The document discusses business planning and financial statements for startups. It covers:

1) The business cycle of a typical company, including how equity/debt is used to fund operations and the flow of cash through production, sales, collections, and dividends/reinvestment.

2) The key financial statements - balance sheet, income statement, and cash flow statement - and how they reflect the business cycle and financial condition.

3) Components of the balance sheet in more detail, including assets like cash, receivables, inventory, fixed assets; and liabilities. It also discusses accounting principles like depreciation.

Please respond in 150 with what you understand from the reading bel.docx

1. Please respond in 150 with what you understand from the

reading below

Financial and Business Planning

CHAPTER OVERVIEW

The business planning of startups is often summarized in a

document called the business plan. However, it is important to

understand that business planning is much broader than the

business plan document. This chapter reviews the main aspects

of the general business planning process, while emphasizing the

factors that are important to early stage companies.

The first part of the chapter discusses the company's business

cycle and the manner of presenting information in the financial

statements. Understanding the principles underlying the

financial statements, the manner of preparing them, and the

presentation of the data is essential to anyone involved in the

high tech industry in general, and to persons engaged in

business planning in particular. The second part of this chapter

reviews the main methods of financial forecasting. The last part

of this chapter reviews other issues relating to strategic

planning and reviews the business plan, which is one of the

products of business planning.

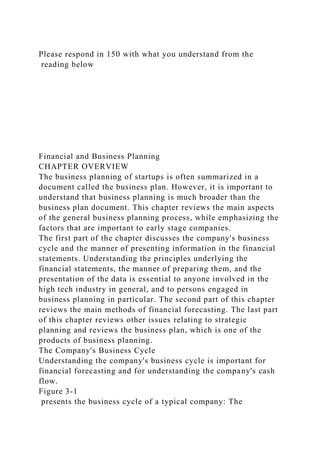

The Company's Business Cycle

Understanding the company's business cycle is important for

financial forecasting and for understanding the company's cash

flow.

Figure 3-1

presents the business cycle of a typical company: The

2. company's equity providers or debt holders infuse money (in the

form of capital and debt, respectively) into the company's cash

account. This cash is used by the company to pay for services,

salaries (human capital), and raw materials for the production

process and to purchase production equipment. The human

capital and the raw materials are used for the development and

production (through means of production such as machinery and

computers) of services and products. Products pass through the

company's inventory and are sold to customers, and services are

provided to customers directly. Customers either pay for the

products or services in cash or receive credit from the company

that is paid later. At the end of each period (cycle), any cash not

returned to the company's debt holders is paid to the tax

authorities, distributed to the shareholders in the form of

dividends, or is re-invested in the company to allow further

business cycles.

Figure 3-1 The Company's Business Cycle

Financial Statements

The company's business cycle is reflected in its financial

statements; the main ones are the company's balance sheet,

income statement, and cash flow statement. The company's

financial statements provide information about its financial

condition: The main purpose of the balance sheet is to describe

the assets and liabilities of the company on a given date; the

main purpose of the income statement is to describe the

transactions and changes in the assets and liabilities of the

company over a period of time; and the cash flow statement

describes the changes in the company's cash flow over a period

of time.

The company's financial statements are usually prepared in

accordance with generally accepted accounting principles

(GAAP). In most cases, the company prepares two sets of

statements: One is used for reporting to the company's

shareholders and debt holders, and the other, which is based on

the tax rules governing the recording of transactions, is used for

reporting to the tax authorities. Obviously, the statements report

3. the same business results, but different rules used for different

needs create differences between the reported results. The

reason for the differences in most cases is the existence of

specific directives for tax reporting, as opposed to other

financial reporting principles that attempt to reflect the

company's business condition in general.

In order to understand the company's financial condition and

prepare financial and business plans accordingly, entrepreneurs

need to understand the meaning of the different statements and

the logic behind the reflection of the company's business cycle.

The following explanation of the statements and their

components is consistent with the customary reporting rules, but

is based on the economic principles underlying them, rather

than on the precise reporting rules.

