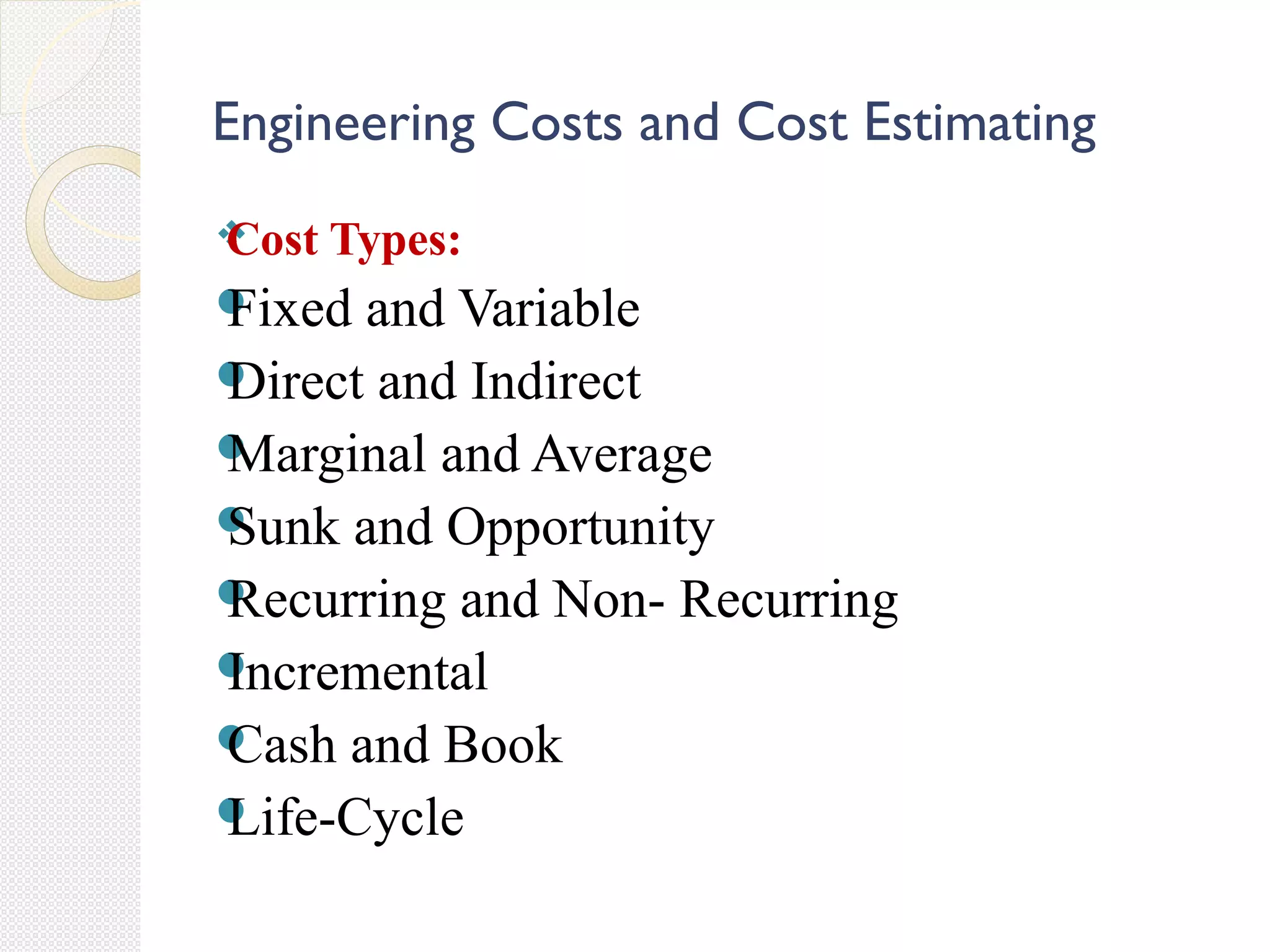

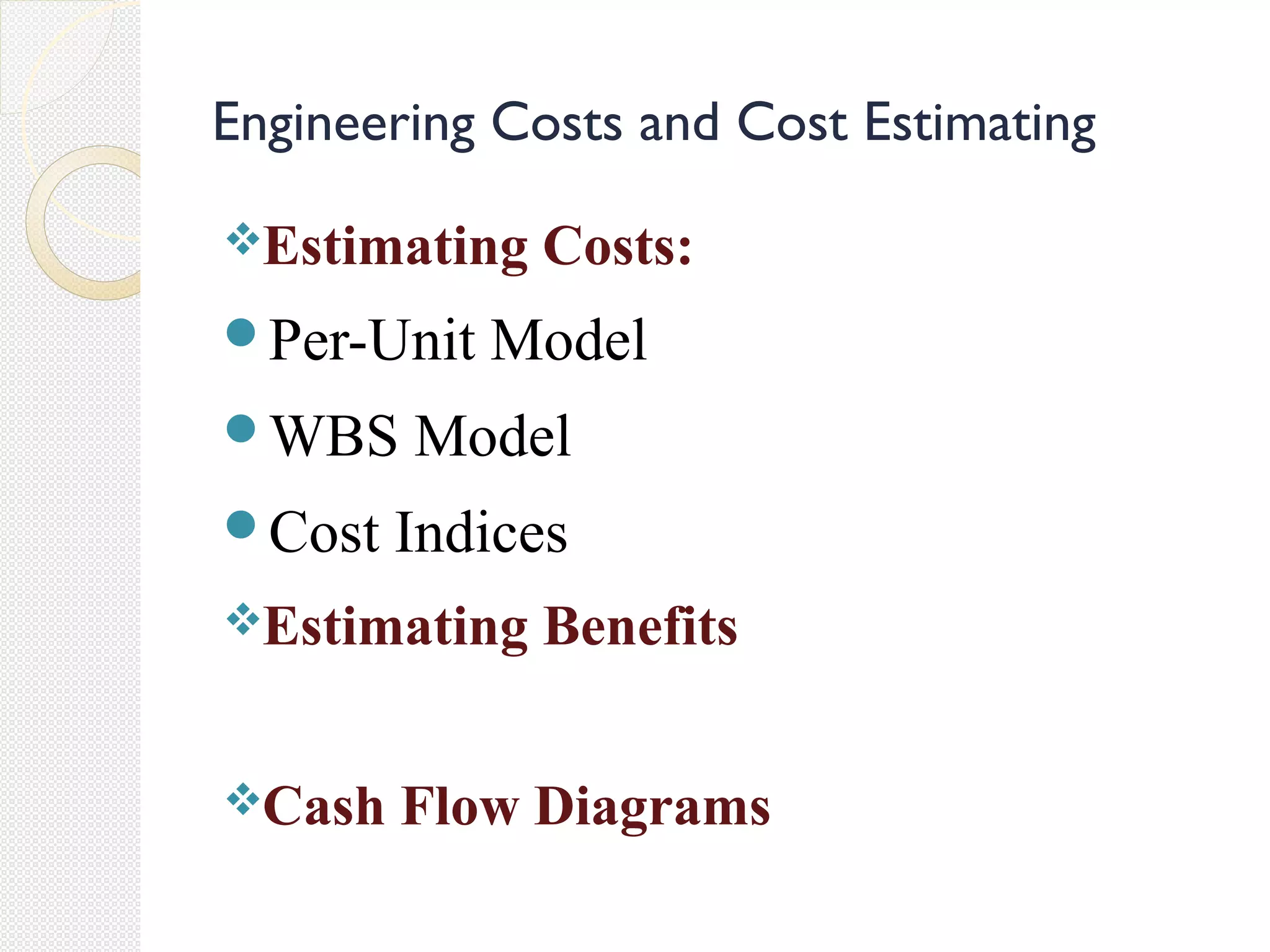

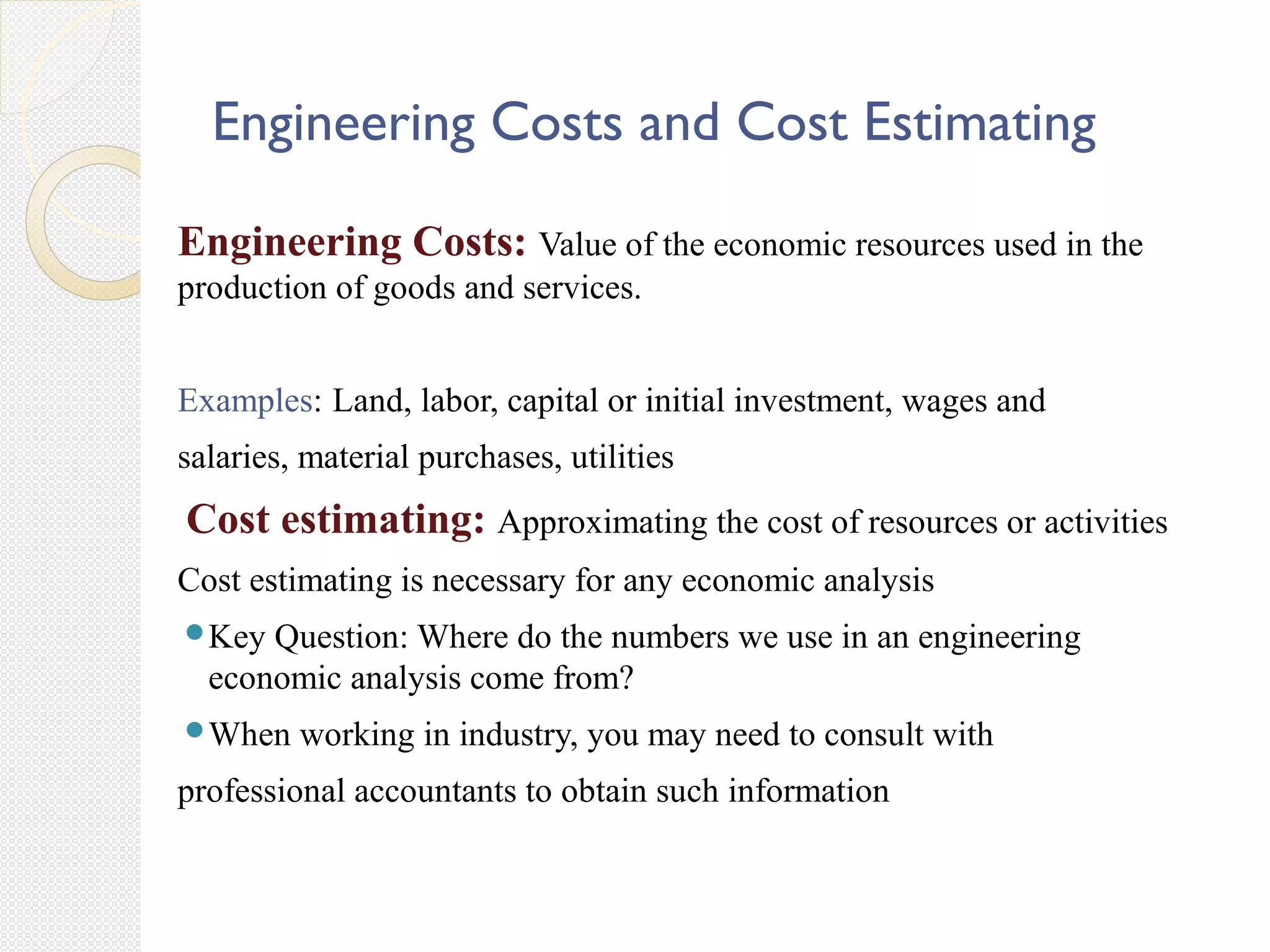

