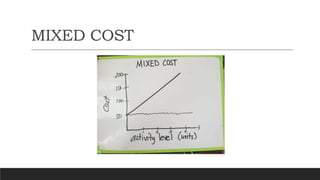

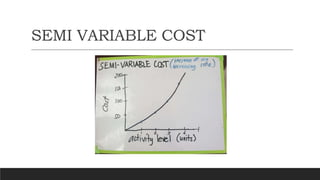

This document discusses different types of cost behavior and methods for analyzing mixed costs. It describes variable costs, fixed costs, and semi-variable costs. Several methods are presented for separating mixed costs into variable and fixed components, including account analysis, industrial engineering, conference methods, high-low analysis, regression analysis, and scattergraph analysis. Each method has strengths and weaknesses for estimating cost functions based on factors like objectivity, use of data points, and complexity.