Downloaded 420 times

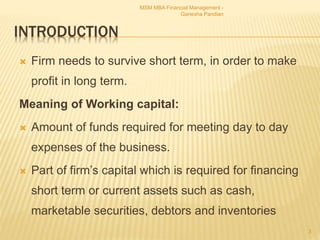

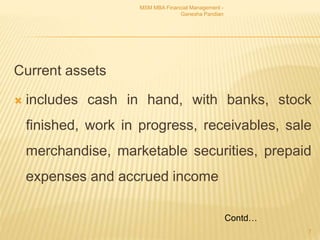

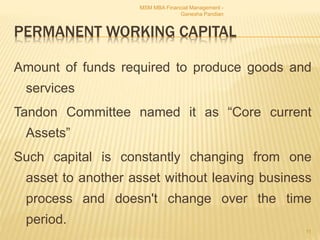

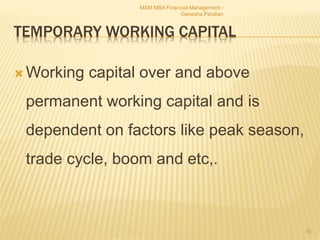

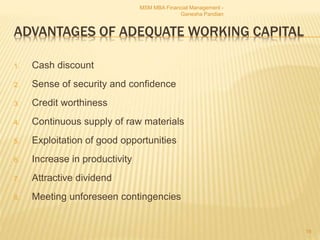

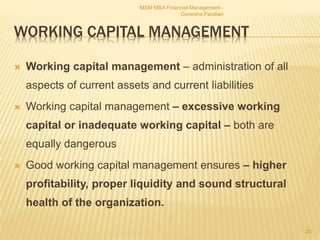

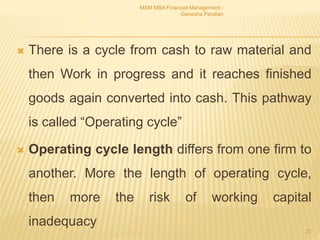

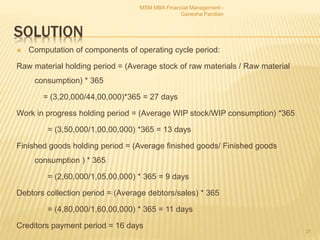

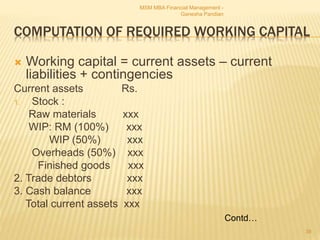

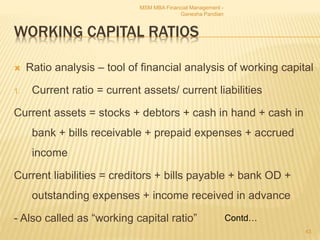

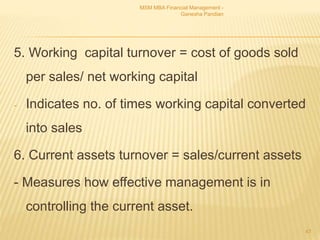

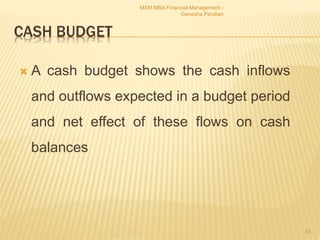

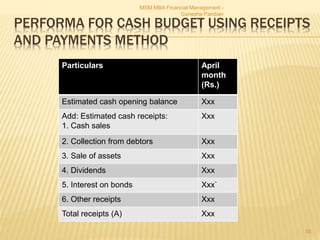

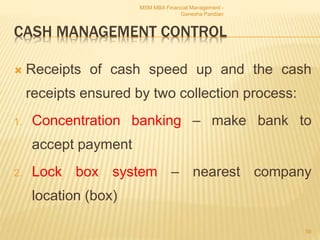

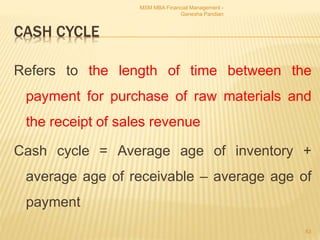

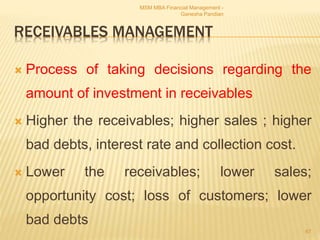

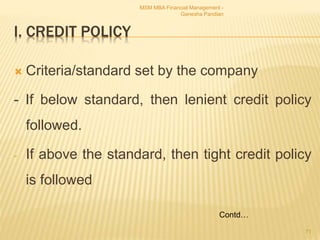

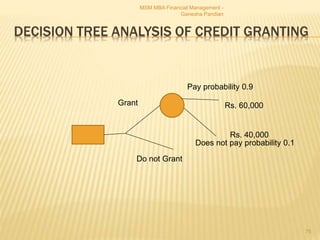

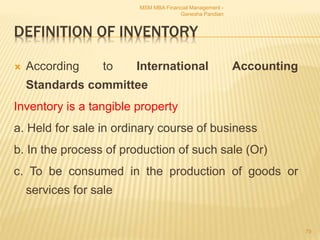

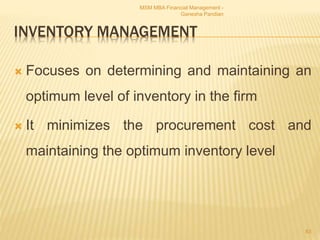

![FORMULA FOR ESTIMATING CURRENT ASSETS

a. Stock of raw materials = [ estimated production

* estimated cost of RM/unit]*Average RM

holding period/365

b. Stock of finished goods = [estimated

production * estimated cost of production/unit] *

average holding period of finished goods/365

MSM MBA Financial Management -

Ganesha Pandian

35

Contd…](https://image.slidesharecdn.com/financialmanagementunit4workingcapitalmanagement-180326172135/85/Financial-management-unit-4-working-capital-management-35-320.jpg)

