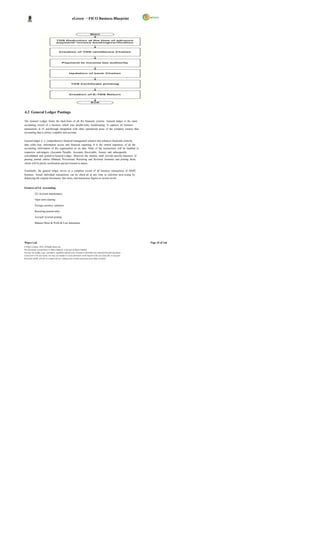

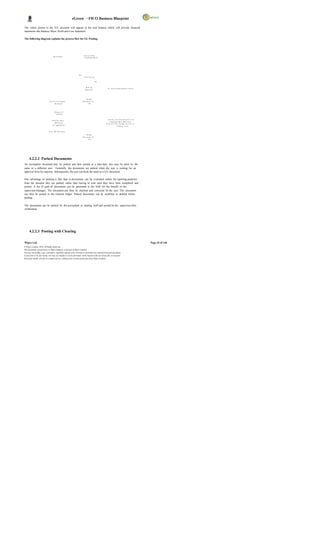

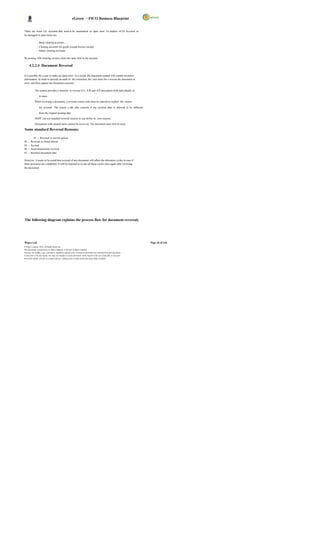

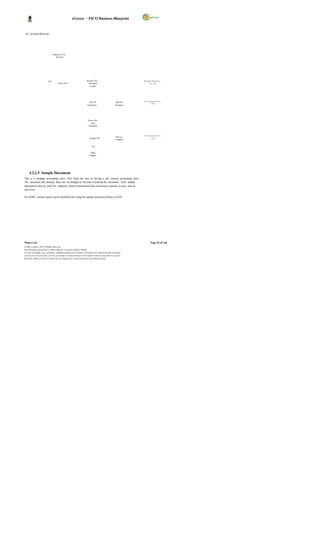

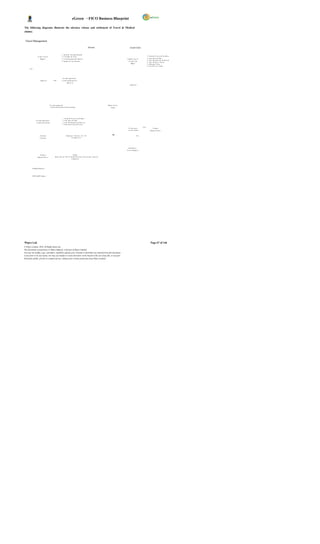

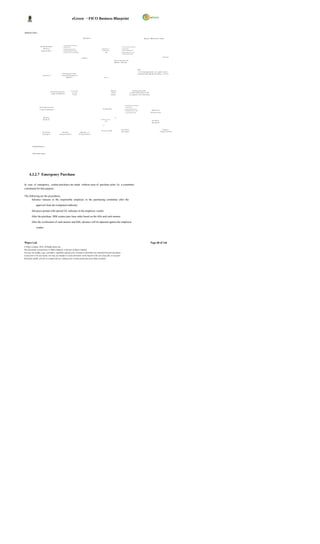

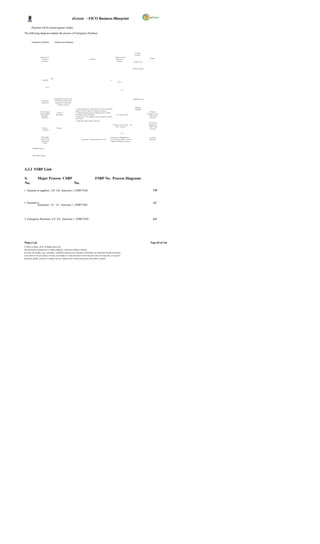

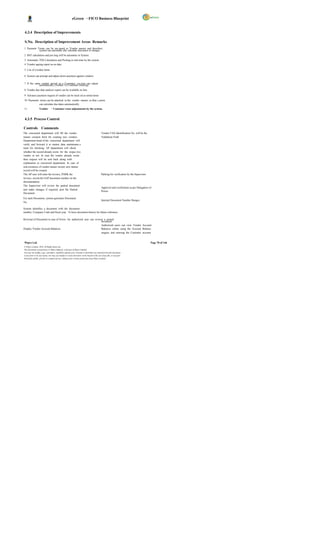

This document provides a business blueprint for financial accounting and controlling processes for Druk Green Power Corporation Limited and Dagachhu Hydropower Corporation Limited. It discusses the organizational structure, master data, configuration settings, and key business processes like general ledger postings and account payables. The blueprint aims to integrate financial accounting with other modules like fixed assets, materials management, and human resources for efficient financial management.