This document provides an introduction to control accounts in financial accounting. It defines key terms like ledgers, explains the main purposes of control accounts to verify subsidiary ledger balances and locate errors. It also discusses how control accounts relate to the double entry system and provides examples of common control account types like the sales ledger control account and purchases ledger control account. Sample control account transactions and solutions to practice questions are presented to illustrate the application of control account principles.

Objectives

By the endof this unit, you should be able to:

Define key terms such as ledger, sales ledger, purchases ledger

and control account

Explain the main purposes of a control account

Explain how control accounts relate to the double entry system

Accurately prepare sales and purchases ledger control accounts

Apply control accounts principles to general ledger accounts

3.

What is aledger?

A ledger records financial transactions from journals as

debits and credits

It holds account information that is needed to prepare

financial statements

Three main types of ledgers:

Sales ledger

Purchases ledger

General ledger

4.

Types of ledgers(cont’d)

Sales Ledger

A subsidiary ledger in which the personal accounts of

credit customers (debtors) are kept

The balance of a customer’s account shows the amount

that the customer owes the business

Therefore, the total of balances in the sales ledger is the

total owed by credit customers (accounts receivable)

5.

Types of ledgers(cont’d)

Purchases Ledger

A subsidiary ledger in which the personal accounts of

credit suppliers (creditors) are kept

The balance of a supplier’s account shows the amount

that the business owes the supplier

Therefore, the total of balances in the purchases ledger is

the total owed to credit suppliers (accounts payable)

6.

Types of ledgers(cont’d)

General Ledger

Master set of accounts

Captures all the financial transactions relating to all

asset, liability, capital, revenue and expense accounts

It also contains summarised information from the

subsidiary ledgers

7.

What is acontrol account?

A control account is “summary” account in the general

ledger

It contains the totals for transactions that have been

otherwise recorded in subsidiary ledger accounts

It is most commonly used to summarise the sales ledger

and purchases ledger

8.

Purposes of controlaccounts

Act as an extension of the double entry system

Provide a check of the accuracy of entries made in the

sales ledger and purchases ledger accounts

Assist in locating errors early in the accounting period, as

control accounts may be prepared daily, weekly, etc

Ascertain missing figures such as credit sales or credit

purchases

9.

Common types ofcontrol accounts

The two most commonly used control accounts:

Sales ledger control account

Purchases ledger control account

10.

Sales ledger controlaccount

The sales ledger control account (SLCA) is used to verify

the balance in the sales ledger accounts

It is also called the total debtors control account

11.

