Downloaded 14 times

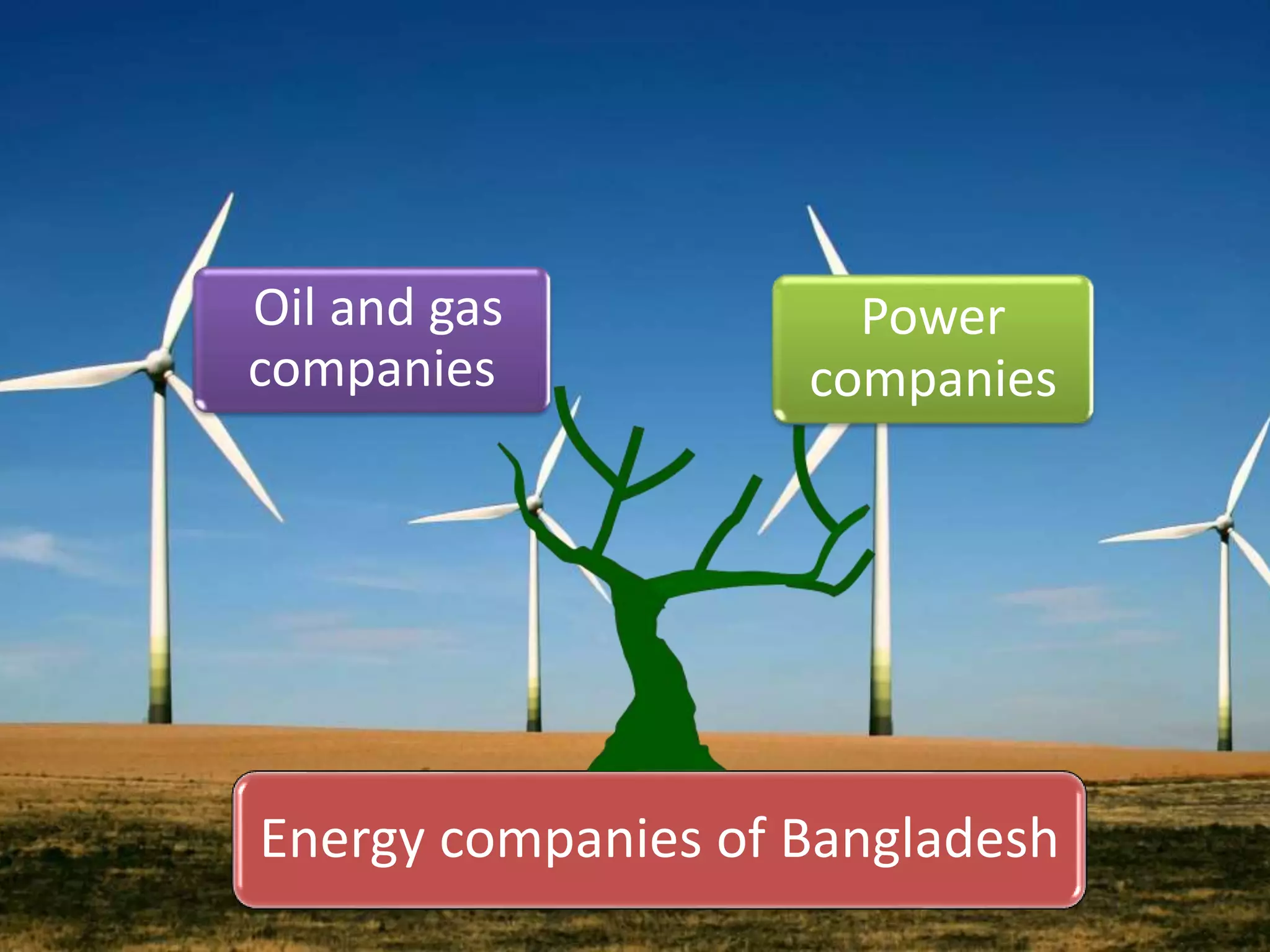

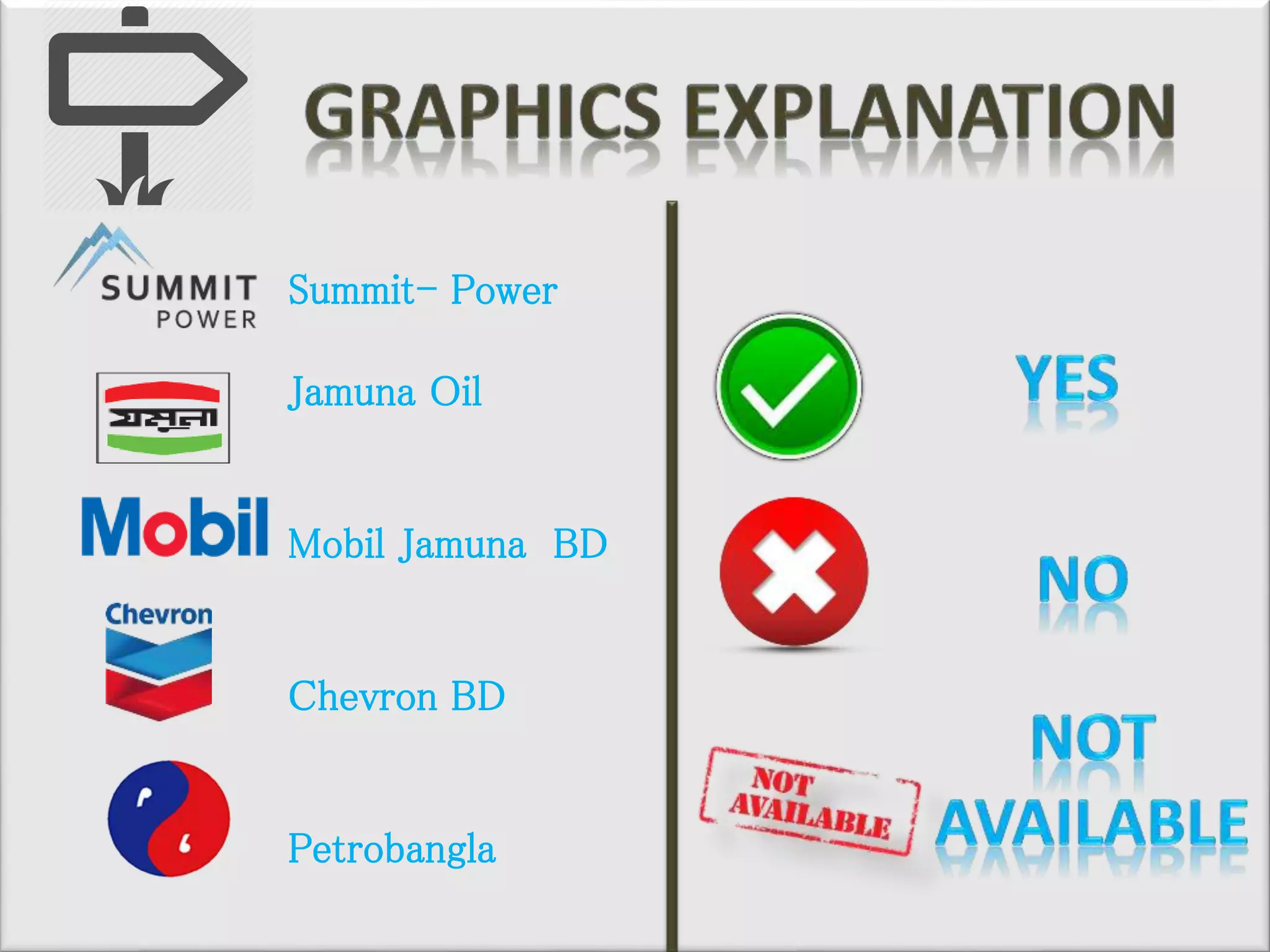

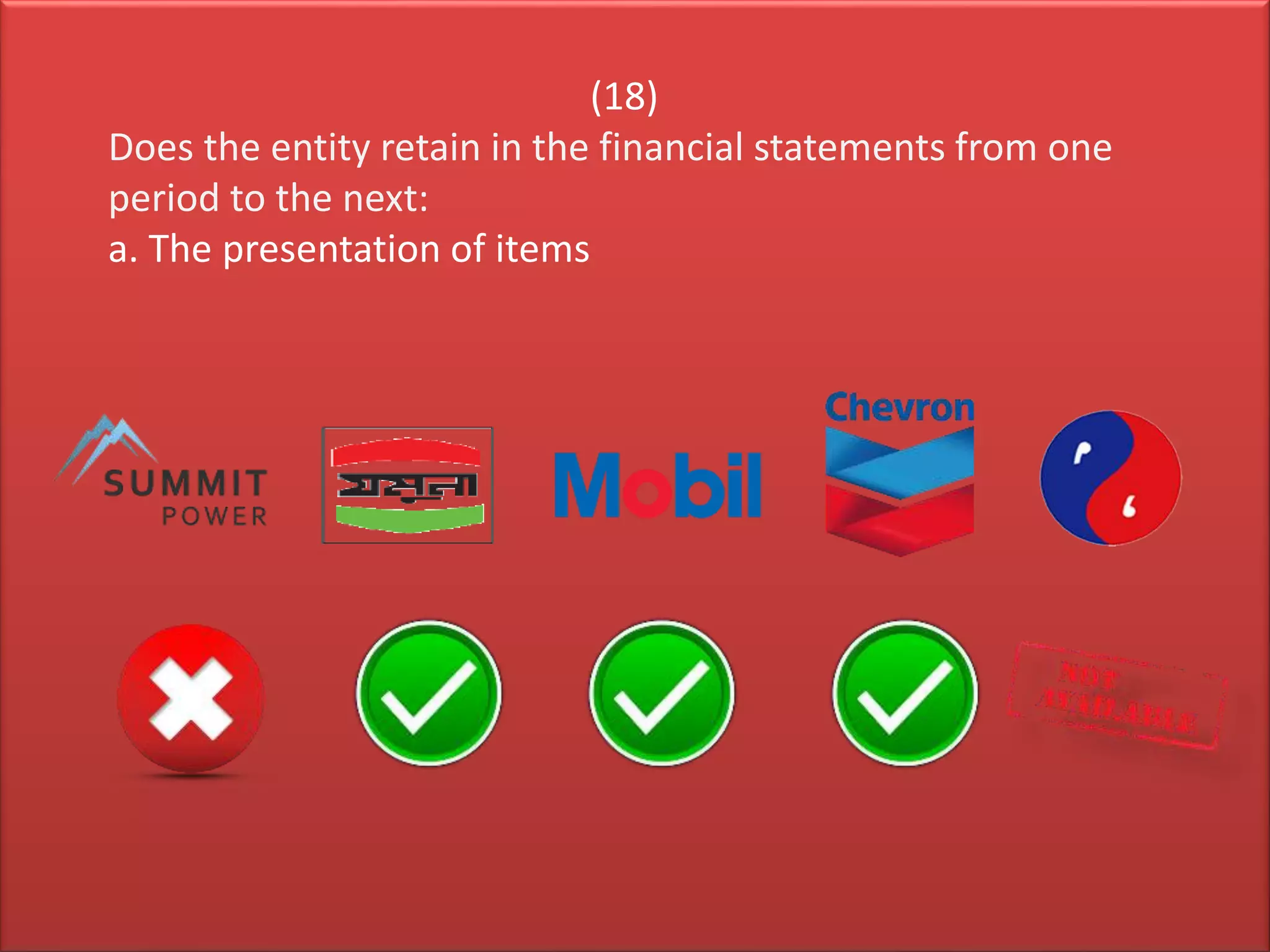

