The document discusses concerns that led to the Fundamental Review of the Trading Book (FRTB). It summarizes that pre-FRTB there was unclear classification between banking and trading books allowing regulatory capital arbitrage. Risk measures also failed to fully capture risks like procyclicality, model risk for complex products, and comprehensive risks. The FRTB aims to address these issues with changes like standardized approaches, constraints on modeling, and convergence of prudential and accounting rules. It signals a strategic shift towards limiting internal modeling and preventing methodology arbitrage.

Outlook and market survey on the fresh Standards for Minimum capital requirements for market risk, published January 14th, 2016.

FRTB will deeply impact banks on IT, process, organization and human aspects.

CH&Co can help banks cope with these changes.

Overview of the Basel Committee's revised "Minimum capital requirements for market risk" (formerly FRTB), with notes and tips for technical implementation.

CH&CO - VaR methodology whitepaper - 2015 C Louiza

In the framework of knowledge promotion and expertise sharing, Chappuis Halder & Co. decided to give free access to the “Value-at-Risk Valuation tool” named in our paper “VaR spreadsheet estimator”. It contains the detail sheets simulations for the three main Value-at-Risk methods: Variance/covariance VaR, Historical VaR and Monte-Carlo VaR. The presented methodologies are not exhaustive and more exist and can be adapted depending on the process constraints.

This paper aims to have a theoretical approach of VaR and define all relevant steps to compute VaR according to the defined methodology. And to go further, it seems important to define VaR for a linear financial instrument. Thus, illustrations to monitor the VaR for an equity stock has been performed with a European call option VaR simulations for a better understanding of the concept and the tool. This article only focuses on VaR but will provide opportunities to open to more quantitative risk indicators as Stress-tests, Back-testing, Comprehensive risk measure (CRM), Expected Tail Loss (ETL) or Conditional VaR… more or less linked with the VaR methodologies…

everis Marcus Evans FRTB Conference 23Feb17Jonathan Philp

everis was Gold Sponsor of the Marcus Evans Conference ‘4th Edition: Impact of the Fundamental Review of the Trading Book’ at Canary Wharf, London on 23-24th February 2017.

This was a timely opportunity to catch up with banks and solution partners as we move into the implementation phase of Fundamental Review of the Trading Book (FRTB) programmes. We heard views and case studies across a range of topics including market risk methodology, operating model definition and data and systems architecture design.

Our presentation at the conference focused on the architectural challenges posed by FRTB.

Outlook and market survey on the fresh Standards for Minimum capital requirements for market risk, published January 14th, 2016.

FRTB will deeply impact banks on IT, process, organization and human aspects.

CH&Co can help banks cope with these changes.

Overview of the Basel Committee's revised "Minimum capital requirements for market risk" (formerly FRTB), with notes and tips for technical implementation.

CH&CO - VaR methodology whitepaper - 2015 C Louiza

In the framework of knowledge promotion and expertise sharing, Chappuis Halder & Co. decided to give free access to the “Value-at-Risk Valuation tool” named in our paper “VaR spreadsheet estimator”. It contains the detail sheets simulations for the three main Value-at-Risk methods: Variance/covariance VaR, Historical VaR and Monte-Carlo VaR. The presented methodologies are not exhaustive and more exist and can be adapted depending on the process constraints.

This paper aims to have a theoretical approach of VaR and define all relevant steps to compute VaR according to the defined methodology. And to go further, it seems important to define VaR for a linear financial instrument. Thus, illustrations to monitor the VaR for an equity stock has been performed with a European call option VaR simulations for a better understanding of the concept and the tool. This article only focuses on VaR but will provide opportunities to open to more quantitative risk indicators as Stress-tests, Back-testing, Comprehensive risk measure (CRM), Expected Tail Loss (ETL) or Conditional VaR… more or less linked with the VaR methodologies…

everis Marcus Evans FRTB Conference 23Feb17Jonathan Philp

everis was Gold Sponsor of the Marcus Evans Conference ‘4th Edition: Impact of the Fundamental Review of the Trading Book’ at Canary Wharf, London on 23-24th February 2017.

This was a timely opportunity to catch up with banks and solution partners as we move into the implementation phase of Fundamental Review of the Trading Book (FRTB) programmes. We heard views and case studies across a range of topics including market risk methodology, operating model definition and data and systems architecture design.

Our presentation at the conference focused on the architectural challenges posed by FRTB.