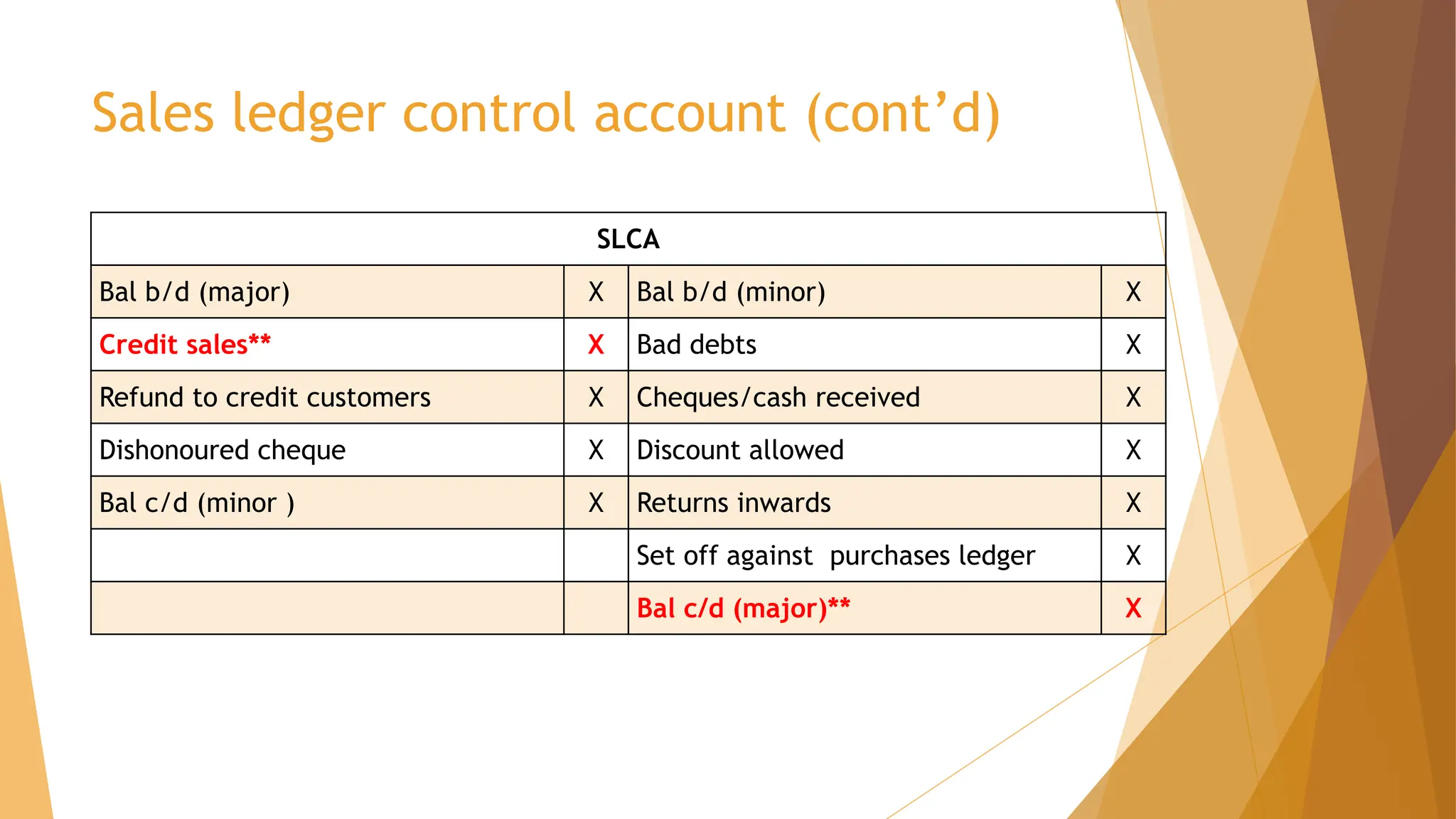

Sales ledger controlaccount (cont’d)

SLCA

Bal b/d (major) X Bal b/d (minor) X

Credit sales** X Bad debts X

Refund to credit customers X Cheques/cash received X

Dishonoured cheque X Discount allowed X

Bal c/d (minor ) X Returns inwards X

Set off against purchases ledger X

Bal c/d (major)** X

12.

Purchases ledger controlaccount

The purchases ledger control account (PLCA) is used to

verify the balance in the purchases ledger accounts

It is also called the total creditors control account

13.

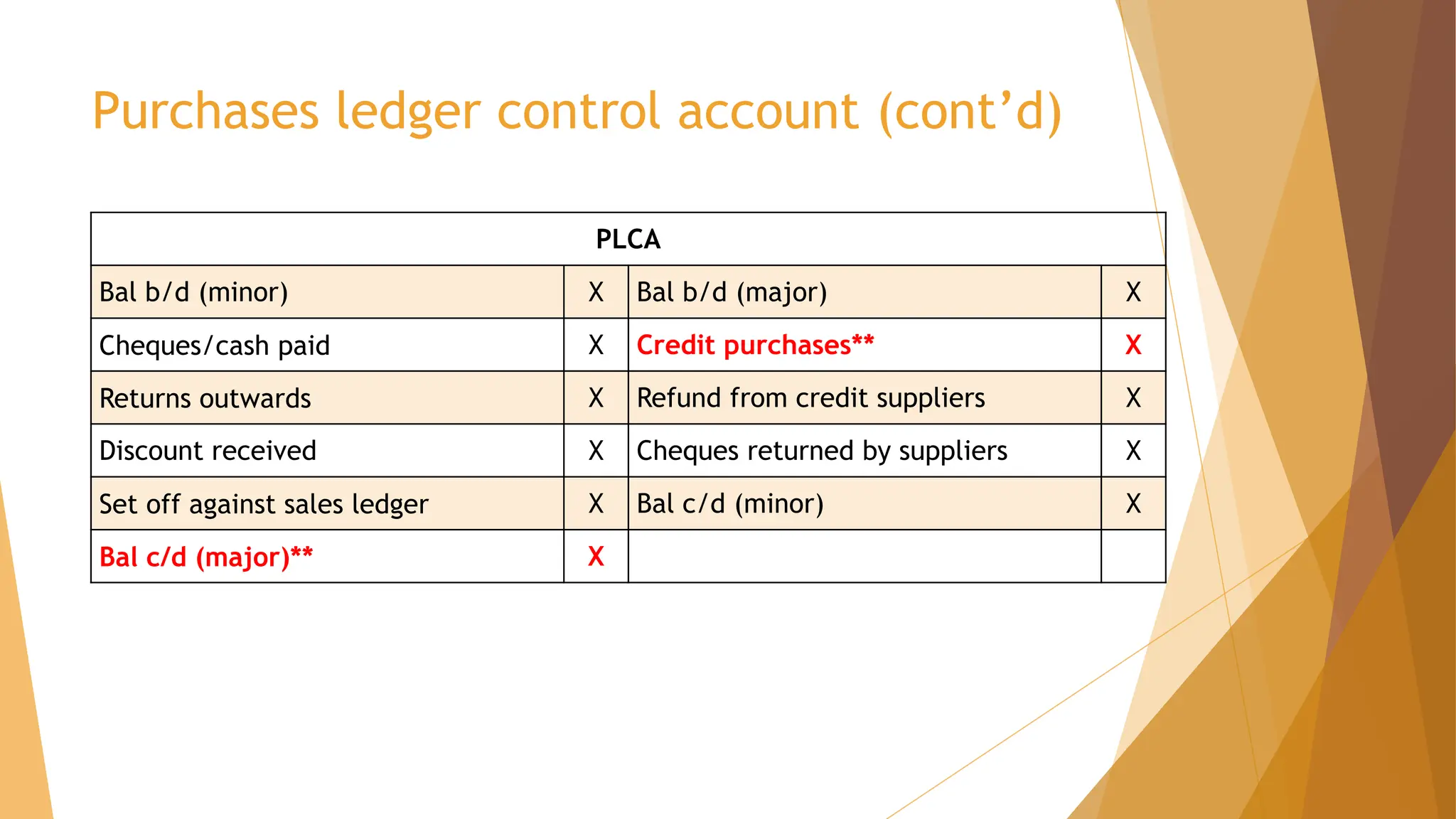

Purchases ledger controlaccount (cont’d)

