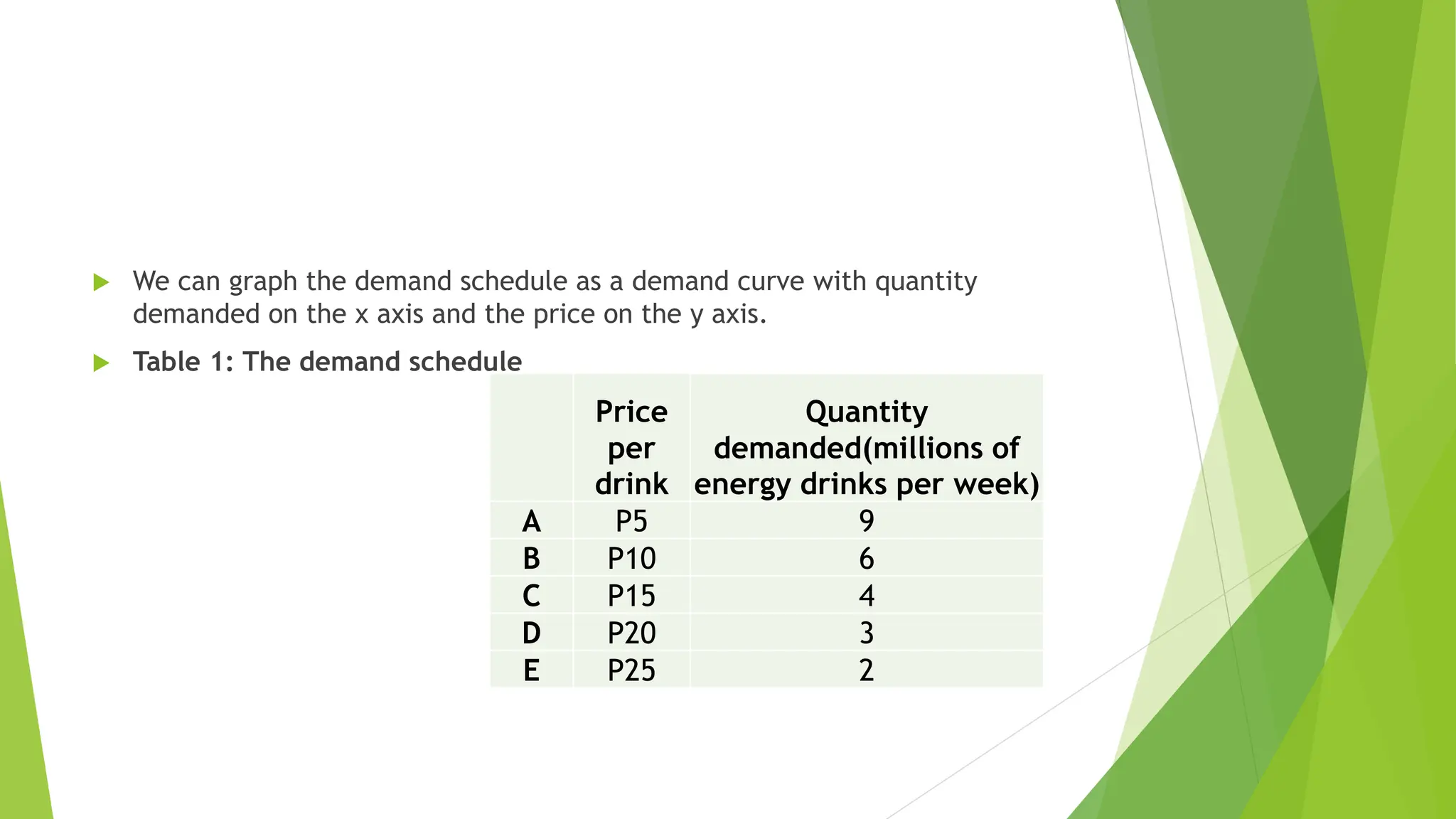

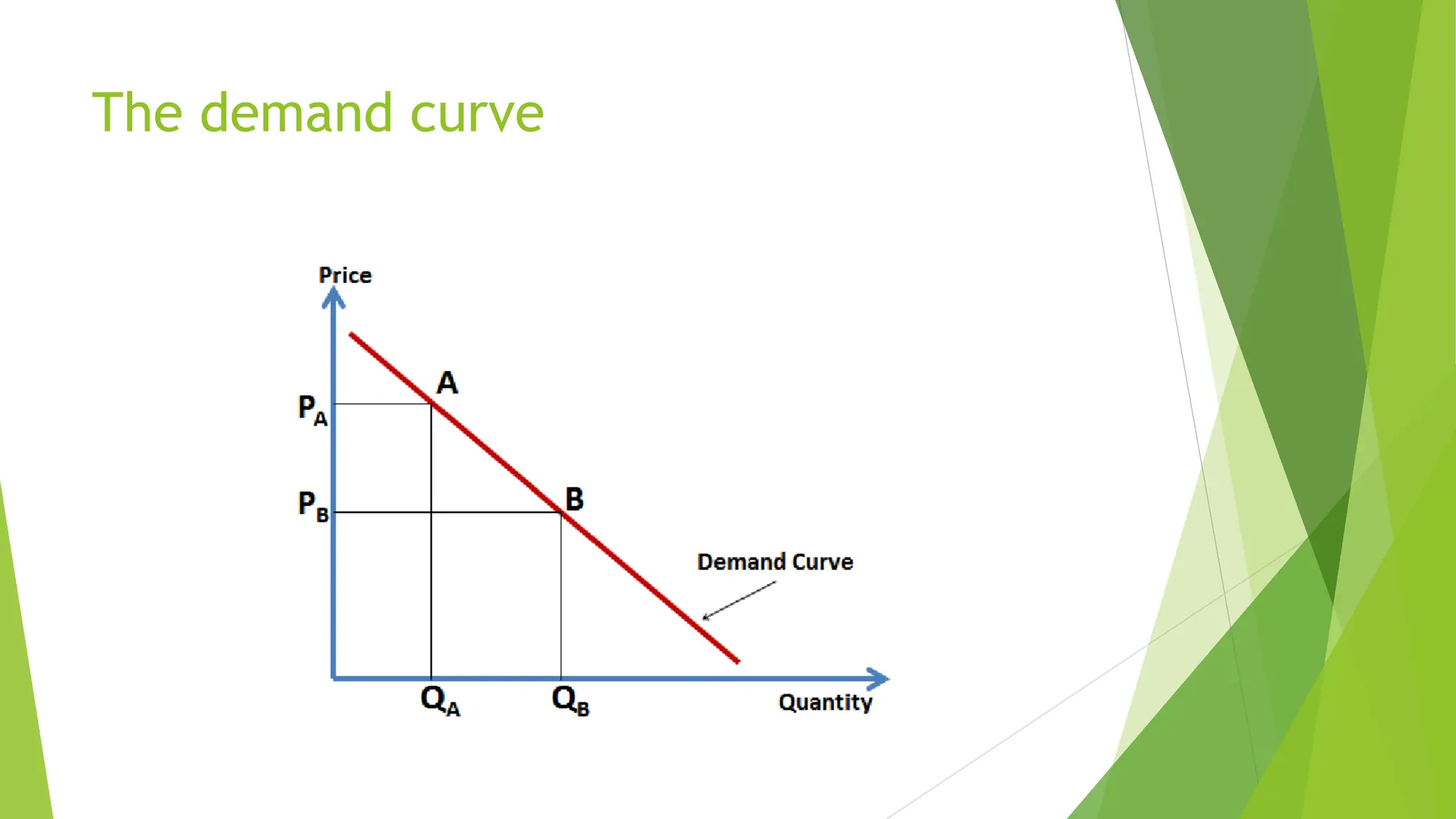

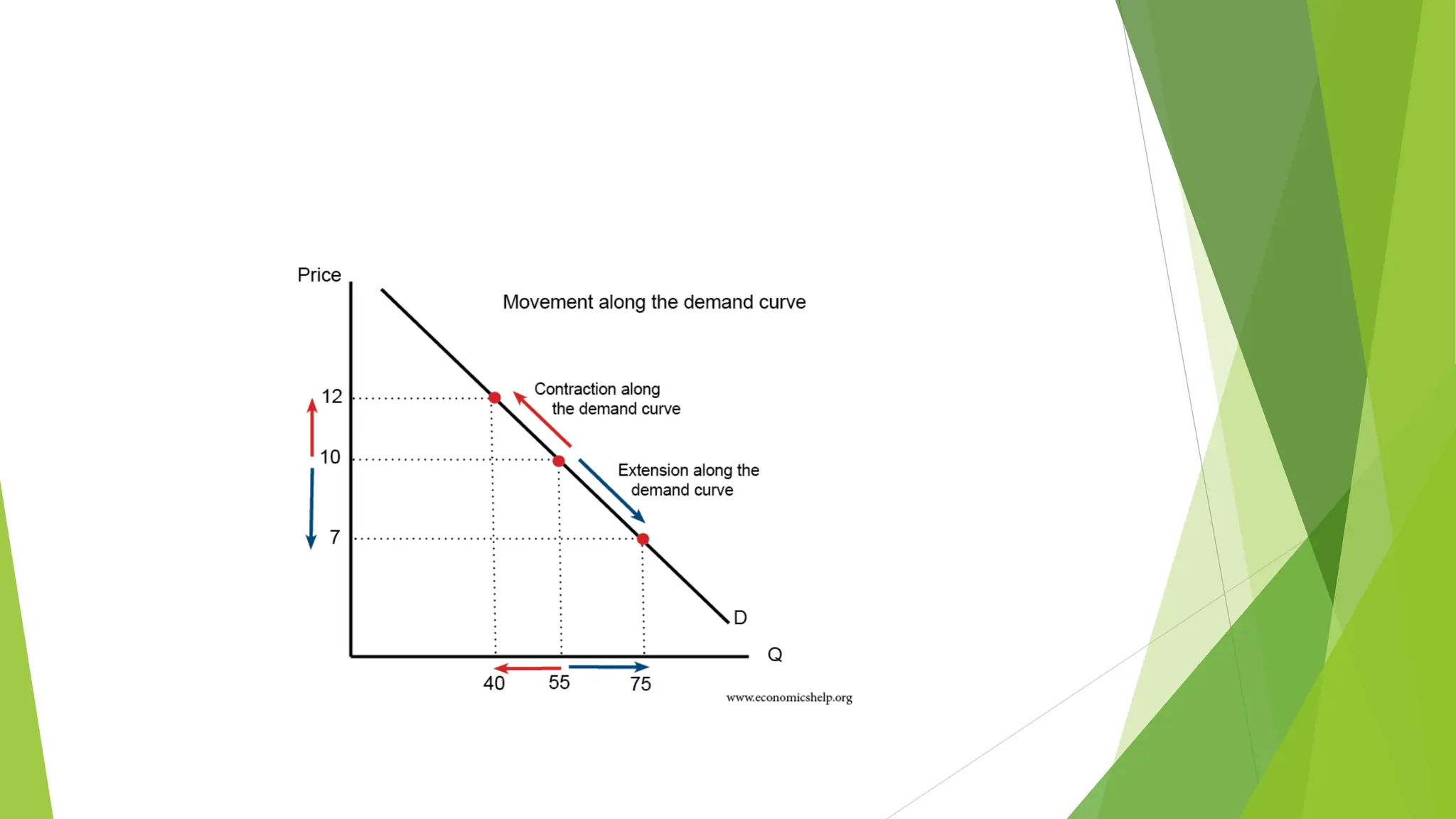

