Downloaded 11 times

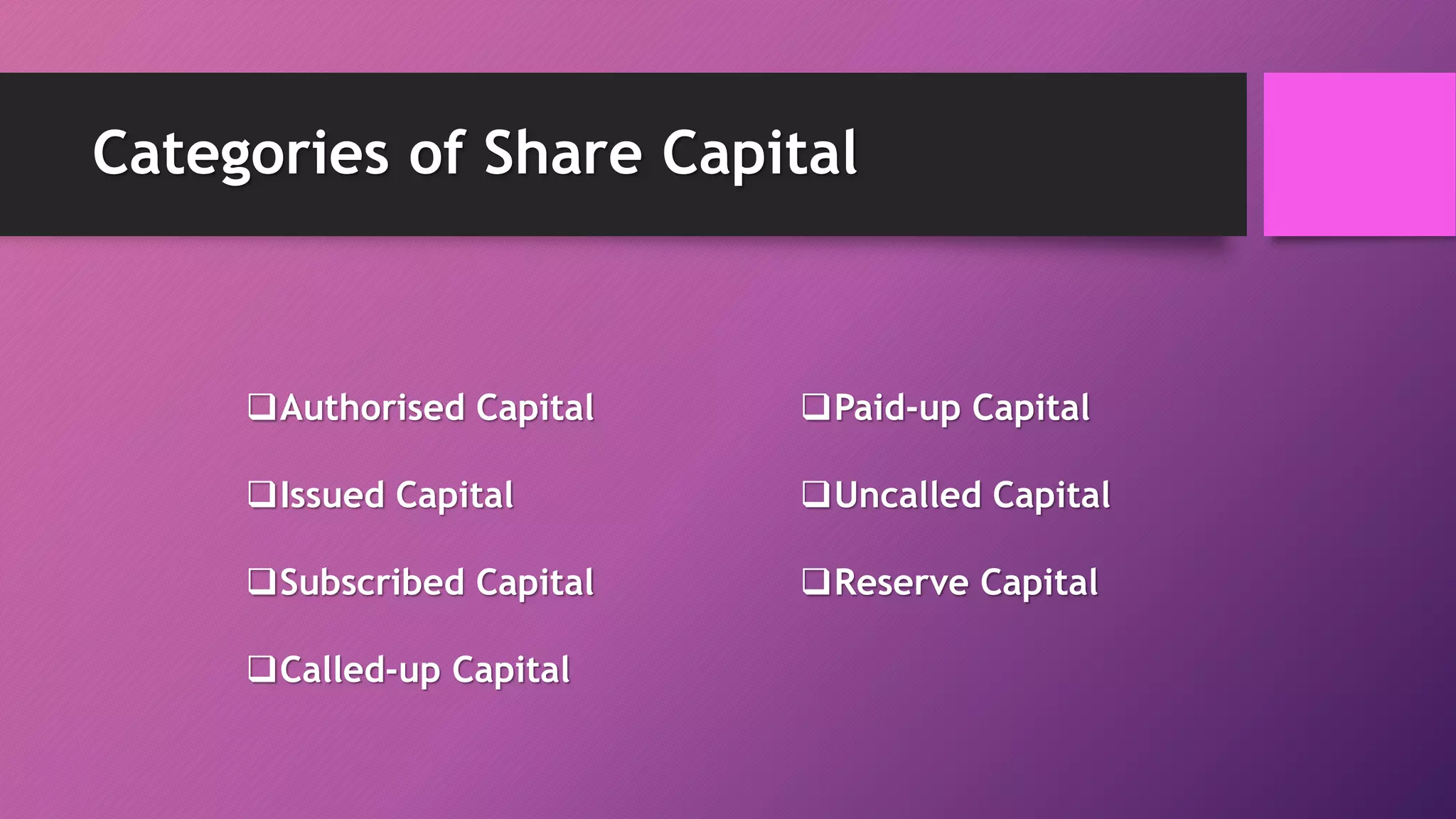

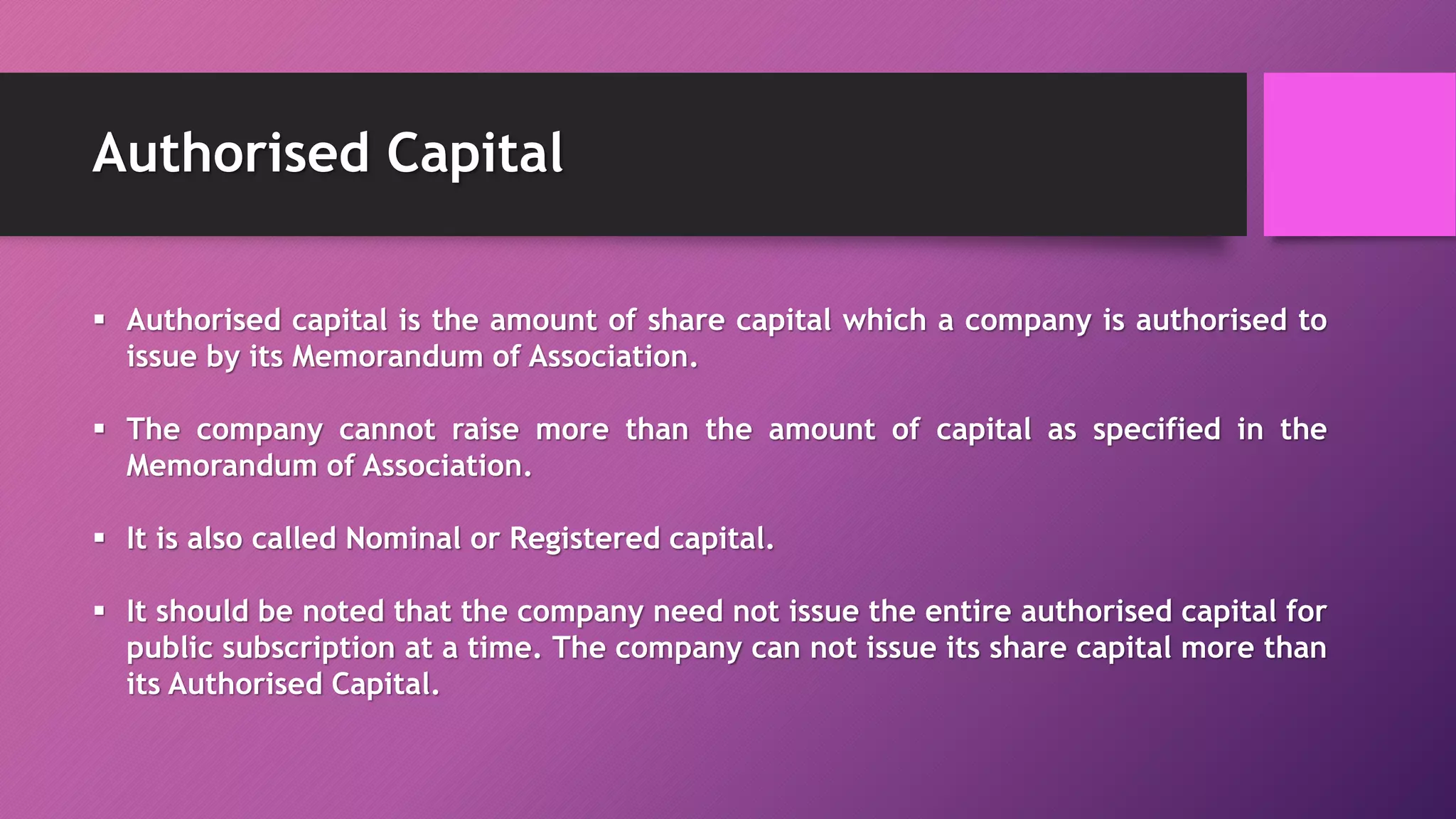

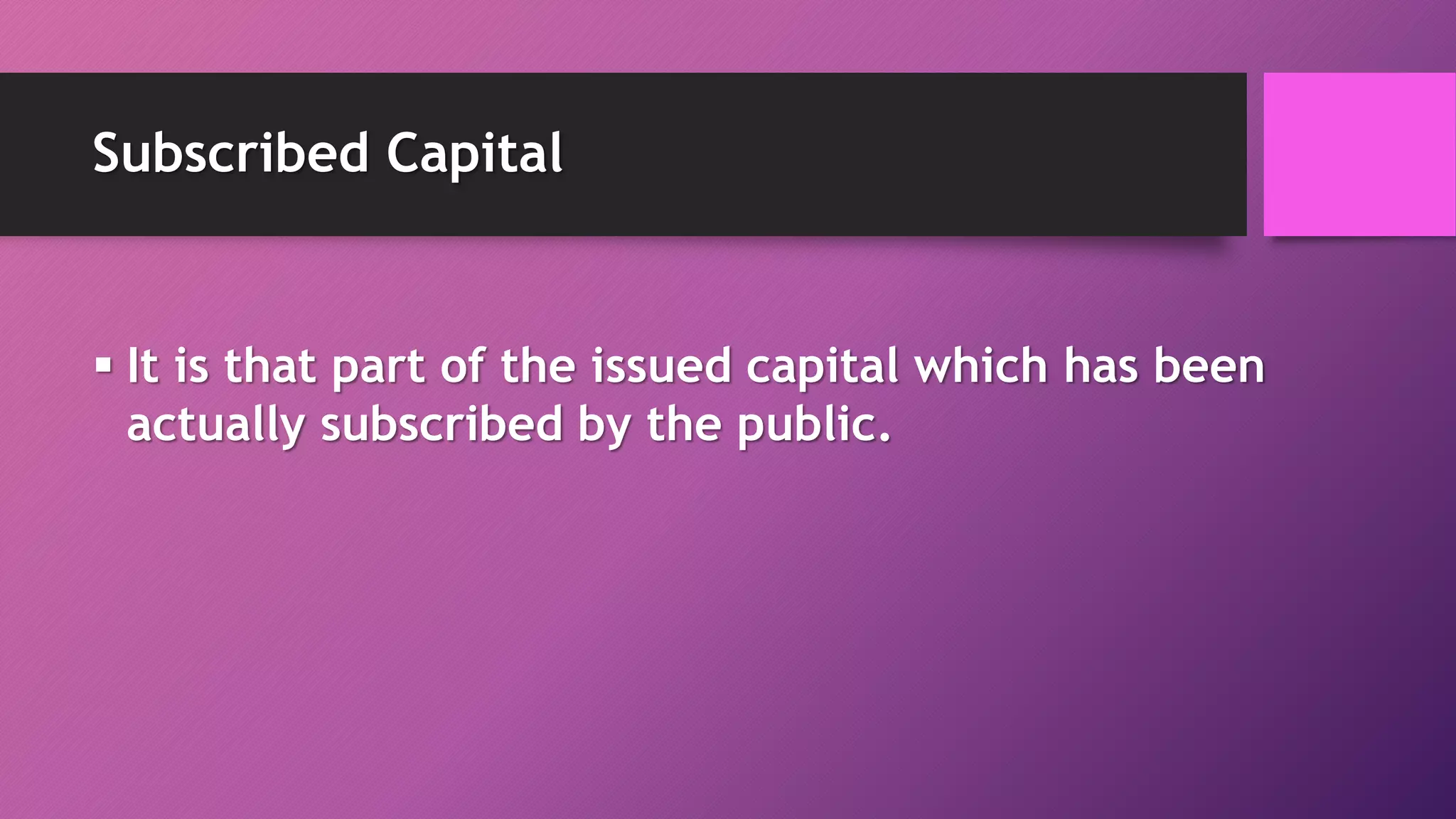

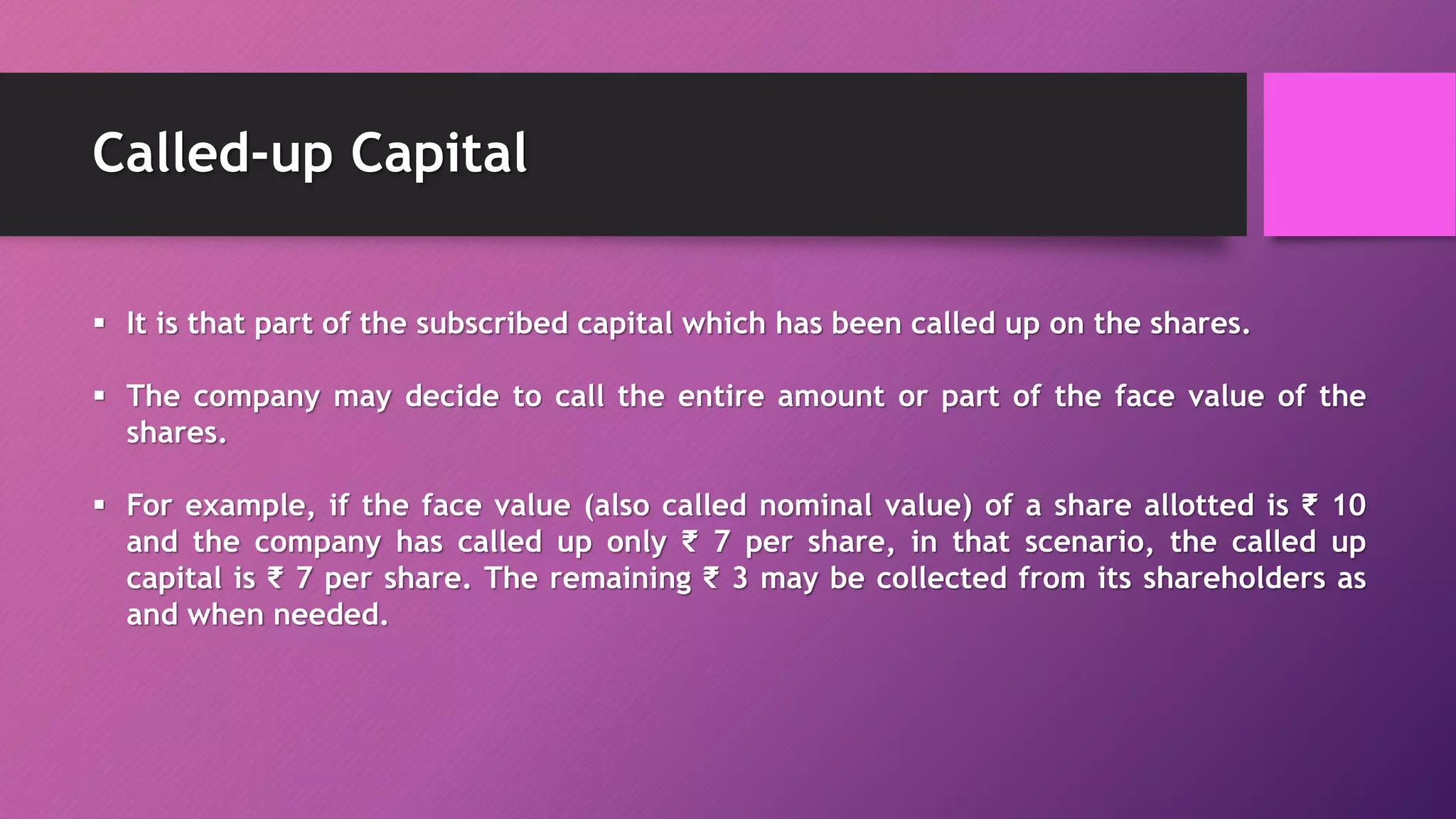