PLCA

Bal b/d (minor) X Bal b/d (major) X

Cheques/cash paid X Credit purchases** X

Returns outwards X Refund from credit suppliers X

Discount received X Cheques returned by suppliers X

Set off against sales ledger X Bal c/d (minor) X

Bal c/d (major)** X

14.

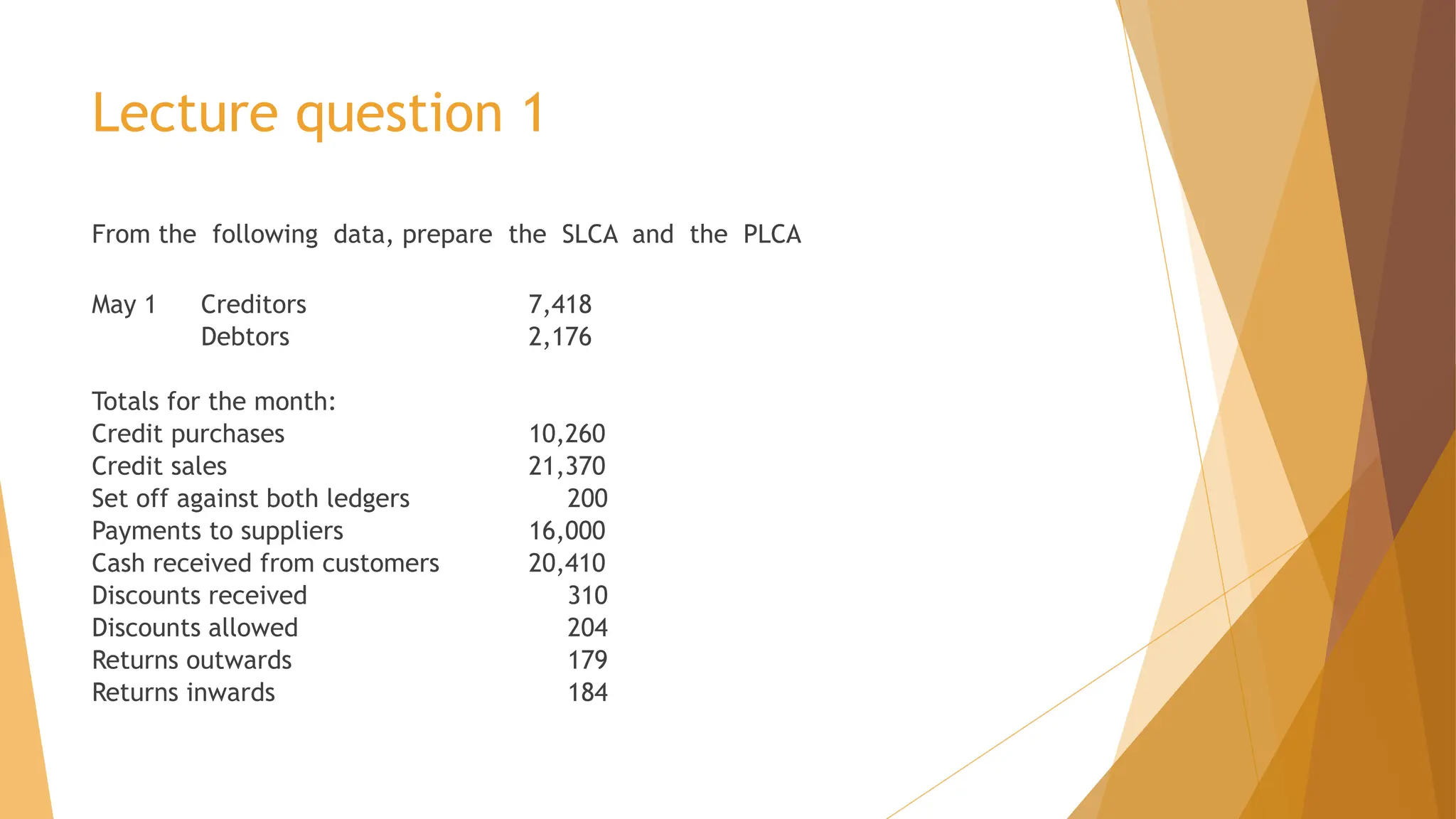

Lecture question 1

Fromthe following data, prepare the SLCA and the PLCA

May 1 Creditors 7,418

Debtors 2,176

Totals for the month:

Credit purchases 10,260

Credit sales 21,370

Set off against both ledgers 200

Payments to suppliers 16,000

Cash received from customers 20,410

Discounts received 310

Discounts allowed 204

Returns outwards 179

Returns inwards 184

15.

