The document discusses estimating initial margin for a bank's OTC contracts using machine learning techniques, emphasizing the need to forecast the initial margin under various scenarios. It reviews several regression methods including least-squares, kernel regression, and gradient boosting, while highlighting that K-nearest neighbor regression may offer the best balance of simplicity and performance. The document concludes with recommendations for validating assumptions and improving neural network models for more complex portfolios.

![Initial Margin

Our purpose is to be able to produce the forecast of initial margin.

For the purpose of MVA, the expectation Et [IM(t)] is needed, e.g.

Green and Kenyon

MVA = −

∫ T

t

((1 − RB)λB(u) − sI (u)) e−

∫ u

t (r(s)+λB (s)+λC (s))ds

×Et [IM(t)] du,

but in general, if the intention is to calculate exposure, what we will

strive for is the forecast along a particular scenario path m

IMm(t) = Q99 (∆m(t; δIM)|Ft)

where Q99 is the 99-th percentile, δIM is the MPoR, and ∆m(t; δIM)

is the clean change in portfolio value

∆m(t; δIM) = Vm(t + δIM) + Um(t, t + δIM) − Vm(t) (1)

4](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-4-320.jpg)

![Assumptions

We follow L. Andersen, M. Pykhtin, and A. Sokol and assume that

as δIM is relatively short, the P&L under the quantile is Gaussian

with zero drift

IMm(t) ≈ σm(t)Φ−1

(99%)

and where the variance is defined as

σ2

m(t) = E

[

∆2

m(t, δIM)|Ft

]

Forecasting the variance σ2

m(t) is really the purpose of this talk.

5](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-5-320.jpg)

![Longstaff-Schwartz Regression

F(t0, t) = E [f (xt; t0, t)|Ft0 ]

For square-integrable functions L2(Ω, F, Q), the expansion via or-

thonormal functions can be used to resolve the expectation

f (xt; t0, t) =

∞∑

i=0

ai (t0, t)Li (xt)

where Li (xt) is part of an orthonormal function sequence, which

covers the L2 space

F(t0, t) =

∞∑

i=0

ai (t0, t)

7](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-7-320.jpg)

![Longstaff-Schwartz Regression

The coefficients ai (t0, t) are proportional to

ai (t0, t) = E [f (xt; t0, t)Li (xt)|Ft0 ] (2)

With such a sequence, one can guarantee that for a chosen error

tolerance ϵ, there exists an N such that

F(t0, t) −

N∑

i=0

ai (t0, t) < ϵ

However, if one would need to evaluate Eq.(2) to use the method,

there would be little use for it.

8](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-8-320.jpg)

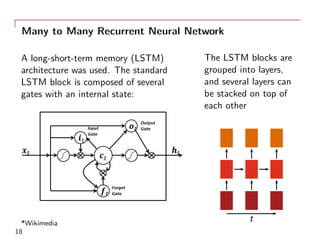

![Machine Learning tools

While there are a myriad methods available from the machine learn-

ing toolkit, for time constrain we will look at the following methods

Least-Squares Regression (LSE)

Nadaraya-Watson kernel Regression (NWK)

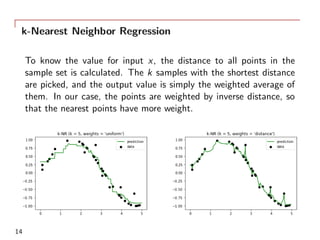

k-Nearest Neighbor Regression (kNR)

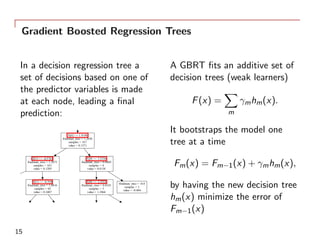

Gradient Boosted Regression Trees (GBRT)

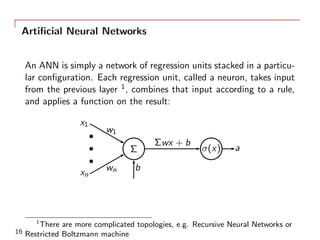

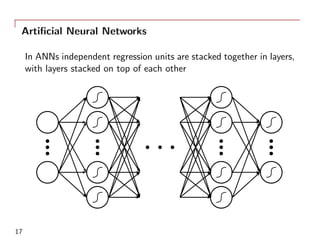

Recurrent Neural Network (LSTM)