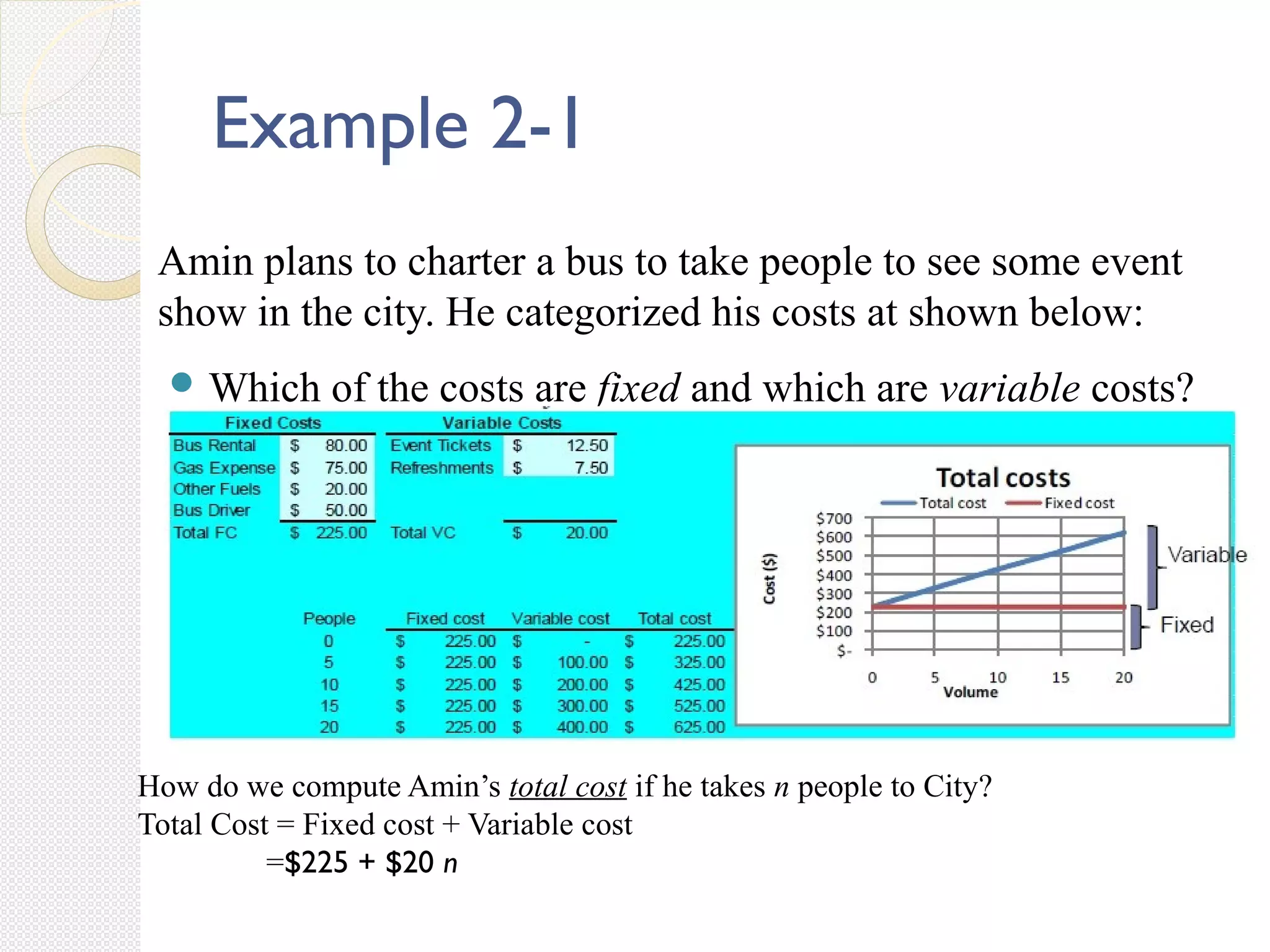

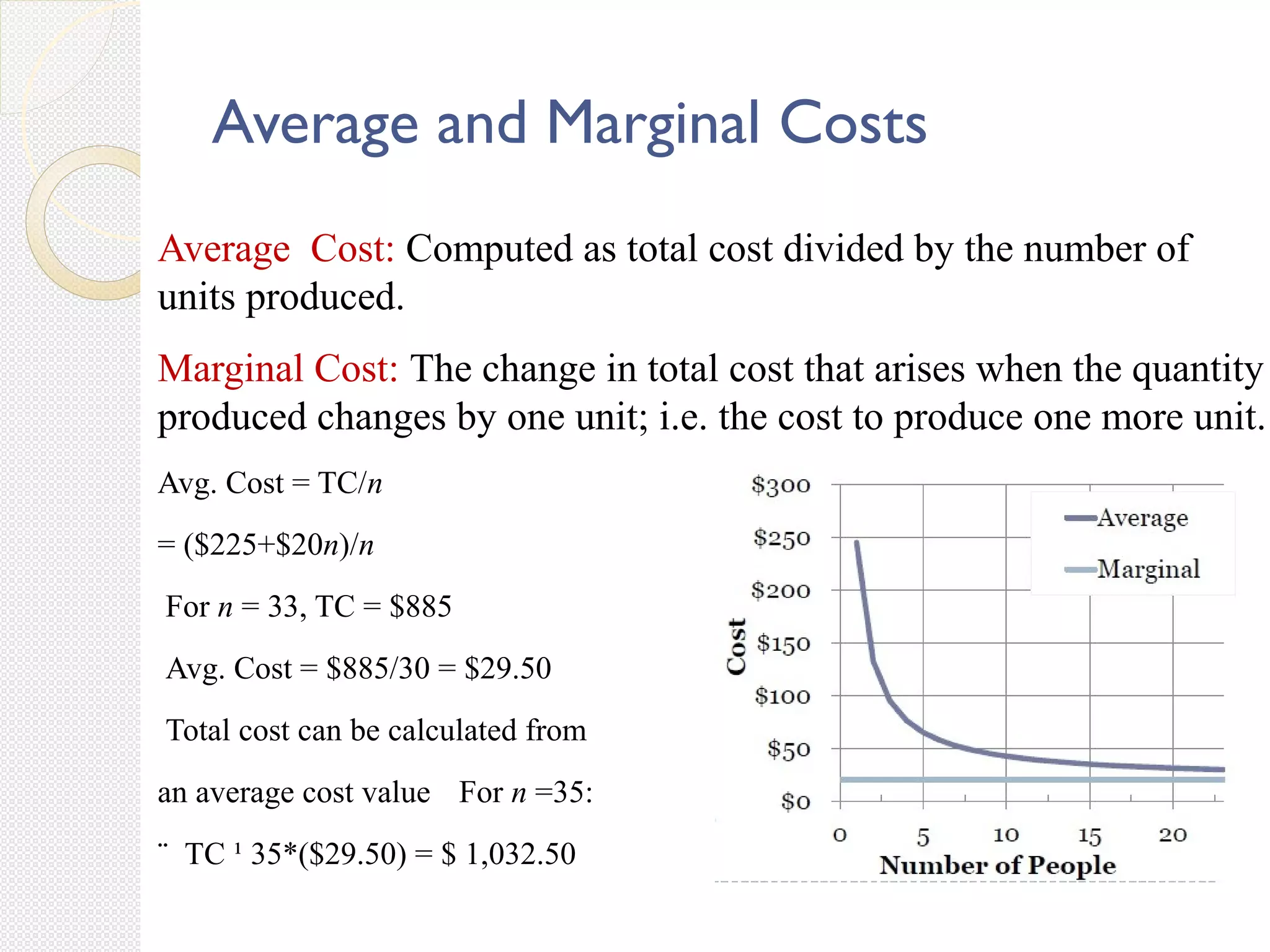

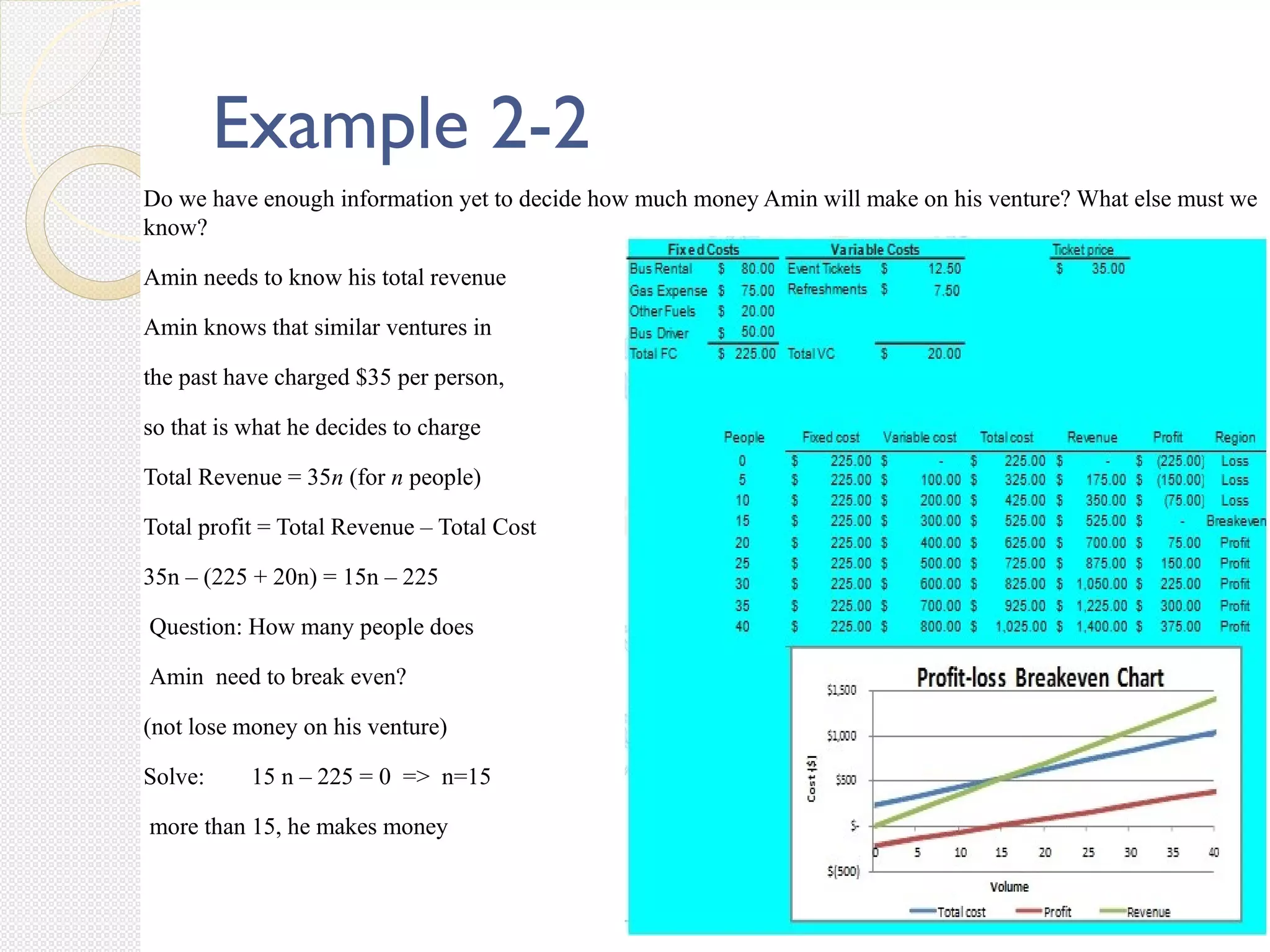

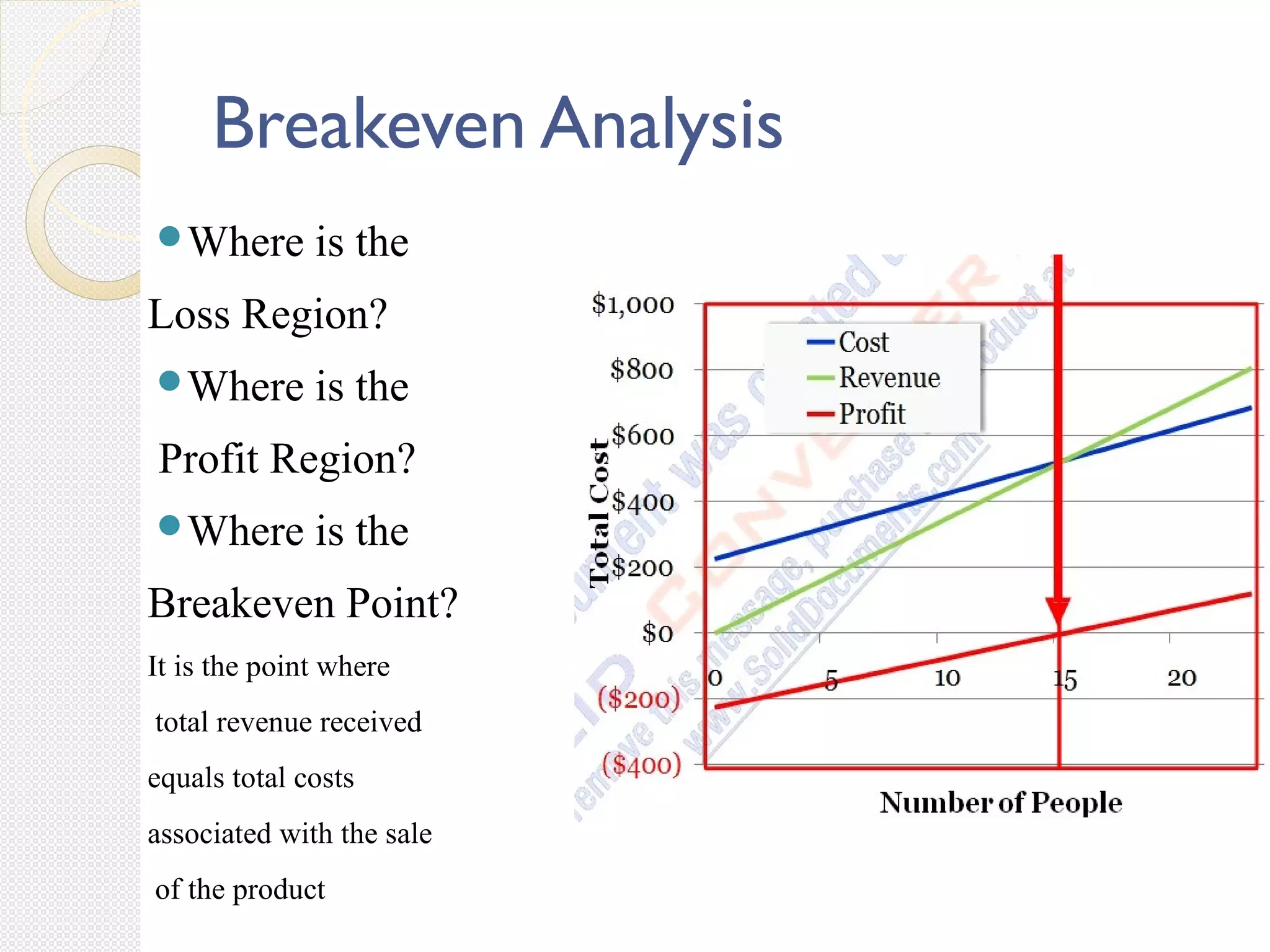

