Downloaded 11 times

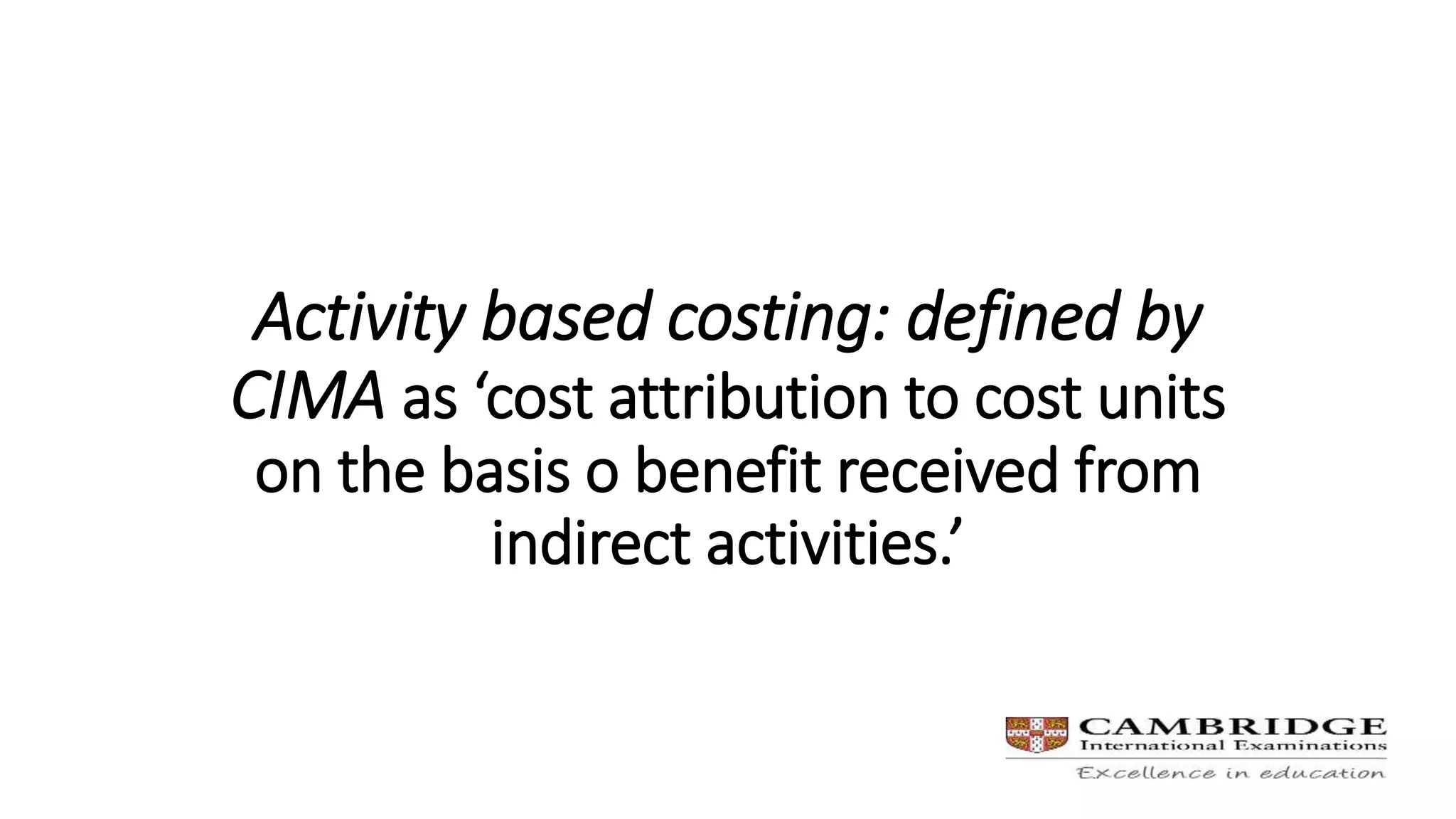

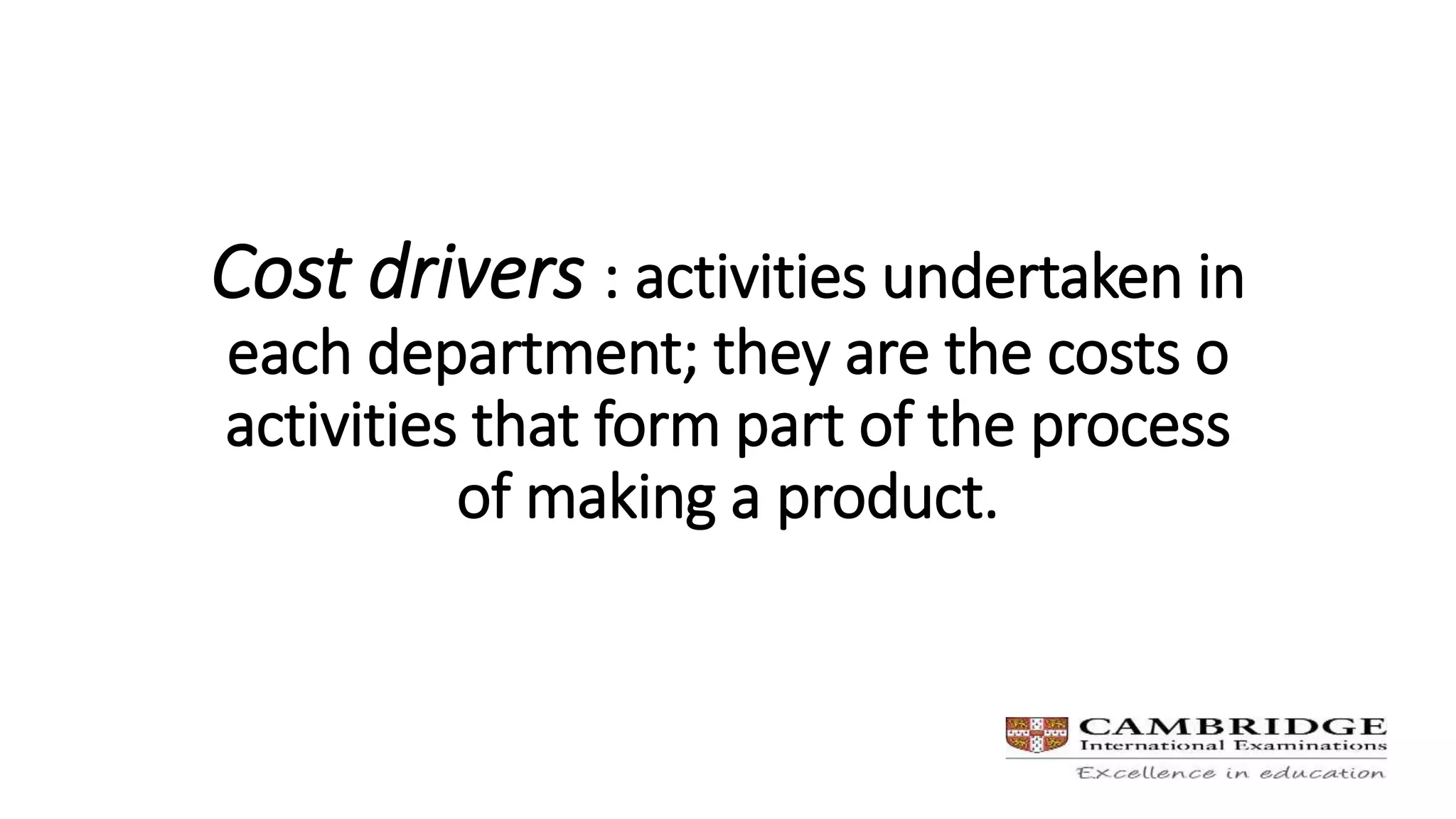

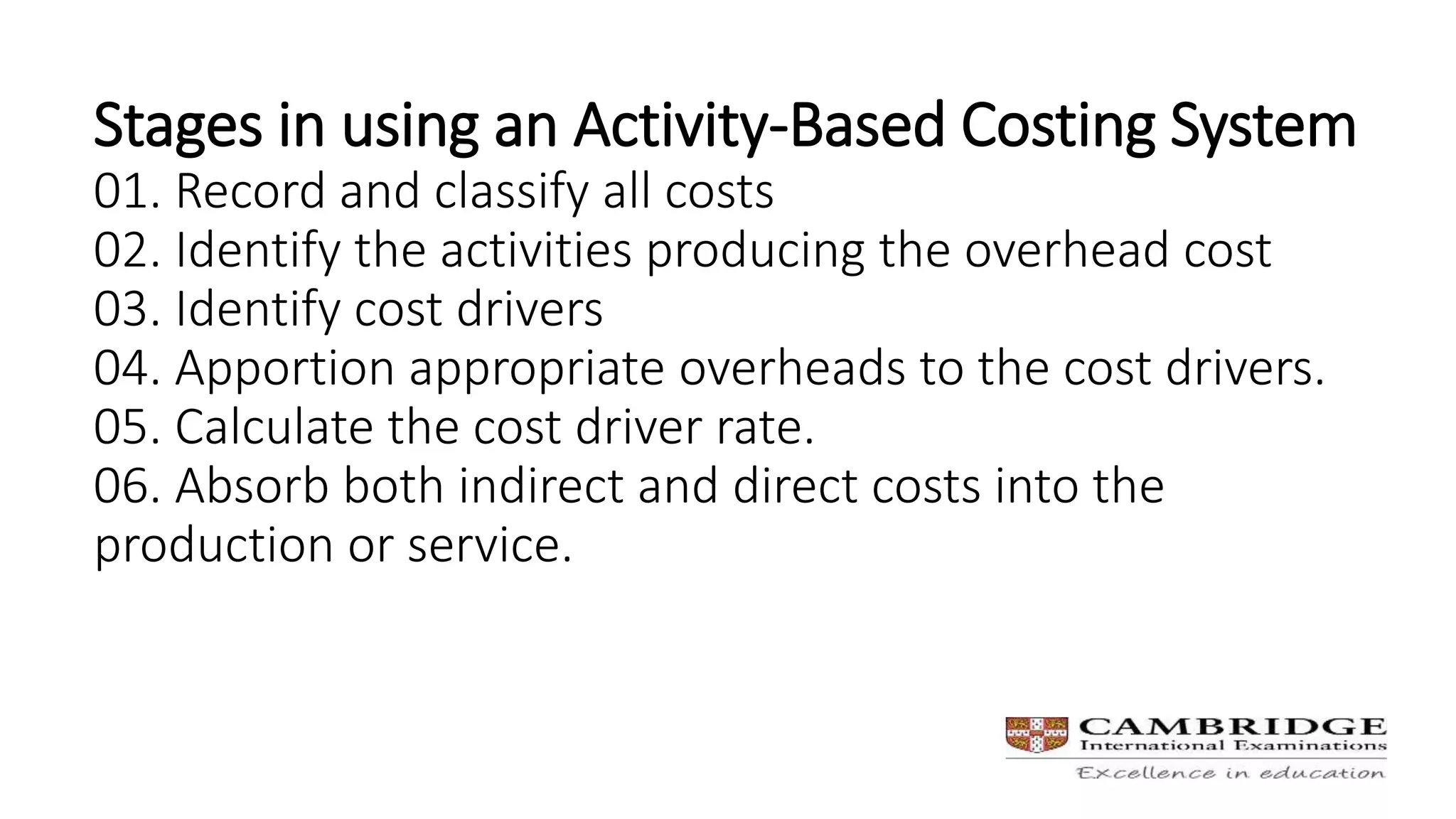