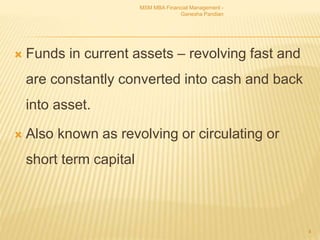

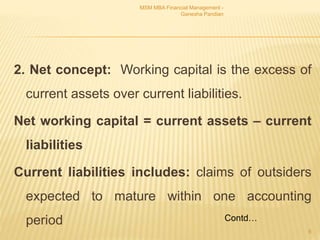

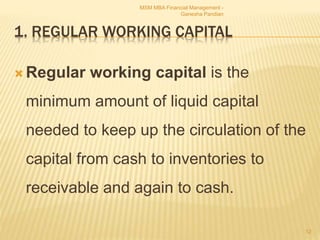

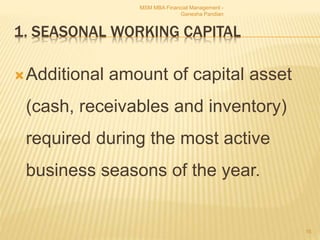

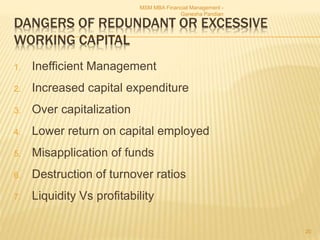

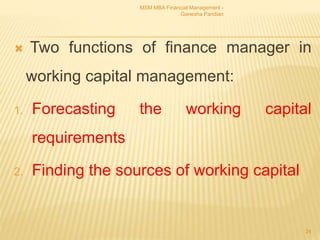

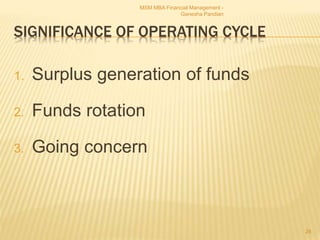

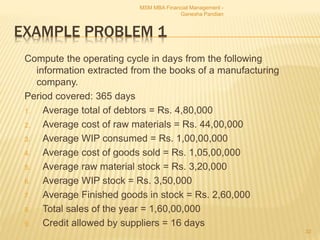

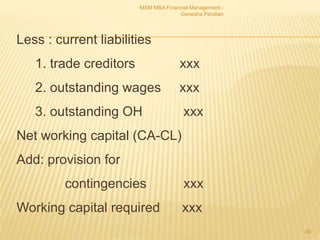

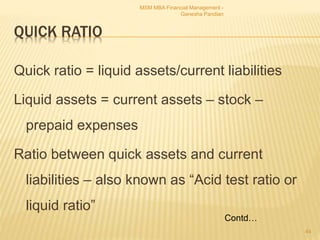

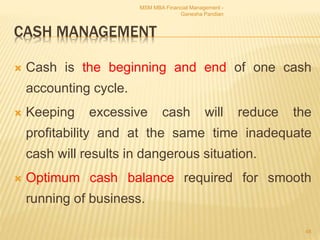

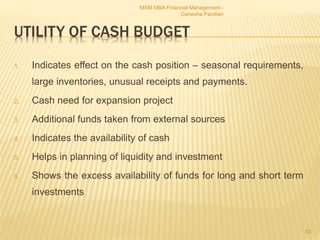

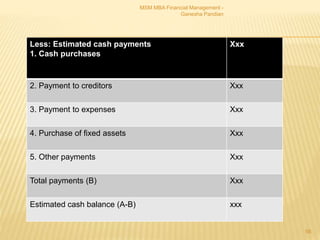

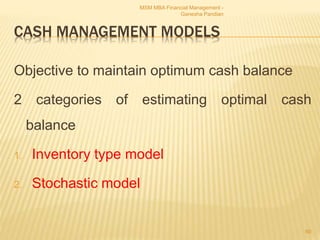

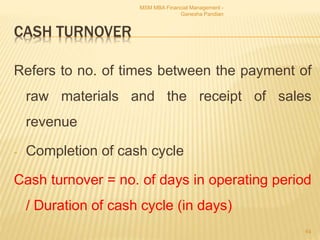

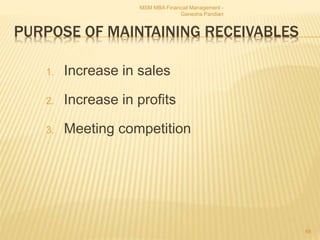

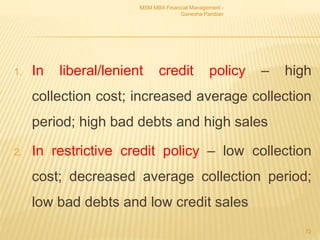

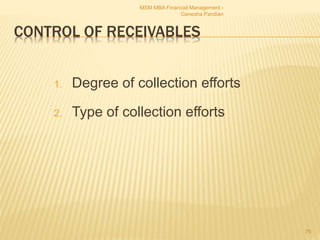

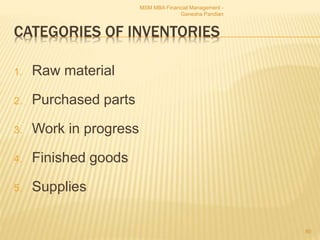

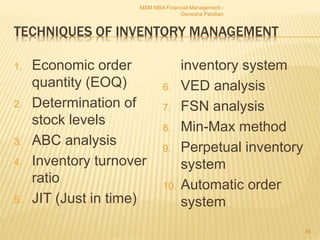

![ Stock of Work in progress calculation is

different 50% labor and 50% overheads

consumed

[estimated production * estimated cost of Work in

progress]* average WIP holding period/365 =

xxx

Add: Labor

[estimated production * estimated cost of labor in

progress]* average WIP holding period/365 * 1/2 =

xxx

Add: overheads

[estimated production * estimated cost of overheads]*

average WIP holding period/365*1/2 =

xxx

MSM MBA Financial Management -

Ganesha Pandian

36

Contd…](https://image.slidesharecdn.com/financialmanagementunit4workingcapitalmanagement-180326172135/85/Financial-management-unit-4-working-capital-management-36-320.jpg)