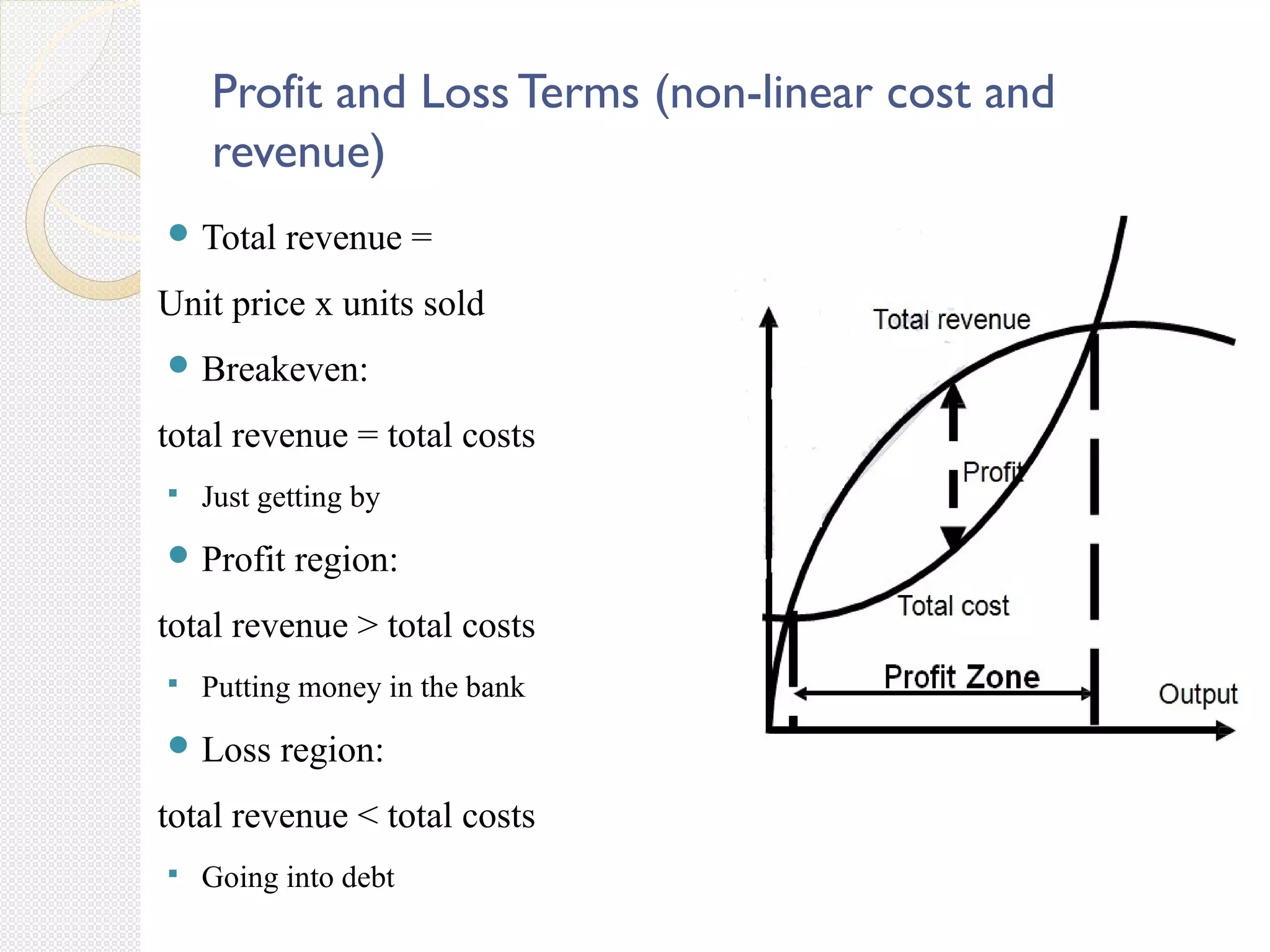

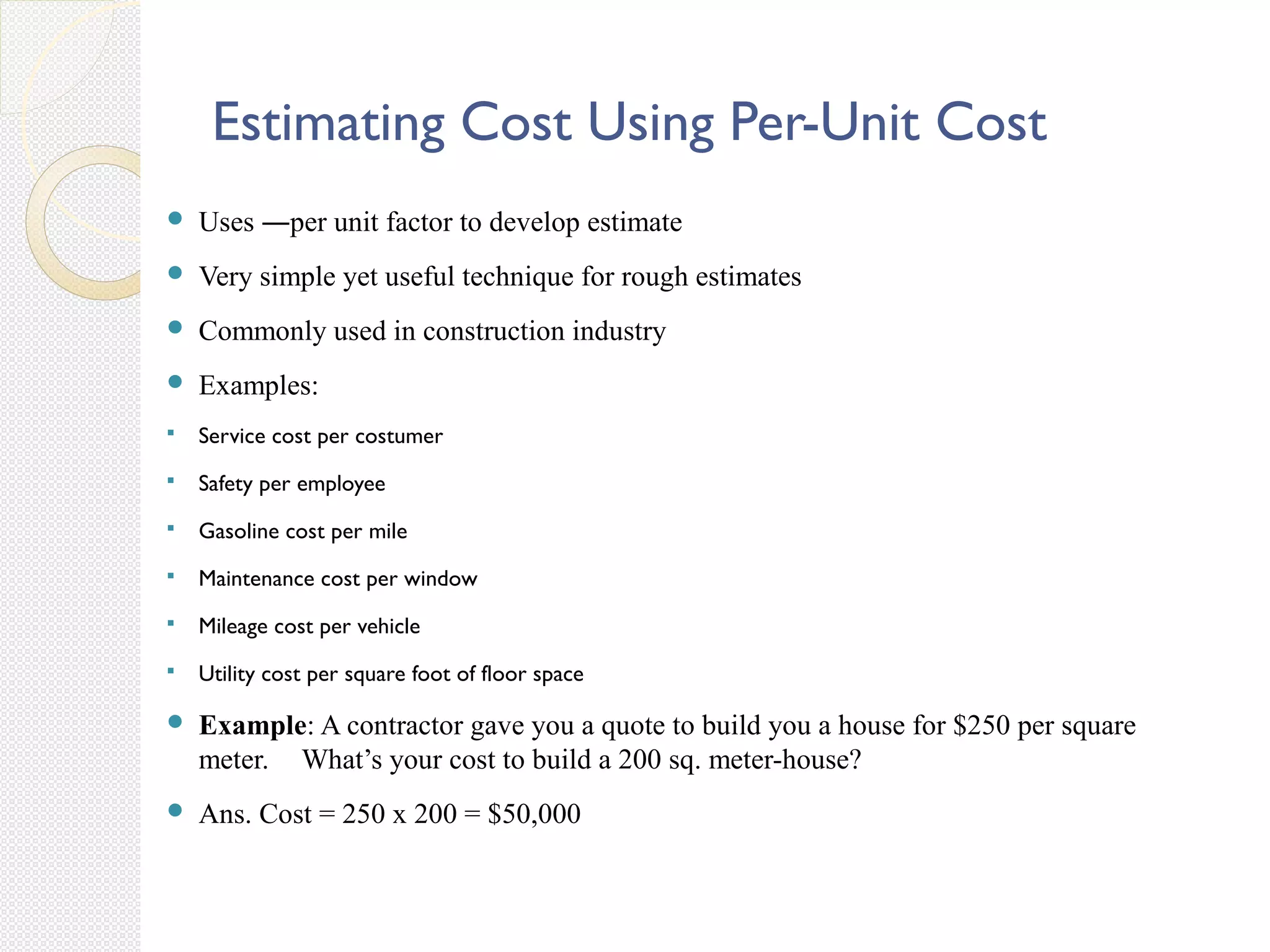

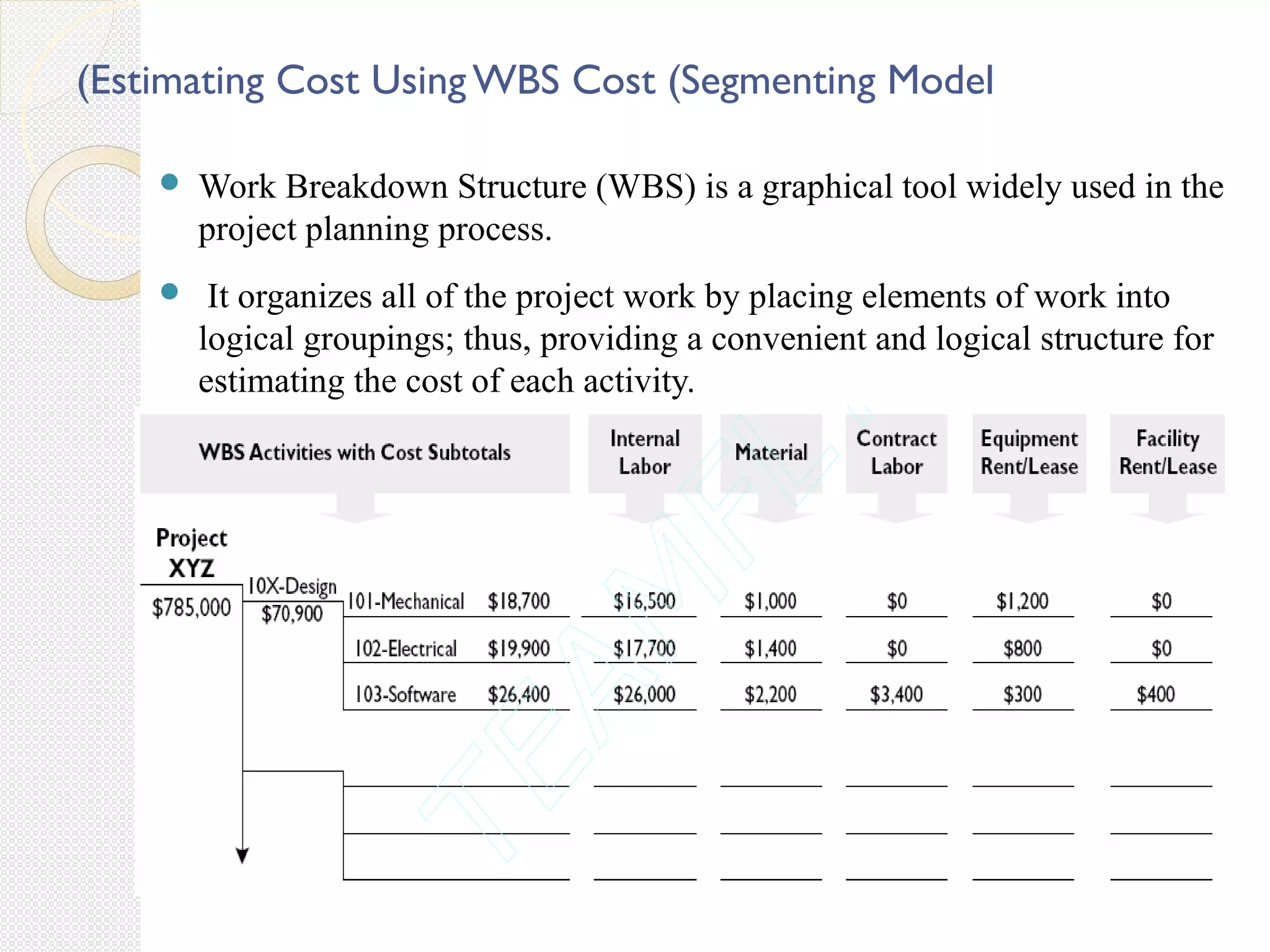