Because the VaR starts to be « old fashioned » and not so "Normal" :-), CH&Co. and its GRA team wanted to pay a last tribute to this world famous Market Risk Method.

This paper comes along with a Excel Tool

With our experience and our experts, Chappuis Halder & Co would provide appropriate incentives at every level of your organization. It could help you at the time to manage “modern” risk alongside performance

Solving the FRTB Challenge: Why You Should Consider an Aggregation SolutionFIS

Many banks face multiple challenges around market risk, with outdated infrastructure, fragmented systems, and inflexible reporting tools. And now FRTB raises the stakes. The Fundamental Review of the Trading Book is the biggest change in market risk rules that we’ve seen in a generation.

The answer to the FRTB challenge is a centralized aggregation solution that allows you to source required prices from one or more front-office and risk engines, perform bank-wide FRTB calculations using those inputs, and combine the results with intermediate data and expose inputs via reporting and analysis tools.

View our slideshow to learn more about aggregation challenges and why you should consider an external solution.

Challenges in Practical Market Risk Management - a presentation by Anshuman Prasad, Director, Risk and Analytics at CRISIL GR&A made at the 15th Annual GARP Risk Management Convention, New York.

Operational Risk Loss Forecasting Model for Stress TestingCRISIL Limited

Presentation on ‘Operational Risk Loss Forecasting Model for Stress Testing – A Three-Stage Approach’ made by Dr. James Lu, Director, Risk & Analytics, CRISIL Global Research & Analytics (GR&A) at The 17th Annual OpRisk North America 2015, New York

everis was Gold Sponsor of the Marcus Evans Conference ‘4th Edition: Impact of the Fundamental Review of the Trading Book’ at Canary Wharf, London on 23-24th February 2017.

This was a timely opportunity to catch up with banks and solution partners as we move into the implementation phase of Fundamental Review of the Trading Book (FRTB) programmes. We heard views and case studies across a range of topics including market risk methodology, operating model definition and data and systems architecture design.

Our presentation at the conference focused on the architectural challenges posed by FRTB.

Outlook and market survey on the fresh Standards for Minimum capital requirements for market risk (FRTB), published January 14th, 2016.

FRTB will deeply impact banks on IT, process, human and organizational aspects.

CH&Co can assist banks navigate through these fundamental changes

BCBS 239 Compliance: A Comprehensive ApproachCognizant

In 2013, the Basel Committee on Banking Supervision (BCBS) issued 14 principles for effectively aggregating risk data and reporting, with the goal of enabling banks to understand and address risk exposures that influence their major decisions. While Global Systemically Important Banks (GSIBs) have made progress in complying with BCBS 239, Domestic Systemically Important Banks (DSIBs) are still in the early stages.

Because the VaR starts to be « old fashioned » and not so "Normal" :-), CH&Co. and its GRA team wanted to pay a last tribute to this world famous Market Risk Method.

This paper comes along with a Excel Tool

With our experience and our experts, Chappuis Halder & Co would provide appropriate incentives at every level of your organization. It could help you at the time to manage “modern” risk alongside performance

Solving the FRTB Challenge: Why You Should Consider an Aggregation SolutionFIS

Many banks face multiple challenges around market risk, with outdated infrastructure, fragmented systems, and inflexible reporting tools. And now FRTB raises the stakes. The Fundamental Review of the Trading Book is the biggest change in market risk rules that we’ve seen in a generation.

The answer to the FRTB challenge is a centralized aggregation solution that allows you to source required prices from one or more front-office and risk engines, perform bank-wide FRTB calculations using those inputs, and combine the results with intermediate data and expose inputs via reporting and analysis tools.

View our slideshow to learn more about aggregation challenges and why you should consider an external solution.

Challenges in Practical Market Risk Management - a presentation by Anshuman Prasad, Director, Risk and Analytics at CRISIL GR&A made at the 15th Annual GARP Risk Management Convention, New York.

Operational Risk Loss Forecasting Model for Stress TestingCRISIL Limited

Presentation on ‘Operational Risk Loss Forecasting Model for Stress Testing – A Three-Stage Approach’ made by Dr. James Lu, Director, Risk & Analytics, CRISIL Global Research & Analytics (GR&A) at The 17th Annual OpRisk North America 2015, New York

everis was Gold Sponsor of the Marcus Evans Conference ‘4th Edition: Impact of the Fundamental Review of the Trading Book’ at Canary Wharf, London on 23-24th February 2017.