Balance Sheet

The company's balance sheet reflects the company's overall

assets and liabilities or, in other words, its financial condition

at a given point of time. The balance sheet may be likened to a

snapshot of the company's financial condition. It distinguishes

among various types of assets and liabilities, such as cash held

by the company or in its bank accounts, as opposed to

inventories. The balance sheet also reflects the shareholders'

equity, namely, the investment in the company made by the

shareholders and the profits accumulated in the company

(retained earnings). The company's total recorded assets are

always equal to the sum of its liabilities plus the shareholders'

equity (see

Figure 3-2

).

Figure 3-2 The balance sheet

According to the reporting principles, the company is required

to distinguish between current assets and liabilities which may

be liquidated or are due within one year or less, and other assets

and liabilities, referred to as long-term assets and liabilities,

whose life span is longer than one year. Assets are presented in

a declining order of liquidity, i.e., the most liquid assets appear

4. before the less liquid assets. The first assets presented (namely,

the most liquid) include cash and traded securities, and the

assets presented last are the company's fixed assets, such as

industrial equipment and real estate.

It is important to note that the presentation of assets and

liabilities in financial statements is guided by the principle of

conservativeness: Assets are recorded according to their lowest

reasonable value (in other words, they are not likely to be

liquidated for less), whereas liabilities are recorded according

to their highest reasonable value.

The main assets and liabilities appearing on the balance sheet

(see

Figure 3-2

), are the following:

Assets

Cash, cash-equivalents and securities—

These are the first among the company's current assets. Cash,

cash-equivalents, and securities include, except for the cash in

the company's bank account, all short-term deposits owned by

the company and traded securities, including treasury bills. The

guiding principle underlying the classification of these assets is

that they entail a relatively low risk in proportion to their value

at the time of liquidation, and can be liquidated quickly

(usually, within less than three months).

Accounts Receivable—

Since most companies do not receive payment in cash for all of

their sales, almost every company that has reached the stage of

sales has an Accounts Receivable (or Receivables) item. These

are short-term customer debts that the company records on its

balance sheet after offsetting allowance for doubtful debts

which it does not expect to collect. For example: a company by

the name of Speed is owed $1,000 by its customers, but predicts

that only $800 will be paid. The company will present in its

balance sheet a net amount of $800 under this item, representing

5. the portion of the debts that the company expects to collect.

This amount is produced by deducting an allowance of $200 for

doubtful debts from the gross debt of $1,000.

Inventory—

Inventories are assets in various stages of production that the

company expects to sell as products. Inventories are divided

into several types in accordance with their stage along the

production process. Companies usually specify the types of

inventories they have, since investors attribute a different value

to different types of inventories. For instance, in most cases, an

inventory of raw materials is easier to liquidate than an

inventory of products in progress. A manufacturing company

will generally have three types of inventories: an inventory of

raw materials, an inventory of goods in process, and an

inventory of finished goods. Inventories are estimated according

to their cost, not according to the revenue they are expected to

produce, unless such revenue is lower than the cost of

production (in which case, the principle of conservativeness

directs that they be recorded according to their net realizable

value). The reporting of inventories in progress, as well as

inventories of finished products, usually includes also allocated

labor and overhead costs (such as electricity and some of the

depreciation of the equipment used to manufacture them).

When analyzing inventories, it is important to pay attention to

the method of recording of the inventories, since a company

selling products uses inventories of raw materials and finished

products which might be recorded according to different prices.

For instance, let us assume that Speed manufactures instruments

that it combines with tractors that it purchases. In one month,

the company purchased three identical tractors at different

prices (according to the order of acquisition): $100,000,

$120,000 and $115,000. At the end of the month, the company

sold one set of equipment (a tractor on which the company's

equipment was assembled) for $200,000. Obviously, the

reported financial results reported by Speed will be affected by

6. the choice of the tractor that constitutes a material part of the

sold equipment. If the company uses an inventory method called

FIFO (First In, First Out), then, assuming that Speed had no

prior inventories, it will report an inventory of $235,000.

$100,000 (the cost of the first tractor) will be reported as part

of the cost of the equipment sold (see the next subsection for a

further discussion of revenues and expenses). If the company

uses the method of LIFO (Last In, First Out), then the company

will report an inventory of $220,000. According to yet another

method, the inventory (and the components of the cost of the

goods sold) is calculated according to the average cost of the

components of the sale. In our case, the inventory at the end of

the period will be reported at: (100,000 + 120,000 +

115,000)*(2/3) = 223,333.33.