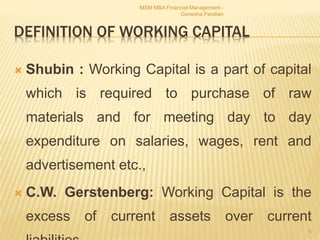

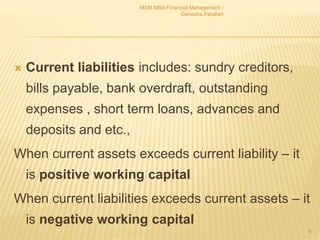

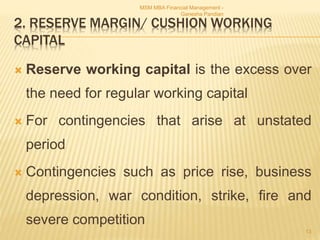

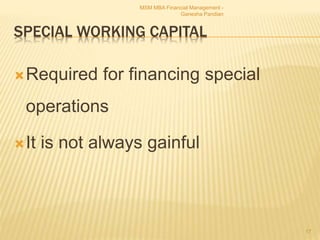

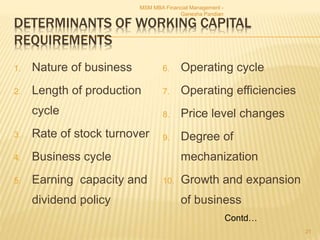

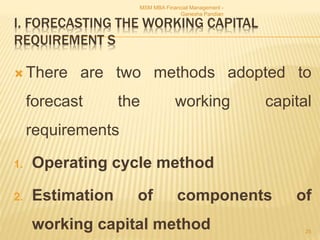

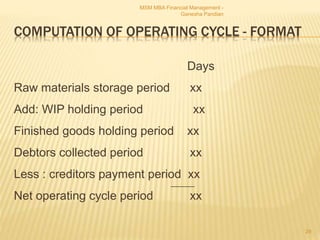

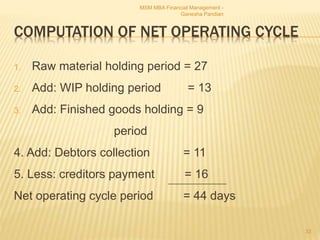

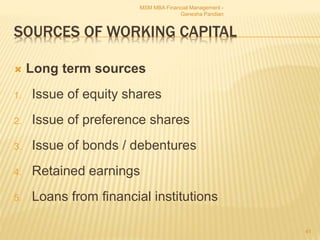

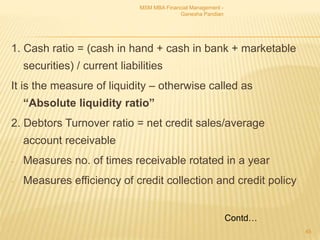

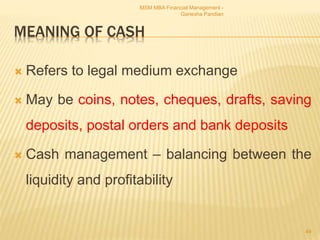

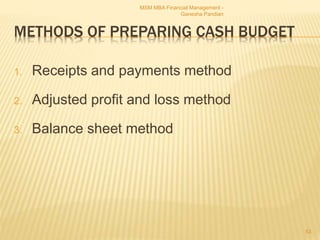

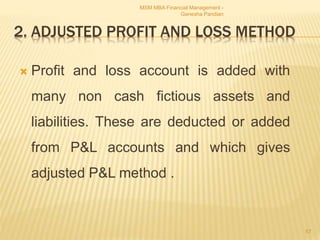

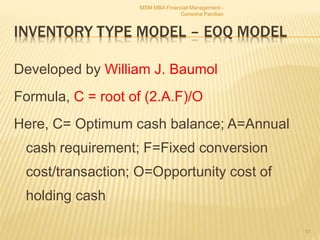

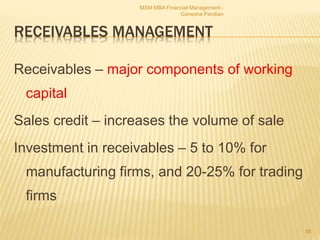

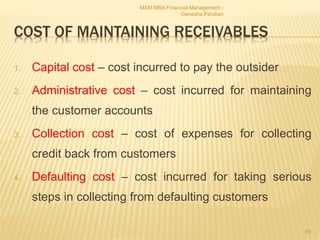

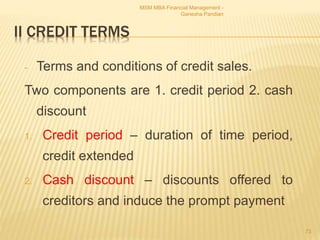

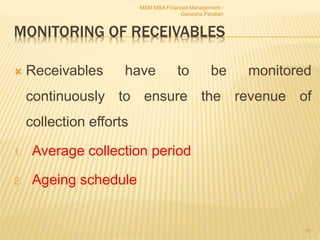

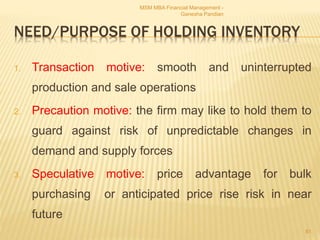

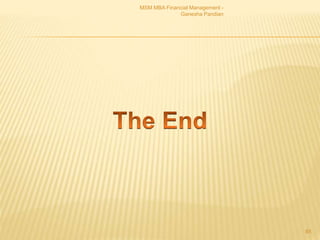

![C, stock of finished goods = [estimated

production*cost of

production/unit]*Average holding period of

finished goods/365

D, Trade debtors = [estimated credit

sales*cost of sales/units]* debt collection

period

MSM MBA Financial Management -

Ganesha Pandian

37](https://image.slidesharecdn.com/financialmanagementunit4workingcapitalmanagement-180326172135/85/Financial-management-unit-4-working-capital-management-37-320.jpg)

