Downloaded 130 times

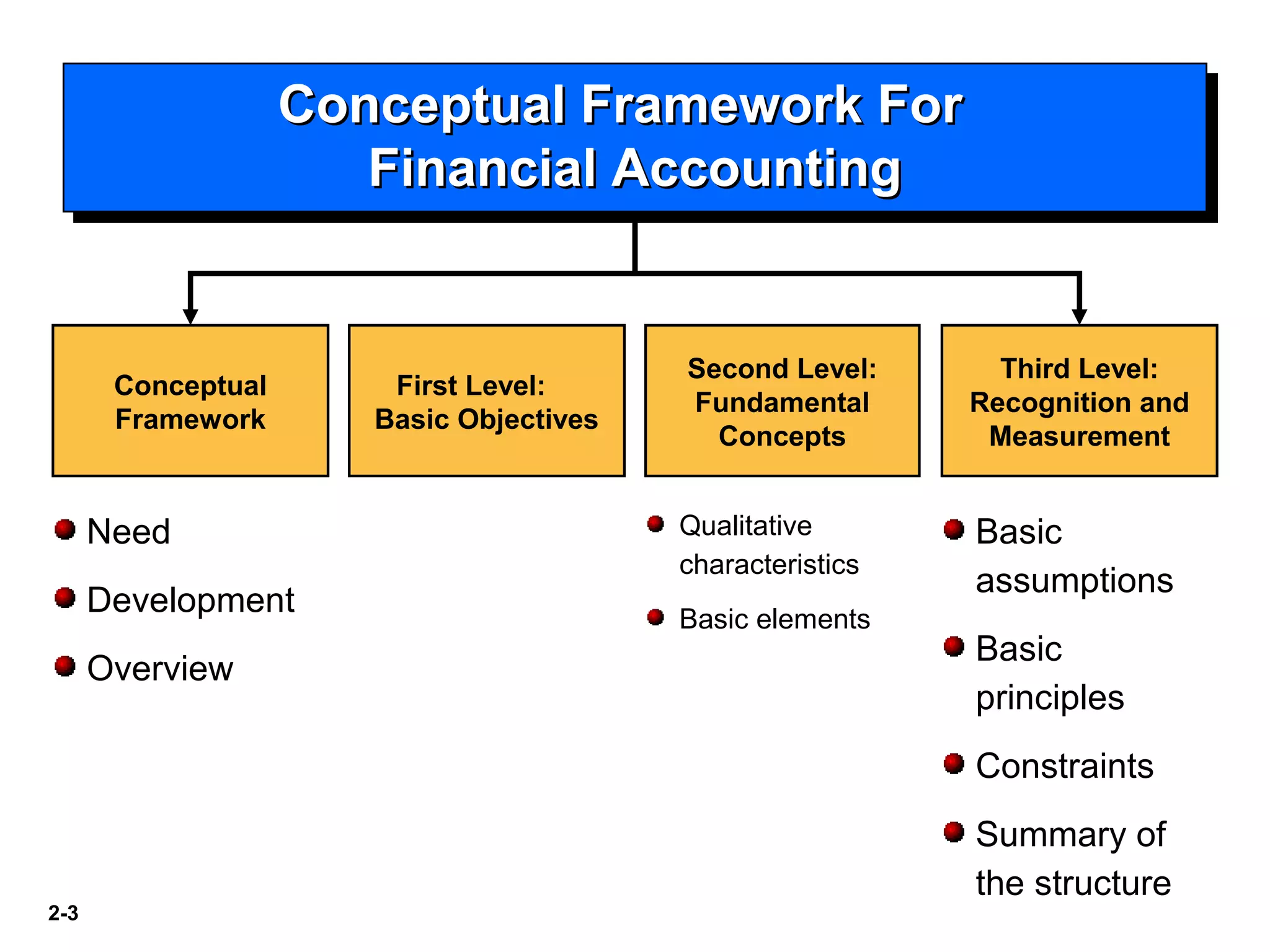

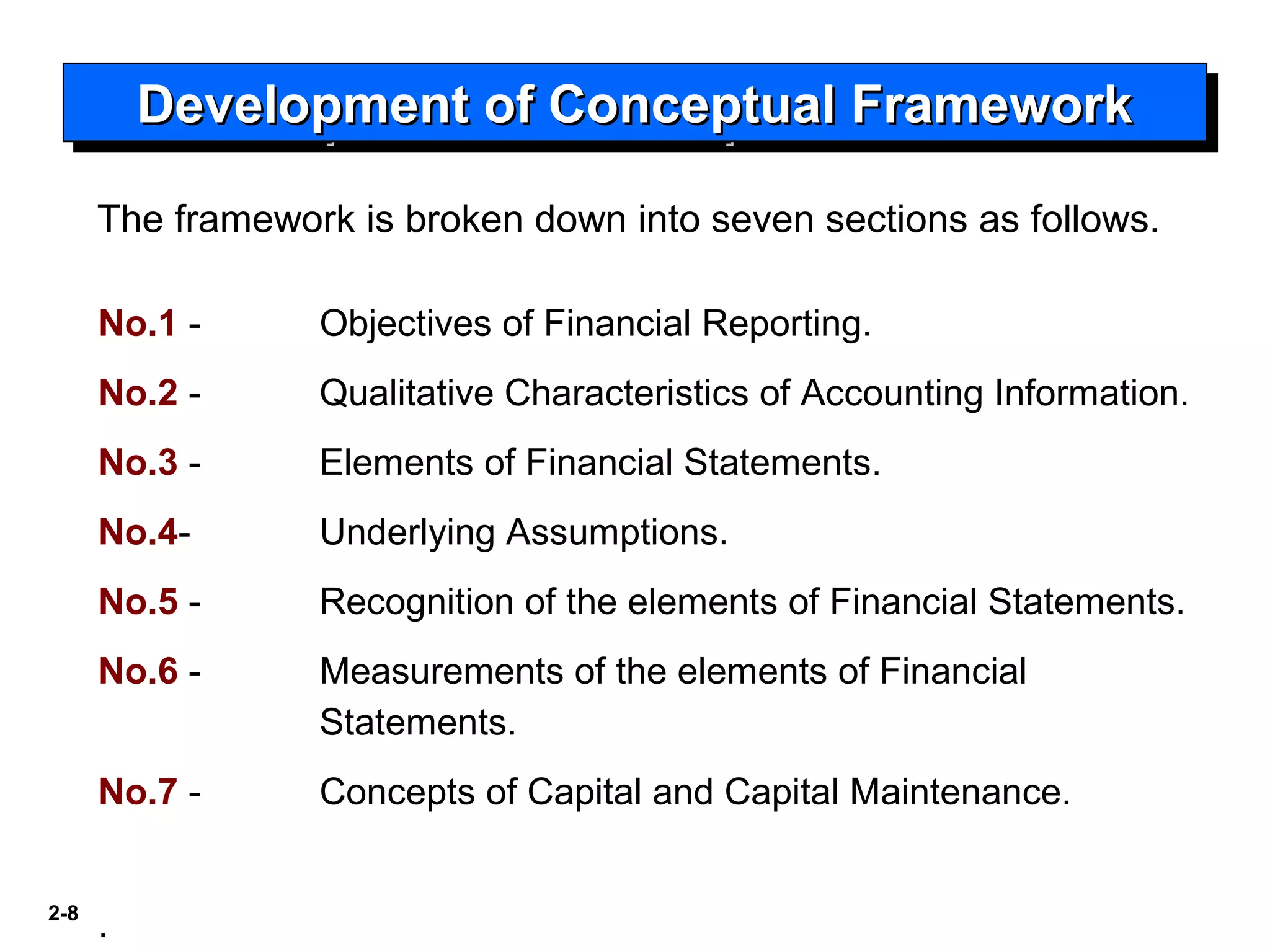

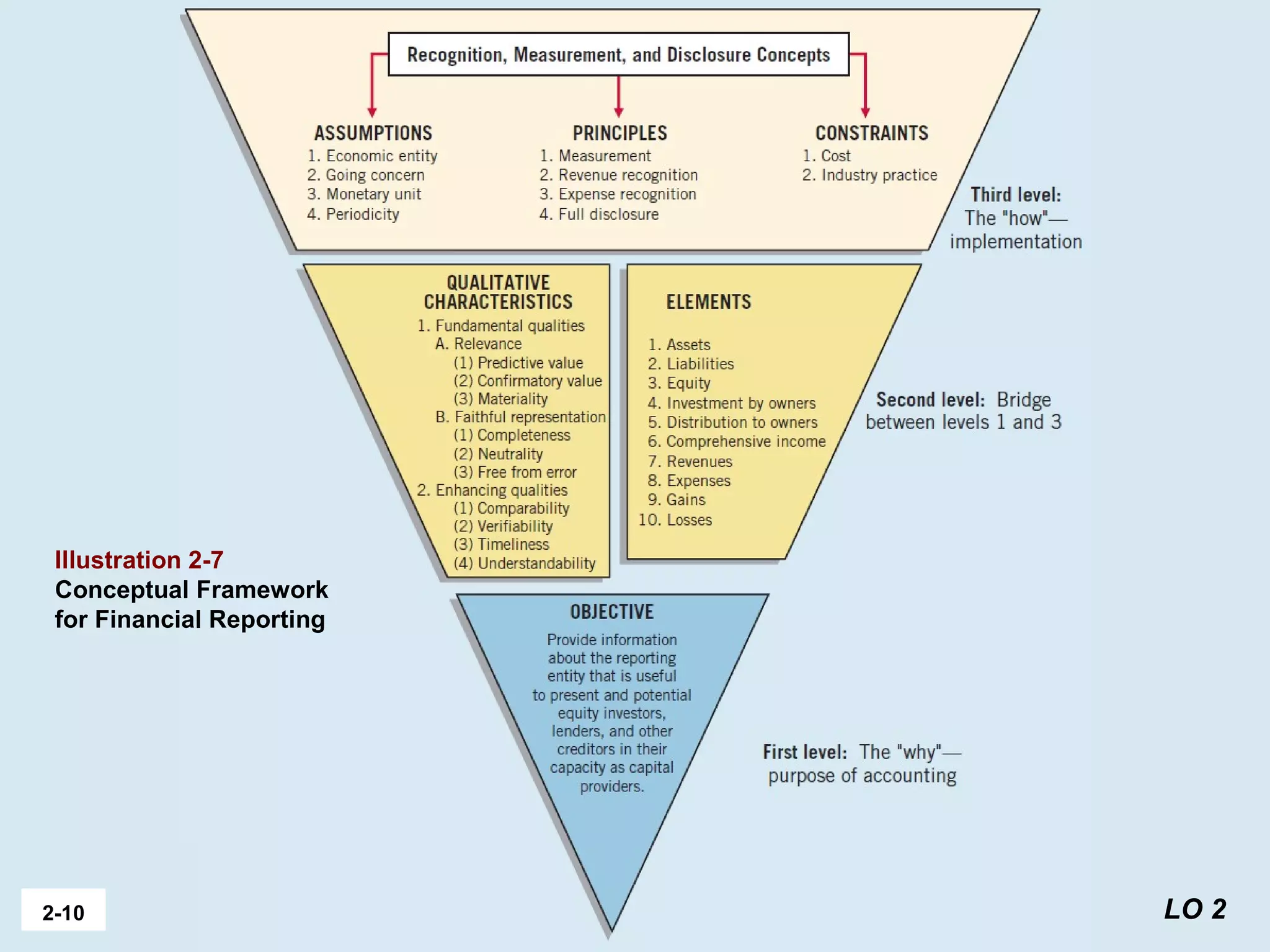

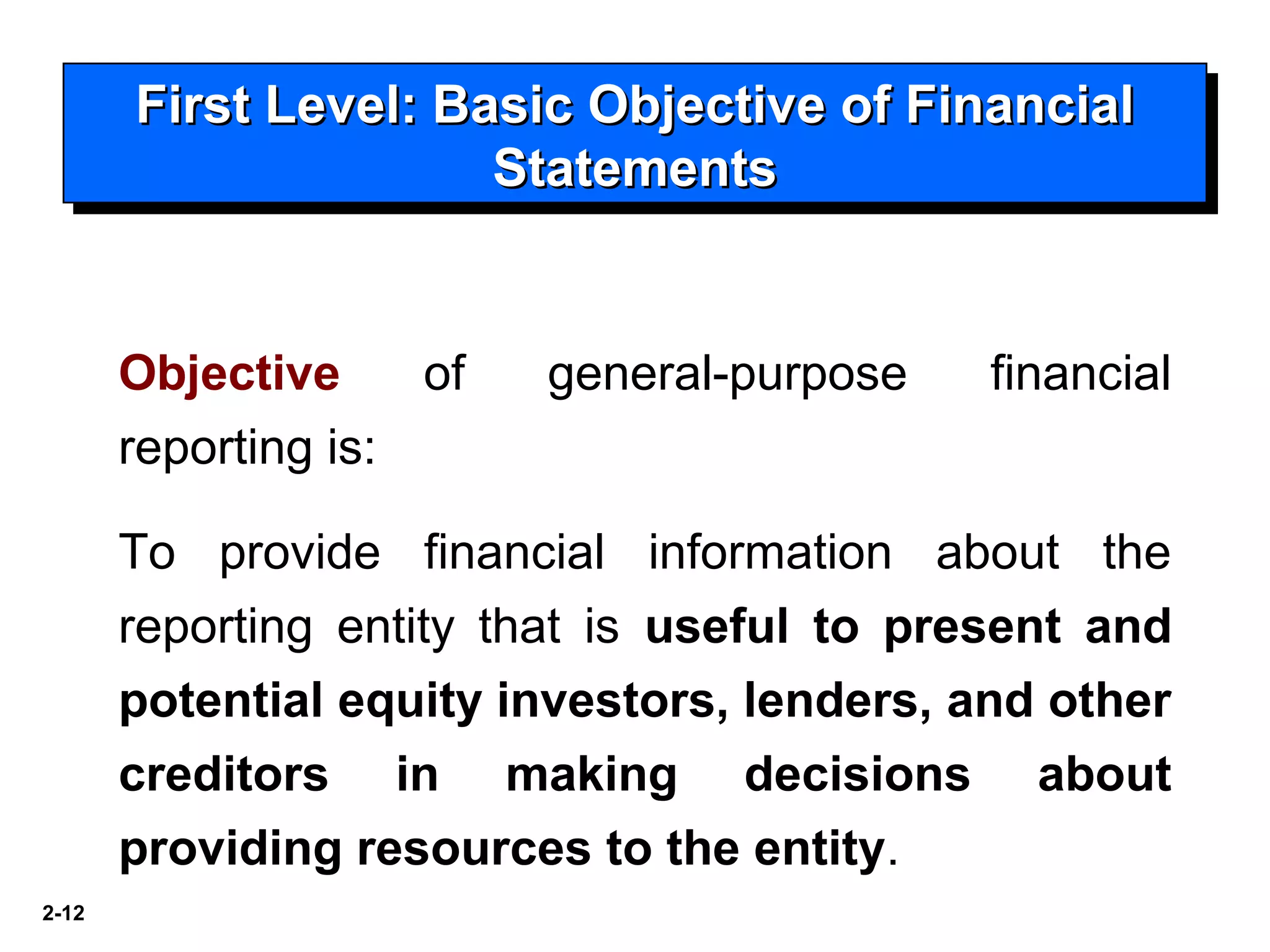

