Downloaded 16 times

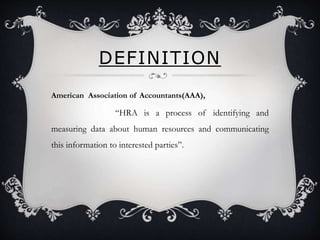

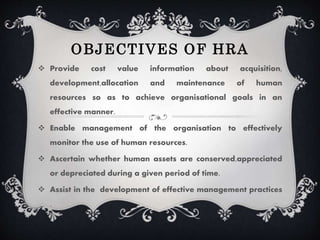

Human resource accounting is defined as identifying and measuring data about human resources and communicating this information to interested parties. The objectives of HRA are to provide cost information about acquiring, developing, allocating, and maintaining human resources to achieve organizational goals effectively, enable management to monitor human resource use, and determine if human assets are conserved, appreciated or depreciated over time. HRA advantages include providing useful information about an organization's human capital, strengths and weaknesses of employees, and evaluating HR policies and practices effectiveness. Limitations are lack of clear guidelines distinguishing human resource costs and value, measurement problems, and potential lack of employee and union acceptance. HRA valuation methods include monetary approaches like historical cost, replacement cost, opportunity cost, and asset