Downloaded 555 times

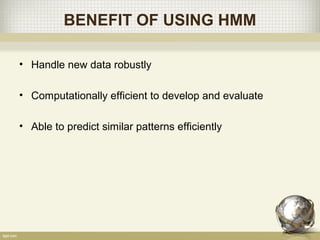

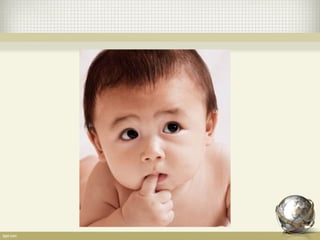

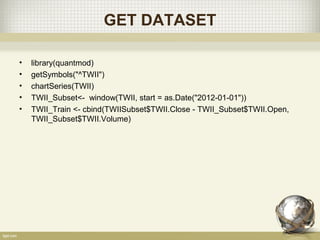

![SCATTER PLOT

• TWII_Predict <- cbind(TWII_Subset$TWII.Close, VitPath$states)

• chartSeries(TWII_Predict[,1])

• addTA(TWII_Predict[TWII_Predict[,2]==1,1],on=1,type="p",col=5,pch=25)

• addTA(TWII_Predict[TWII_Predict[,2]==2,1],on=1,type="p",col=6,pch=24)

• addTA(TWII_Predict[TWII_Predict[,2]==3,1],on=1,type="p",col=7,pch=23)

• addTA(TWII_Predict[TWII_Predict[,2]==4,1],on=1,type="p",col=8,pch=22)

• addTA(TWII_Predict[TWII_Predict[,2]==5,1],on=1,type="p",col=10,pch=21)](https://image.slidesharecdn.com/hmmandstock-130423115118-phpapp02/85/Hidden-Markov-Model-Stock-Prediction-17-320.jpg)

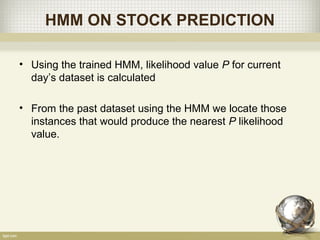

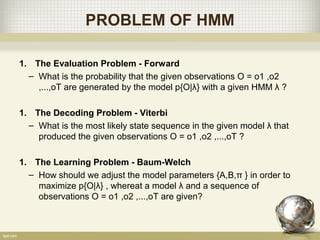

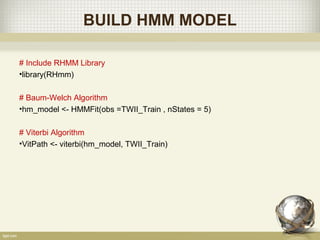

![SCIKIT LEARN

#Baum-Welch Algorithm

•n_components = 5

•model = GaussianHMM(n_components, "diag")

•model.fit([X], n_iter=1000)

# predict the optimal sequence of internal hidden state

•hidden_states = model.predict(X)](https://image.slidesharecdn.com/hmmandstock-130423115118-phpapp02/85/Hidden-Markov-Model-Stock-Prediction-19-320.jpg)

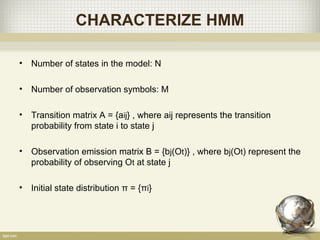

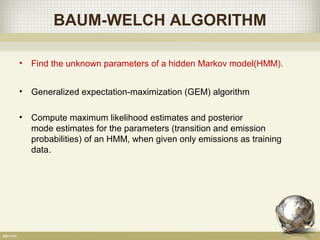

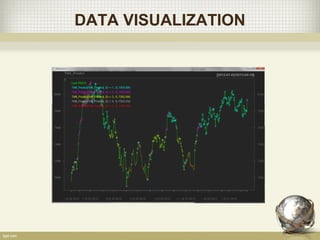

![PREDICTION

#State Prediction – using Scikit-learn

•data_vec = [diff[last_day], volume[last_day]]

•State = model.predict([data_vec])](https://image.slidesharecdn.com/hmmandstock-130423115118-phpapp02/85/Hidden-Markov-Model-Stock-Prediction-23-320.jpg)

This document discusses using hidden Markov models (HMM) for stock price prediction. HMMs can model time series data as a probabilistic finite state machine. The document explains that HMMs can handle new stock market data robustly and efficiently predict similar price patterns to past data. It provides an overview of HMM components like states, transition probabilities, and emission probabilities. The document also demonstrates building an HMM model on stock data using the RHMM package in R, including training the model with Baum-Welch and predicting state sequences with Viterbi.