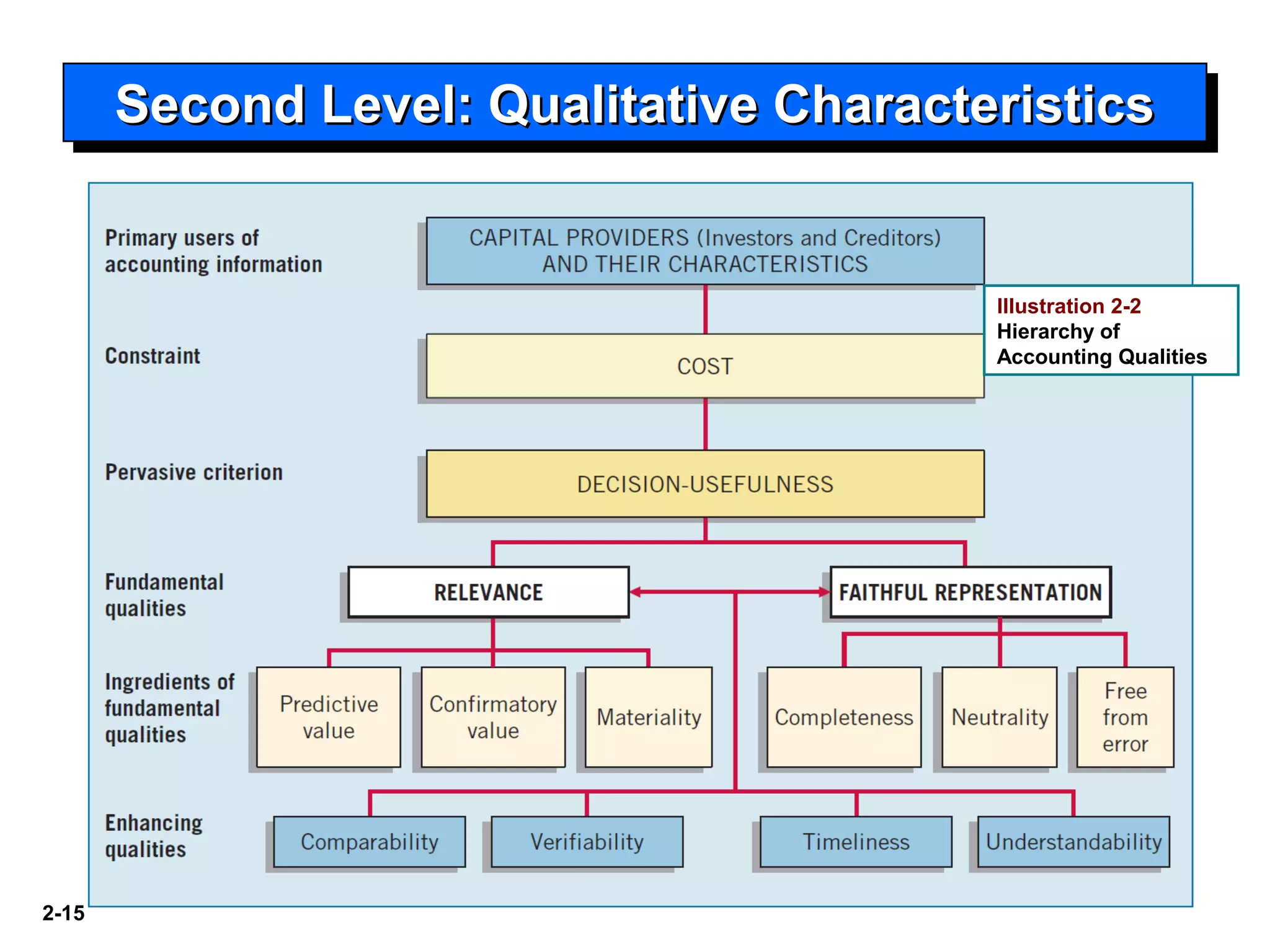

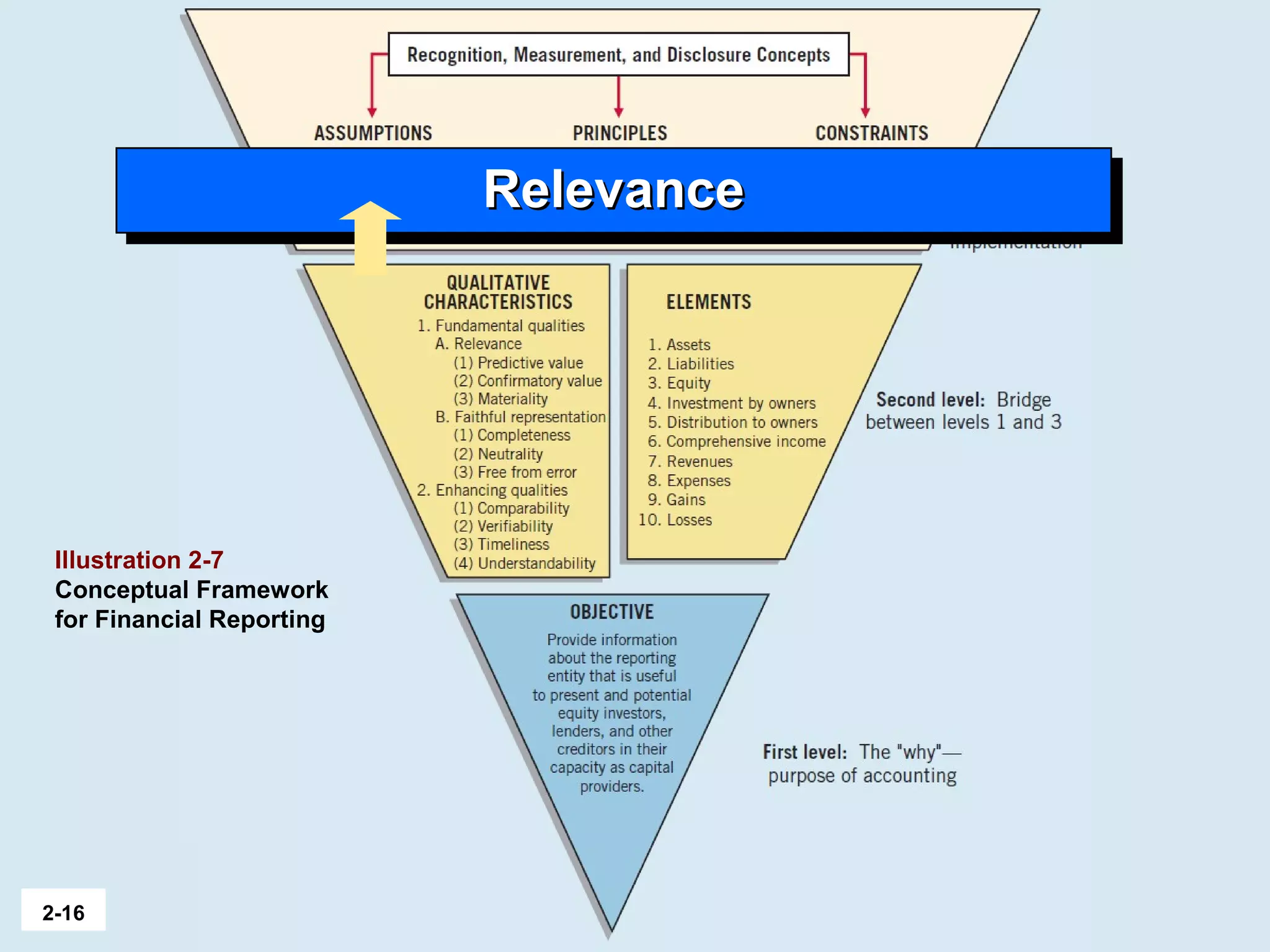

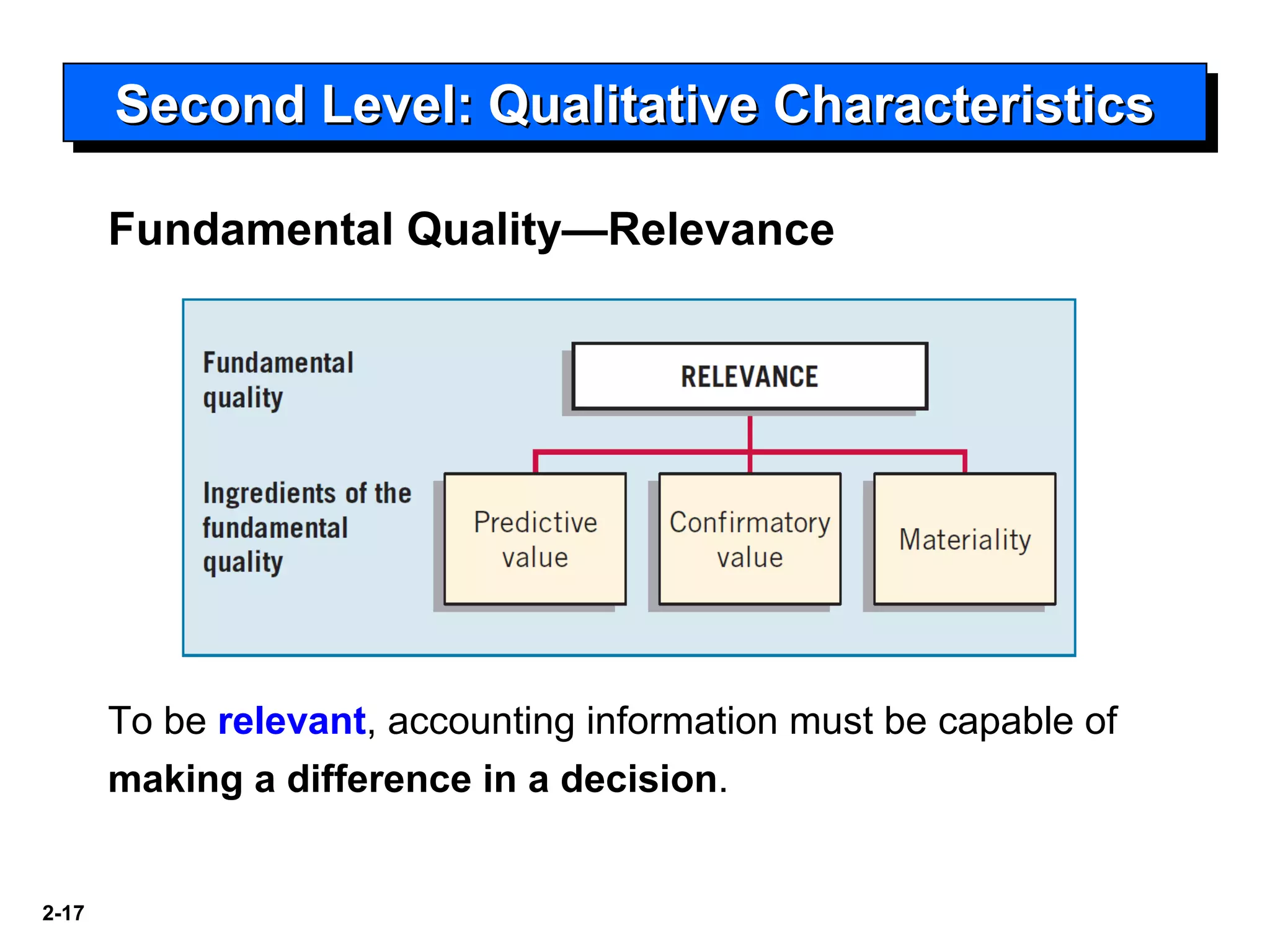

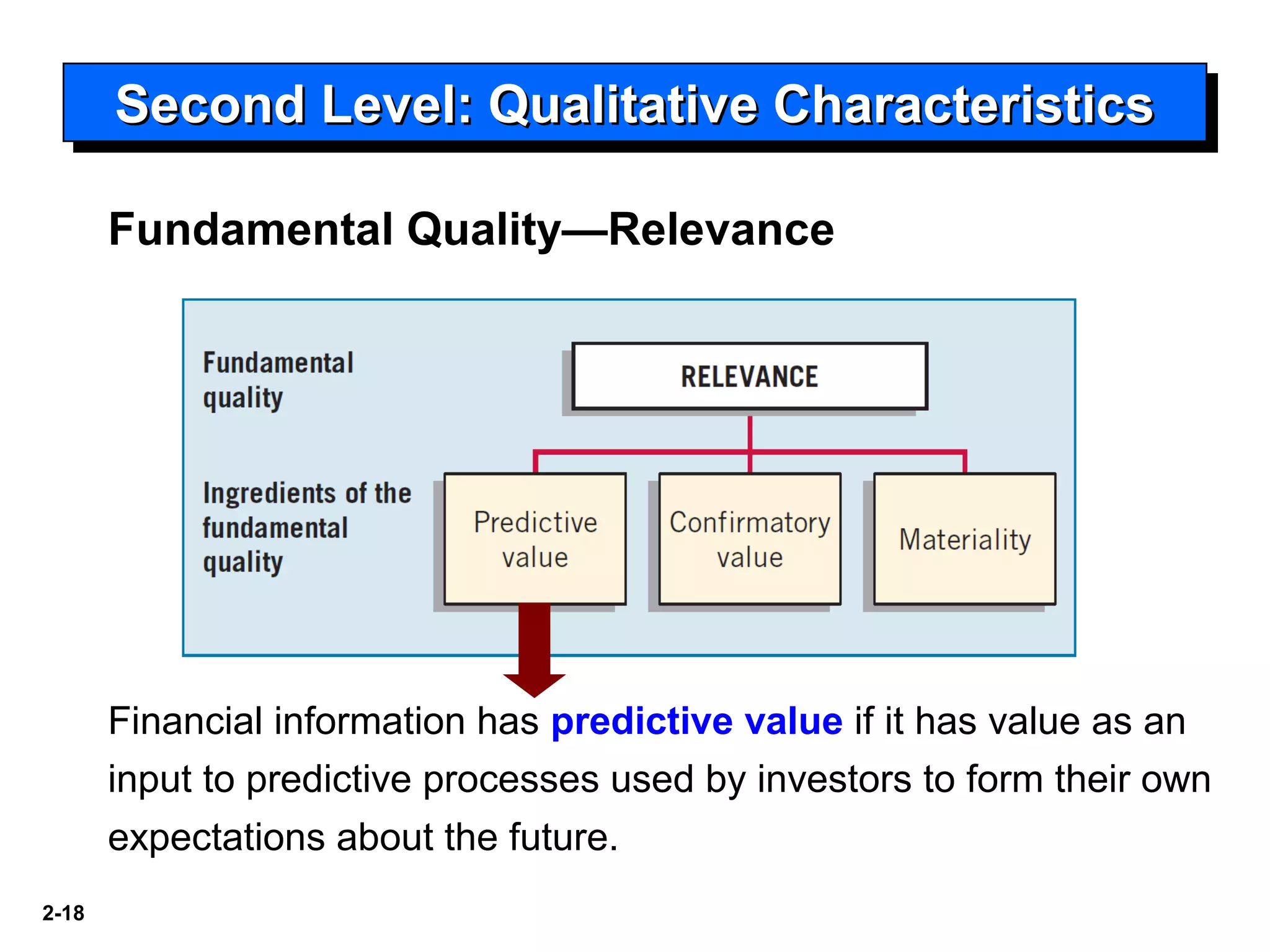

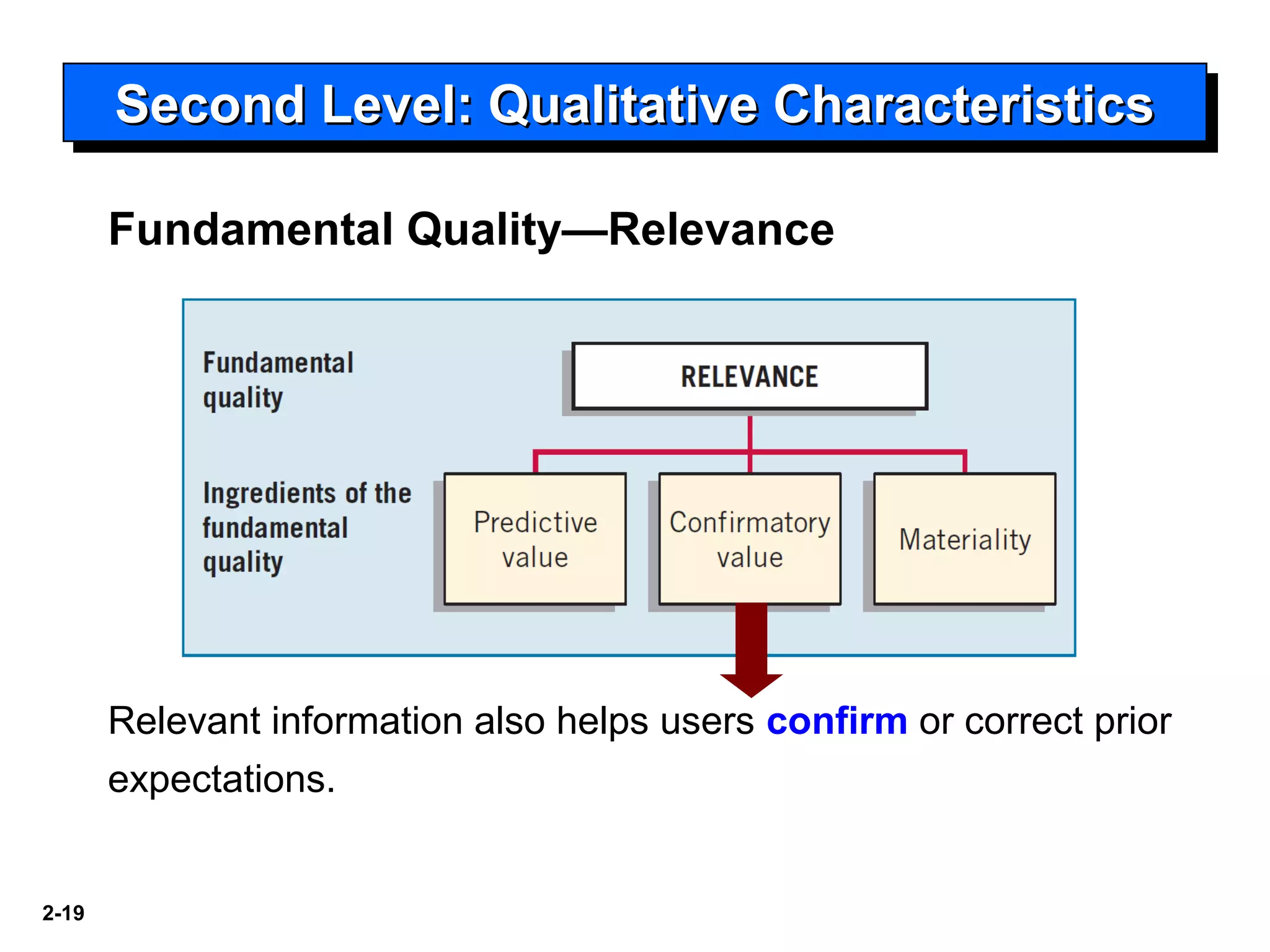

