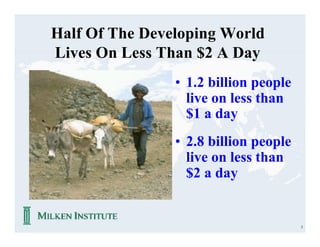

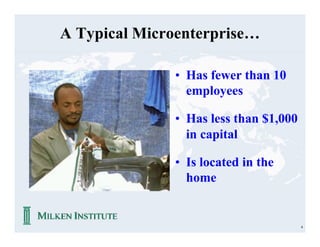

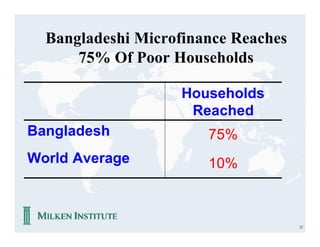

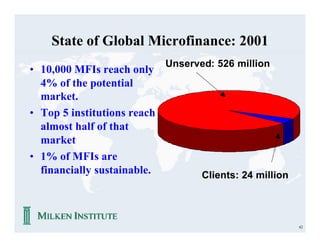

1) Over 2.8 billion people live on less than $2 a day and 1.2 billion on less than $1, with many supporting themselves through microenterprises consisting of less than 10 employees and $1,000 in capital.

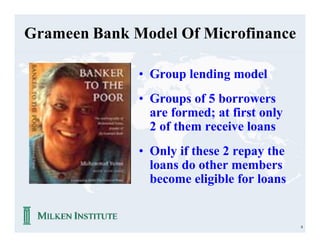

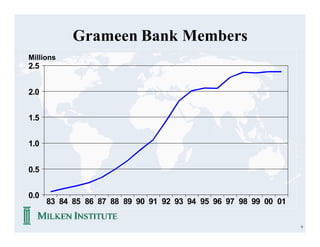

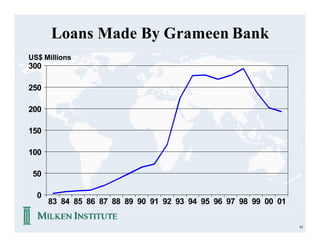

2) Microfinance provides small loans to the poor for self-employment and has grown to over 13 million borrowers and $7 billion in loans with repayment rates of 98% on average.

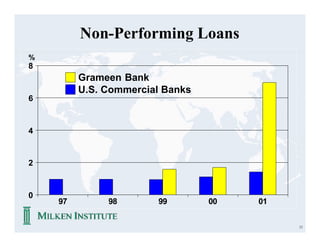

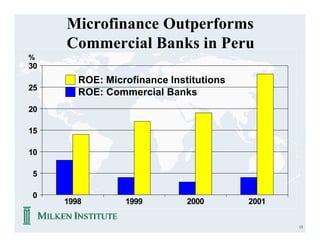

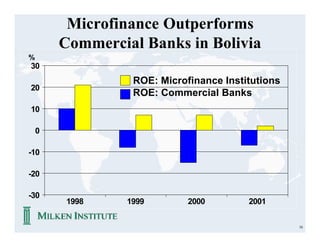

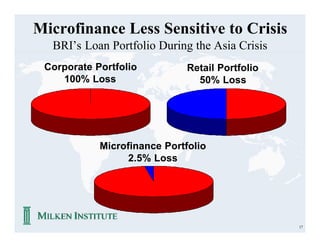

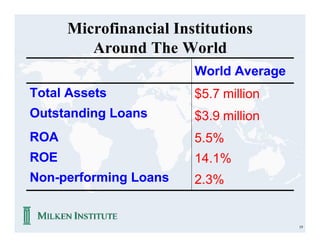

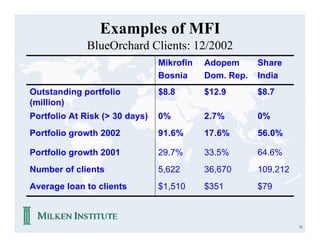

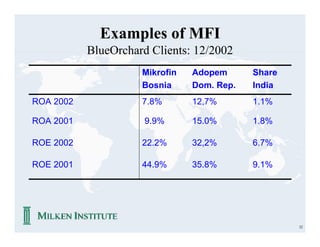

3) Microfinance institutions have higher returns than traditional banks in many countries, showing the potential of this sector to fight poverty through financial inclusion and support of microenterprises.