All attempt to approximate the conditional expectation of Y relative

to a variable X

E [Y |X] = m(X)

11](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-11-320.jpg)

![Benchmark

Originally we intended to use forward SIMM as the benchmark, but

as what we are calculating and SIMM are different, and need to

be scaled to compare them (see Anfuso et. al 2016), a different

benchmark was used

σ2

m(t) ≈ E

[

∆2

m(t, δIM)|V (t) = Vm(t)

]

≈ E

[

∆2

m(t, δIM)|V (t) ≈ Vm(t)

]

= E

[

∆2

m(t, δIM)| |V (t) − Vm(t)| < ϵ

]

For the regular calculations 1k scenarios are used, but 100k for the

benchmark calculations. ϵ is chosen on a timestep basis, at most

being half the width of the distance between the two nearest points

on that time step.

20](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-20-320.jpg)

![IR Swap

0 50 100 150 200 250

Timestep

1.78e+09

3.56e+09

5.34e+09

7.12e+09

8.90e+09

1.07e+10

1.25e+10

1.42e+10

1.60e+10

E[σ2(t)]

LSE

NWK

kNR

GBRT

LSTM

Benchmark

21](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-21-320.jpg)

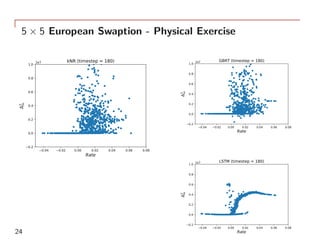

![5 × 5 European Swaption - Physical Exercise

0 50 100 150 200 250

Timestep

1.88e+06

3.76e+06

5.64e+06

7.52e+06

9.40e+06

1.13e+07

1.32e+07

1.50e+07

1.69e+07

E[σ2(t)]

LSE

NWK

kNR

GBRT

LSTM

Benchmark

22](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-22-320.jpg)

![5 × 5 European Swaption - Physical Exercise

While all methods so far would probably be acceptable to calculate

E[IM(t)], and hence MVA, not all would be acceptable to calculate

exposure

−0.04 −0.02 0.00 0.02 0.04 0.06

Rate

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Δ2

m

1e7 BenchmarkΔ(timestepΔ=Δ180)

−0.04 −0.02 0.00 0.02 0.04 0.06 0.08

Rate

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Δ2

m

1e7 LSEΔ(timestepΔ=Δ180)

23](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-23-320.jpg)

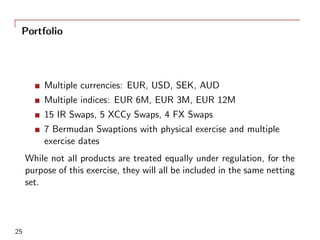

![Portfolio

0 50 100 150 200 250

Timestep

1.33e+13

1.73e+13

2.14e+13

2.54e+13

2.95e+13

3.35e+13

3.76e+13

4.16e+13

4.57e+13

E[σ2(t)]

LSE

NWK

kNR

GBRT

LSTM

Benchmark

26](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-26-320.jpg)

![k-Nearest Neighbor Single Model for Swaption

0 50 100 150 200 250

Timestep

1.88e+06

3.76e+06

5.64e+06

7.52e+06

9.40e+06

1.13e+07

1.32e+07

1.50e+07

1.69e+07

E[σ2(t)]

2 day delay

pre-trained kNR

timestep trained kNR

Benchmark

28](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-28-320.jpg)

![k-Nearest Neighbor Single Model for Swaption

0 50 100 150 200 250

Timestep

1.69e+06

3.38e+06

5.07e+06

6.76e+06

8.45e+06

1.01e+07

1.18e+07

1.35e+07

1.52e+07

E[σ2(t)]

10 day delay

pre-trained kNR

timestep trained kNR

Benchmark

29](https://image.slidesharecdn.com/andreshernandezmvann20170324-170327112459/85/Estimating-Future-Initial-Margin-with-Machine-Learning-29-320.jpg)

![STOCK PRICE PREDICTION USING MACHINE LEARNING [RANDOM FOREST REGRESSION MODEL]](https://cdn.slidesharecdn.com/ss_thumbnails/irjet-v10i7108-230815114054-b07e3795-thumbnail.jpg?width=640&height=640&fit=bounds)