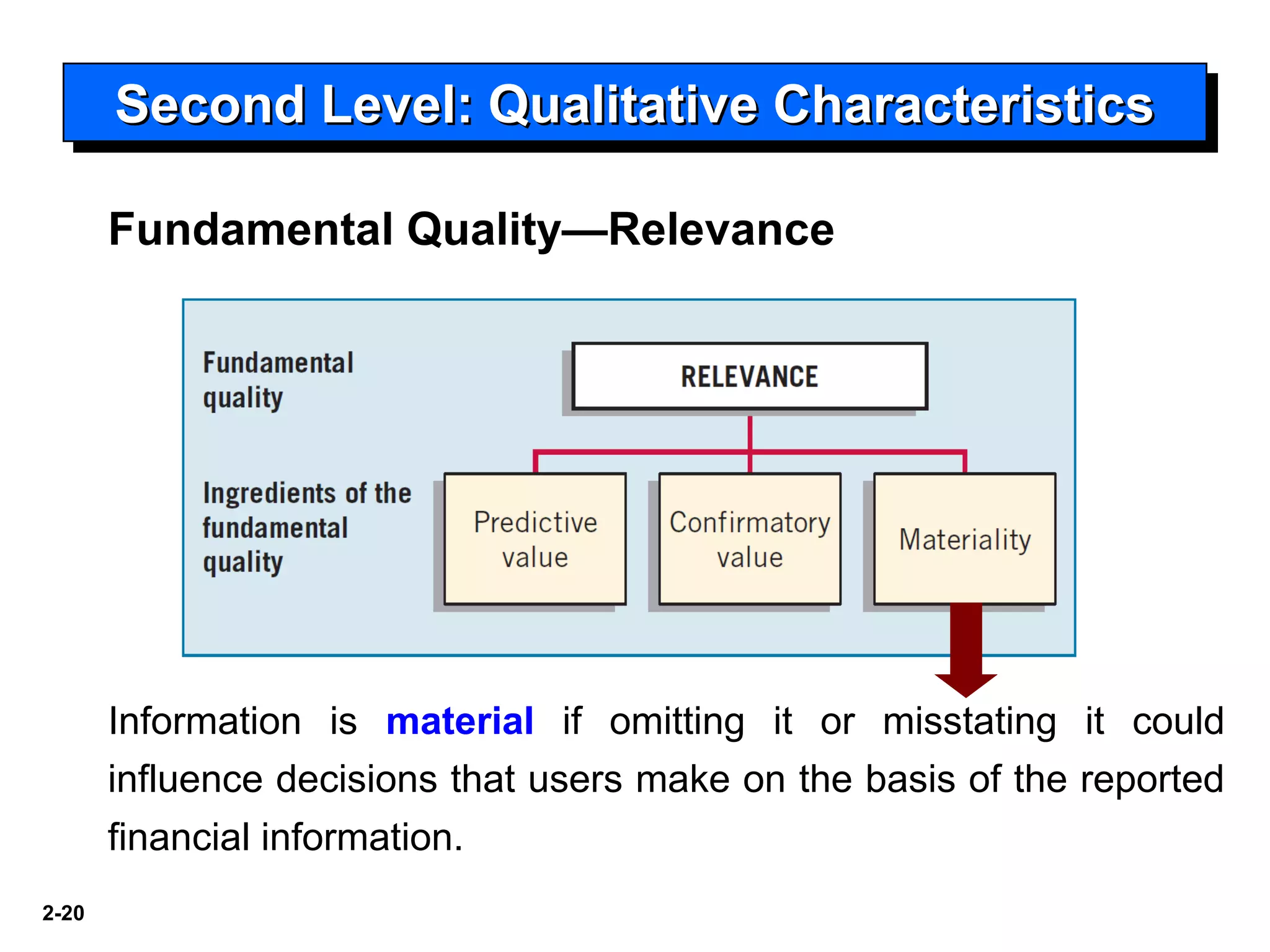

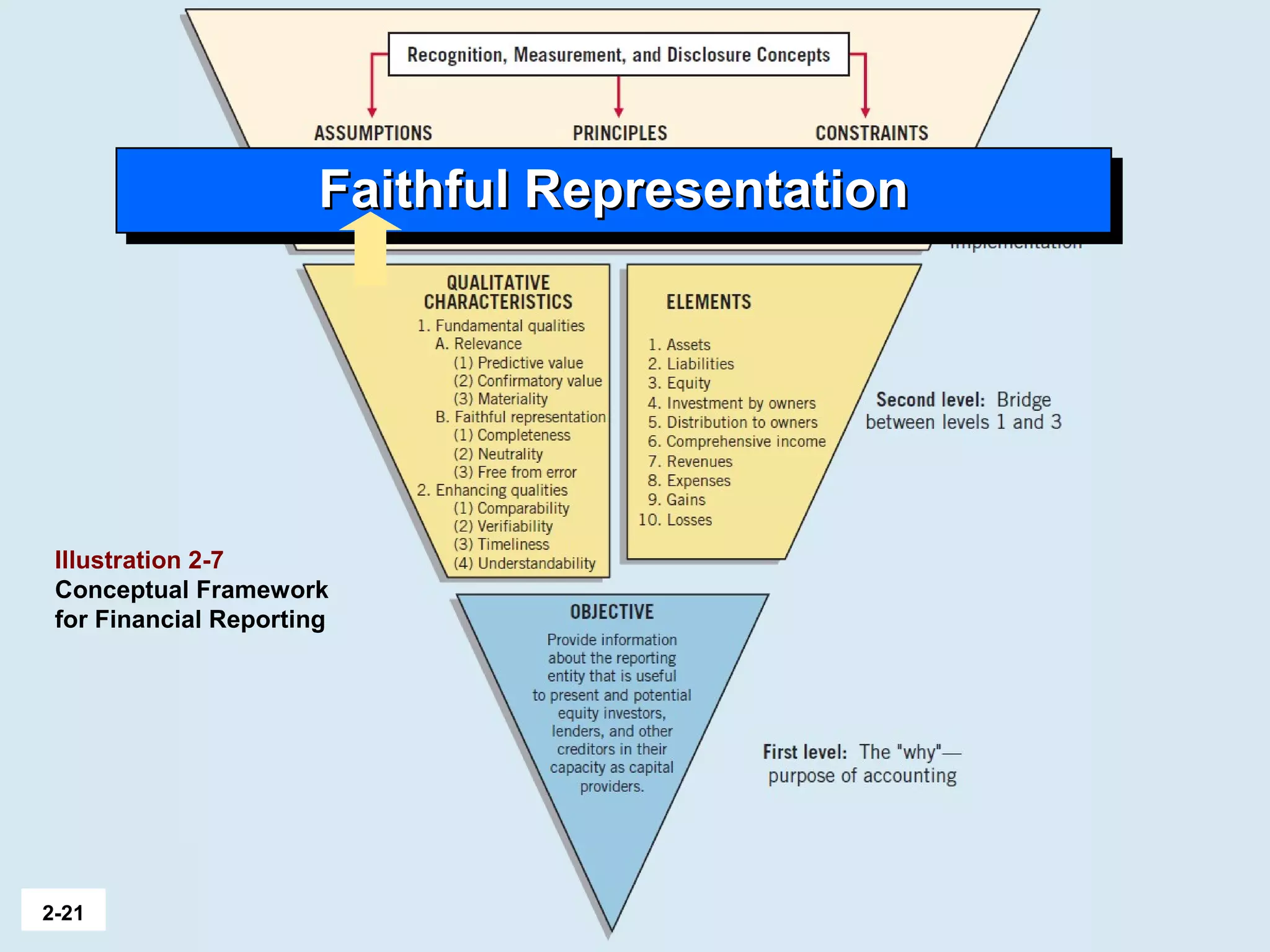

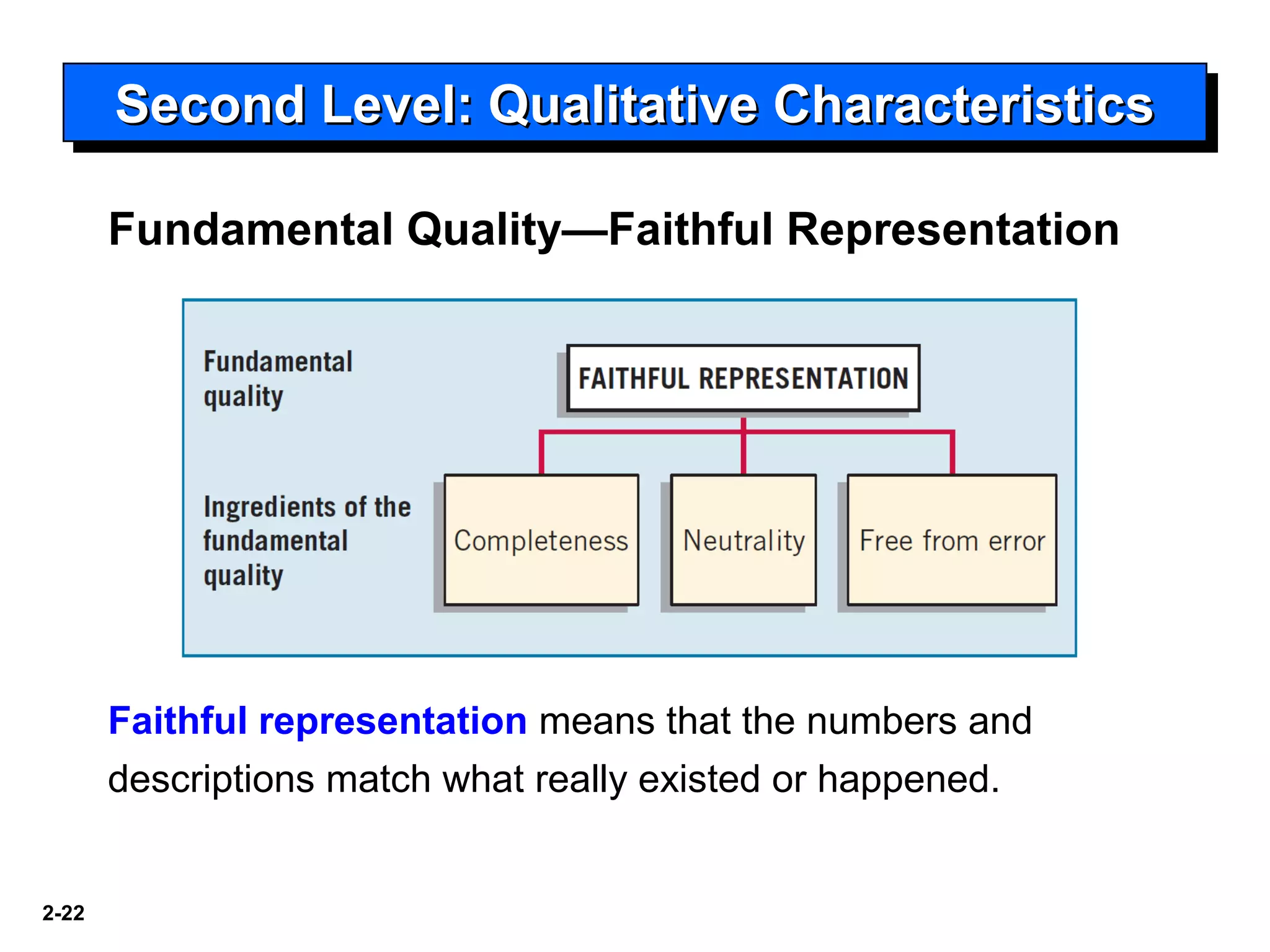

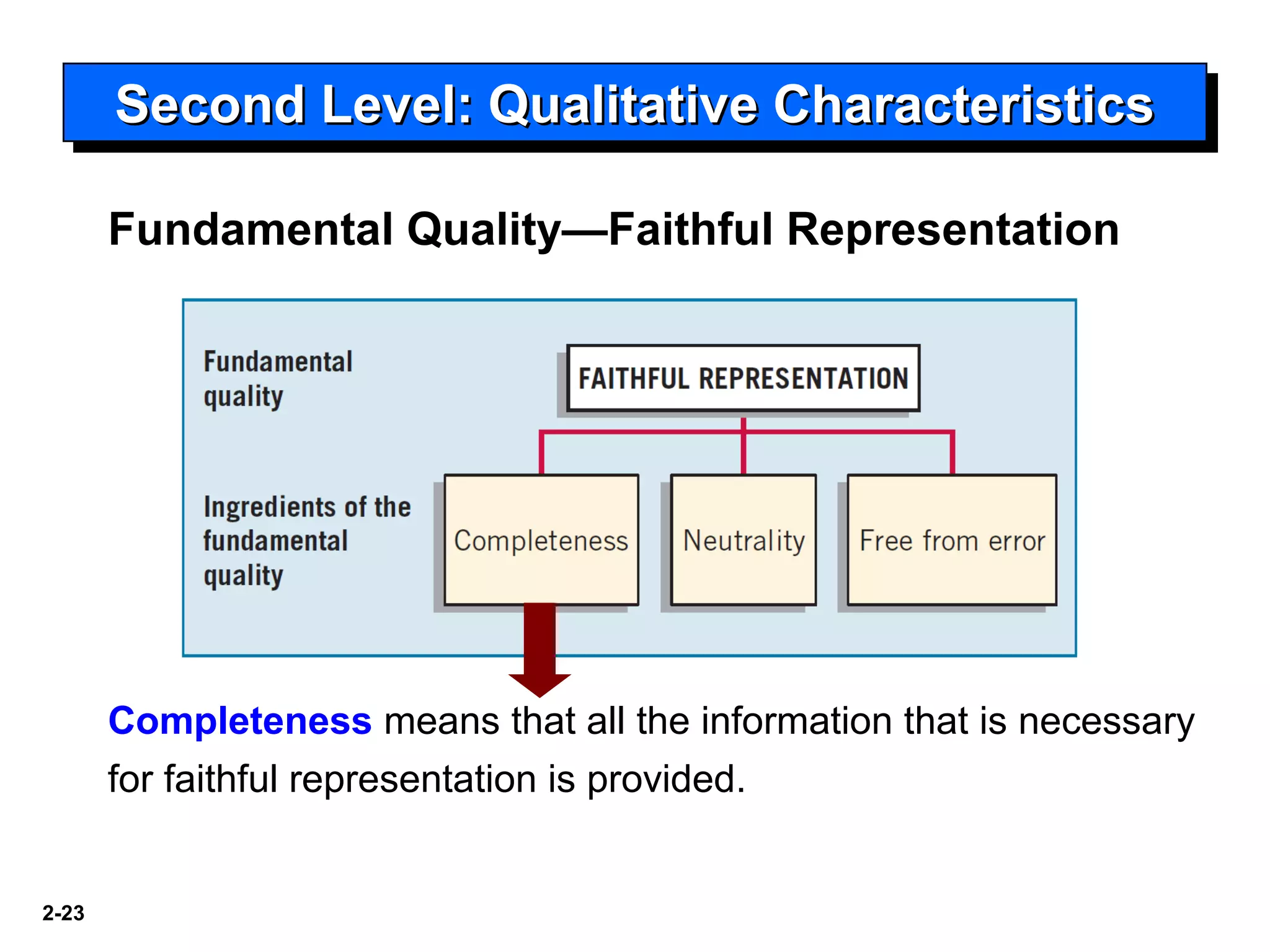

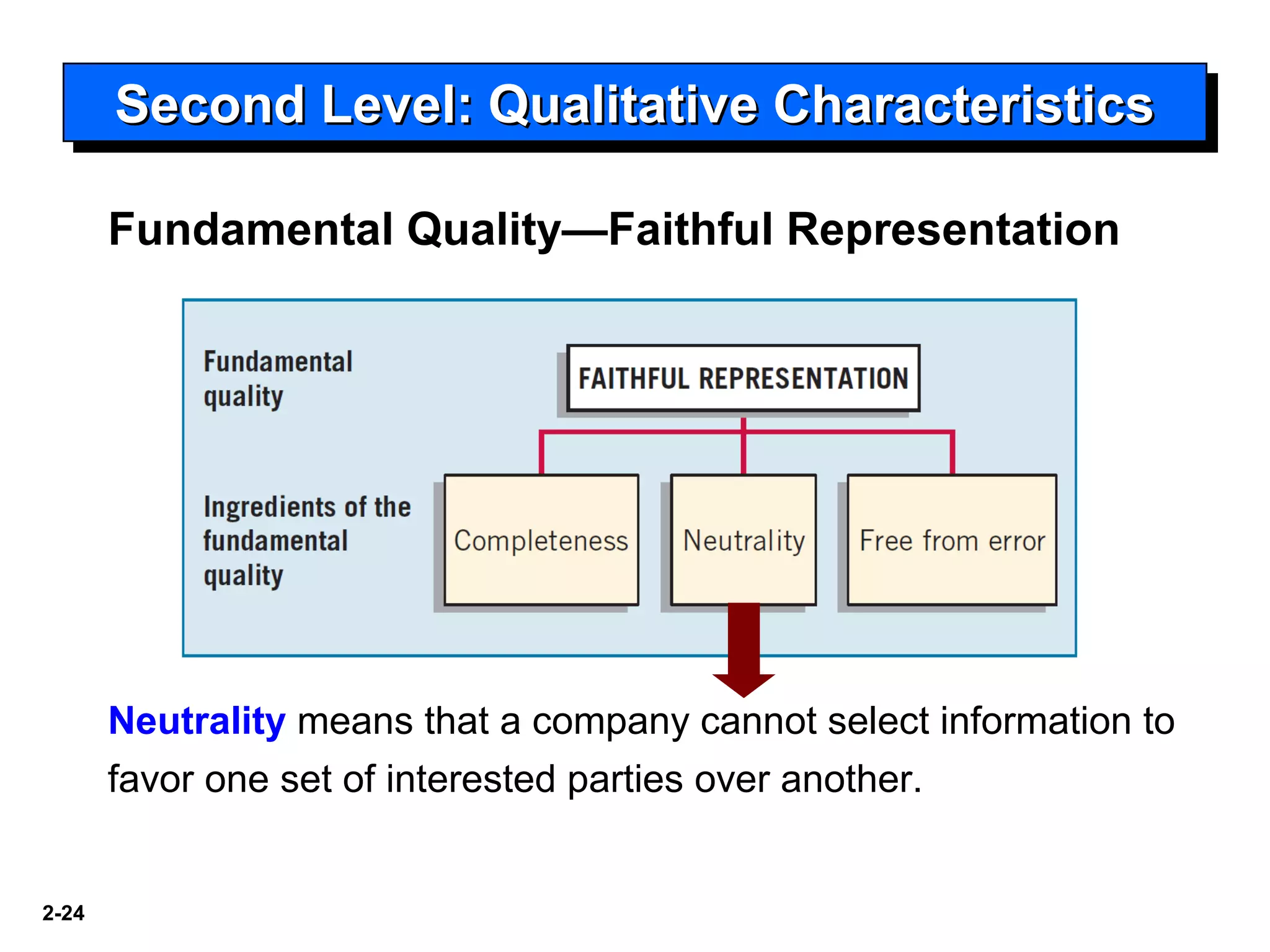

