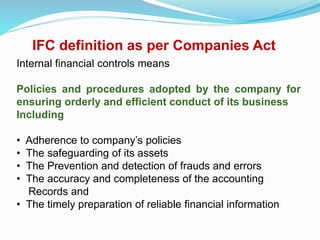

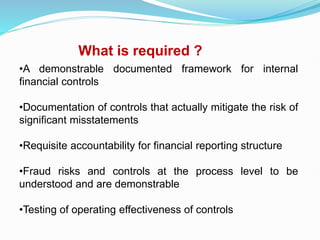

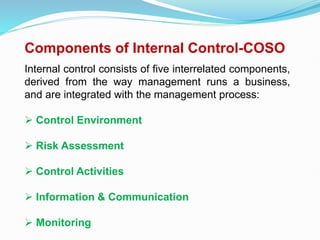

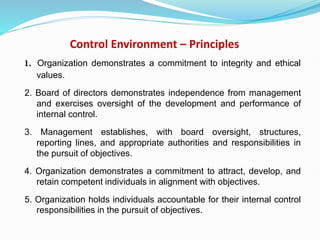

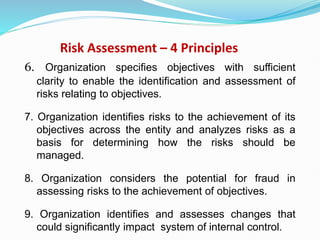

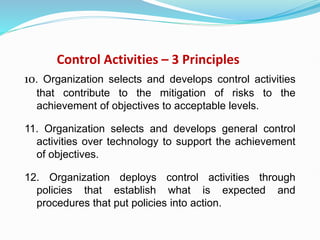

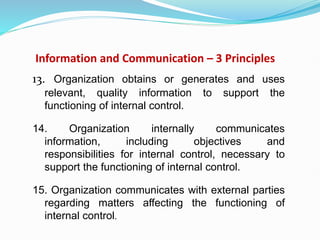

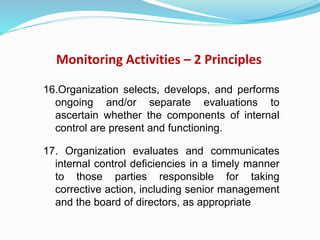

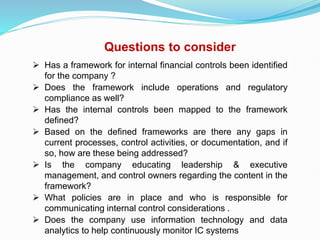

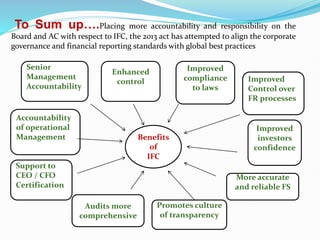

The document discusses internal financial controls (IFC) that companies in India are required to establish and maintain under the Companies Act of 2013. It provides background on regulations requiring boards to ensure adequate IFC and operating effectiveness. IFC include policies and procedures for orderly business conduct, regulatory compliance, and fraud prevention. Statutory auditors must report on IFC adequacy and effectiveness beginning in 2015. The document also outlines IFC framework components from the Committee of Sponsoring Organizations of the Treadway Commission (COSO) including control environment, risk assessment, control activities, information/communication, and monitoring. Questions to consider regarding IFC frameworks, mapping, gaps, communication and monitoring are also discussed.