Downloaded 22 times

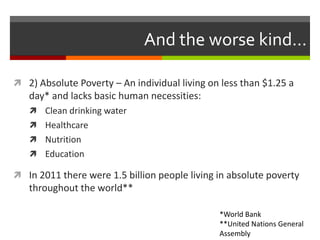

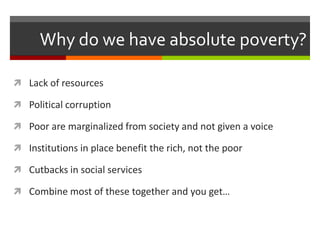

This document provides an overview of microfinancing and how it aims to help alleviate poverty. It discusses the two types of poverty, absolute and relative, and how absolute poverty affects over 1.5 billion people living on less than $1.25 per day. Microfinancing attempts to address this through small loans (microcredit) to help the poor establish small businesses or improve their economic circumstances. Key aspects covered include high repayment rates of microloans, the emphasis on female borrowers, and debates around the long-term effectiveness of microfinancing.