This was a timely opportunity to catch up with banks and solution partners as we move into the implementation phase of Fundamental Review of the Trading Book (FRTB) programmes. We heard views and case studies across a range of topics including market risk methodology, operating model definition and data and systems architecture design.

Our presentation at the conference focused on the architectural challenges posed by FRTB.

Outlook and market survey on the fresh Standards for Minimum capital requirements for market risk (FRTB), published January 14th, 2016.

FRTB will deeply impact banks on IT, process, human and organizational aspects.

CH&Co can assist banks navigate through these fundamental changes

BCBS 239 Compliance: A Comprehensive ApproachCognizant

In 2013, the Basel Committee on Banking Supervision (BCBS) issued 14 principles for effectively aggregating risk data and reporting, with the goal of enabling banks to understand and address risk exposures that influence their major decisions. While Global Systemically Important Banks (GSIBs) have made progress in complying with BCBS 239, Domestic Systemically Important Banks (DSIBs) are still in the early stages.

The European Banking Authority (EBA) launched a consultation on its draft Regulatory Technical Standards on assessment methodology for internal ratings-based approach. These draft RTS are a key component of the EBA's work to ensure consistency in models outputs and comparability of risk-weighted exposures and will contribute to harmonize the supervisory assessment methodology across all EU Member States. The consultation runs until 12 March 2015.

In this Quarterly release Joseph Hill shares his thoughts on relationship lending, community bank CRE growth, and the competitive edge of truly understanding a Borrower’s business. We then would like to introduce Mr. Dean Morgan as CEIS’ Regional Executive for Tennessee and the nearby Southern States, and lastly, leave with an excellent article on tackling Risk Management of a Commercial Real Estate Concentration.

In March 2016, the BCBS published a consultation regulatory document setting a new set of regulatory measures in order to reduce the heterogeneity of banks’ capital charge using IRB models. This document goes through these proposals and provides opposing views regarding these proposals from different academic references.

Only one year after its creation, the GRA team has been completely transformed. Surpassing all of the original ambitions, the team now stretches over three zones (Europe, Asia and the US) and continues to grow.

Our philosophy is distinctly influenced by the gratification of working together on subject matter which daily fascinates and inspires us. It also conveys the richness of our exchanges, as we collaborate with several practitioners and enthusiasts.

This document has no other purpose than to bring some responsive elements to the questions we face constantly, reminding us also to practice patience and humility - for many answers are possible, and the path of discovery stretches out long before us...”

Interest rate risk management what regulators want in 2015 7.15.2015Craig Taggart MBA

Areas covered in this section

Why Interest Rate Risk (IRR) should not be ignored

• Forward Rate Agreements (FRA’s) Forwards, Futures

• Swaps, Options

Why Bank Regulators continue to have a poor handle on interest rate risk

• Interest Rate Caps, floors, Collars

• LIBOR and UBS & Barclays rigging rates

• How should Financial Institutions determine which IRR vendor models are appropriate?

IRR Measurement methodologies are institutions

EBA definition of Default intended to harmonize the default flag across the EU. All the financial institutions under the scope of CRR will have to implement the new definition of default.

IFRS (International Financial Reporting Standards) 9 is not just an accounting standard, but a game-changer. In today’s capital constrained environment, the increased volatility of P&L and that of associated regulatory capital are likely to have a profound impact across the stakeholder community. This presentation provides an overview of our assistance themes. If you are project sponsor or a stakeholder, please feel free to organize a call with us to discuss how Nexx can assist you.

USDA Loans in California: A Comprehensive Overview.pptxmarketing367770

USDA Loans in California: A Comprehensive Overview

If you're dreaming of owning a home in California's rural or suburban areas, a USDA loan might be the perfect solution. The U.S. Department of Agriculture (USDA) offers these loans to help low-to-moderate-income individuals and families achieve homeownership.

Key Features of USDA Loans:

Zero Down Payment: USDA loans require no down payment, making homeownership more accessible.

Competitive Interest Rates: These loans often come with lower interest rates compared to conventional loans.

Flexible Credit Requirements: USDA loans have more lenient credit score requirements, helping those with less-than-perfect credit.

Guaranteed Loan Program: The USDA guarantees a portion of the loan, reducing risk for lenders and expanding borrowing options.

Eligibility Criteria:

Location: The property must be located in a USDA-designated rural or suburban area. Many areas in California qualify.

Income Limits: Applicants must meet income guidelines, which vary by region and household size.

Primary Residence: The home must be used as the borrower's primary residence.

Application Process:

Find a USDA-Approved Lender: Not all lenders offer USDA loans, so it's essential to choose one approved by the USDA.

