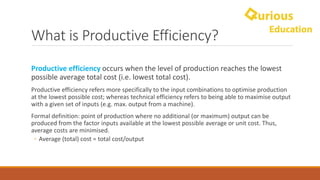

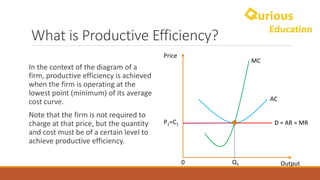

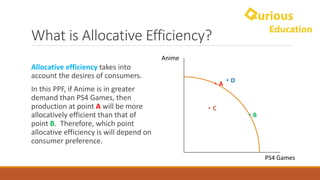

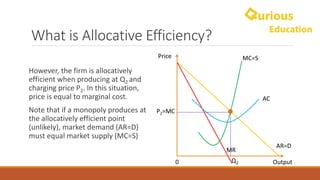

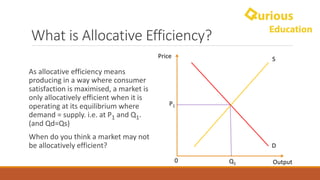

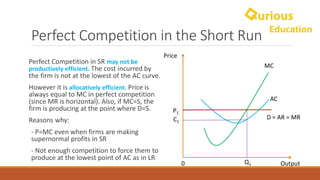

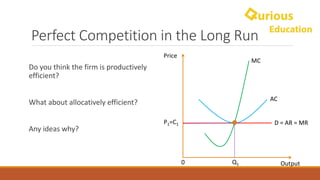

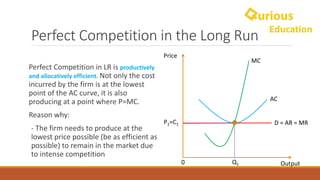

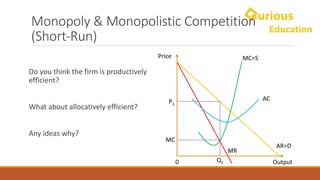

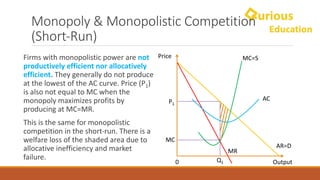

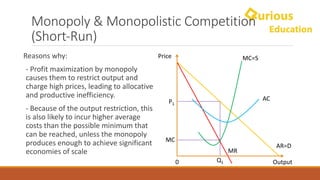

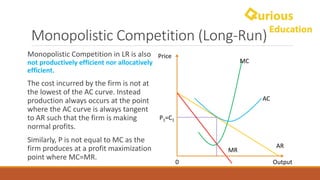

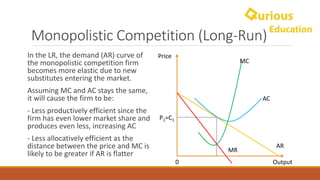

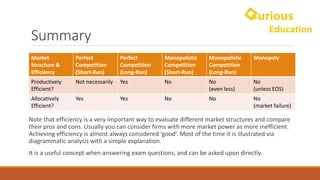

The document outlines the concepts of productive and allocative efficiency in economics, detailing their definitions, implications within various market structures (perfect competition, monopoly, and monopolistic competition), and how these efficiencies can affect consumer satisfaction and production costs. It explains that productive efficiency occurs when goods are produced at the lowest cost, while allocative efficiency is achieved when consumer demand meets supply at a price equal to marginal cost. Market failures and external factors can disrupt these efficiencies, highlighting the importance of understanding these concepts for evaluating different market structures.