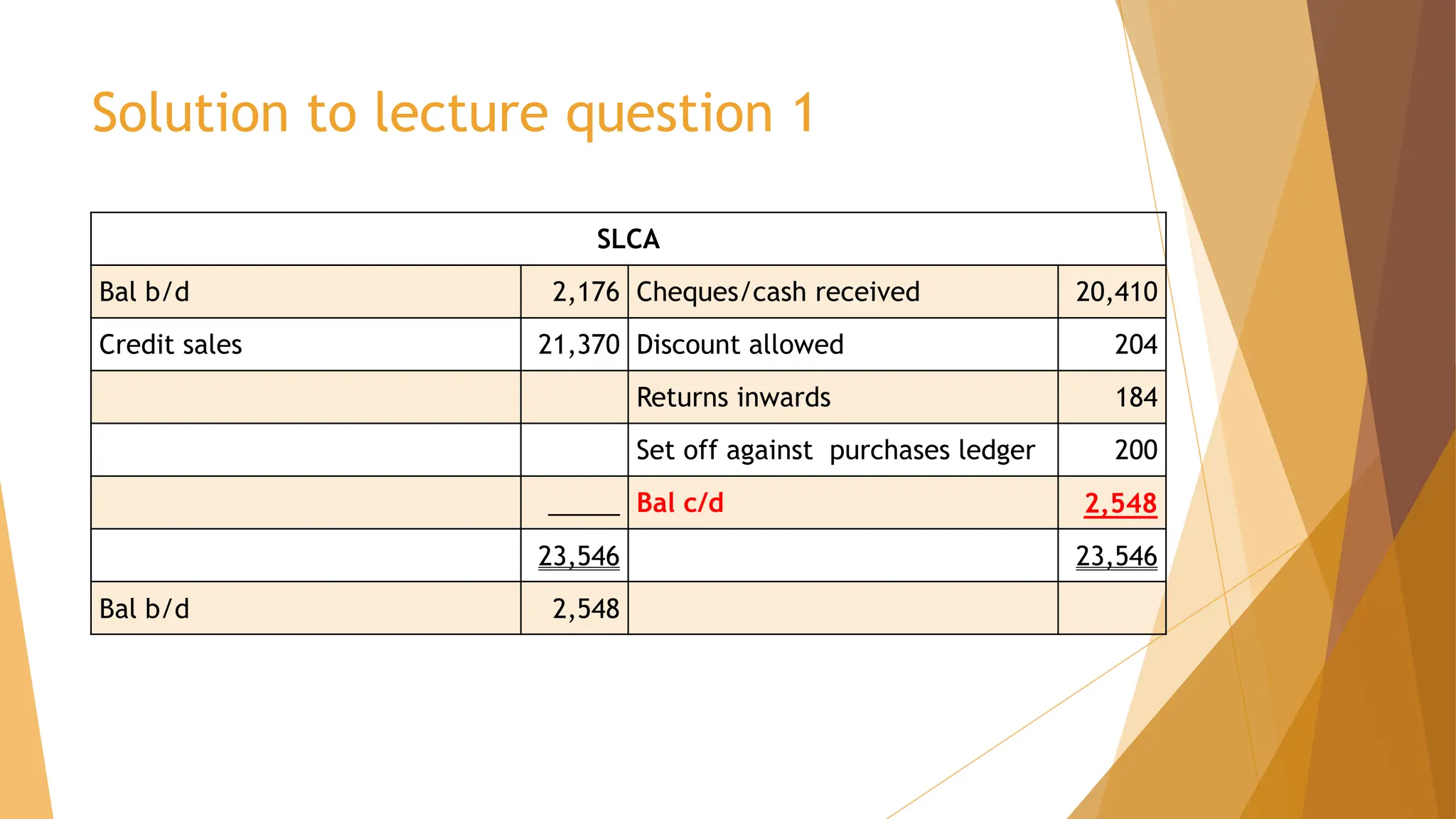

Solution to lecturequestion 1

SLCA

Bal b/d 2,176 Cheques/cash received 20,410

Credit sales 21,370 Discount allowed 204

Returns inwards 184

Set off against purchases ledger 200

_____ Bal c/d 2,548

23,546 23,546

Bal b/d 2,548

16.

