This document provides an overview of microeconomics concepts including:

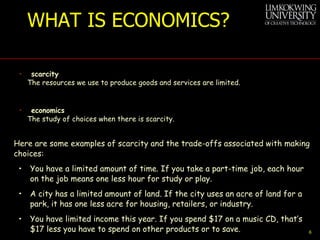

1. Economics is defined as the study of how scarce resources are allocated among alternative uses.

2. Key concepts in microeconomics include rational choice, incentives, marginal analysis, and opportunity cost.

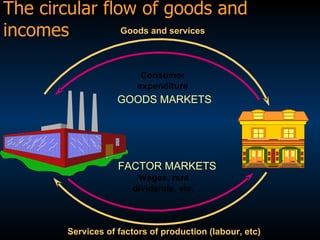

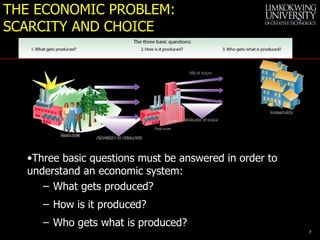

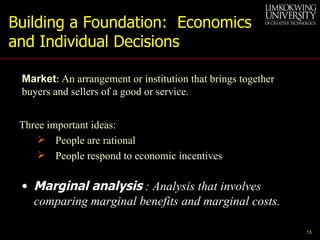

3. Economic systems must answer questions about what to produce, how to produce it, and who receives it given the constraints of scarce resources.

![LECTURE 1 BASIC CONCEPTS OF ECONOMICS Shan Faculty of Business Management & Globalization Limkokwing Executive Leadership College [email_address] Tel: +603 - 8317 8833 (ext. 8407) BECON1201: Microeconomics MICROECONOMICS](https://image.slidesharecdn.com/lecture1-basiceconomicconcepts1-090930053723-phpapp01/85/Lecture1-Basic-Economic-Concepts-1-1-320.jpg)

![LECTURE 1 BASIC CONCEPTS OF ECONOMICS Shan Faculty of Business Management & Globalization Limkokwing Executive Leadership College [email_address] Tel: +603 - 8317 8833 (ext. 8407) BECON1201: Microeconomics MICROECONOMICS](https://image.slidesharecdn.com/lecture1-basiceconomicconcepts1-090930053723-phpapp01/75/Lecture1-Basic-Economic-Concepts-1-1-2048.jpg)

![Economics as Social Science Need for integration of social sciences deductive, historical and empirical [statistical] approaches Philosophical and Historical Context To speculate about where you are going, you need to understand where you are To fully understand where you are, you need to know where you came from](https://image.slidesharecdn.com/lecture1-basiceconomicconcepts1-090930053723-phpapp01/85/Lecture1-Basic-Economic-Concepts-1-4-320.jpg)

![ECONOMIC SYSTEMS laissez-faire economy (free market) Literally from the French: “allow [them] to do.” An economy in which individual people and firms pursue their own self-interests without any central direction or regulation. market The institution through which buyers and sellers interact and engage in exchange. Some markets are simple and others are complex, but they all involve buyers and sellers engaging in exchange. The behavior of buyers and sellers in a laissez-faire economy determines what gets produced, how it is produced, and who gets it.](https://image.slidesharecdn.com/lecture1-basiceconomicconcepts1-090930053723-phpapp01/85/Lecture1-Basic-Economic-Concepts-1-28-320.jpg)