Pre-Qualification: Determine your eligibility and the amount you can borrow.

Property Search: Look for properties in eligible rural or suburban areas.

Loan Application: Submit your application, including financial and personal information.

Processing and Approval: The lender and USDA will review your application. If approved, you can proceed to closing.

USDA loans are an excellent option for those looking to buy a home in California's rural and suburban areas. With no down payment and flexible requirements, these loans make homeownership more attainable for many families. Explore your eligibility today and take the first step toward owning your dream home.

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

where can I find a legit pi merchant onlineDOT TECH

Yes. This is very easy what you need is a recommendation from someone who has successfully traded pi coins before with a merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi network coins and resell them to Investors looking forward to hold thousands of pi coins before the open mainnet.

I will leave the telegram contact of my personal pi merchant to trade with

@Pi_vendor_247

If you are looking for a pi coin investor. Then look no further because I have the right one he is a pi vendor (he buy and resell to whales in China). I met him on a crypto conference and ever since I and my friends have sold more than 10k pi coins to him And he bought all and still want more. I will drop his telegram handle below just send him a message.

@Pi_vendor_247

What website can I sell pi coins securely.DOT TECH

Currently there are no website or exchange that allow buying or selling of pi coins..

But you can still easily sell pi coins, by reselling it to exchanges/crypto whales interested in holding thousands of pi coins before the mainnet launch.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and resell to these crypto whales and holders of pi..

This is because pi network is not doing any pre-sale. The only way exchanges can get pi is by buying from miners and pi merchants stands in between the miners and the exchanges.

How can I sell my pi coins?

Selling pi coins is really easy, but first you need to migrate to mainnet wallet before you can do that. I will leave the telegram contact of my personal pi merchant to trade with.

Tele-gram.

@Pi_vendor_247

Currently pi network is not tradable on binance or any other exchange because we are still in the enclosed mainnet.

Right now the only way to sell pi coins is by trading with a verified merchant.

What is a pi merchant?

A pi merchant is someone verified by pi network team and allowed to barter pi coins for goods and services.

Since pi network is not doing any pre-sale The only way exchanges like binance/huobi or crypto whales can get pi is by buying from miners. And a merchant stands in between the exchanges and the miners.

I will leave the telegram contact of my personal pi merchant. I and my friends has traded more than 6000pi coins successfully

Tele-gram

@Pi_vendor_247

how can i use my minded pi coins I need some funds.DOT TECH

If you are interested in selling your pi coins, i have a verified pi merchant, who buys pi coins and resell them to exchanges looking forward to hold till mainnet launch.

Because the core team has announced that pi network will not be doing any pre-sale. The only way exchanges like huobi, bitmart and hotbit can get pi is by buying from miners.

Now a merchant stands in between these exchanges and the miners. As a link to make transactions smooth. Because right now in the enclosed mainnet you can't sell pi coins your self. You need the help of a merchant,

i will leave the telegram contact of my personal pi merchant below. 👇 I and my friends has traded more than 3000pi coins with him successfully.

@Pi_vendor_247

how to sell pi coins at high rate quickly.DOT TECH

Where can I sell my pi coins at a high rate.

Pi is not launched yet on any exchange. But one can easily sell his or her pi coins to investors who want to hold pi till mainnet launch.

This means crypto whales want to hold pi. And you can get a good rate for selling pi to them. I will leave the telegram contact of my personal pi vendor below.

A vendor is someone who buys from a miner and resell it to a holder or crypto whale.

Here is the telegram contact of my vendor:

@Pi_vendor_247

The European Unemployment Puzzle: implications from population agingGRAPE

We study the link between the evolving age structure of the working population and unemployment. We build a large new Keynesian OLG model with a realistic age structure, labor market frictions, sticky prices, and aggregate shocks. Once calibrated to the European economy, we quantify the extent to which demographic changes over the last three decades have contributed to the decline of the unemployment rate. Our findings yield important implications for the future evolution of unemployment given the anticipated further aging of the working population in Europe. We also quantify the implications for optimal monetary policy: lowering inflation volatility becomes less costly in terms of GDP and unemployment volatility, which hints that optimal monetary policy may be more hawkish in an aging society. Finally, our results also propose a partial reversal of the European-US unemployment puzzle due to the fact that the share of young workers is expected to remain robust in the US.

