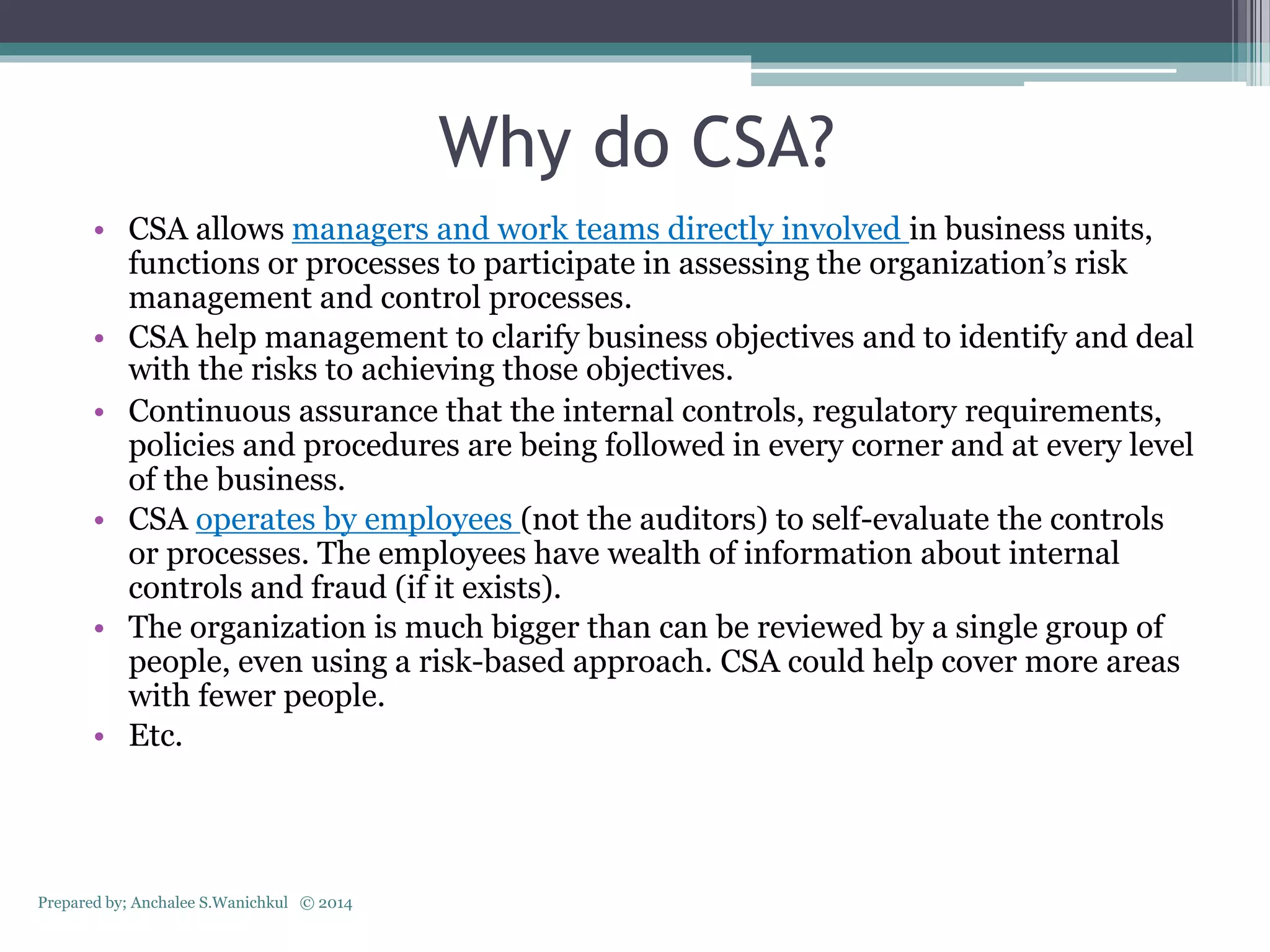

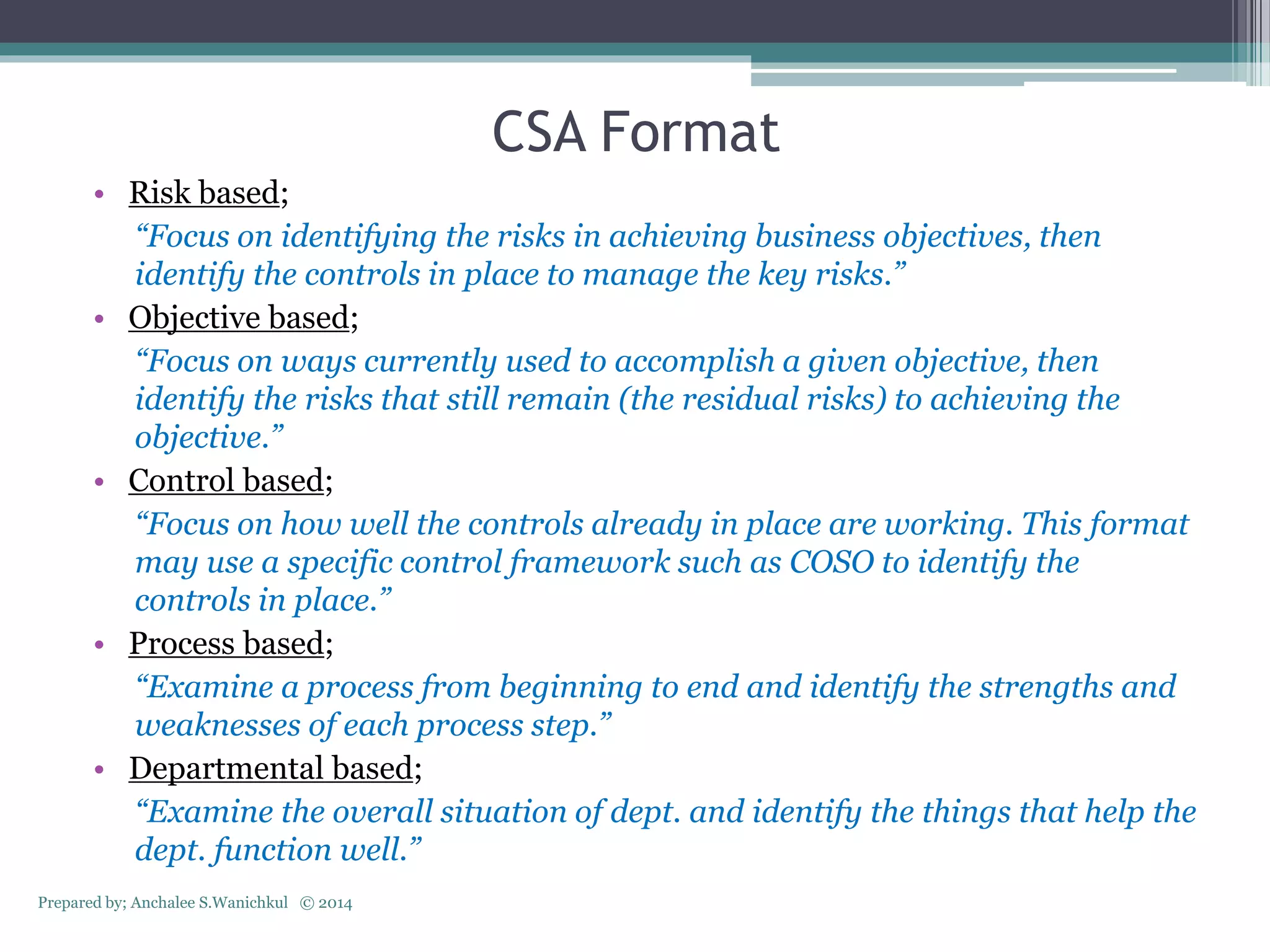

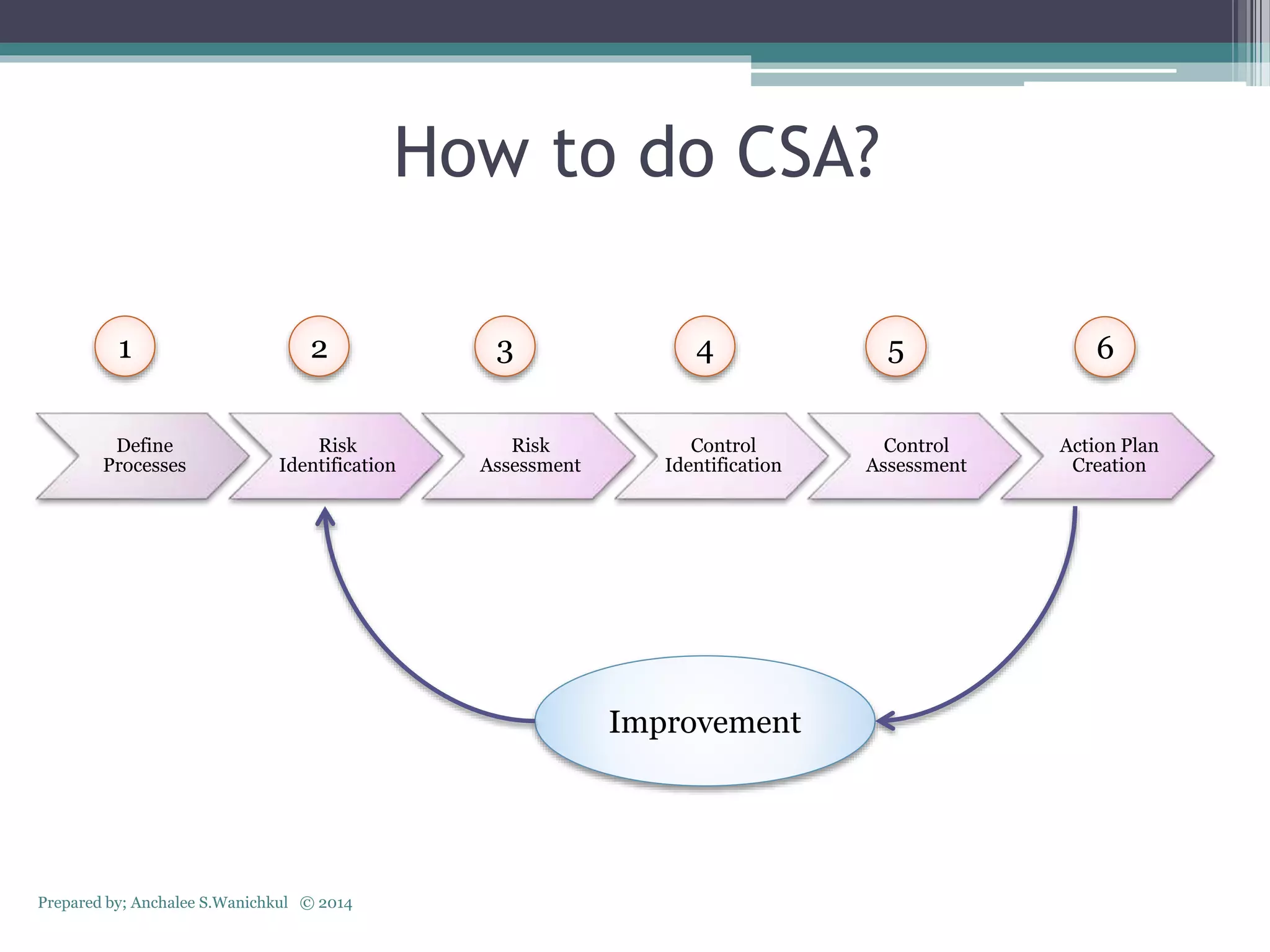

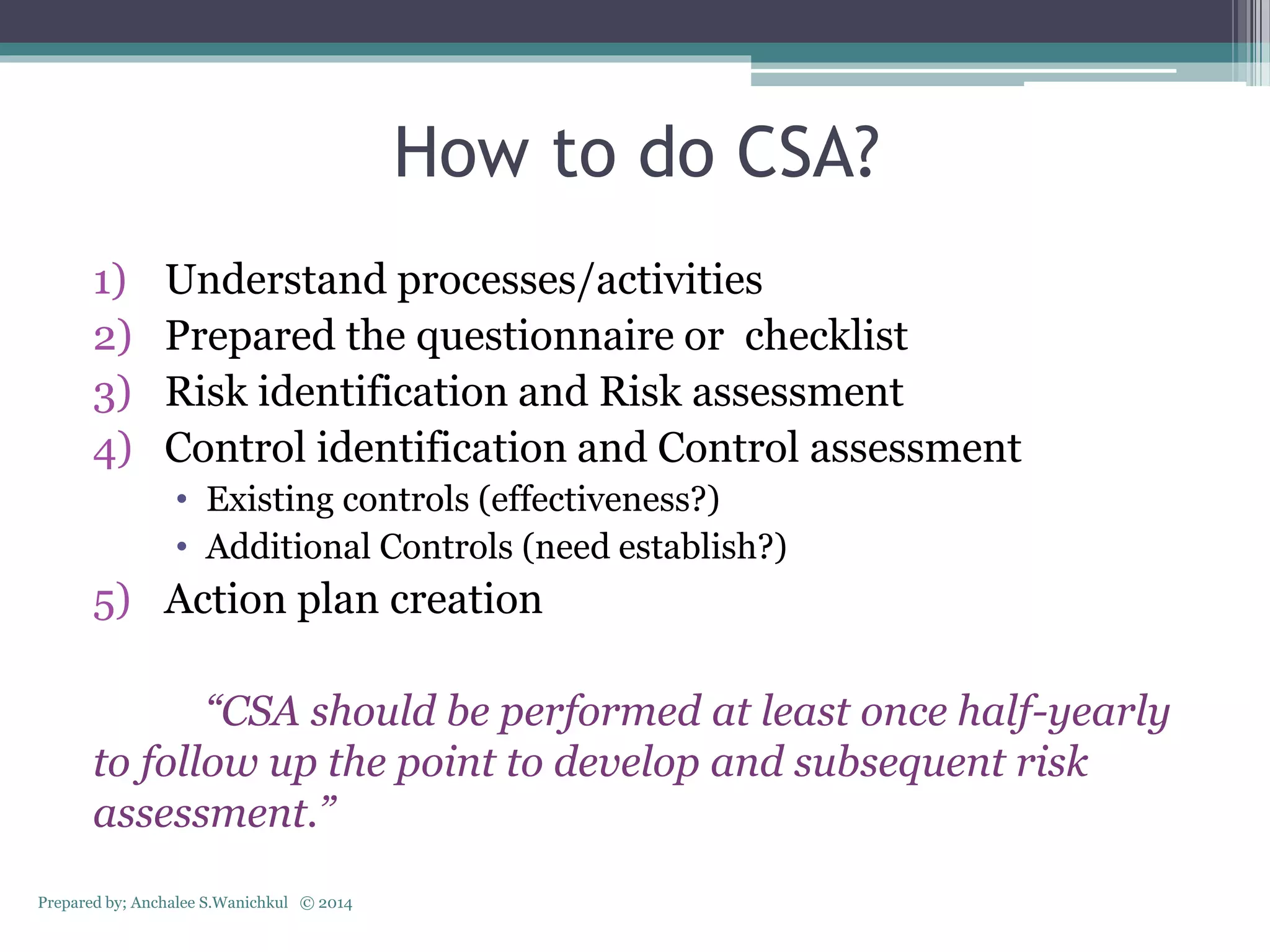