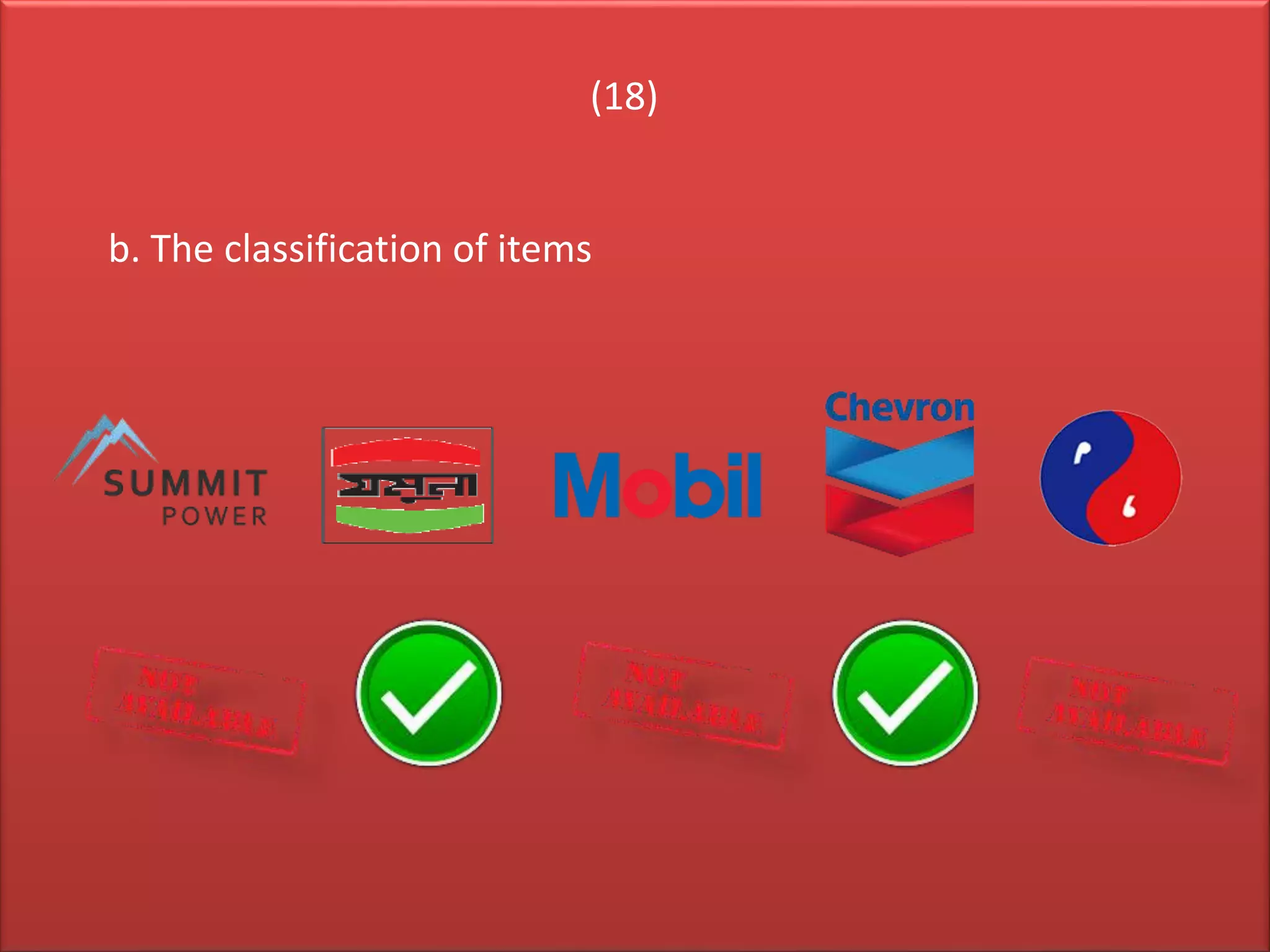

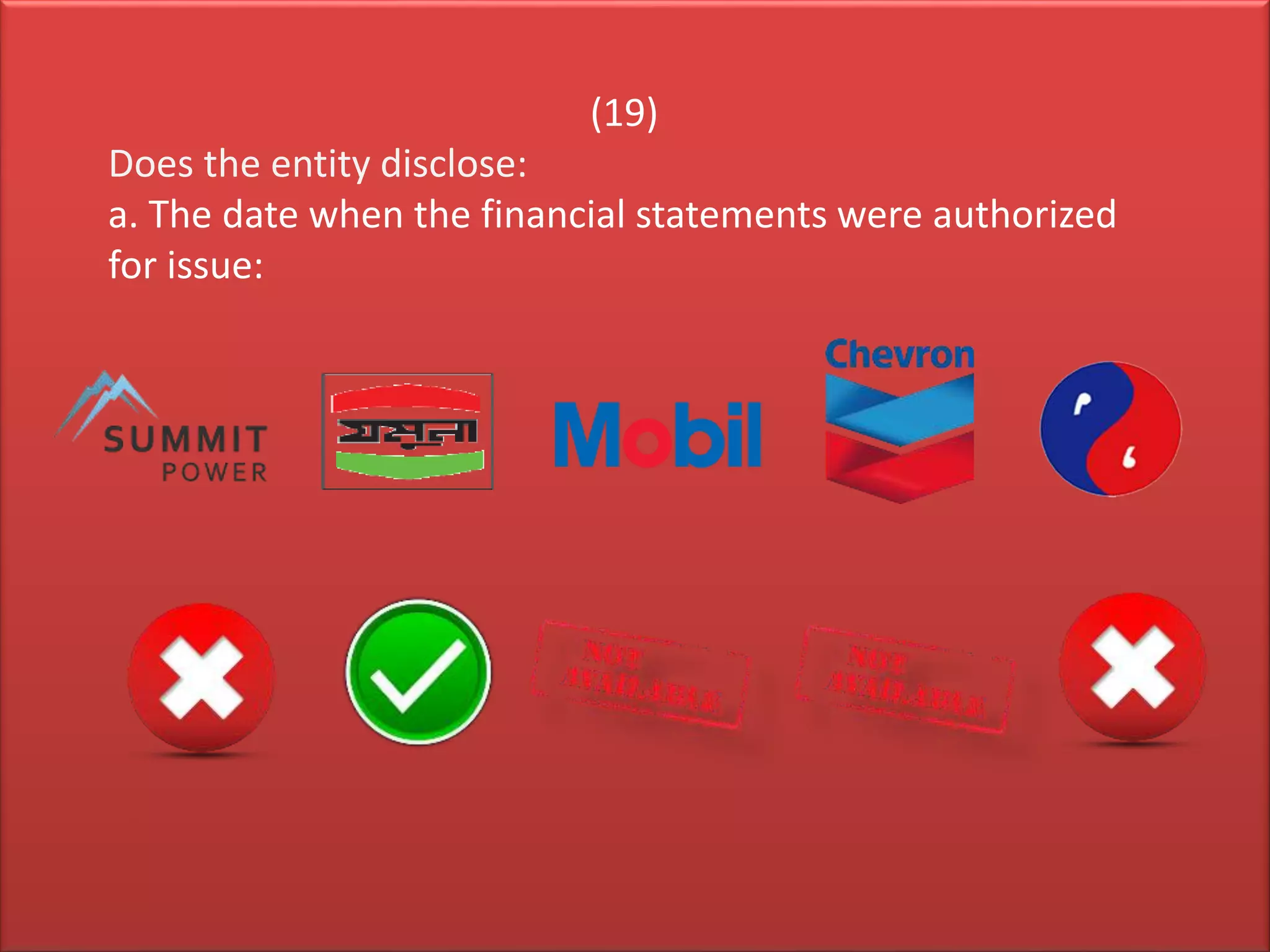

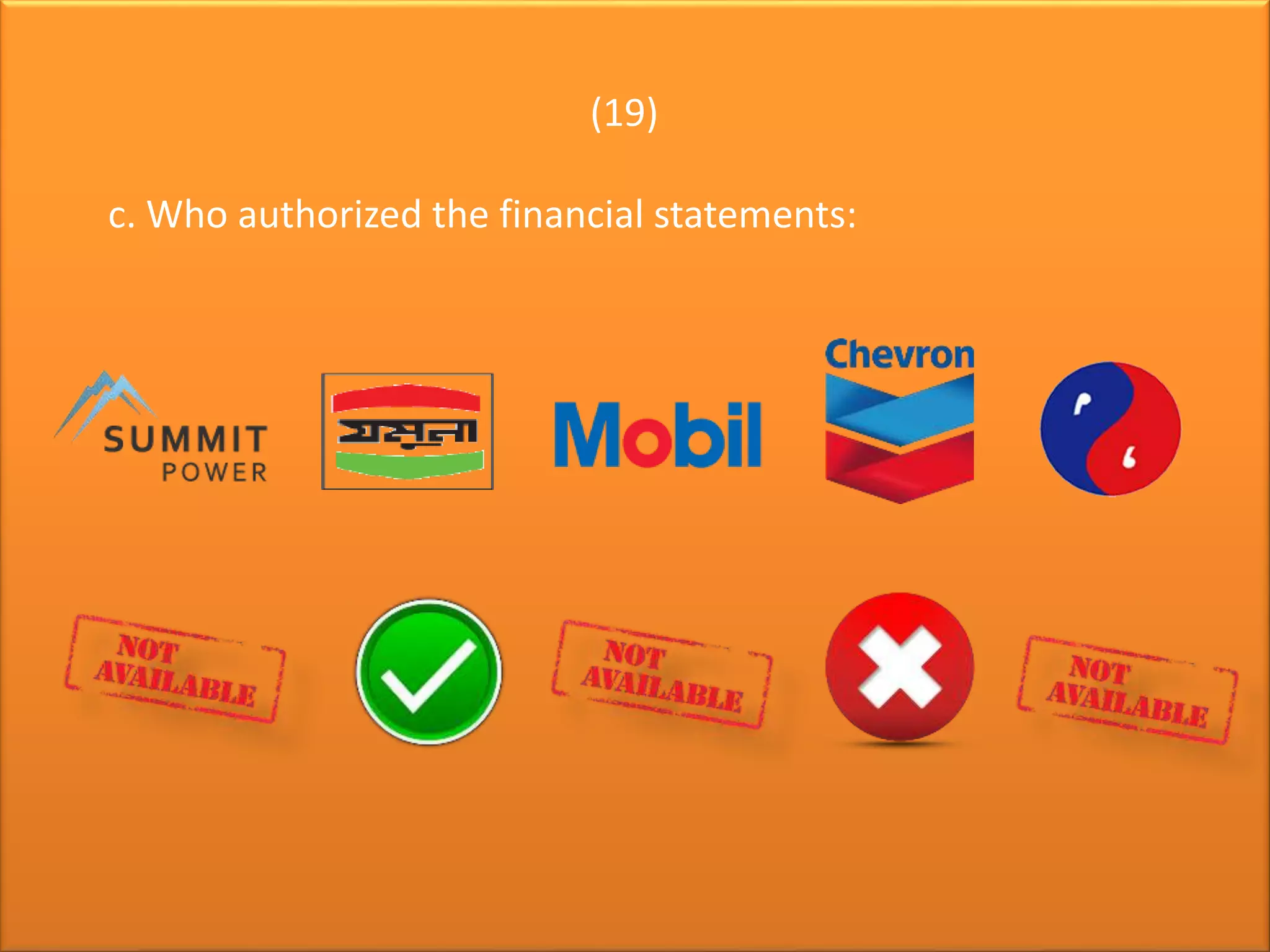