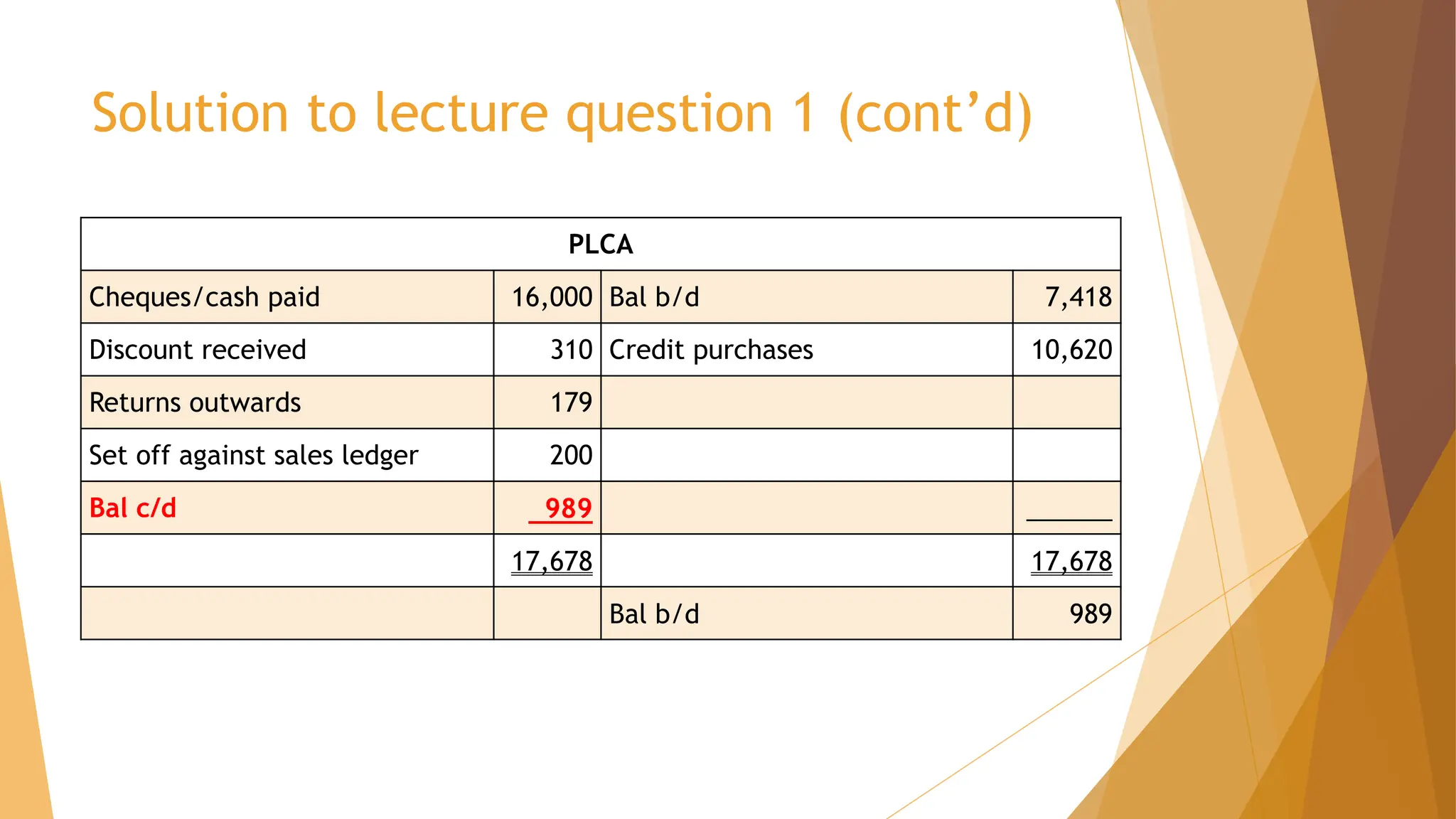

Solution to lecturequestion 1 (cont’d)

PLCA

Cheques/cash paid 16,000 Bal b/d 7,418

Discount received 310 Credit purchases 10,620

Returns outwards 179

Set off against sales ledger 200

Bal c/d 989 ______

17,678 17,678

Bal b/d 989

17.

Other applications ofcontrol accounts

The principles of control accounting can be used for other

types of accounts. For example:

Non current assets

To verify assets based on acquisition, disposal, revaluation

and depreciation

Expenses and revenues

Verifies amounts based on opening balances, payments

during the year, and closing balances

18.