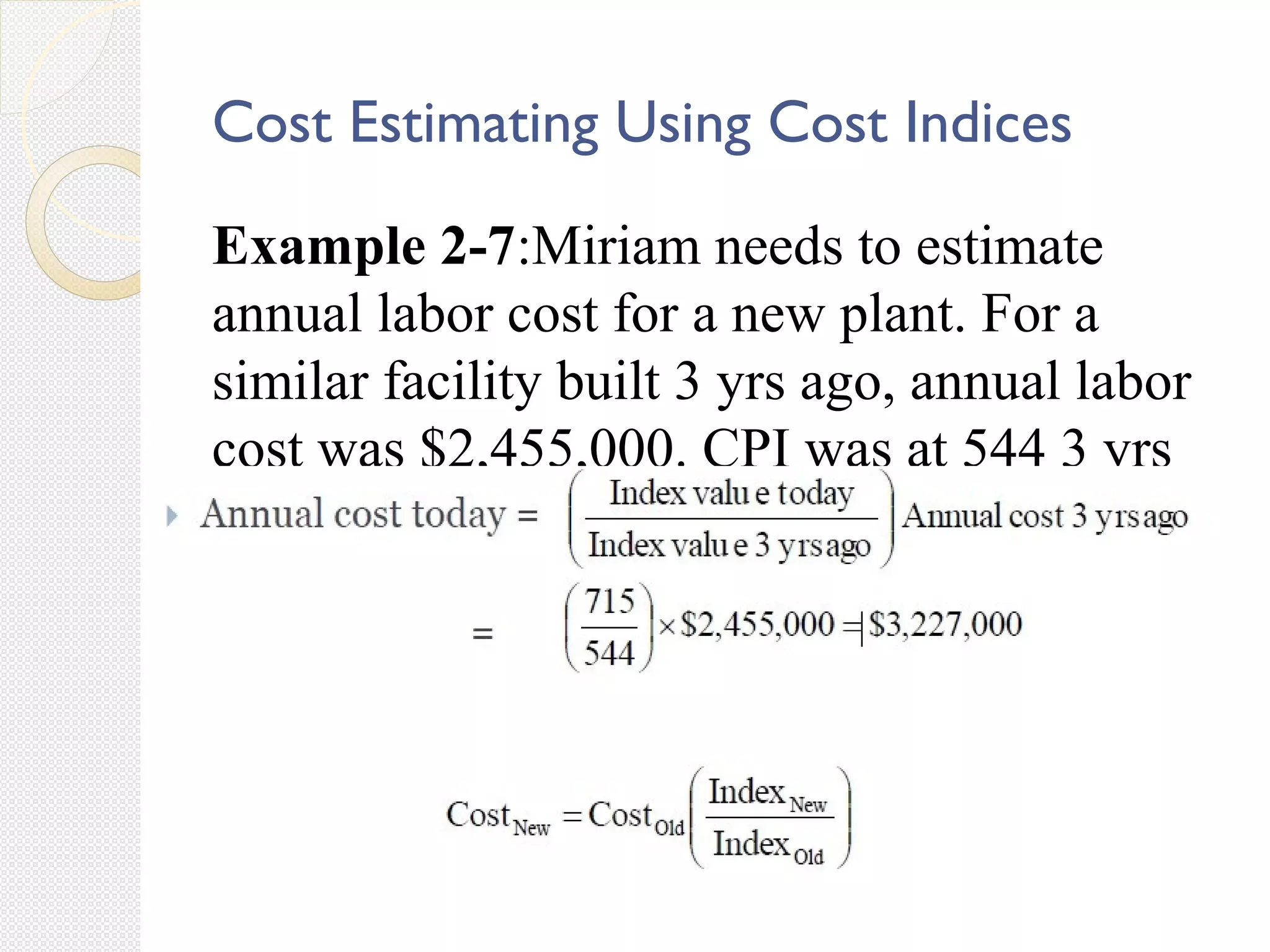

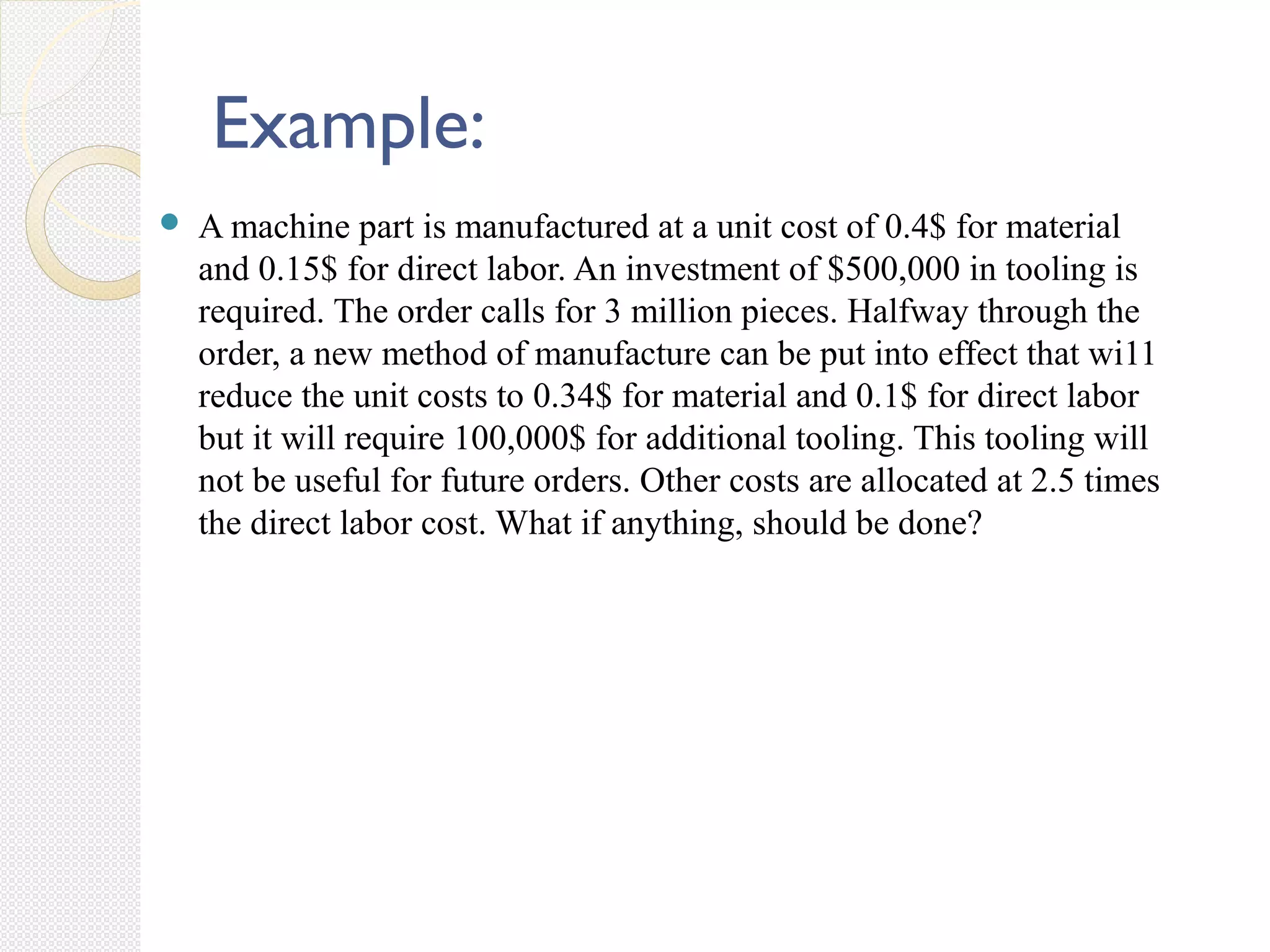

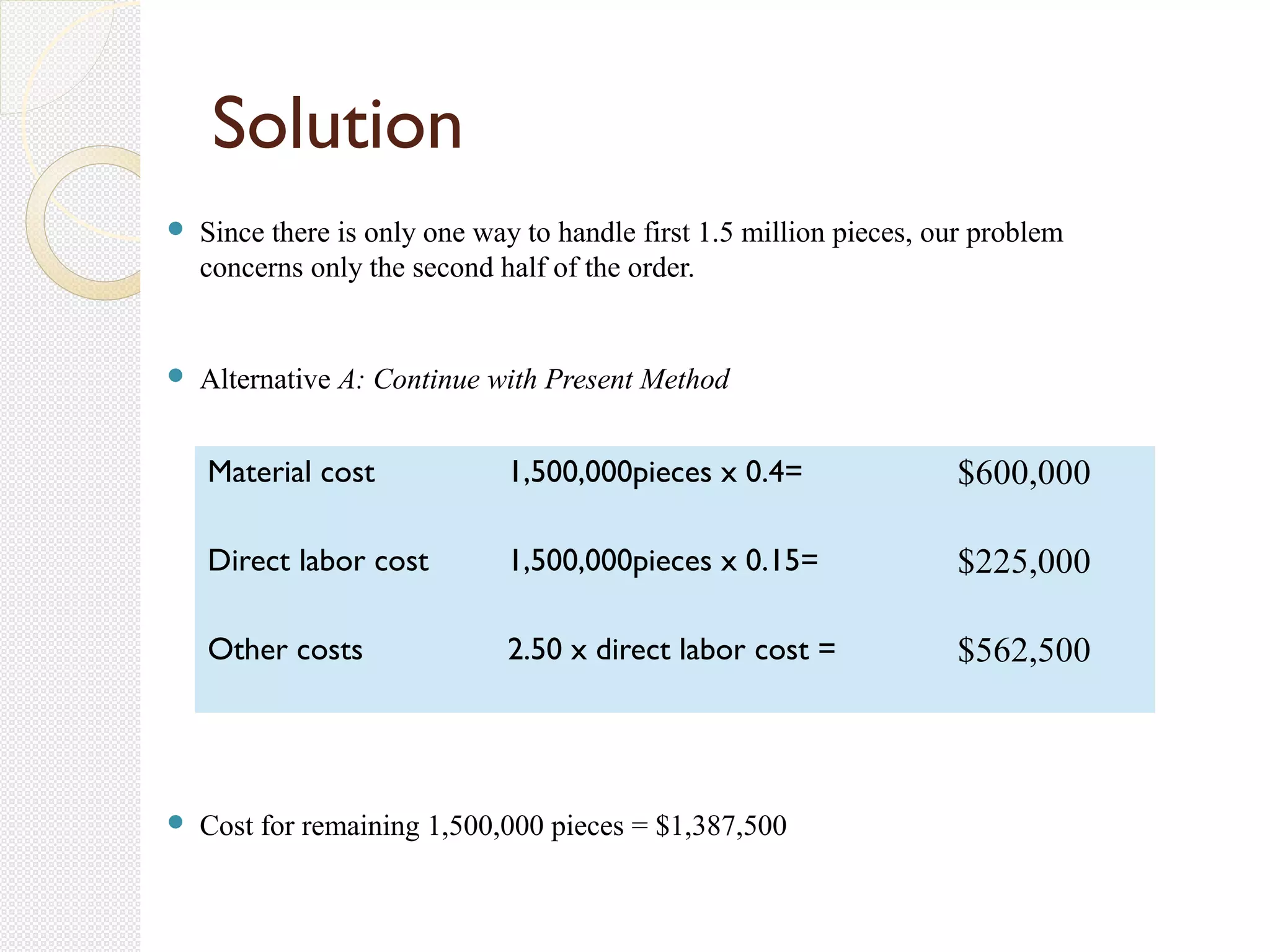