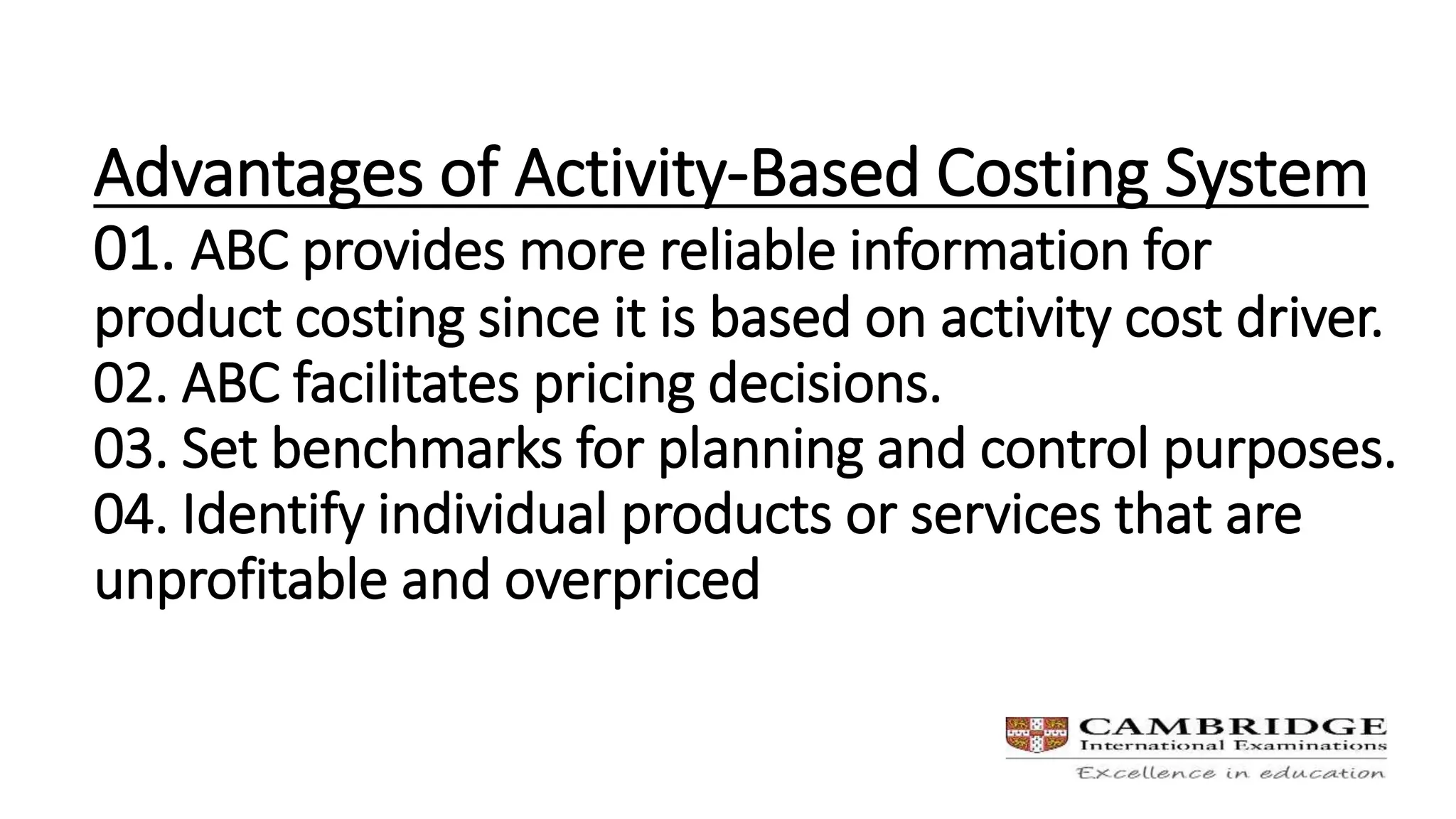

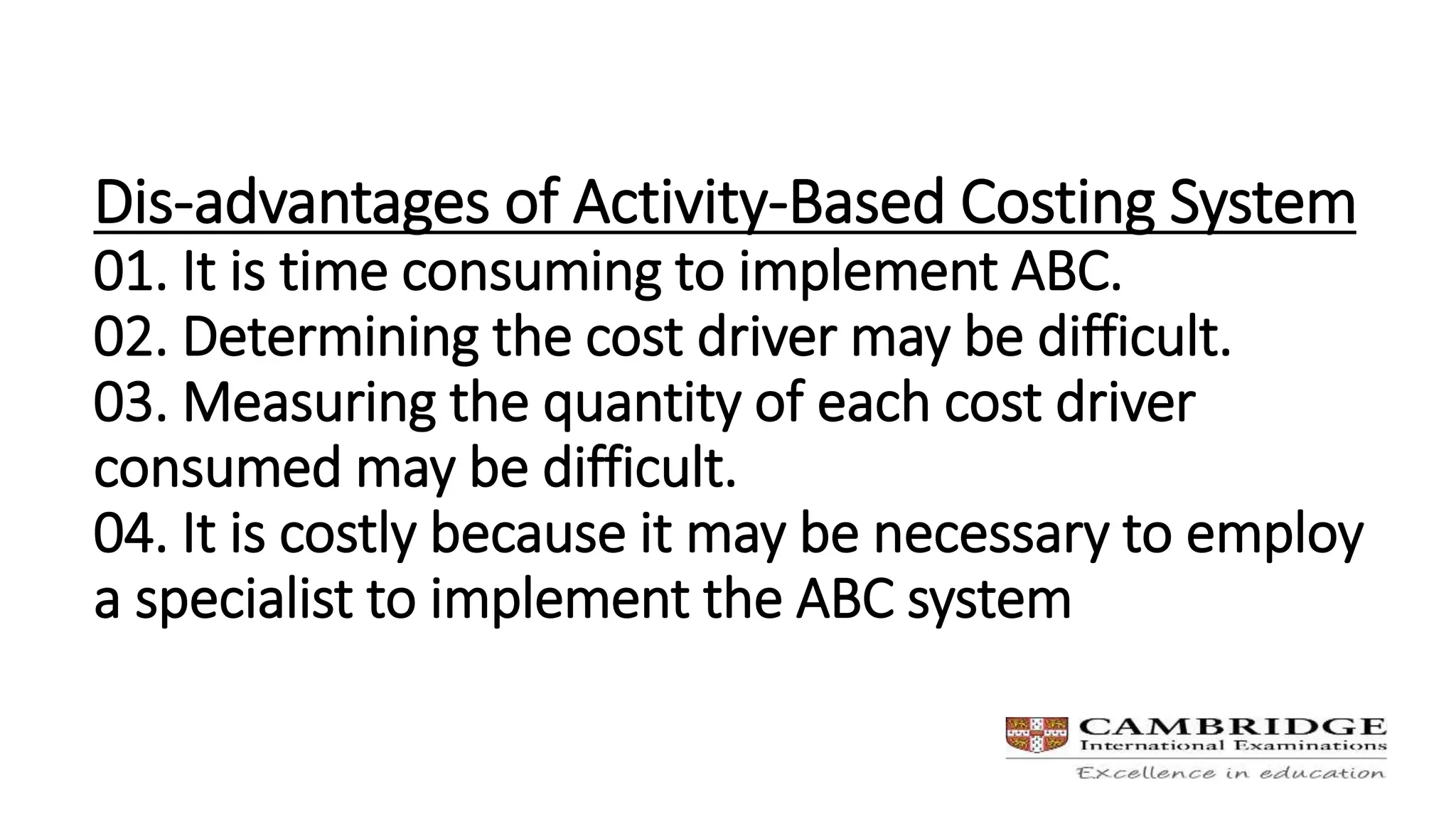

The document discusses Activity-Based Costing (ABC), defining it as the allocation of costs to cost units based on benefits received from indirect activities. It outlines stages for implementing an ABC system, including recording costs, identifying activities and cost drivers, and apportioning overheads. The advantages of ABC include more reliable product costing and better pricing decisions, while disadvantages include its complexity and potential costs.