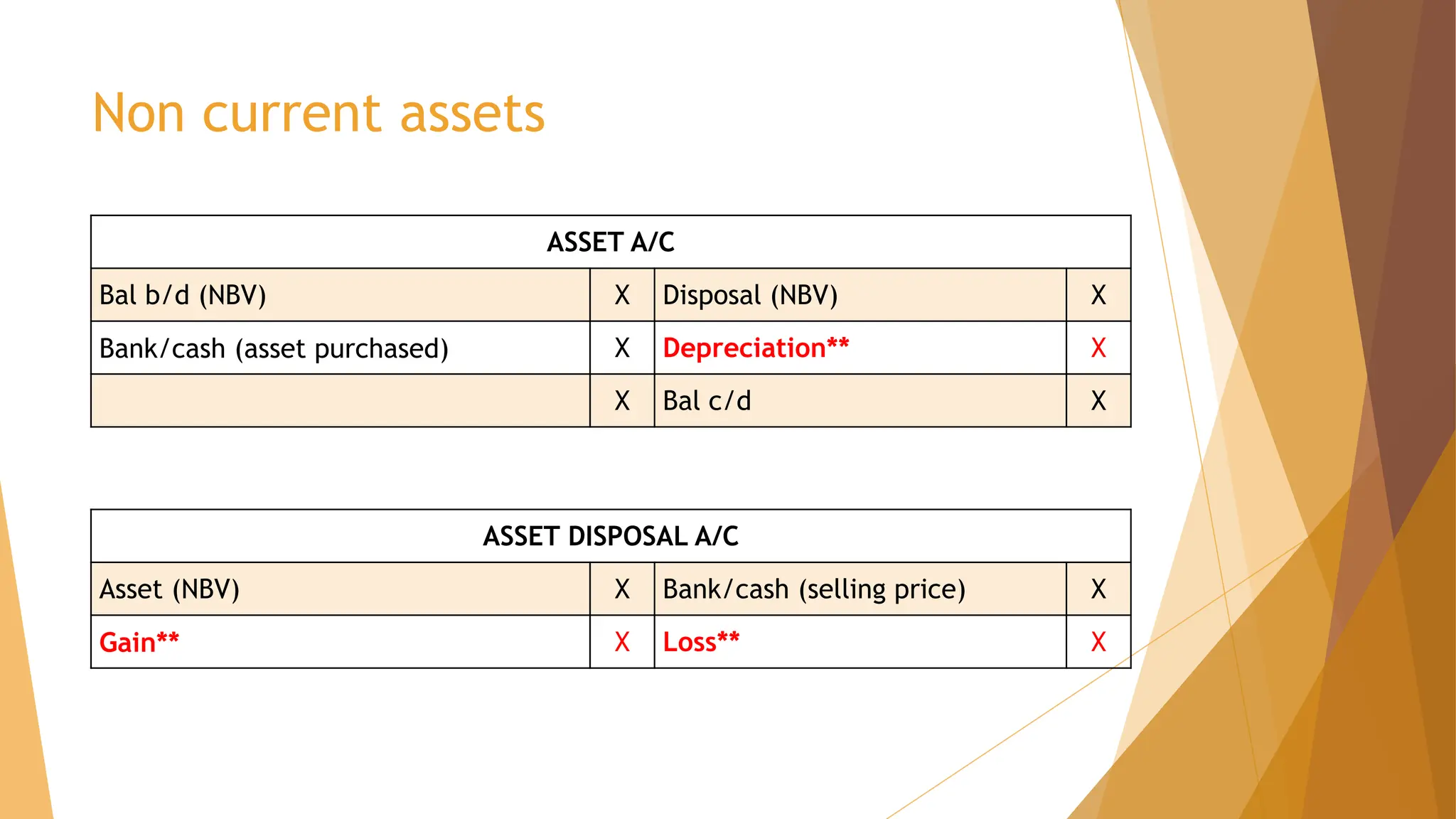

Non current assets

ASSETA/C

Bal b/d (NBV) X Disposal (NBV) X

Bank/cash (asset purchased) X Depreciation** X

X Bal c/d X

ASSET DISPOSAL A/C

Asset (NBV) X Bank/cash (selling price) X

Gain** X Loss** X

19.

