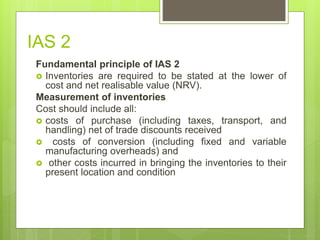

The document discusses international accounting standards. It describes that from 1973 to 2000, the International Accounting Standards Committee issued International Accounting Standards. In 2001, the IASC was replaced by the International Accounting Standards Board which issues International Financial Reporting Standards adopted by over 125 countries. IFRS are principles-based standards drafted for understandability. Application requires increased use of fair values for asset and liability measurement. The document also provides details on specific standards like IAS 1 regarding financial statement presentation.

![IAS 2

IAS 2 does not apply to the measurement of

inventories held by: [IAS 2.3]

producers of agricultural and forest products,

agricultural produce after harvest, and minerals and

mineral products,

commodity brokers and dealers who measure their

inventories at fair value less costs to sell.](https://image.slidesharecdn.com/ifrs-161023113946/85/Ifrs-IAS-1-IAS-2-13-320.jpg)