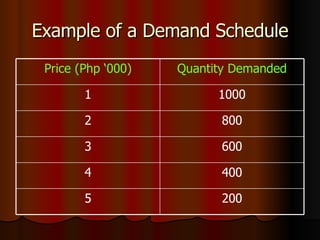

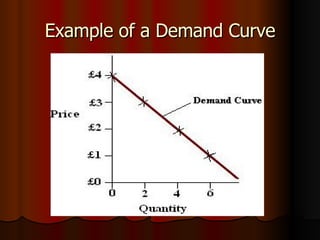

The document discusses the economic concepts of demand, supply, and market equilibrium. It defines demand as the quantity of a good or service consumers are willing and able to purchase at a given price. The main determinants of demand are price, income, tastes and preferences, and prices of related goods. Supply is defined as the maximum quantity of a good producers can offer. The main determinants of supply are costs of inputs, technology, and government taxes/subsidies. Market equilibrium occurs when quantity demanded equals quantity supplied, resulting in a balance between the opposing forces of consumers and producers.