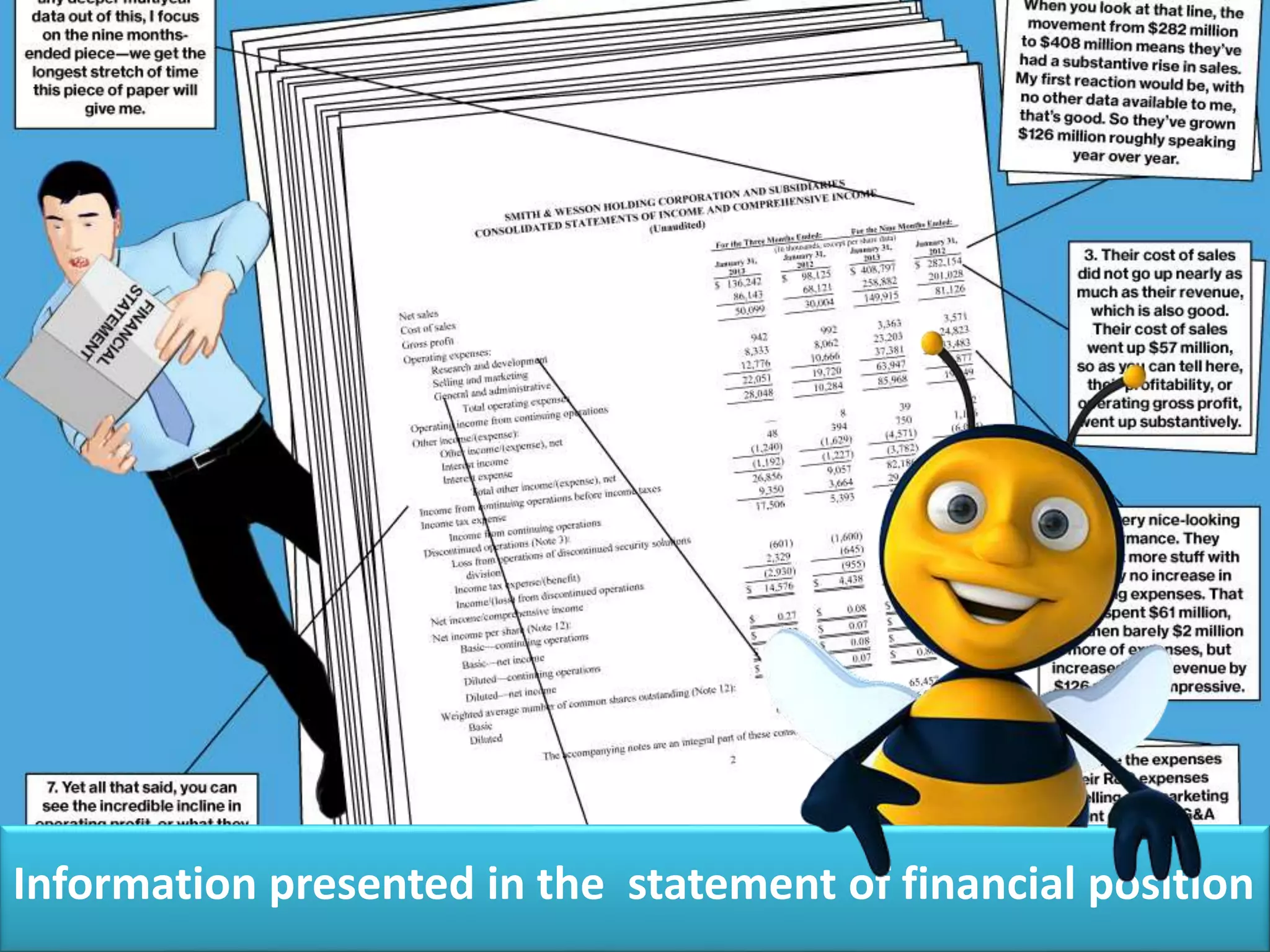

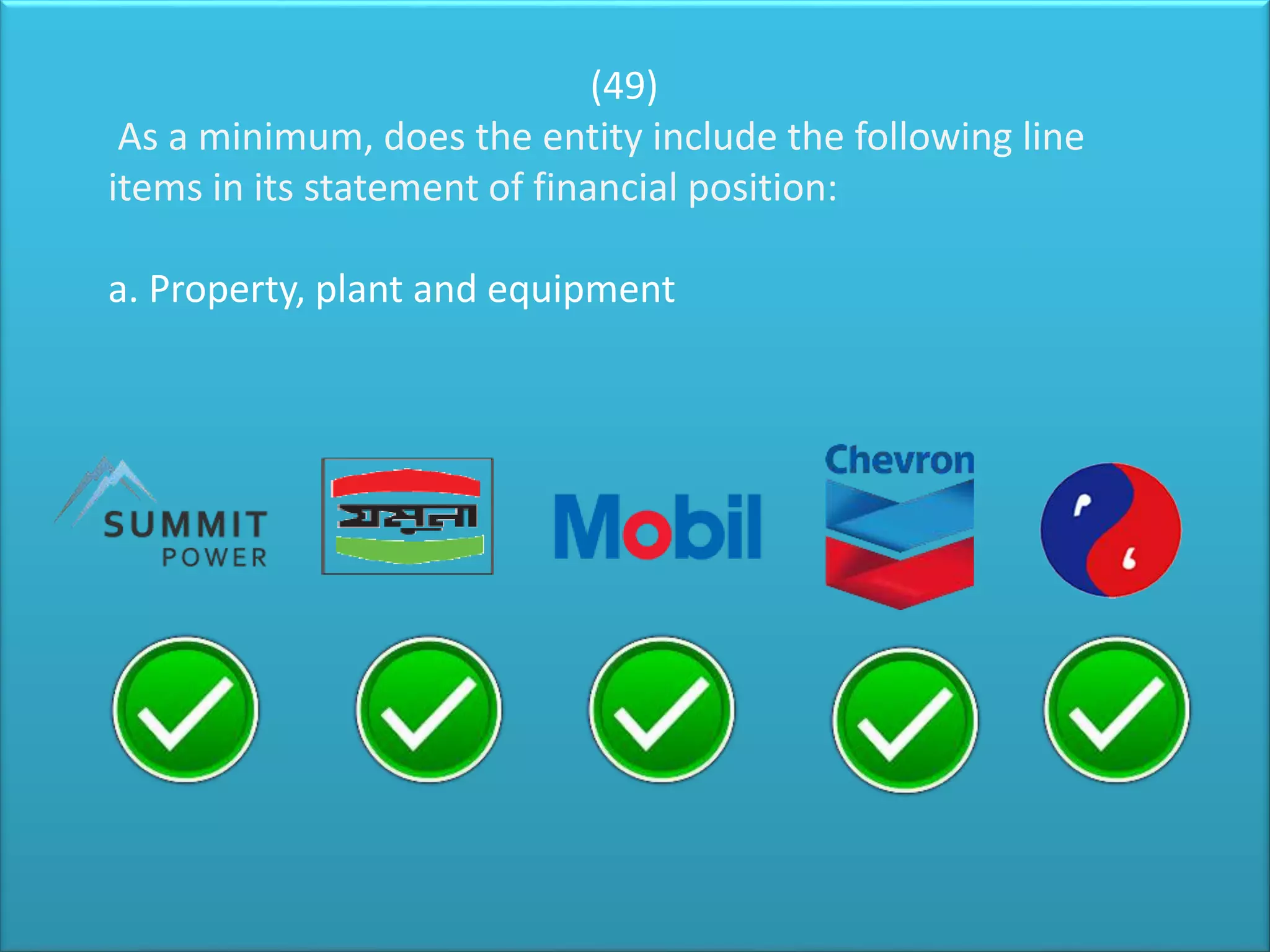

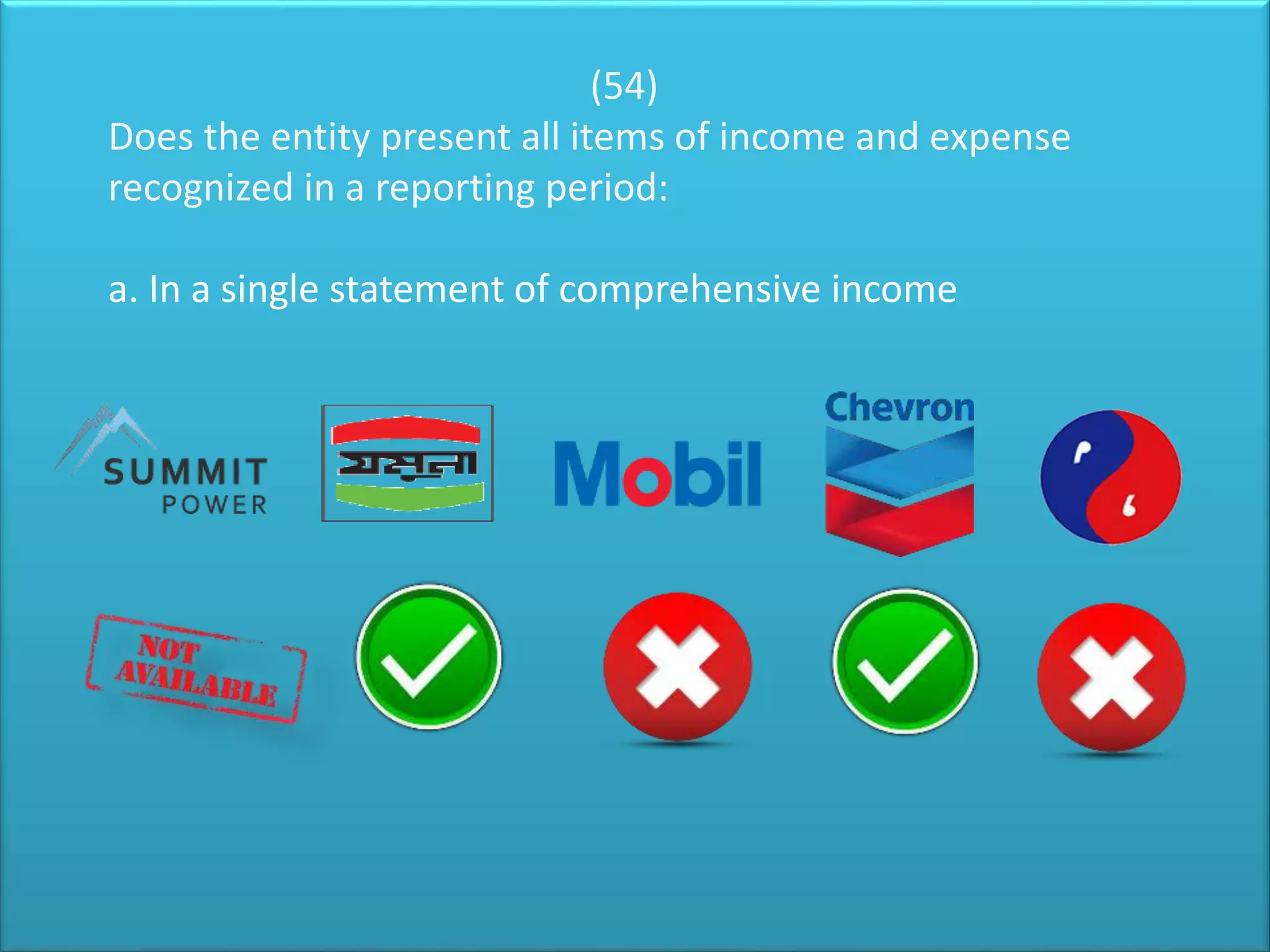