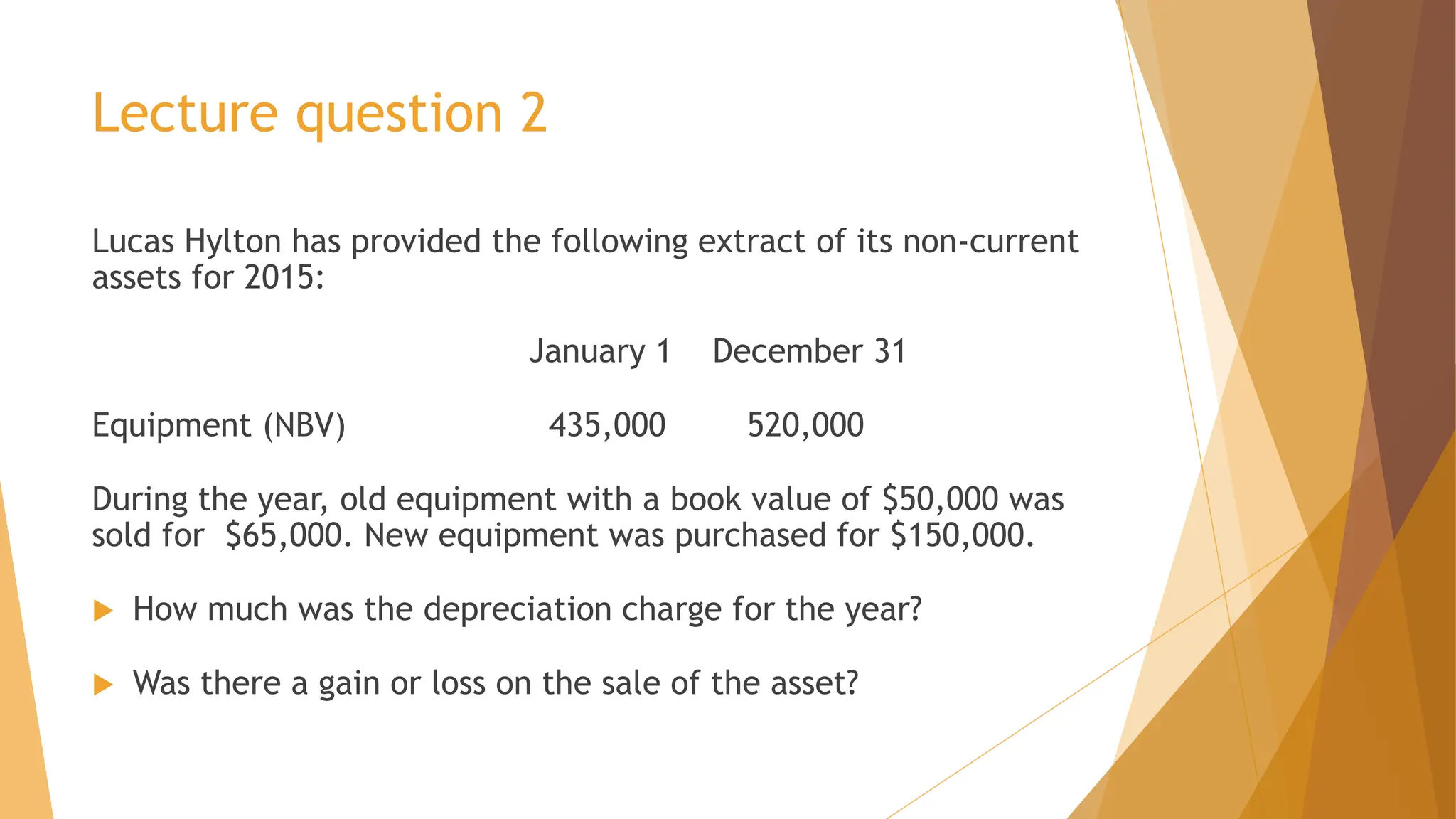

Lecture question 2

LucasHylton has provided the following extract of its non-current

assets for 2015:

January 1 December 31

Equipment (NBV) 435,000 520,000

During the year, old equipment with a book value of $50,000 was

sold for $65,000. New equipment was purchased for $150,000.

How much was the depreciation charge for the year?

Was there a gain or loss on the sale of the asset?

20.

