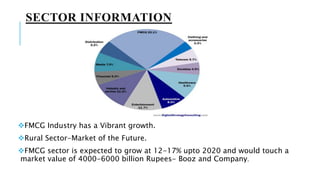

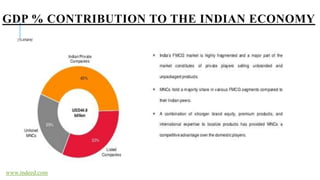

Dabur, established in 1884, is the third-largest FMCG company in India, focusing on health supplements and ayurvedic products. The company faces intense competition and has to continually innovate its product lines to maintain market share in a sector characterized by high buyer and supplier power. The FMCG industry is expected to grow significantly, contributing approximately 2.5% to India's GDP by 2020.