This chapter discusses country risk analysis for multinational corporations. It identifies political and financial risk factors that MNCs consider when evaluating country risk. Techniques for assessing country risk include checklist approaches, the Delphi method, and quantitative analysis. Country risk ratings influence MNC decisions about new investments, monitoring existing operations, and strategies to reduce government takeover exposure in host countries.

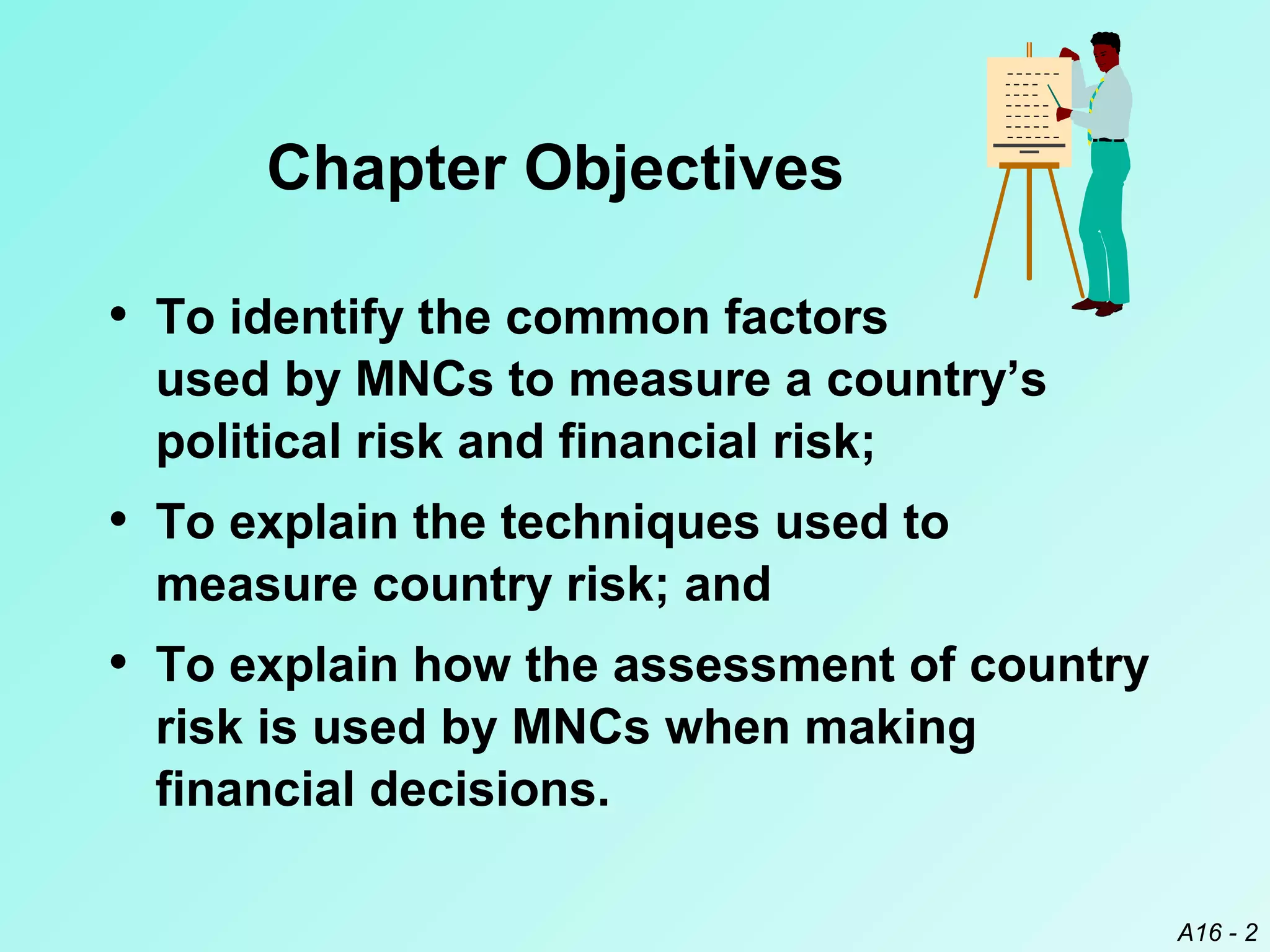

![Impact of Country Risk on an MNC’s Value

Exposure of Foreign Projects

to Country Risks

m

n ∑

[

E ( CFj , t ) × E (ER j , t ) ]

j =1

Value = ∑

t =1 (1 + k ) t

E (CFj,t ) = expected cash flows in

currency j to be received by the U.S. parent at the

end of period t

E (ERj,t ) = expected exchange rate at

which currency j can be converted to dollars at

A16 - 28](https://image.slidesharecdn.com/countryriskanalysis-130401120932-phpapp01/75/Country-risk-analysis-28-2048.jpg)