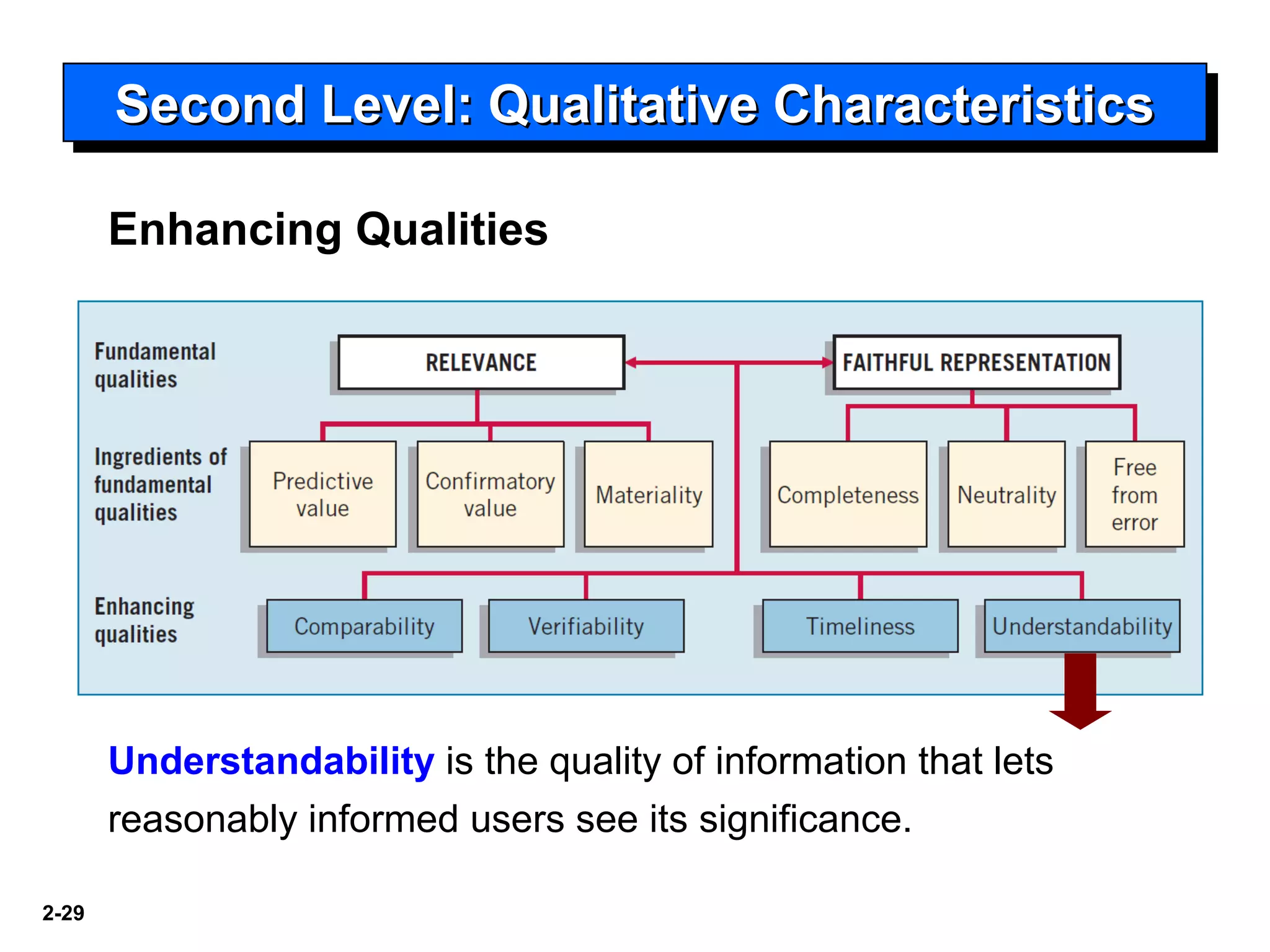

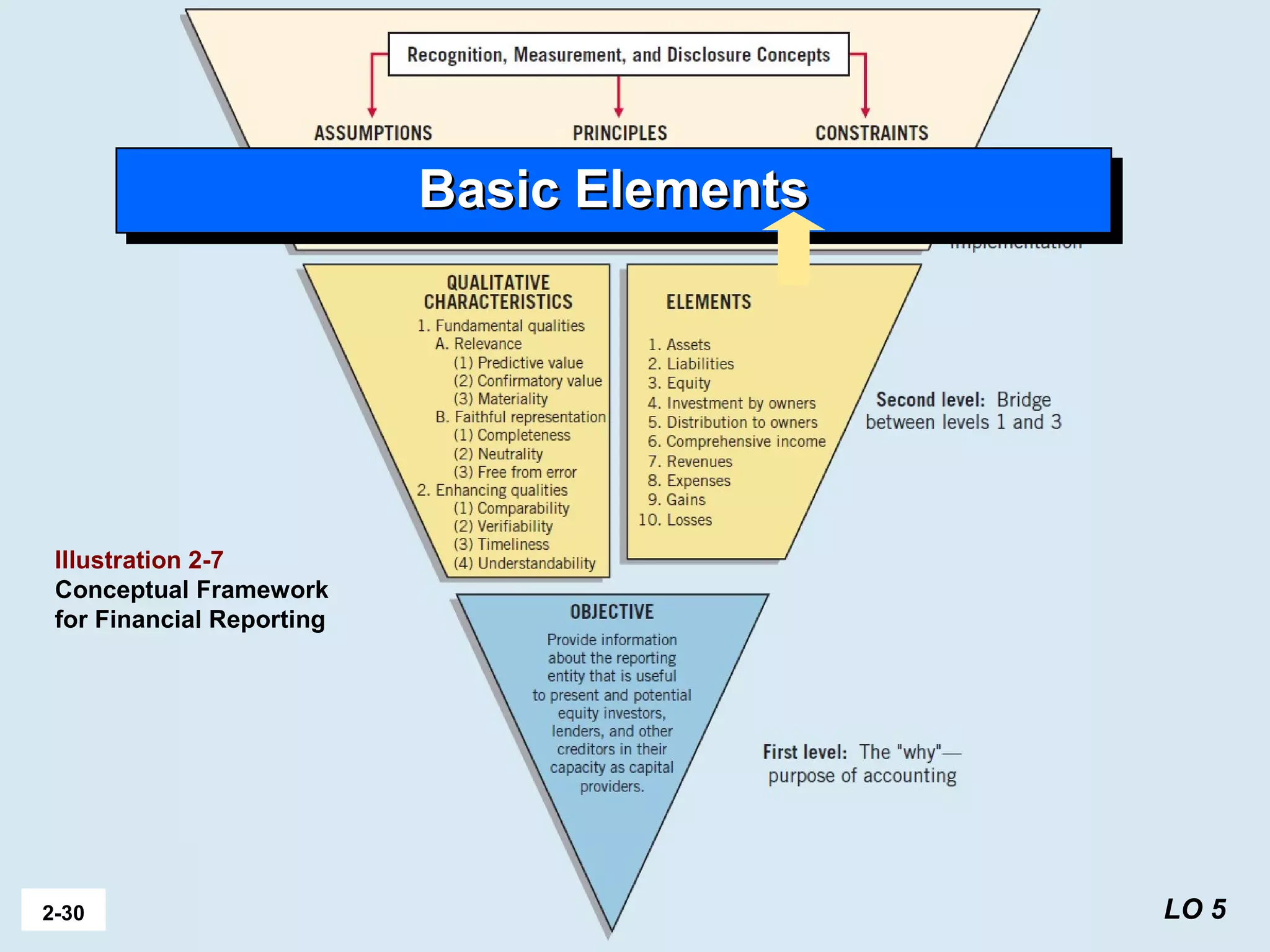

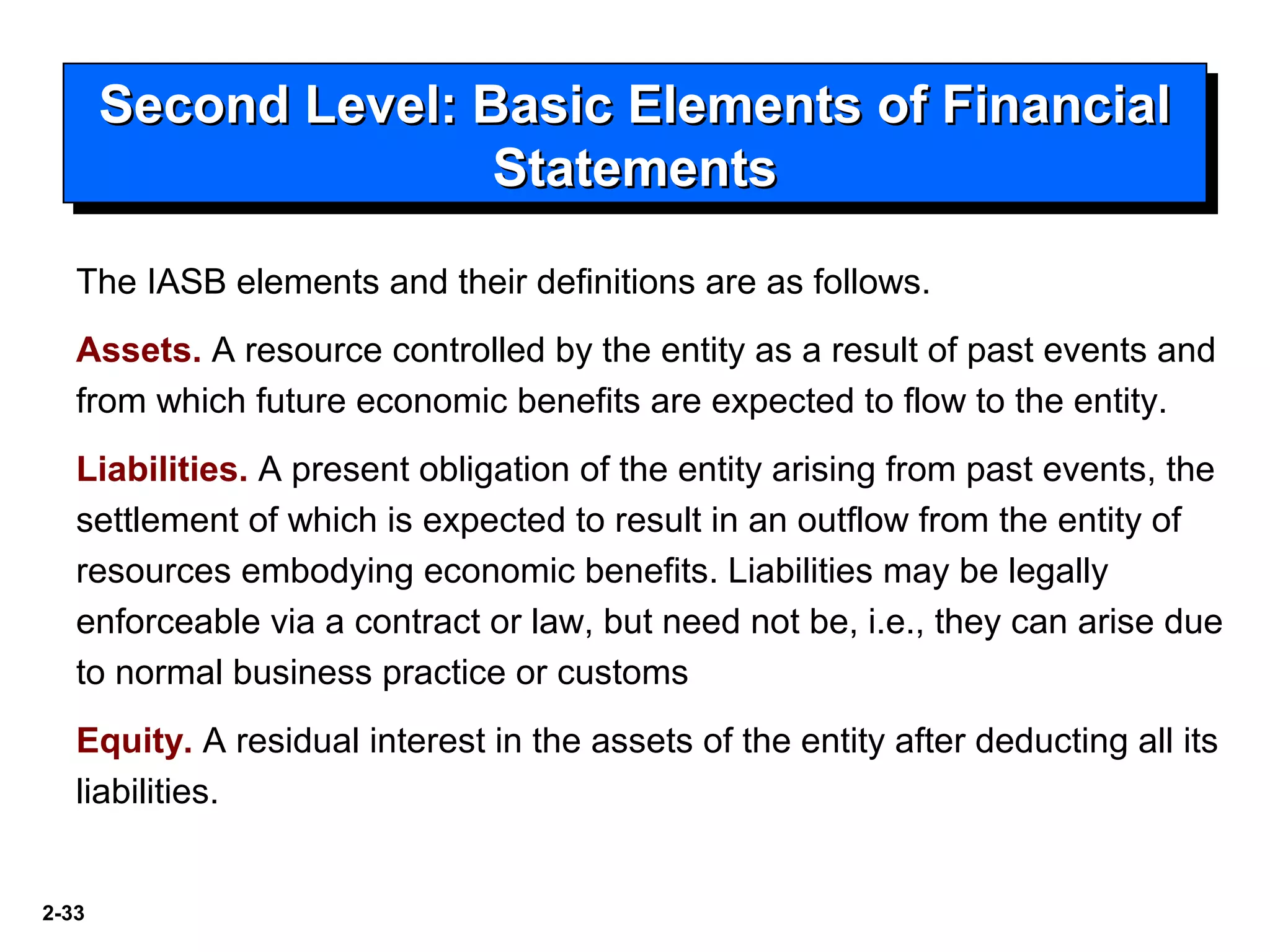

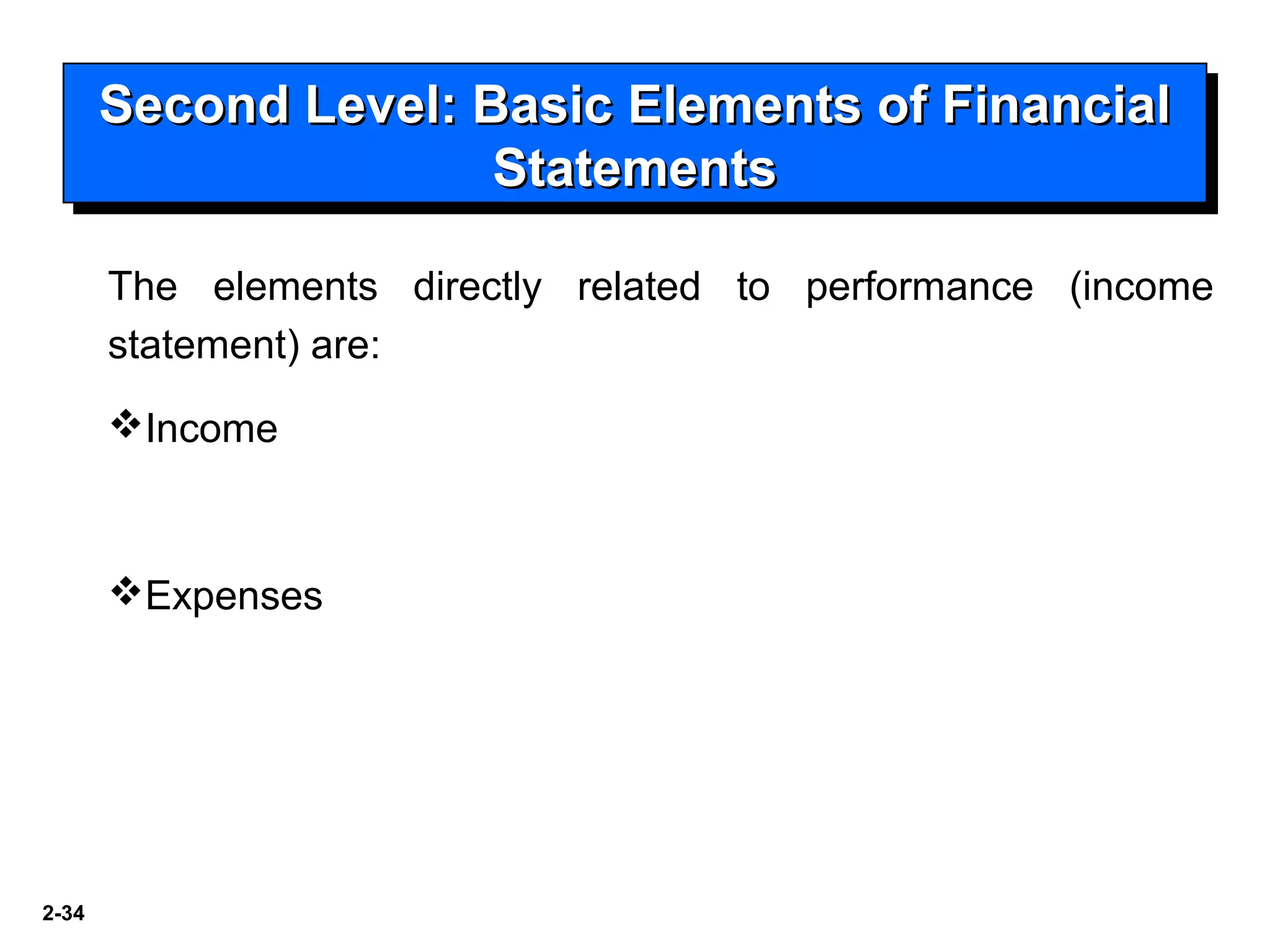

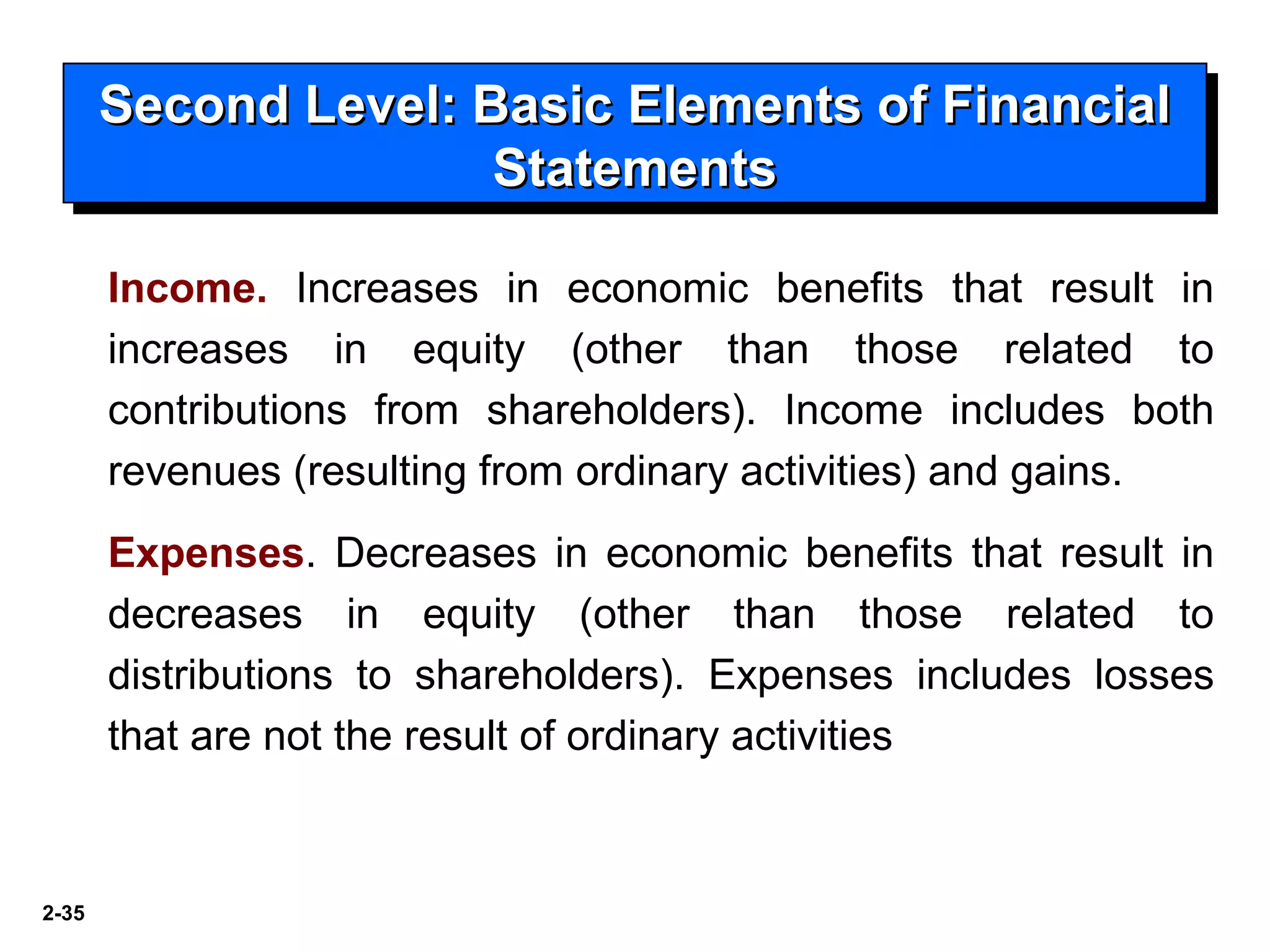