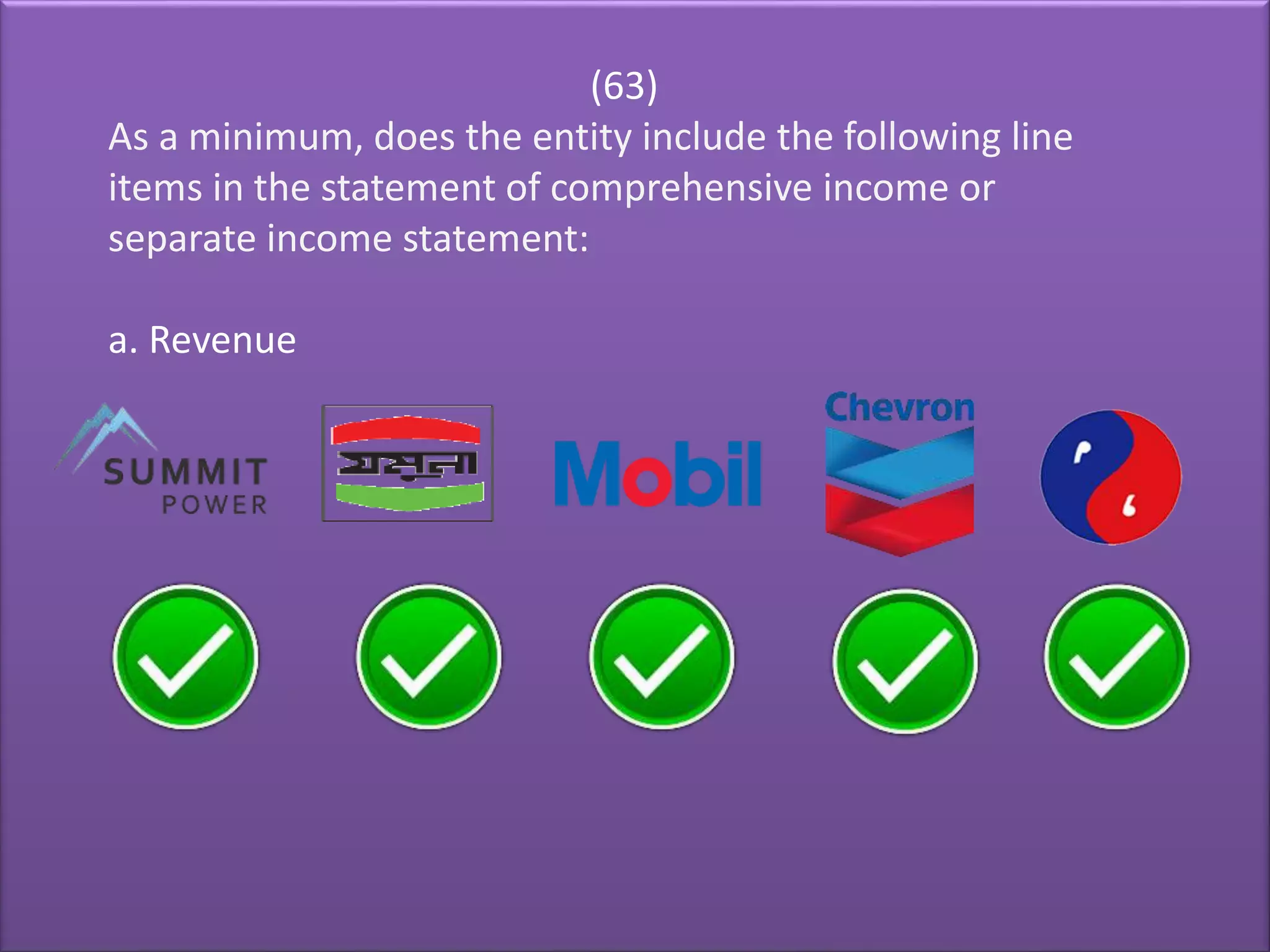

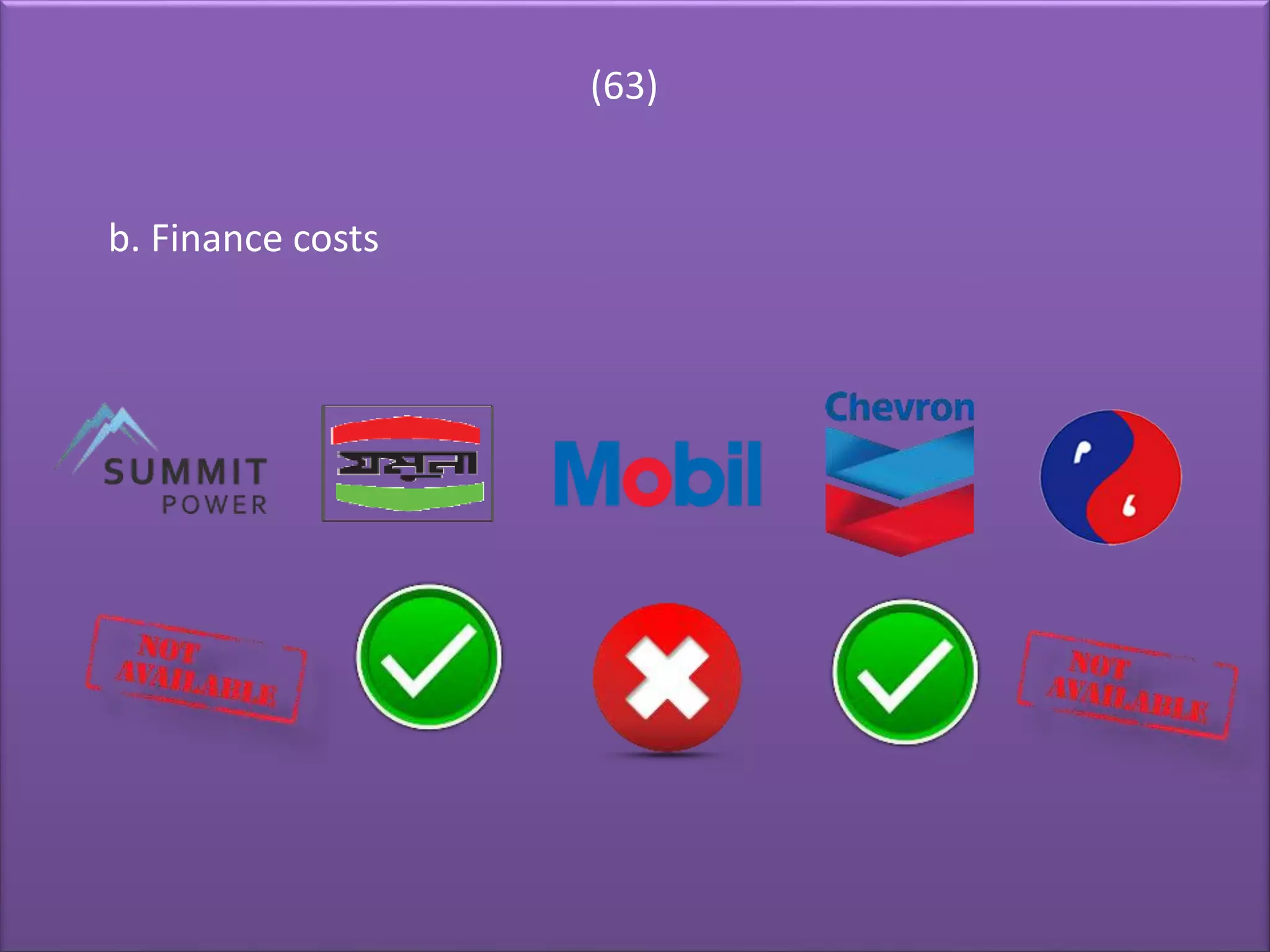

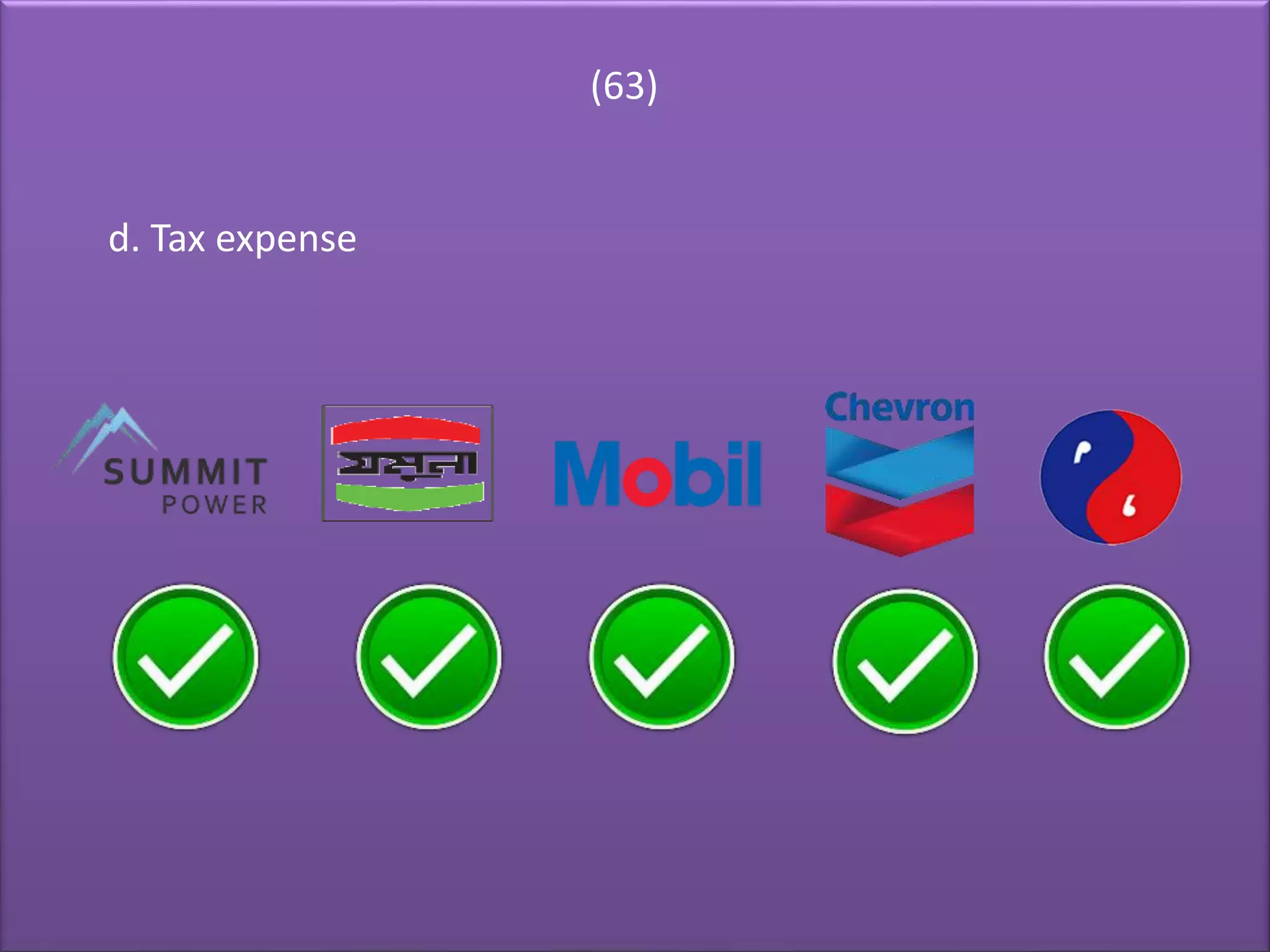