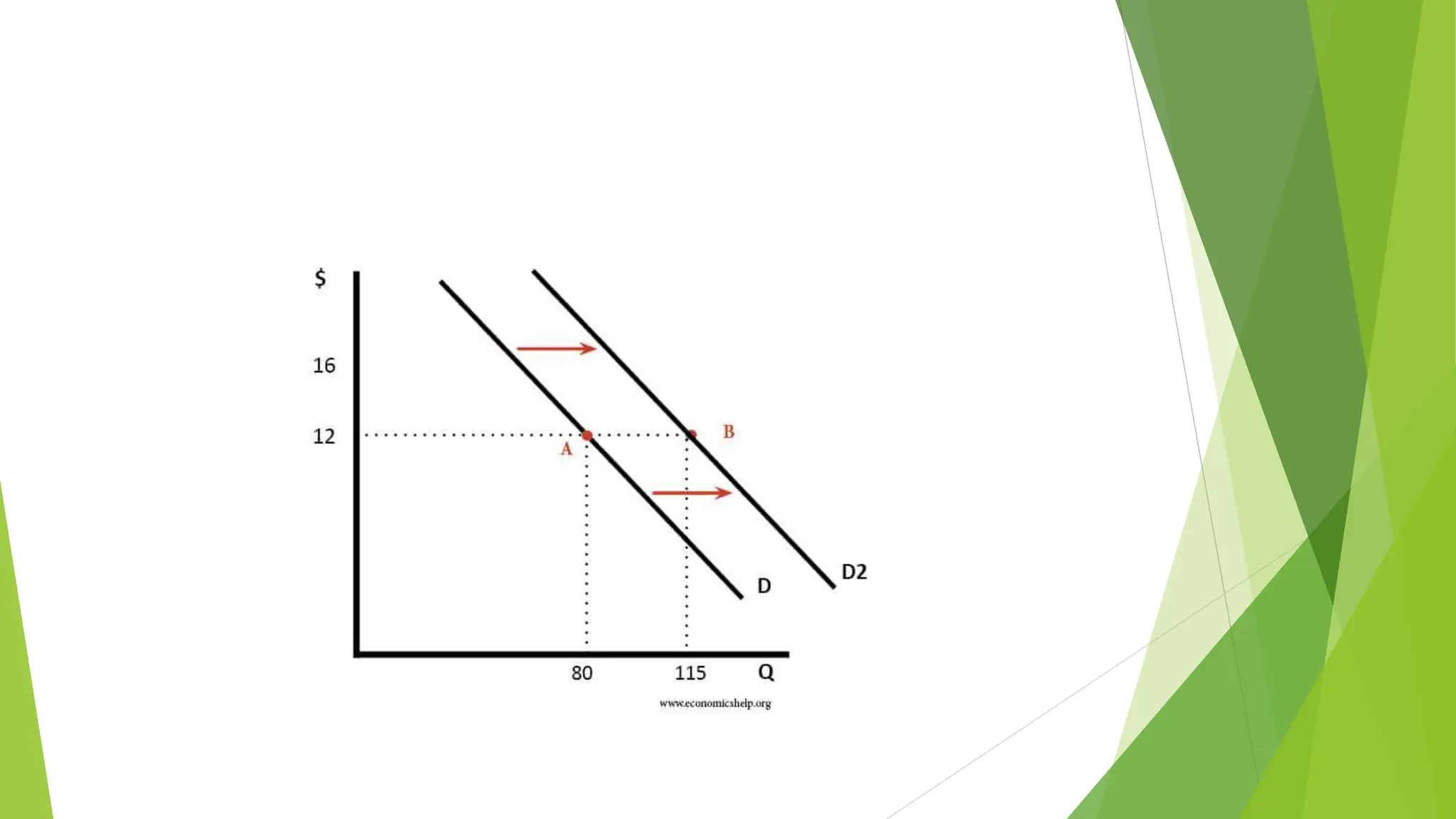

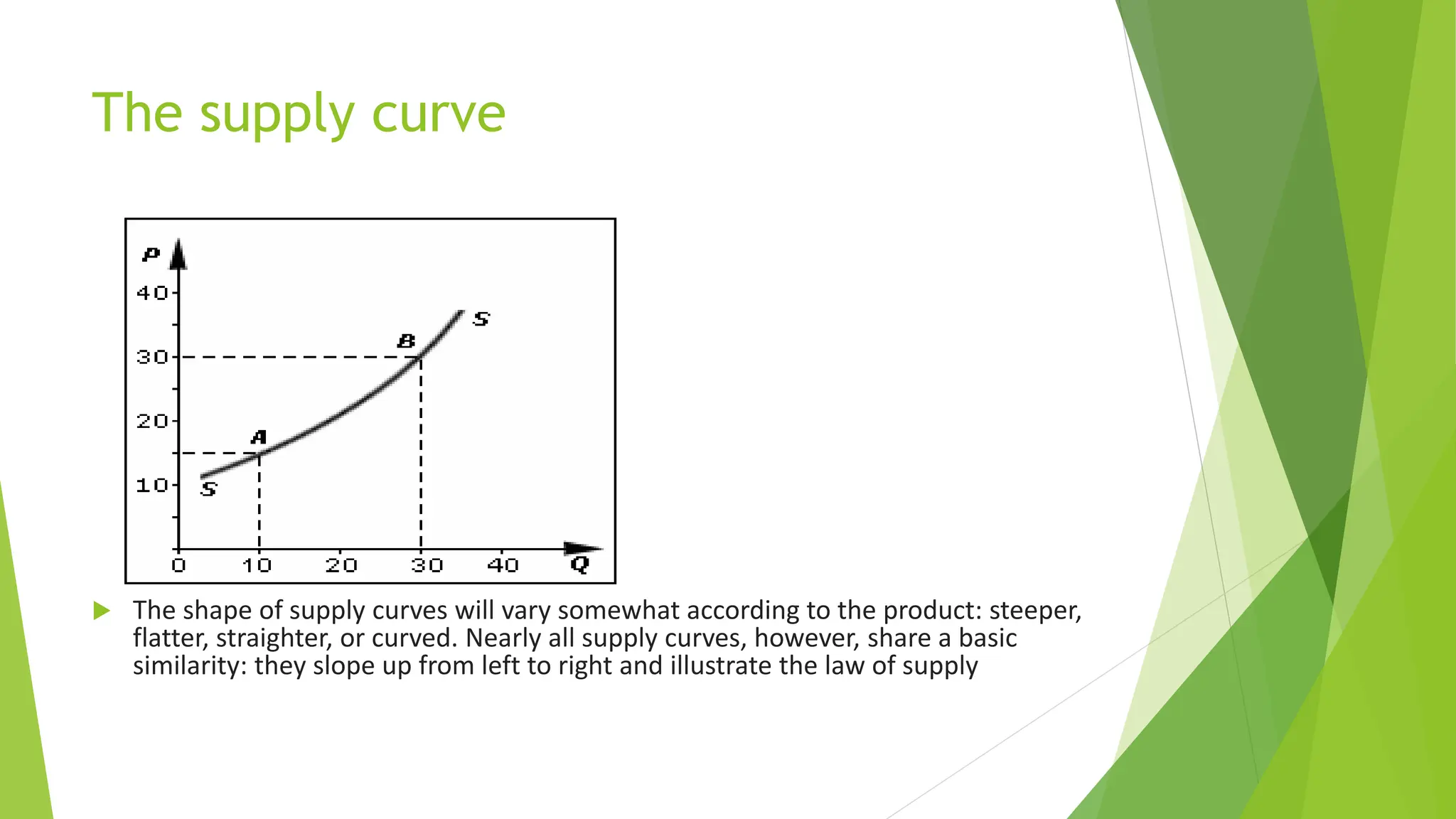

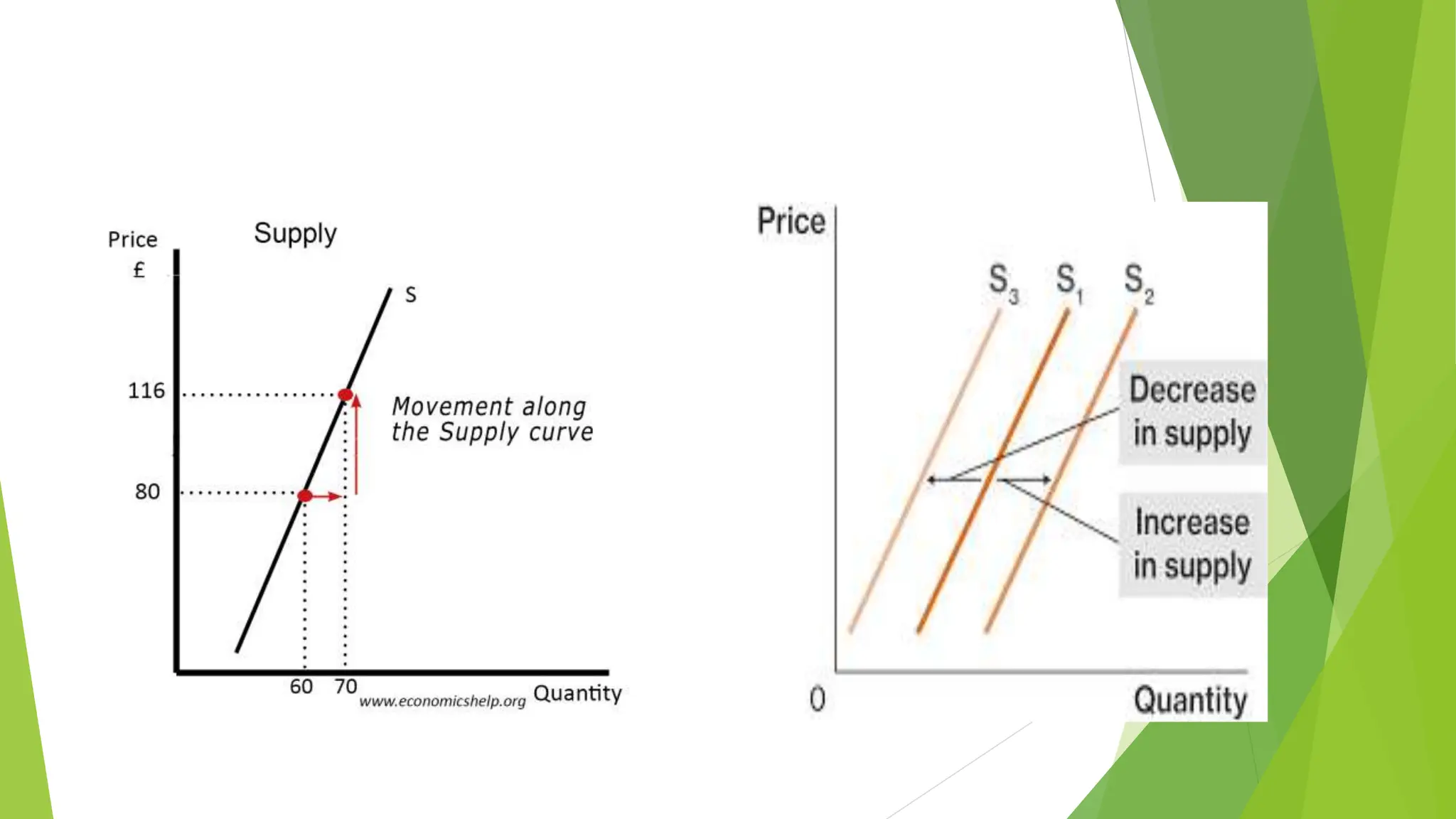