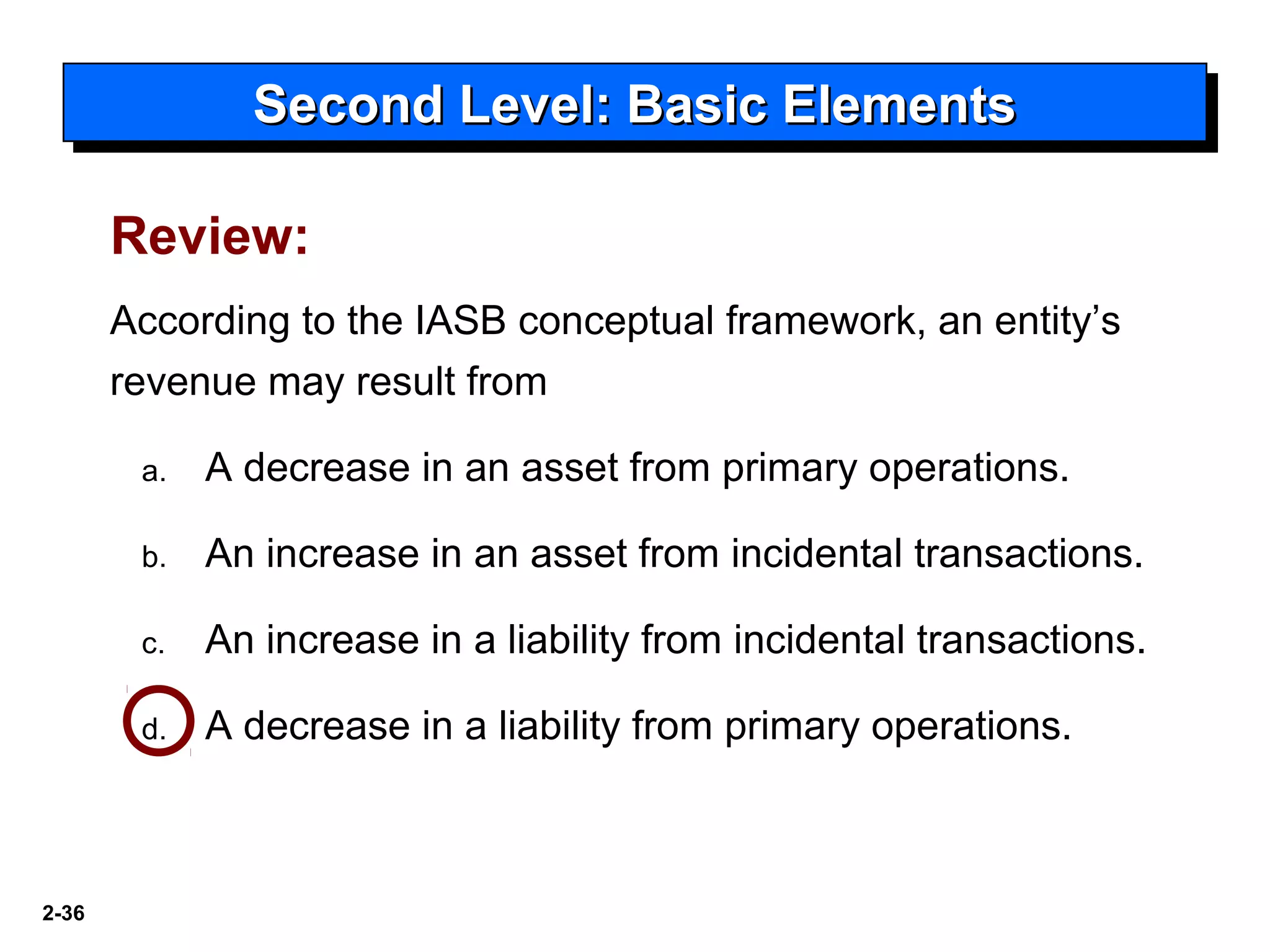

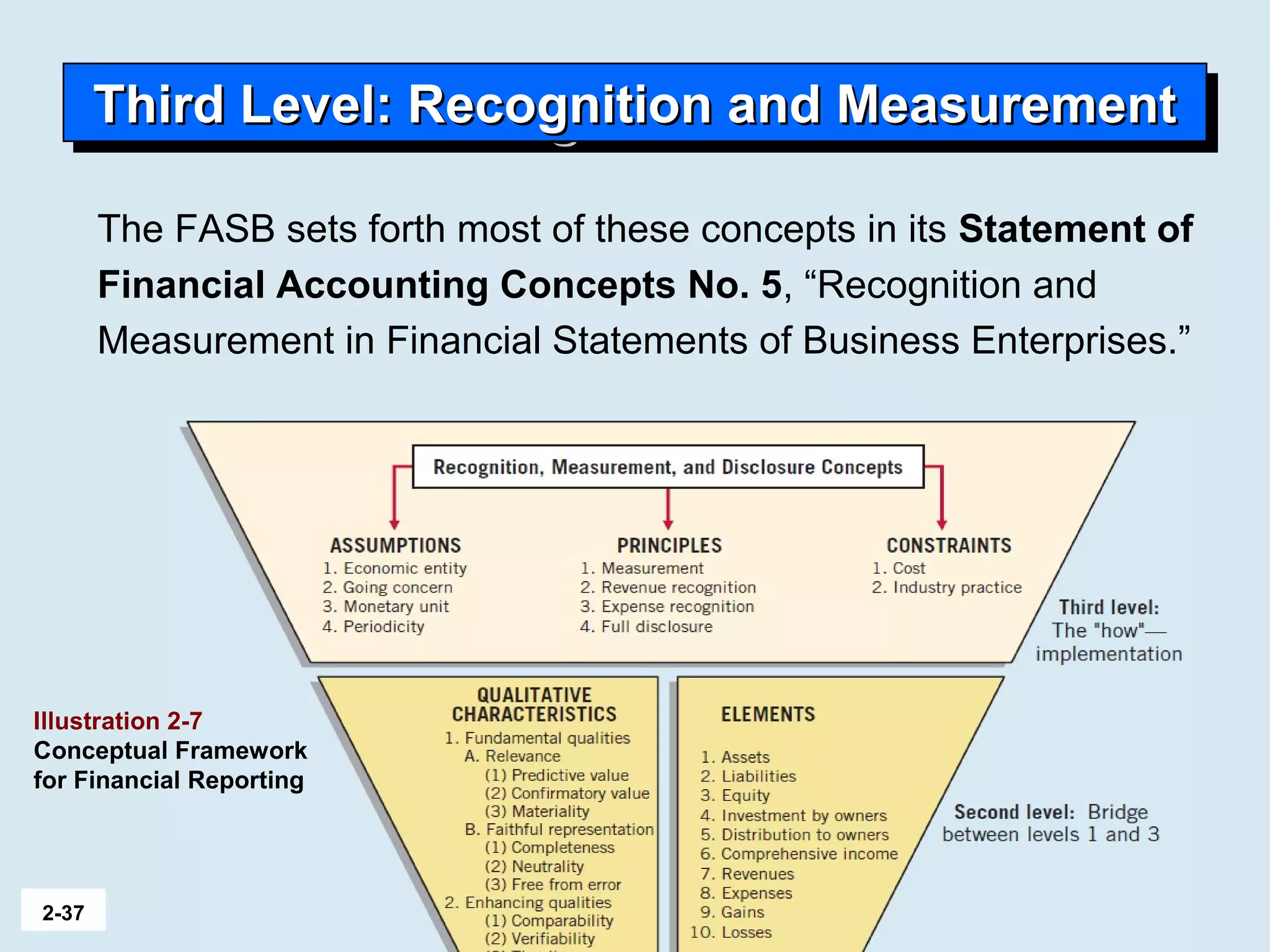

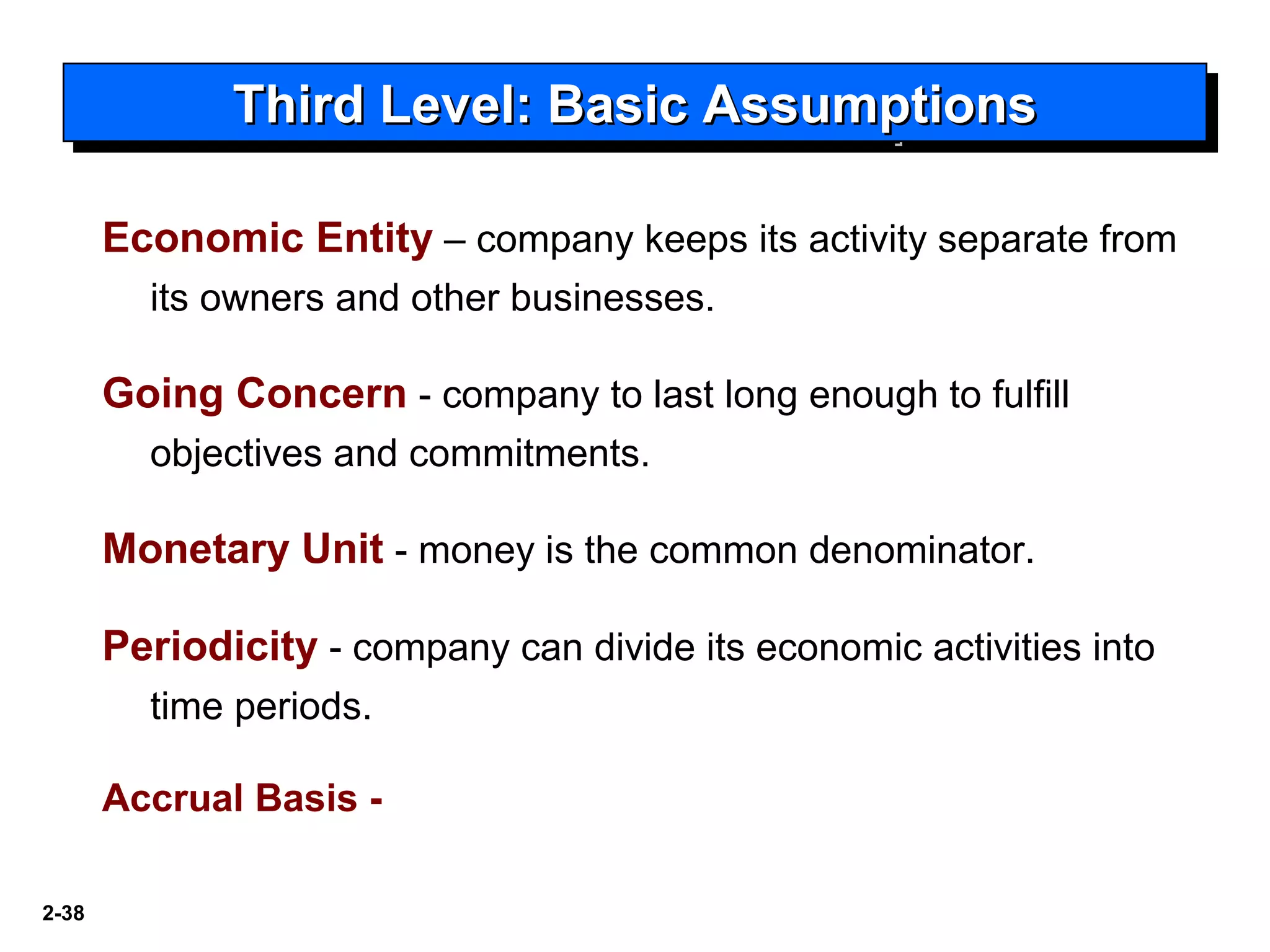

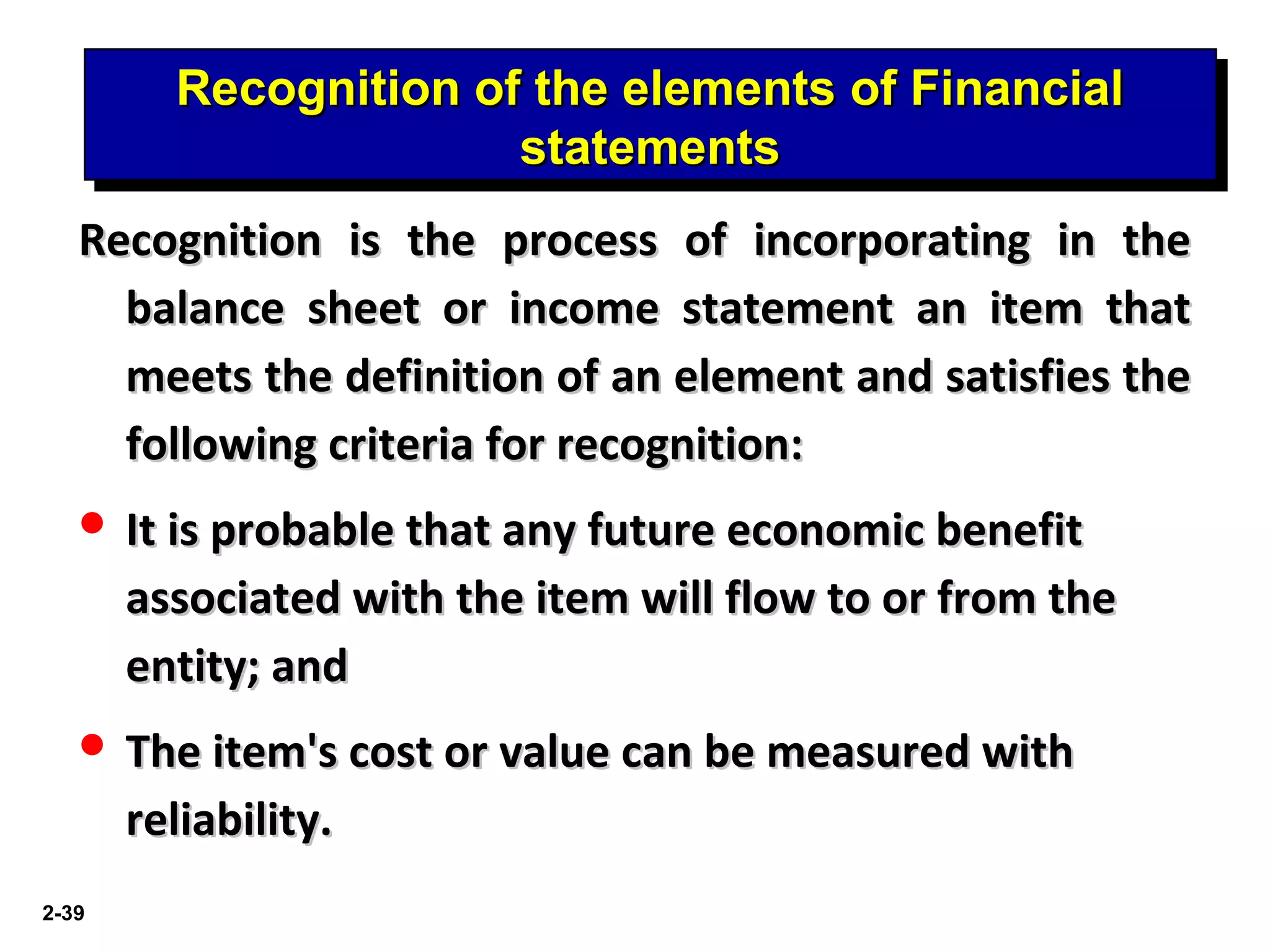