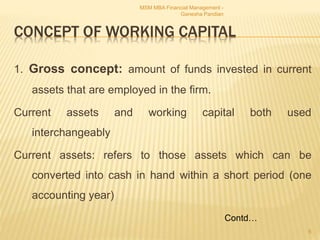

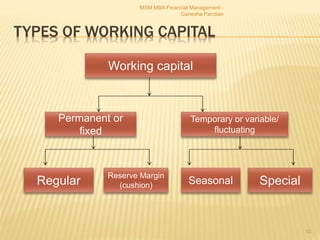

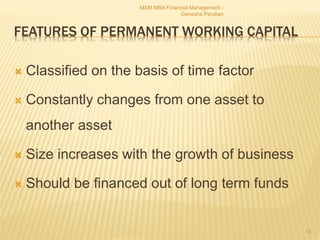

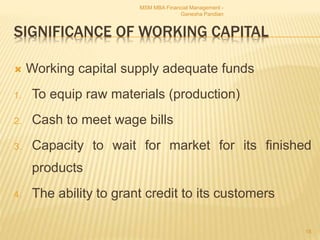

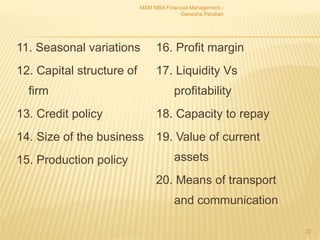

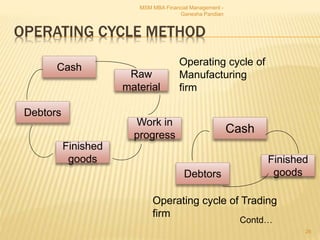

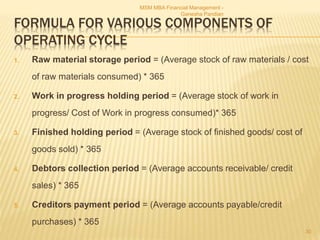

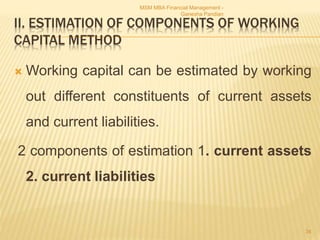

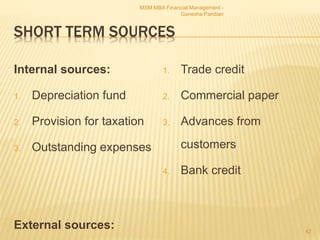

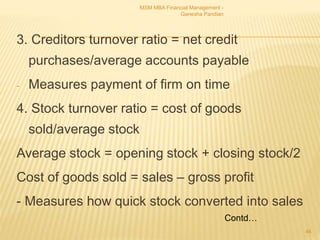

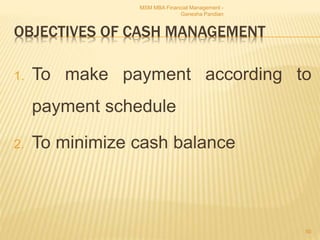

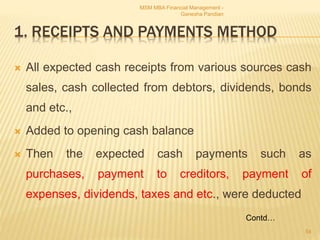

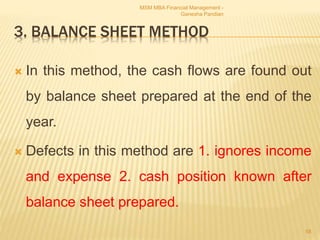

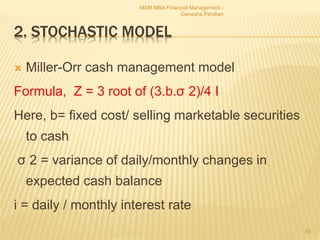

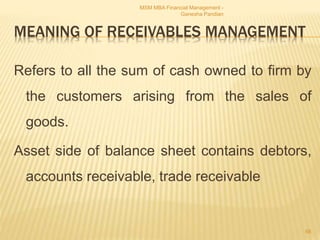

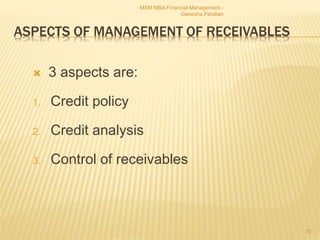

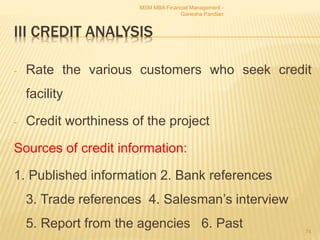

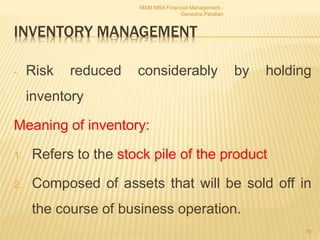

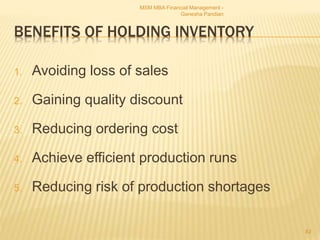

![FORMULA FOR ESTIMATING CURRENT

LIABILITIES

a. Trade creditors = [estimated production (units)* cost of raw

material/ unit] * average payment period/ 365

b. Outstanding expenses:

Outstanding wages = [estimated production(units) * Direct labor] *

average time lag in payment of wages/365

Outstanding overheads = [estimated production (units)*

overheads/unit] * average time lag of payment of OH/365

Note: In case of selling overheads, the relevant item would be

sales volume instead of production volume

MSM MBA Financial Management -

Ganesha Pandian

38](https://image.slidesharecdn.com/financialmanagementunit4workingcapitalmanagement-180326172135/85/Financial-management-unit-4-working-capital-management-38-320.jpg)

This document provides an overview of working capital management. It defines working capital as the amount of funds required for meeting day-to-day business expenses. There are different types of working capital including permanent, temporary, seasonal and special working capital. The document outlines methods for estimating working capital requirements such as the operating cycle method and estimating components. It also discusses sources of working capital, working capital ratios and issues around having too much or too little working capital.