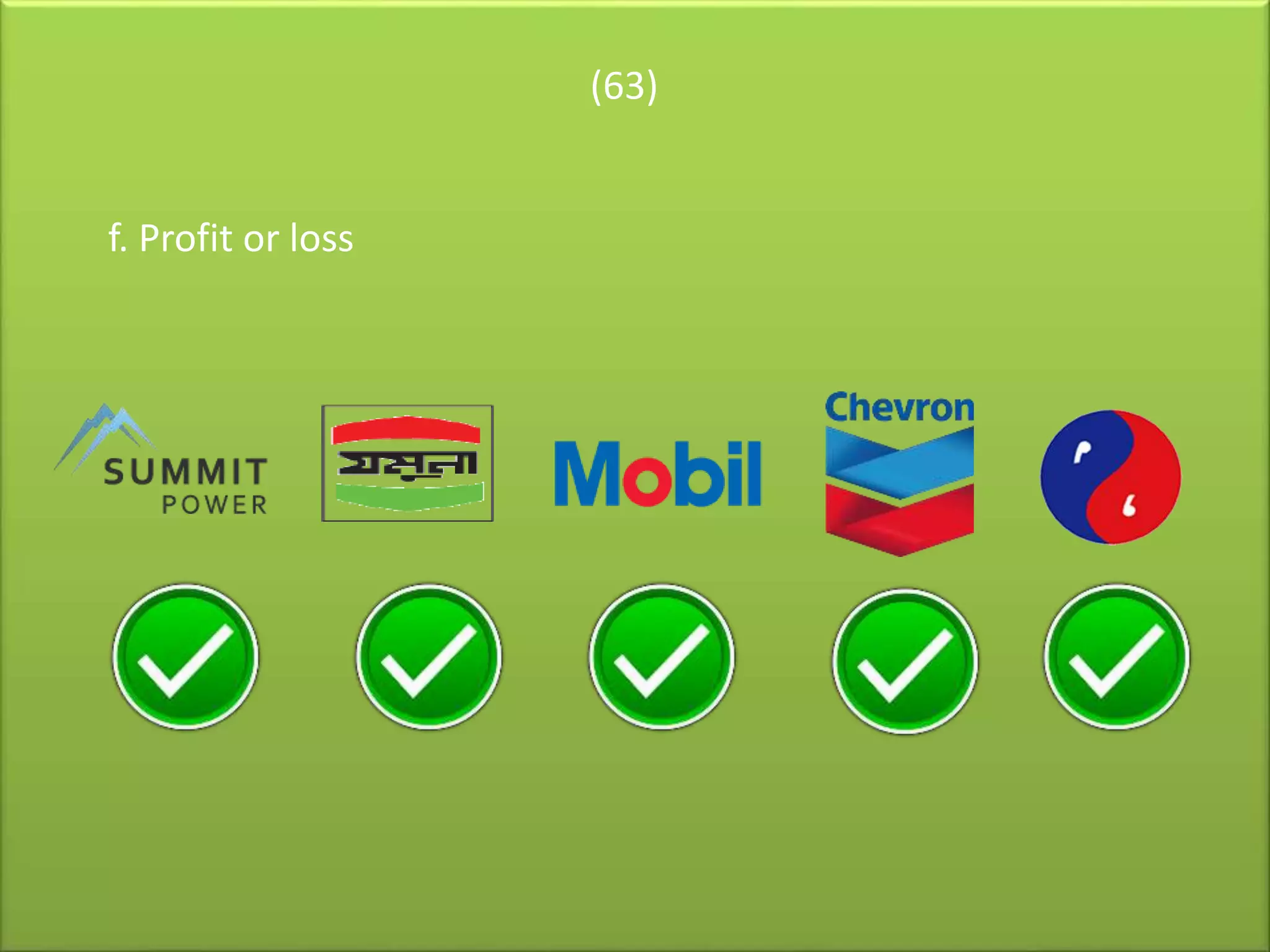

The document discusses power and energy companies in Bangladesh as well as financial statement requirements. It lists several major oil, gas, and power companies in Bangladesh and identifies key components that must be included in financial statements such as statements of financial position, comprehensive income, changes in equity, and cash flows. It also outlines various disclosure requirements for items like comparative information, dates of authorization, and line items to present in statements.