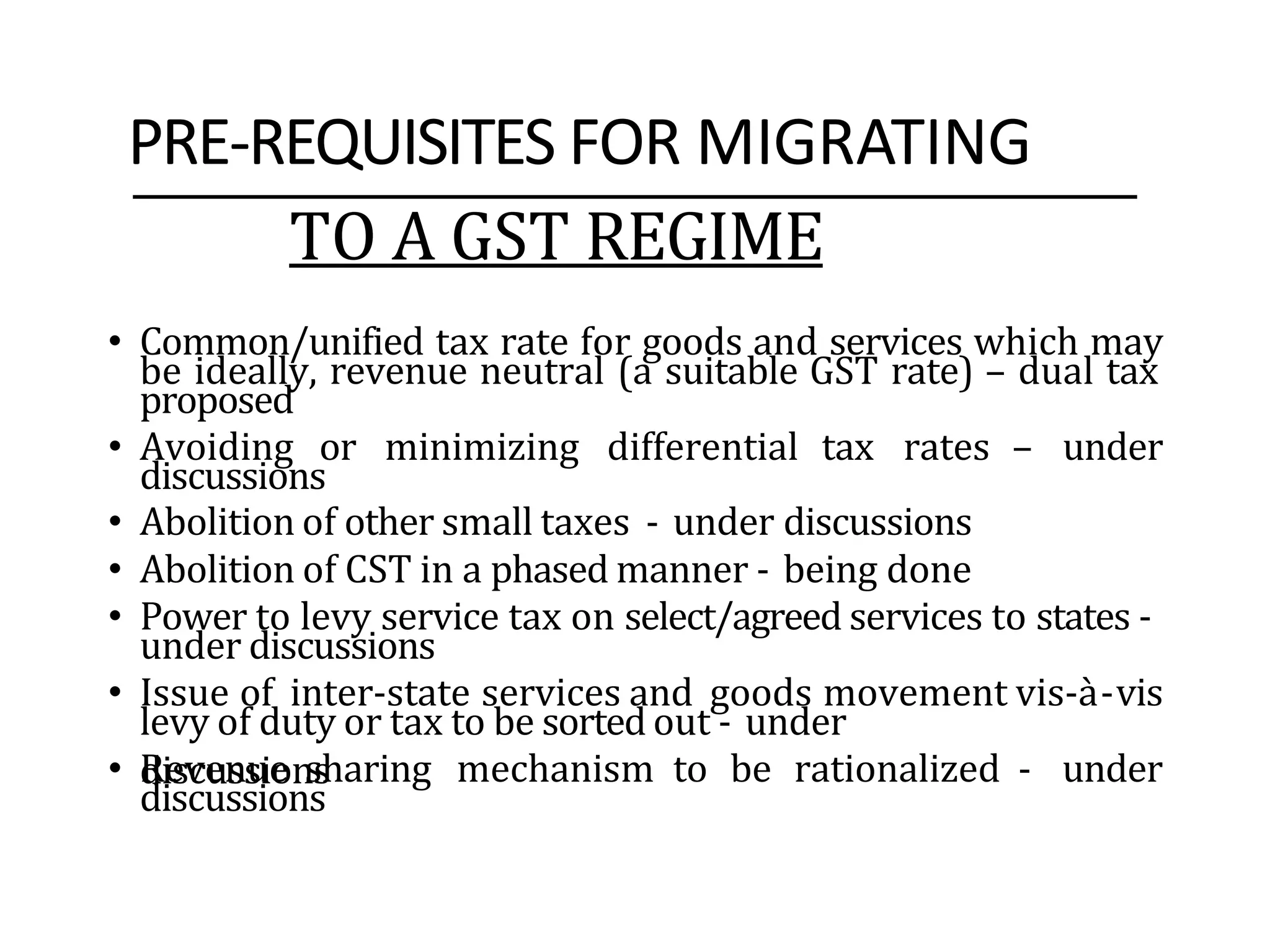

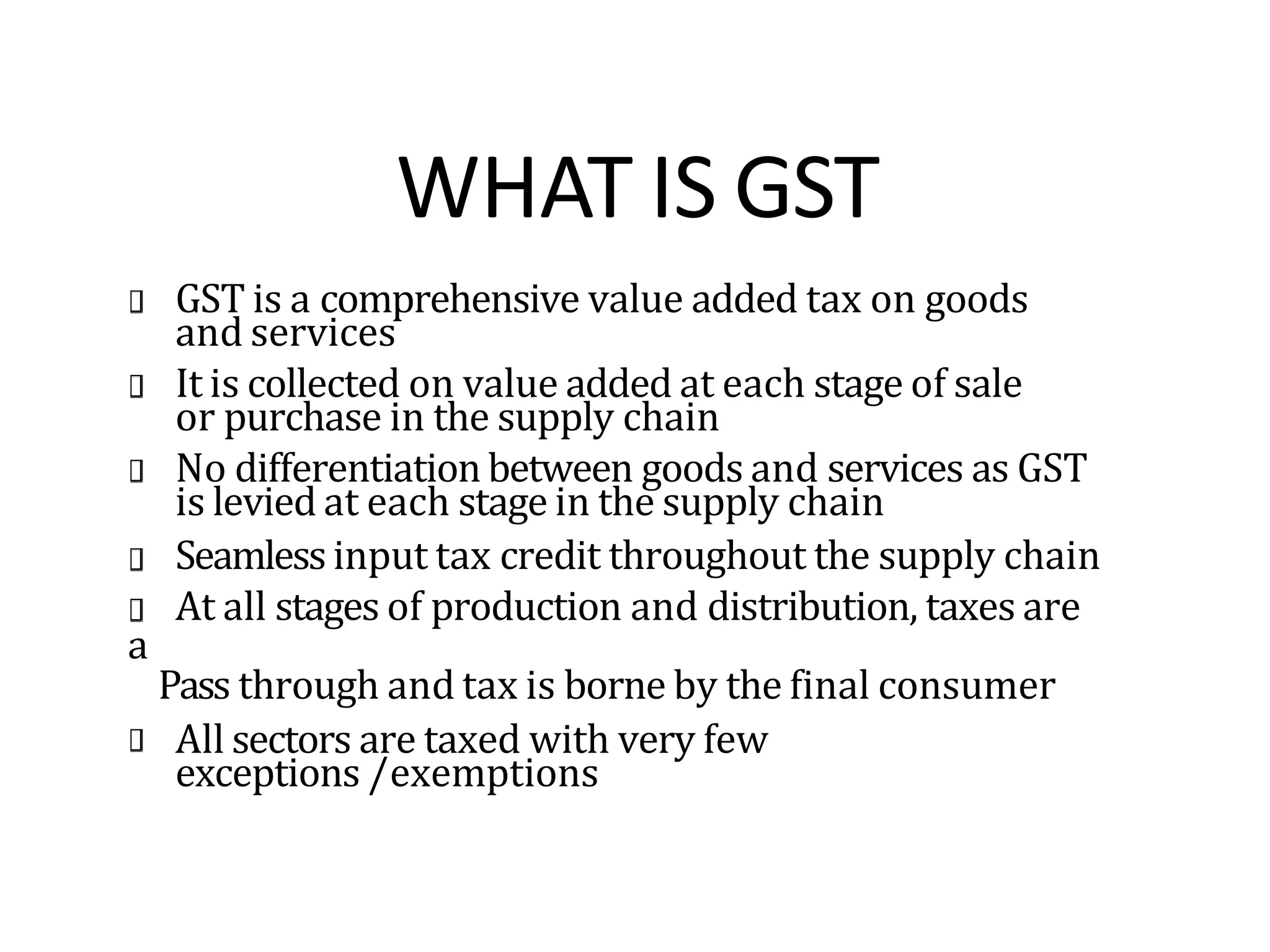

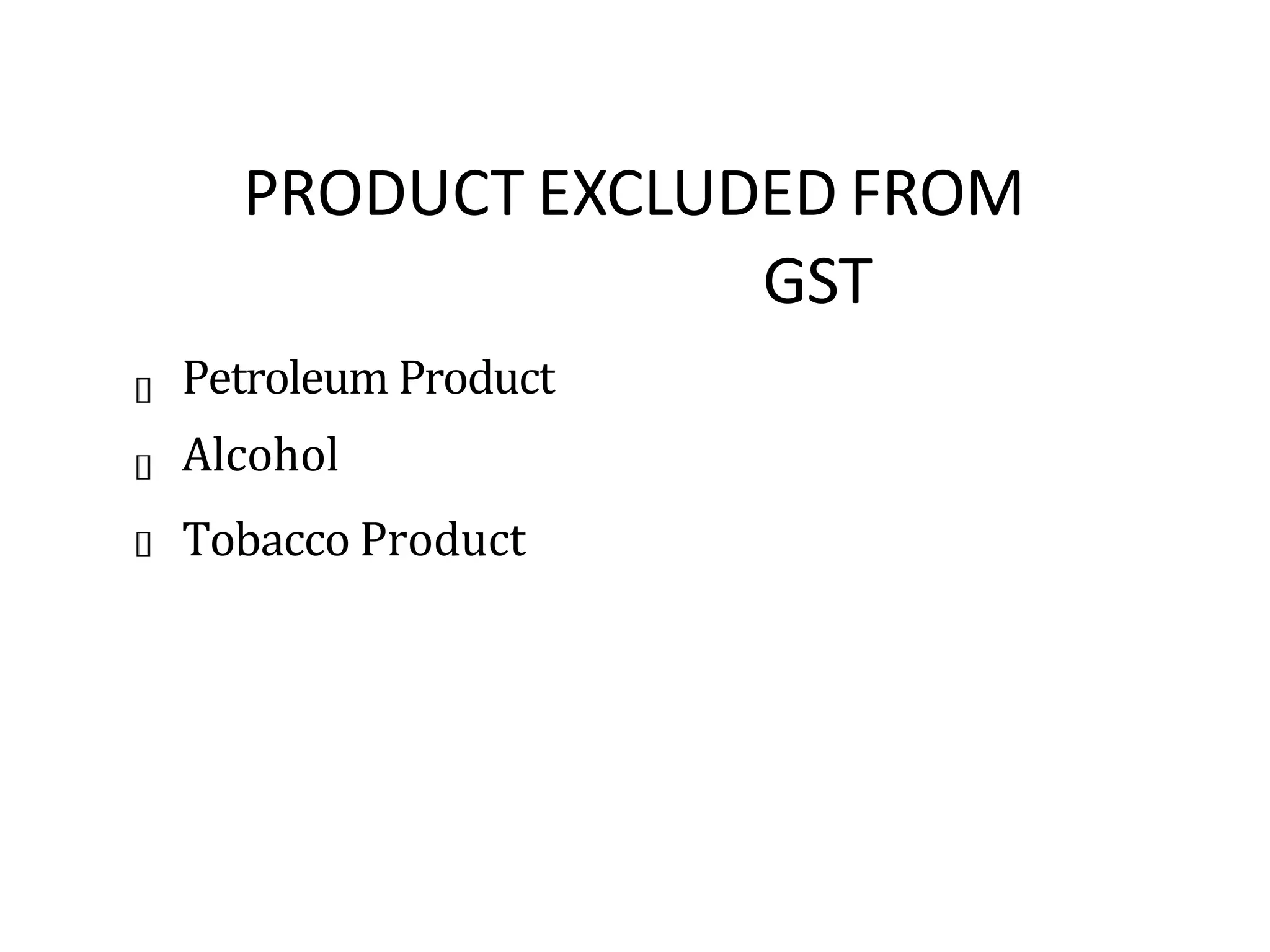

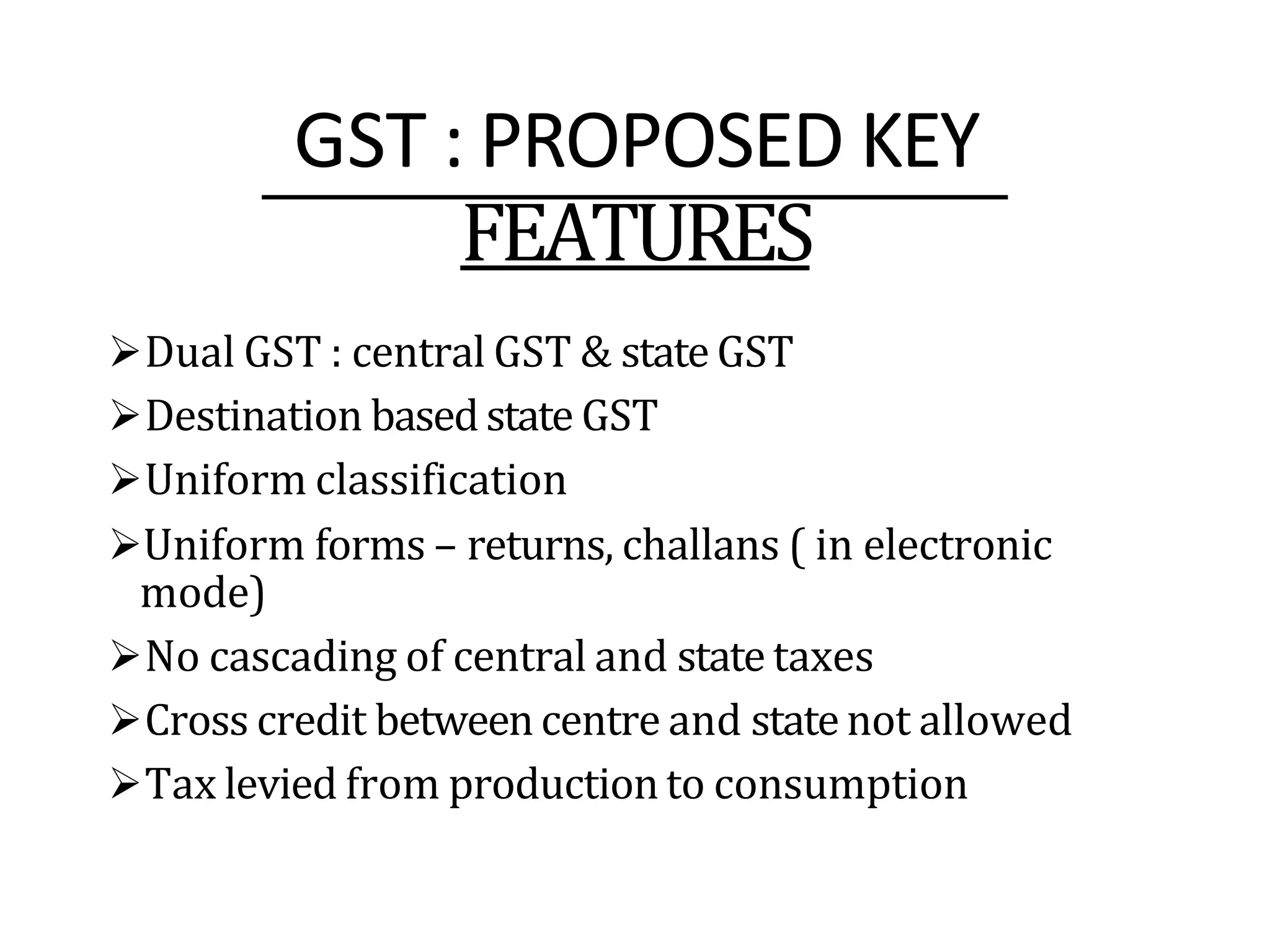

GST (Goods and Services Tax) is a comprehensive indirect tax that will combine multiple taxes and levies into a single tax to be applied at every stage of sale or purchase of goods and services. It aims to create a unified national market, reduce the cascading burden of taxes, and improve compliance. The tax is proposed to be dual, with the center and states concurrently levying it on a common tax base. There are still some issues being discussed such as the GST rate, tax sharing between states and center, and treatment of inter-state transactions.

![Power point presentation on gst[goods and service tax ]](https://cdn.slidesharecdn.com/ss_thumbnails/powerpointpresentationongst-200315095209-thumbnail.jpg?width=640&height=640&fit=bounds)