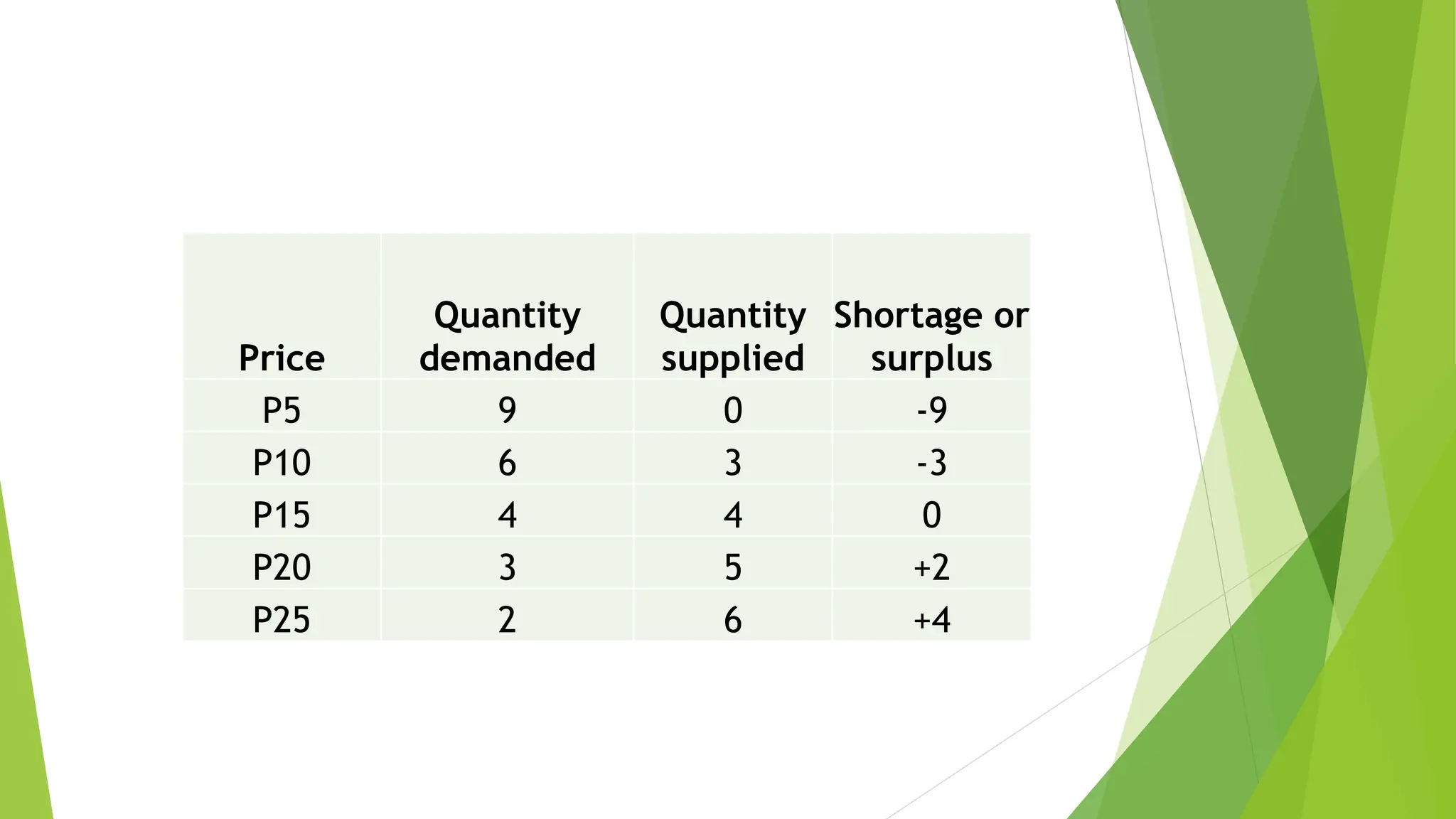

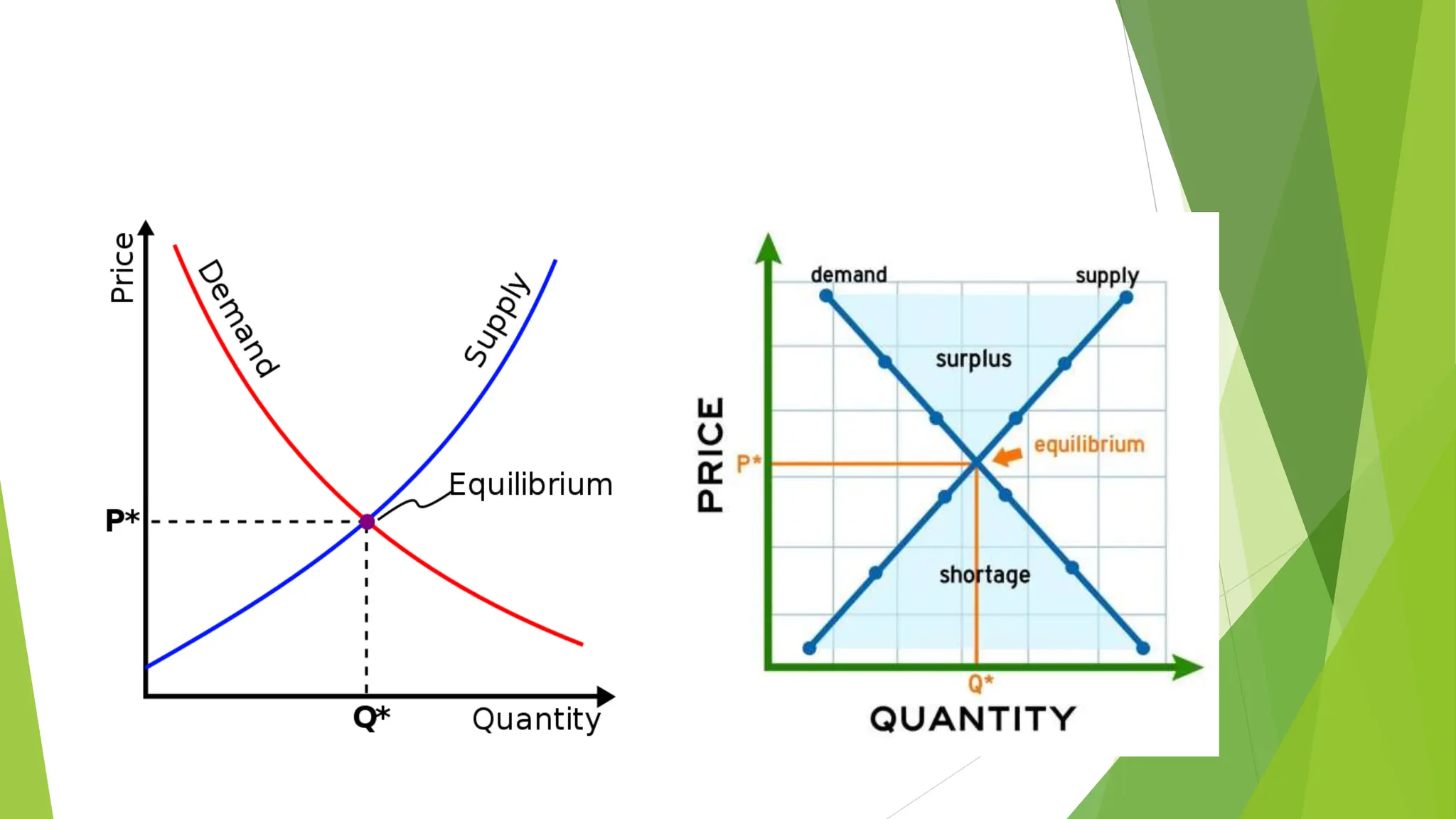

This document provides an overview of an introductory economics course. It includes 6 study units covering topics like markets, productivity, and international trade. Students will be assessed through tests, assignments, and an examination. The first study unit defines economics as studying how humans make choices in the face of scarcity. It explains that supply and demand determine what goods and services are produced and in what quantities through the interaction of buyers and sellers in a market. The document also outlines factors that shift supply and demand curves, like changes in price, income, and preferences.