The European Unemployment Puzzle: implications from population aging

CH&Cie - Fundamental Review of the Trading Book

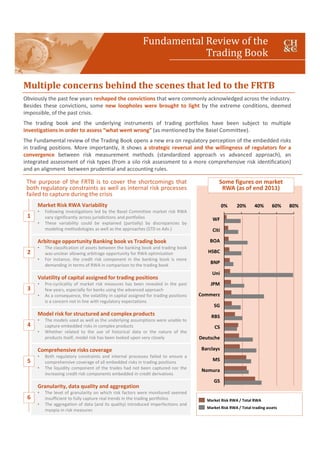

1. Arbitrage opportunity Banking book vs Trading book

• The classification of assets between the banking book and trading book

was unclear allowing arbitrage opportunity for RWA optimization

• For instance, the credit risk component in the banking book is more

demanding in terms of RWA in comparison to the trading book

Volatility of capital assigned for trading positions

• Pro-cyclicality of market risk measures has been revealed in the past

few years, especially for banks using the advanced approach

• As a consequence, the volatility in capital assigned for trading positions

is a concern not in line with regulatory expectations

Model risk for structured and complex products

• The models used as well as the underlying assumptions were unable to

capture embedded risks in complex products

• Whether related to the use of historical data or the nature of the

products itself, model risk has been looked upon very closely

Comprehensive risks coverage

• Both regulatory constraints and internal processes failed to ensure a

comprehensive coverage of all embedded risks in trading positions

• The liquidity component of the trades had not been captured nor the

increasing credit risk components embedded in credit derivatives

Granularity, data quality and aggregation

• The level of granularity on which risk factors were monitored seemed

insufficient to fully capture real trends in the trading portfolios

• The aggregation of data (and its quality) introduced imperfections and

myopia in risk measures

Market Risk RWA Variability

• Following investigations led by the Basel Committee market risk RWA

vary significantly across jurisdictions and portfolios

• These variability could be explained (partially) by discrepancies by

modeling methodologies as well as the approaches (STD vs Adv.)

Multiple concerns behind the scenes that led to the FRTB

Obviously the past few years reshaped the convictions that were commonly acknowledged across the industry.

Besides these convictions, some new loopholes were brought to light by the extreme conditions, deemed

impossible, of the past crisis.

The trading book and the underlying instruments of trading portfolios have been subject to multiple

investigations in order to assess “what went wrong” (as mentioned by the Basel Committee).

The Fundamental review of the Trading Book opens a new era on regulatory perception of the embedded risks

in trading positions. More importantly, it shows a strategic reversal and the willingness of regulators for a

convergence between risk measurement methods (standardized approach vs advanced approach), an

integrated assessment of risk types (from a silo risk assessment to a more comprehensive risk identification)

and an alignment between prudential and accounting rules.

Fundamental Review of the

Trading Book

The purpose of the FRTB is to cover the shortcomings that

both regulatory constraints as well as internal risk processes

failed to capture during the crisis

Market Risk RWA / Total RWA

Market Risk RWA / Total trading assets

1

2

3

4

5

6

40%20%

GS

0%

MS

Nomura

CS

Deutsche

Barclays

RBS

60% 80%

JPM

Commerz

SG

Uni

BNP

HSBC

BOA

Citi

WF

Some figures on market

RWA (as of end 2011)

2. These concerns are to be addressed by a redesign of the

trading portfolios and the risk measures…

The Fundamental Review of the Trading Book presents extensive reshape of the treatment of market

risk. Its redesign is multi-dimensional and ranges from operational implementation, to measurement

and methodologies, to documentation and clarifications…

Trading

book vs

banking

book

• Boundary and classification | The FRTB provides a clarification

on instruments classification and assignment between the banking and

the trading book. Besides providing a pre-defined list of instruments to

be assigned, institutions should provide operational criteria on the

intent of the instrument

Description Impact

• Rigidity of the classification:

once assigned the

reclassification is limited

• Operational constraints to

justify the classification

• Alignment between the books| The FRTB shows a clear

intention of a convergence between the treatment of the two books in

both directions. The treatment of default risk in the trading book is to

get closer to the banking book whereas interest rate risk in the banking

is to be measured in Pillar I (on-going) using a fair value measurement

of the balance sheet

• The intention is to

segregate the two books

while homogenizing the

treatment of risks

Risk

measurem

ent

• Standardized approach| Introduces a higher level of granularity

and bucket differentiation. Each bucket is assigned to a specific

formula. The diversification and hedging positions are better captured

via a revised correlation factor. Design of a method to better capture

various risks (interest rate, FX, equity, …). To be used as a floor

• Higher complexity that the

initial method

• However, it enhances the

transparency in measuring

risks at more granular levels

• Advanced approach| Using internal methods will be definied on a

more granular level via a P&L attribution method,etc… Risk

measurement is consequently done desk by desk. The methodology

relies on the Expected Shortfall (to replace the VaR) with a 97.5%

confidence level (vs 99% for the VaR). Calibration of risks in stress

conditions.