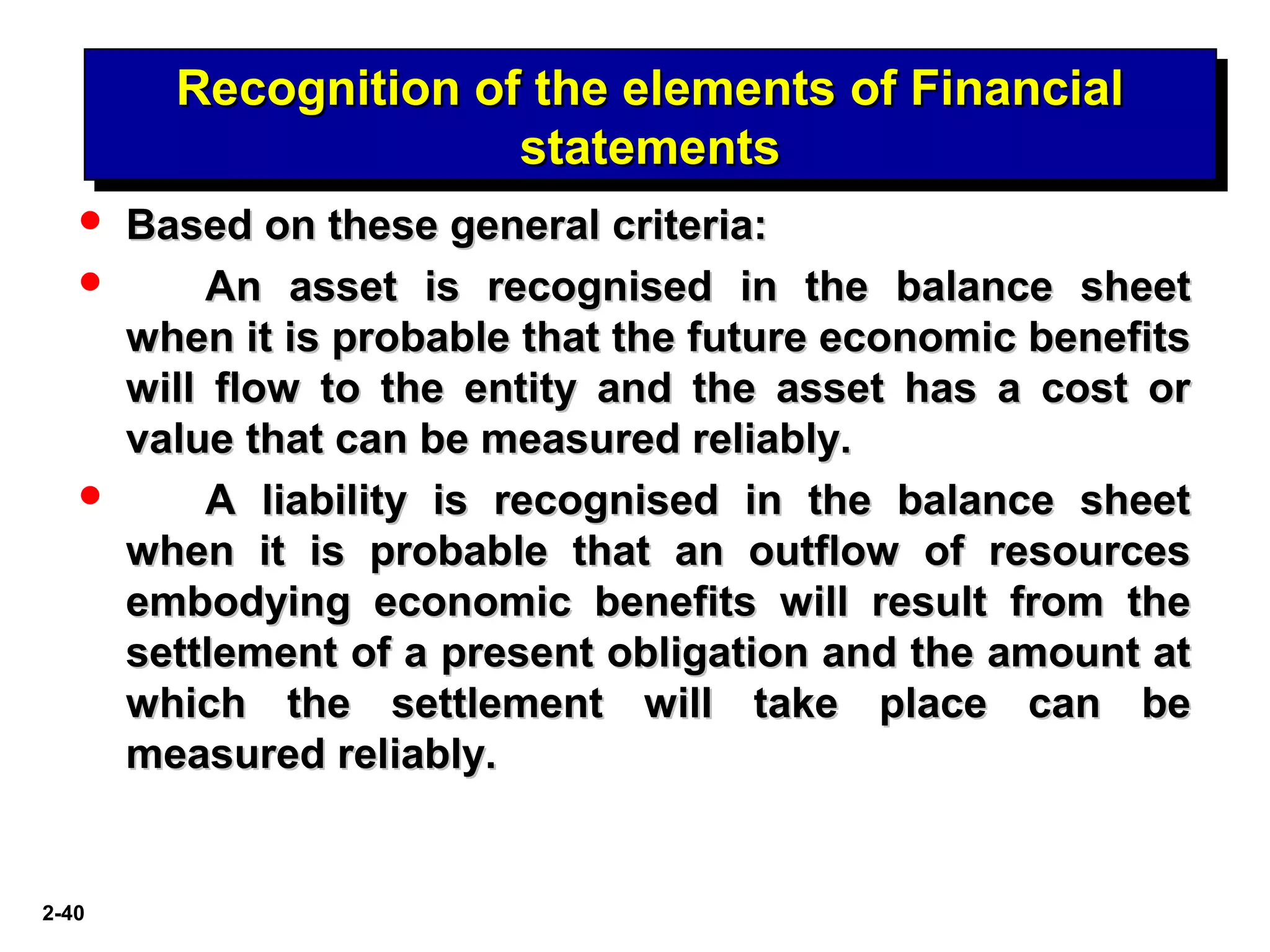

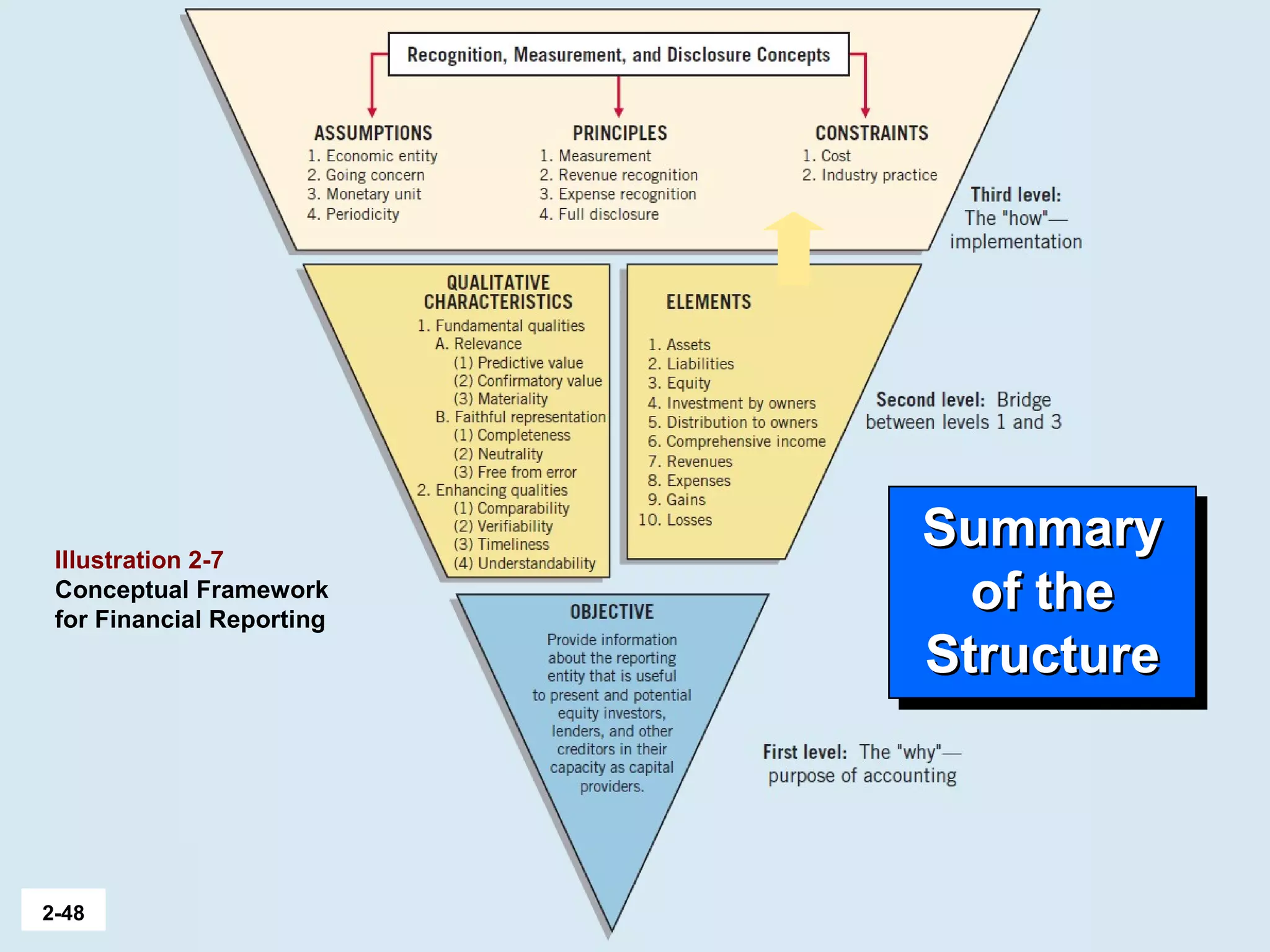

The document discusses the International Accounting Standards Board's (IASB) conceptual framework. It describes the need for a conceptual framework to develop coherent accounting standards and solve emerging problems. The conceptual framework establishes objectives of financial reporting and qualitative characteristics of useful accounting information. It identifies the basic elements of financial statements and underlying assumptions of accounting. The conceptual framework provides a consistent basis for setting standards.