Advance payments—

Although companies usually try to defer payments, in many

cases they pay in advance for services they will receive after the

date of the balance sheet. For instance, companies often pay

rent for several months in advance. The principle in the

statements is to report expenses and revenues at the time of the

economic occurrence of their underlying events. In other words,

since the services will be received after the date of the

statements, the expenses will be recorded concurrently with the

receipt of the service. Therefore, the balance sheet will reflect

an asset incorporating the cost for which the services or product

was not yet received.

Long-term assets—

Assets that are expected to contribute to the production of

revenues over a period longer than one year are referred to as

long-term assets. They are divided into two main groups:

tangible assets and intangible assets (intellectual property).

Tangible assets include real estate, office equipment, production

equipment, long-term financial assets, and stocks in other

companies. These assets are usually recorded according to their

7. historical value, i.e., according to the price of purchase,

adjusted for depreciation.

The term “depreciation” attempts to reflect the devaluation of

assets over their economic life span or usage. The periodic

depreciation of an asset is part of the expenses reflected in the

income statement. There are various methods for calculating

depreciation that are deployed in accordance with the character

of the assets, the industry, and the company holding the asset.

The most widely-used method is that of the “straight line”:

First, the asset's economic life span is estimated, and a

proportionate part of the cost is recorded every year as an

expense. For instance, if a car was bought for $20,000, and its

economic life span is five years, then $4,000 are recorded every

year as an expense, and the asset is reported on the balance

sheet with a value that decreases by such amount every year.

Another common method is that of the “accelerated

depreciation,” whereby the asset is depreciated more in the first

years. This method reflects an accelerated depreciation in the

first years of the asset's life. The value of a new car, for

instance, is known to decline faster in its first few years.

There are other depreciation methods, and in many cases the

chosen method takes into account the amount of use made of the

asset. For instance, consider the case of a factory where one

million cars can be manufactured before it needs to be

renovated. Obviously, it would be logical to express the

depreciation of the factory over time as a function of the

number of cars actually manufactured in it.

Assets appear on the balance sheet according to their historical

value, less depreciation and any other devaluation resulting

from a decline in their market value below their cost. In fact,

the net fixed assets will be equal, at the end of each period, to

the net fixed assets at the end of the previous period, plus new

fixed assets acquired, minus the net cost of fixed assets sold and

minus periodic depreciation and any other reduction in the

recorded value of the fixed assets.

Where the statements of non-American companies are

8. concerned, it is important to understand that in different

countries the value of assets may be expressed differently, and

in many cases assets may be revalued according to their market

value at the time. Fixed assets may be revalued, for instance, in

the United Kingdom and in the Netherlands. The principle in

these countries is that assets are reflected according to the cost

to the company of replacing them. In other words, if the car on

Speed's balance sheet (which, for purposes of this example, will

be reported according to British rules) is one year old, then,

instead of reporting a depreciated value of $16,000 ($20,000 –

$4,000), the cost of a similar used car on the market will be

checked. If such cost is $21,000, then the car will be recorded

in the balance sheet with this value. This change in value will

concurrently be reflected under the item of the company's

shareholders' equity. In all countries, if the market value of an

asset considerably declined below its depreciated cost, and such

devaluation is not expected to be remedied, then the value of

the asset has to be reduced in the balance sheet by recording a

loss as a result of the devaluation of the asset (since such

devaluation is in lieu of future depreciation).

Intangible assets include items such as the cost of acquired

patents, trademarks and trade names, franchises, and the cost of

investments in other companies above the value of their tangible

assets (goodwill). These assets also appear on the balance sheet

and are depreciated in accordance with their expected life span,

with certain restrictions (in accordance with the accounting

rules applicable in each country) with respect to the manner of

recording of various assets and liabilities. For example, if

Speed bought a license to use a patent that will expire in ten

years in consideration for one million dollars, then it will be

depreciated over ten years, unless the patent is expected to

become worthless after a shorter period of time, or is expected

to continue being valuable after it expires.

Following an accounting rule change, effective from the year

2002, goodwill does not have to be depreciated if its value, as

deemed by the company's management, has not declined.