• Complexity in comparing

results related to the

attribution of methods by

desk. Some are eligible

other not eligible

• ES models can be complex

(use of EVT,…)

Framing

and

constraints

• Framing | Securitization positions are no more eligible to the

advanced approach. The Basel Committee imposes the use of the

standardized approach for all securitized positions

• Higher transparency at the

cost of higher RWA

• Constraints | Constraints are provided by the FRTB. A methodology

will be provided for choosing the stressed period. Correlation

parameters in the IDR charge might be constrained as well whereas

the horizons for VaR calculation ( 10 ൈ 1 െ ݀ܽ ܴܸܽ ݕ vs 10 െ

݀ܽ) ܴܸܽ ݕ are subject to similar types of guidance and constraints

• Higher impact on RWA

• Limits arbitrage related to

methodology and methods

This reveals a new tendency in regulatory requirements and the reversal in terms of limiting the ability

for banks in using internal approaches as well as framing methodology arbitrage

• Will this tendency be generalized

because of some discrepancies

that still exist between these

regulations ?

• Under this framework, what is

the relevance of using advanced

approaches?

• Are regulators pushing

(indirectly) for the use of the STD

approach?

• What about overlaps between

the various regulations?

• Are we heading for an over-

coverage of risks?

Convergence between

prudential and accounting rules

Integrated risk assessment

framework

Convergence between the

Standardized and the advanced

approach

Fundamental Review of the

Trading Book

3. Our expertise in the field can help you in various ways

CH&Co dedicated team is constituted of a balanced team of experts in Risk Modeling as well as

regulatory and accounting interpretation. The ability to both interpret the regulation (via benchmarks

and lobbying among the industry participants) and dispatch resources that can assist in quantifying

risks, allows to achieve quick results while being in line and compliant with regulatory requirements.

Our team can deliver the following:

1

2

3

4

5

6

Regulatory Watch & Interpretation

CH&Co has invested in dedicated to both follow-up on regulations and

their evolutions as well as to interpret them and provide our clients

with clear guidelines designed for in-house purposes to measure the

impact on banks’ organization, models, processes and businesses

Model Design

CH&Co Global Research & Analytics (GRA) team is constituted of

dedicated experts in risk modeling and quantification. They can support

in-house teams by both providing a higher workforce as well as

feedback on market best practices

Model Validation

We can assist as well on model validation. Our 15-year expertise in the

field allows providing our clients with added-value in terms of

regulators expectations on tests to be performed, standards to be

achieved and documentation to be put in place

Benchmark

CH&Co contributes to discussions across the industry around regulatory

evolutions and their impact on banks’ business models. CH&Co is also

active in responding to QIS as well as EBA discussions papers (for

instance “Future of the IRB Approach). Plus, CH&Co can deliver

benchmarks on the market best practices

Optimization

CH&Co has led multiple assignments and discussions on optimizing

RWAs in an environment with high pressure on ROEs and capital. The

areas for optimization are important but can’t be achieved without

difficulty. Therefore, managing risks in an integrated way (vs silo) is key

Support in strategic decisions

Multiple institutions are adapting their strategies to the evolutions in

regulations and the financial sector. CH&Co can provide decision-

making solutions by simulating impacts, projecting strategic and

business related items and facilitate communication with Senior

Management

CH&Co is also

active in publishing

articles and White

Papers. Our teams

try to answer

questions among

market participants

as well as work on

Research to

continually

enhance risk

measurement

methodologies.

Check out our

publications and

white papers on

our website:

http://www.chapp

uishalder.com/publ

ications/

Stéphane Eyraud, Partner & CEO

Tel UK: + 44 78 34 55 03 98

Tel FR: + 33 6 12 41 64 06

seyraud@chappuishalder.com

Benoit Genest, Partner & head of GRA

Tel FR: + 33 7 87 68 81 77

bgenest@chappuishalder.com

Ziad Fares, Manager GRA, R&D

Tel FR: + 33 6 62 96 25 00

zfares@chappuishalder.com

Fundamental Review of the

Trading Book