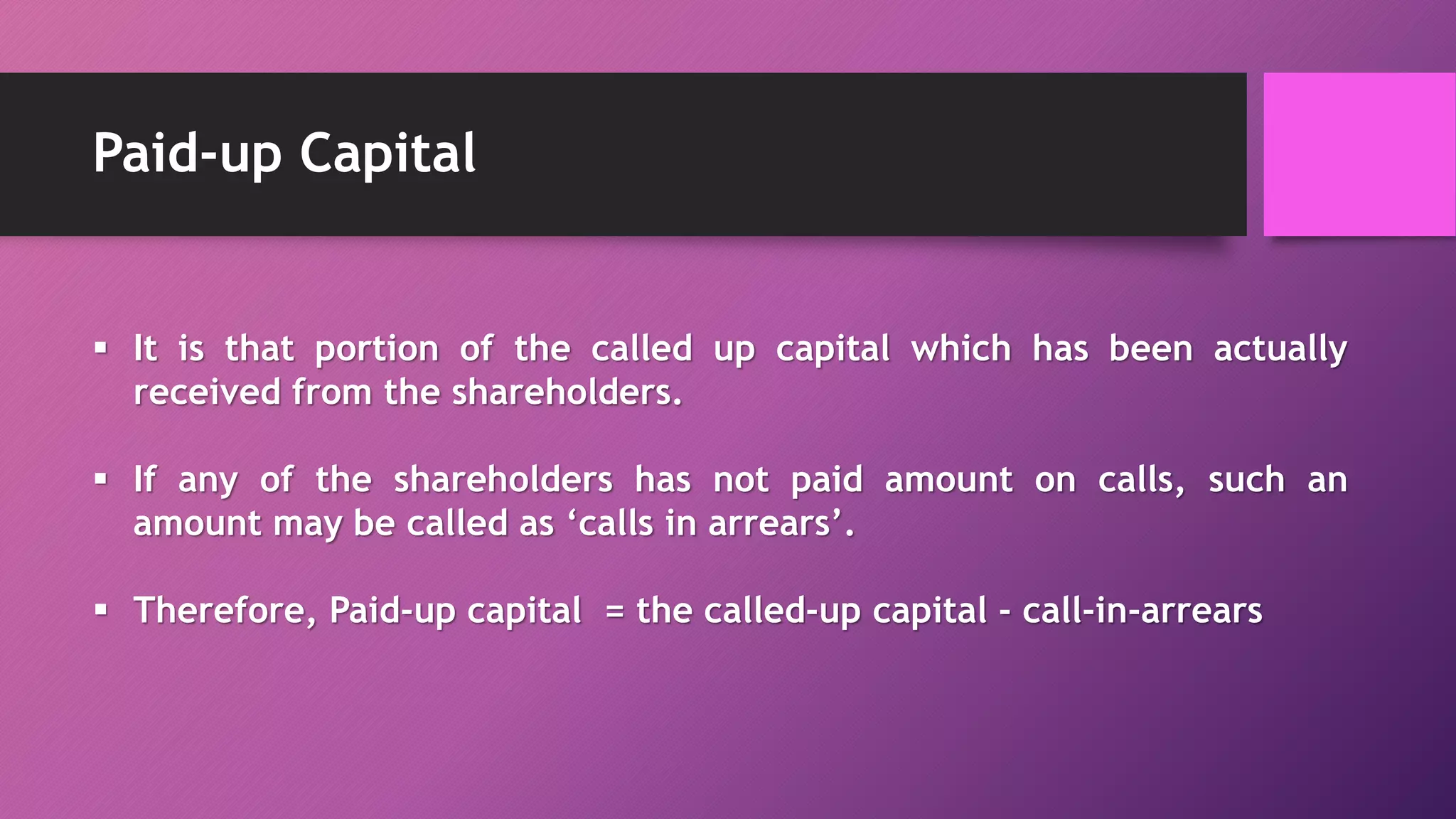

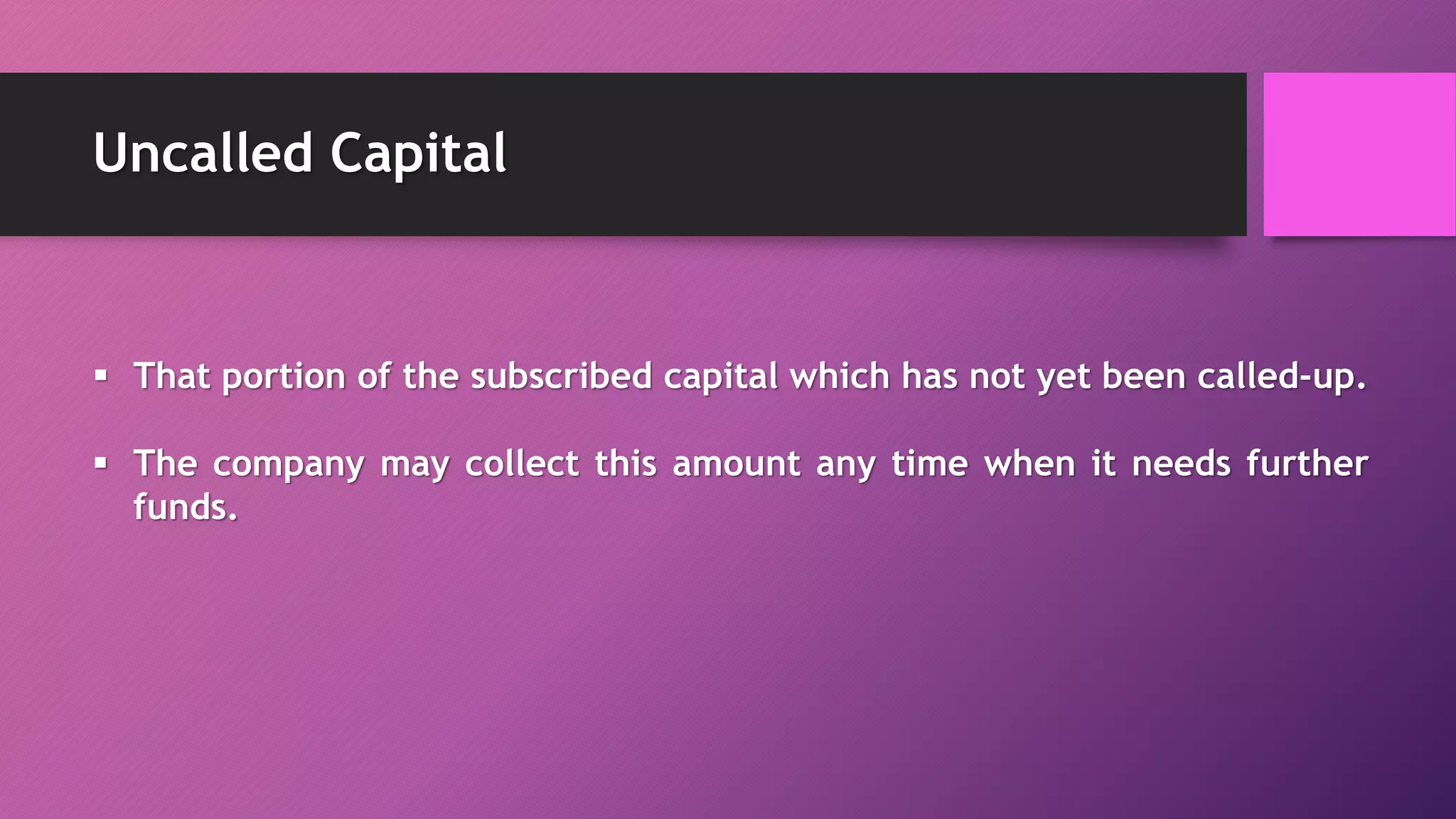

This document defines and explains the different types of share capital for a company. There are 7 main categories: Authorised capital is the maximum amount of share capital a company can issue as specified in its constitution. Issued capital is the part of authorised capital offered to the public. Subscribed capital is the part of issued capital that is subscribed to by the public. Called-up capital is the part of subscribed capital that shareholders are required to pay. Paid-up capital is the portion of the called-up capital that has actually been received. Uncalled capital is the portion of subscribed capital not yet called up. Reserve capital refers to a portion of uncalled capital reserved only to be called in the event of winding up the