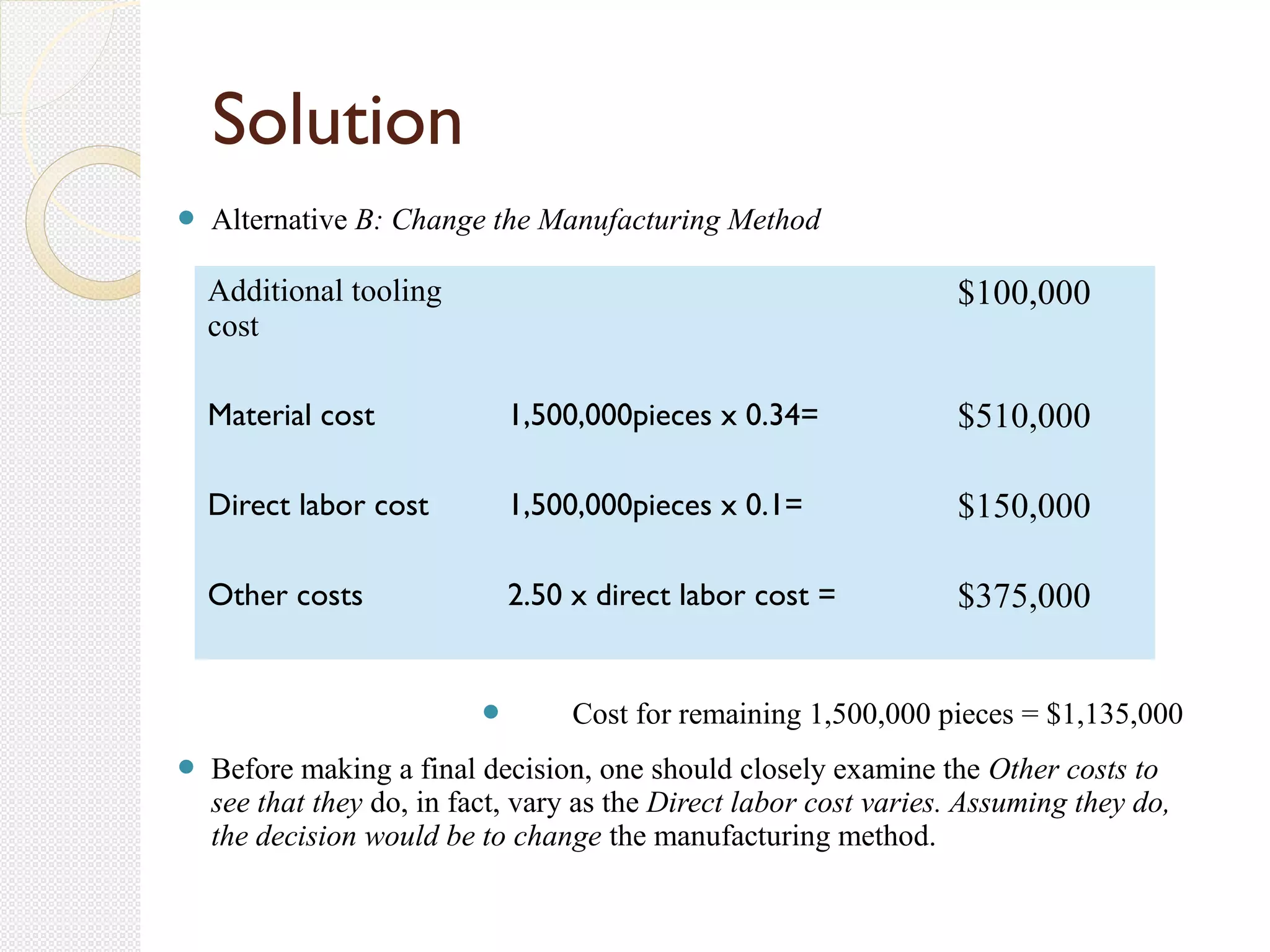

This document discusses various types of engineering costs and methods for estimating costs. It describes fixed and variable, direct and indirect, marginal and average, sunk and opportunity costs. It also discusses recurring and non-recurring costs, incremental costs, cash and book costs, and life-cycle costs. The document then explains methods for estimating costs, including using per-unit models, work breakdown structure (WBS) models, and cost indices. It provides examples to illustrate key cost concepts.