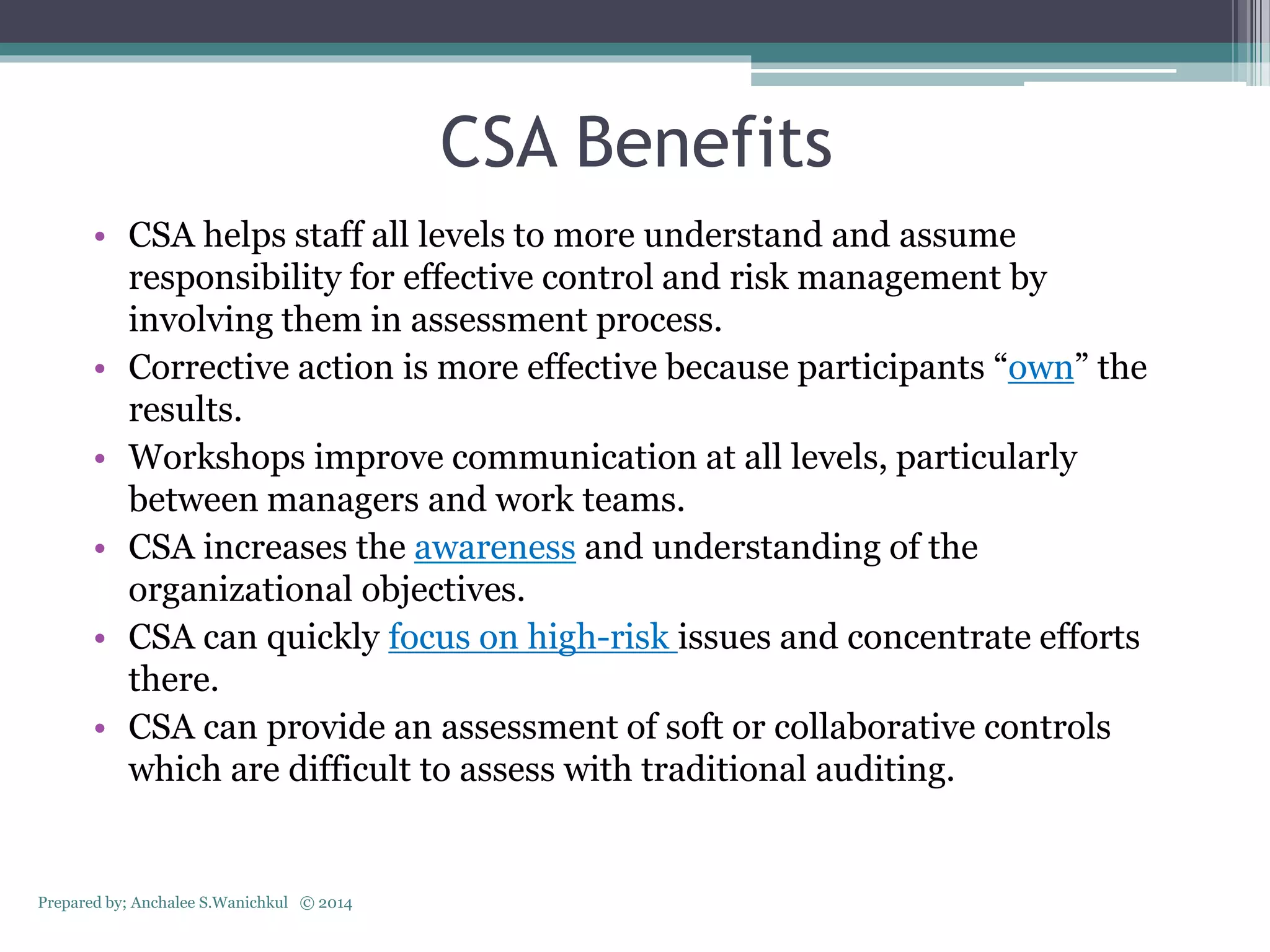

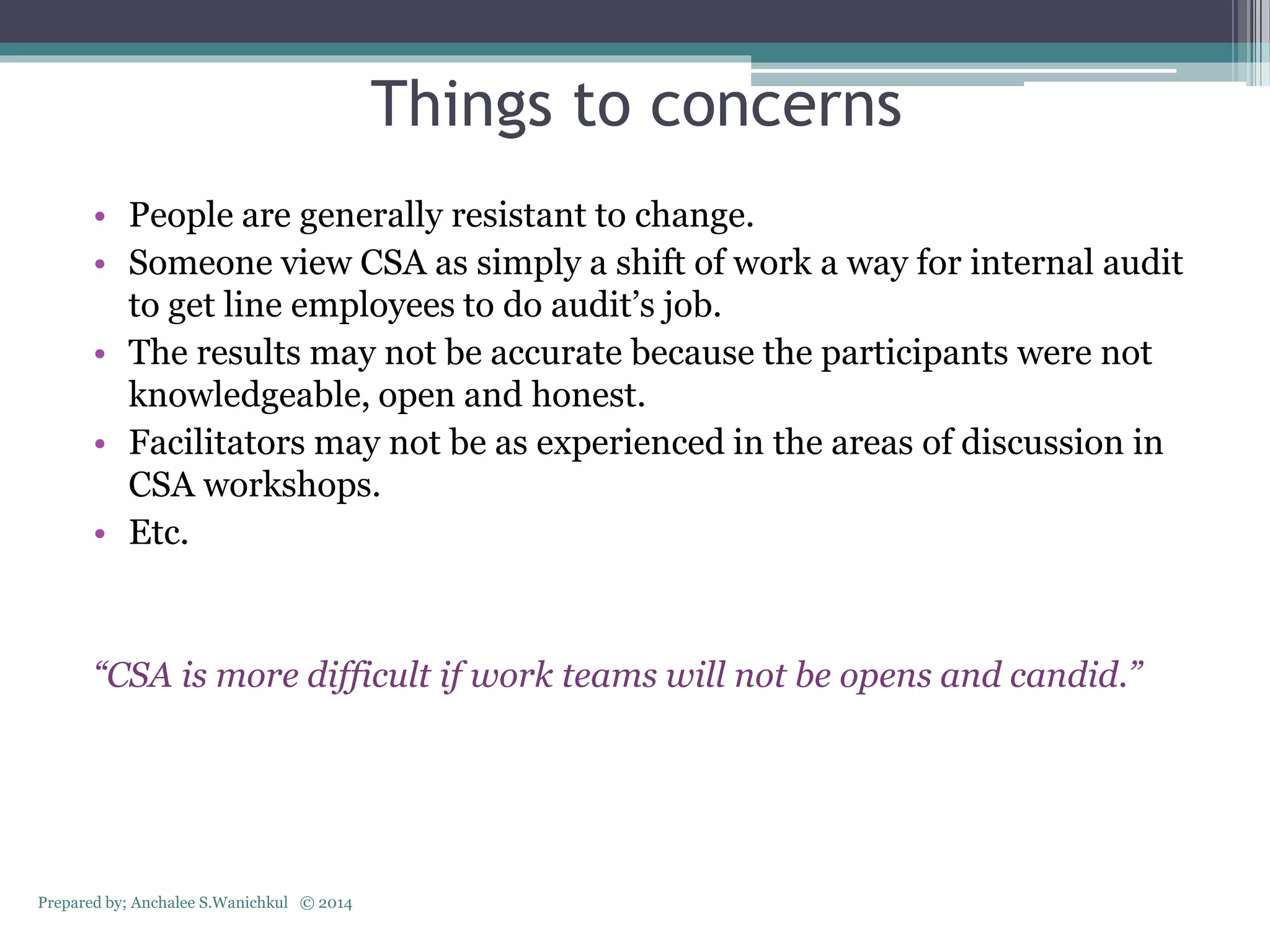

Control Self-Assessment (CSA) allows managers and employees to directly assess an organization's risk management and internal controls. CSA helps clarify business objectives, identify risks to achieving objectives, and ensure controls and regulations are followed. The CSA process involves employees self-evaluating controls and processes through activities like risk identification, control assessment, and action planning. Benefits of CSA include improved understanding and responsibility for controls, more effective corrective actions, and increased awareness of objectives. However, CSA may face resistance to change and requires open and honest participation to provide accurate results.