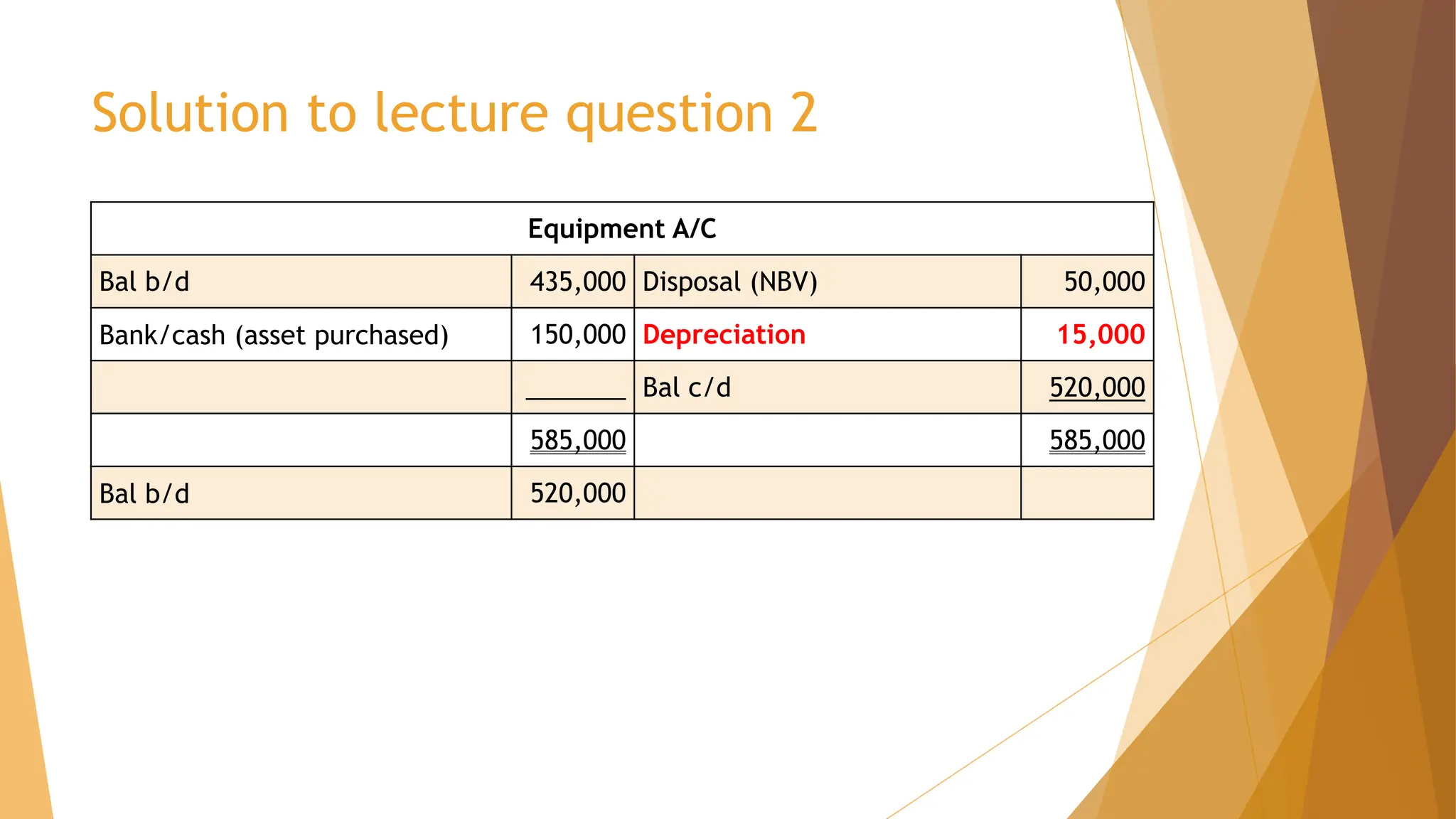

Solution to lecturequestion 2

Equipment A/C

Bal b/d 435,000 Disposal (NBV) 50,000

Bank/cash (asset purchased) 150,000 Depreciation 15,000

_______ Bal c/d 520,000

585,000 585,000

Bal b/d 520,000

21.

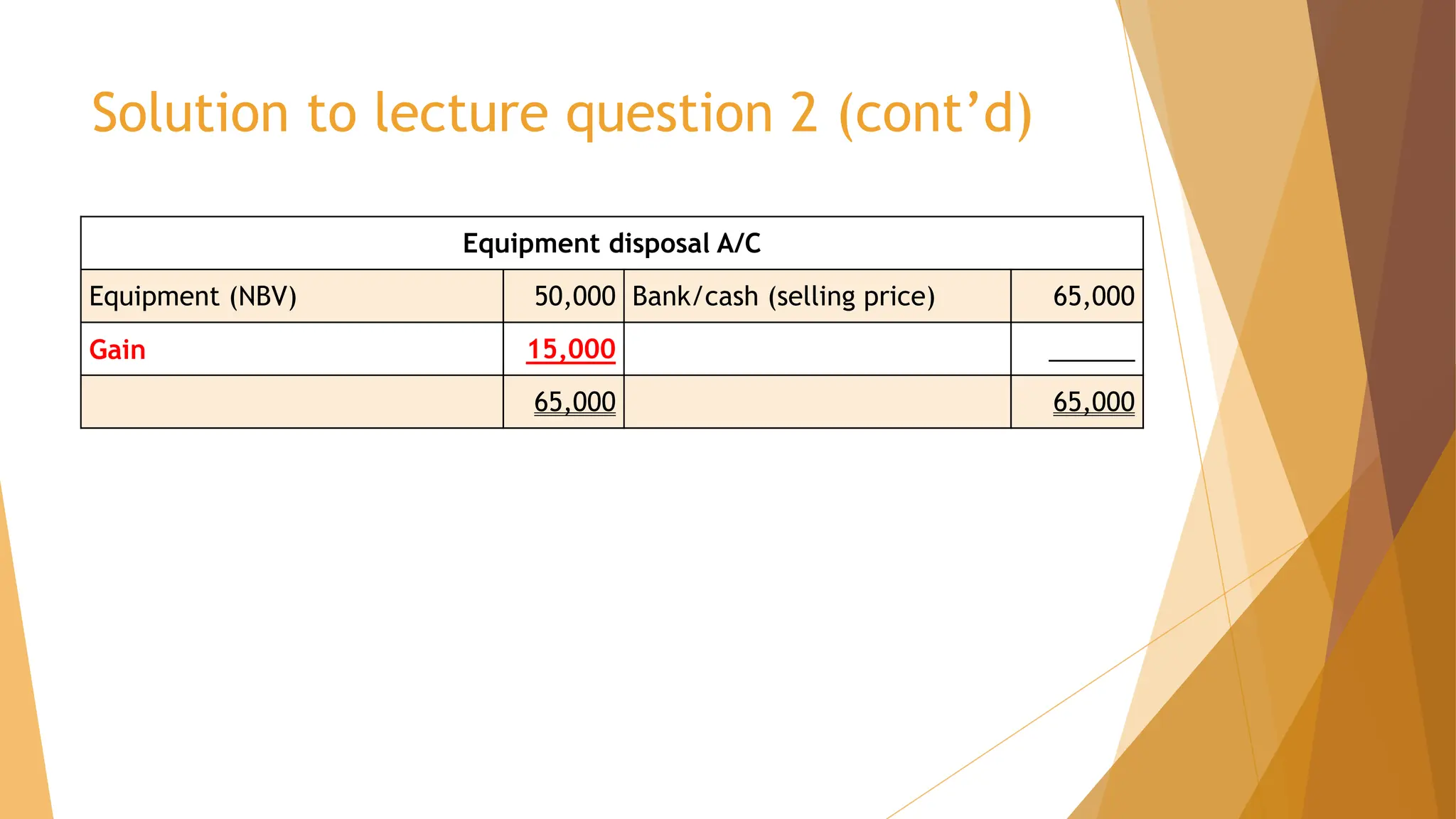

Solution to lecturequestion 2 (cont’d)

Equipment disposal A/C

Equipment (NBV) 50,000 Bank/cash (selling price) 65,000

Gain 15,000 ______

65,000 65,000

22.

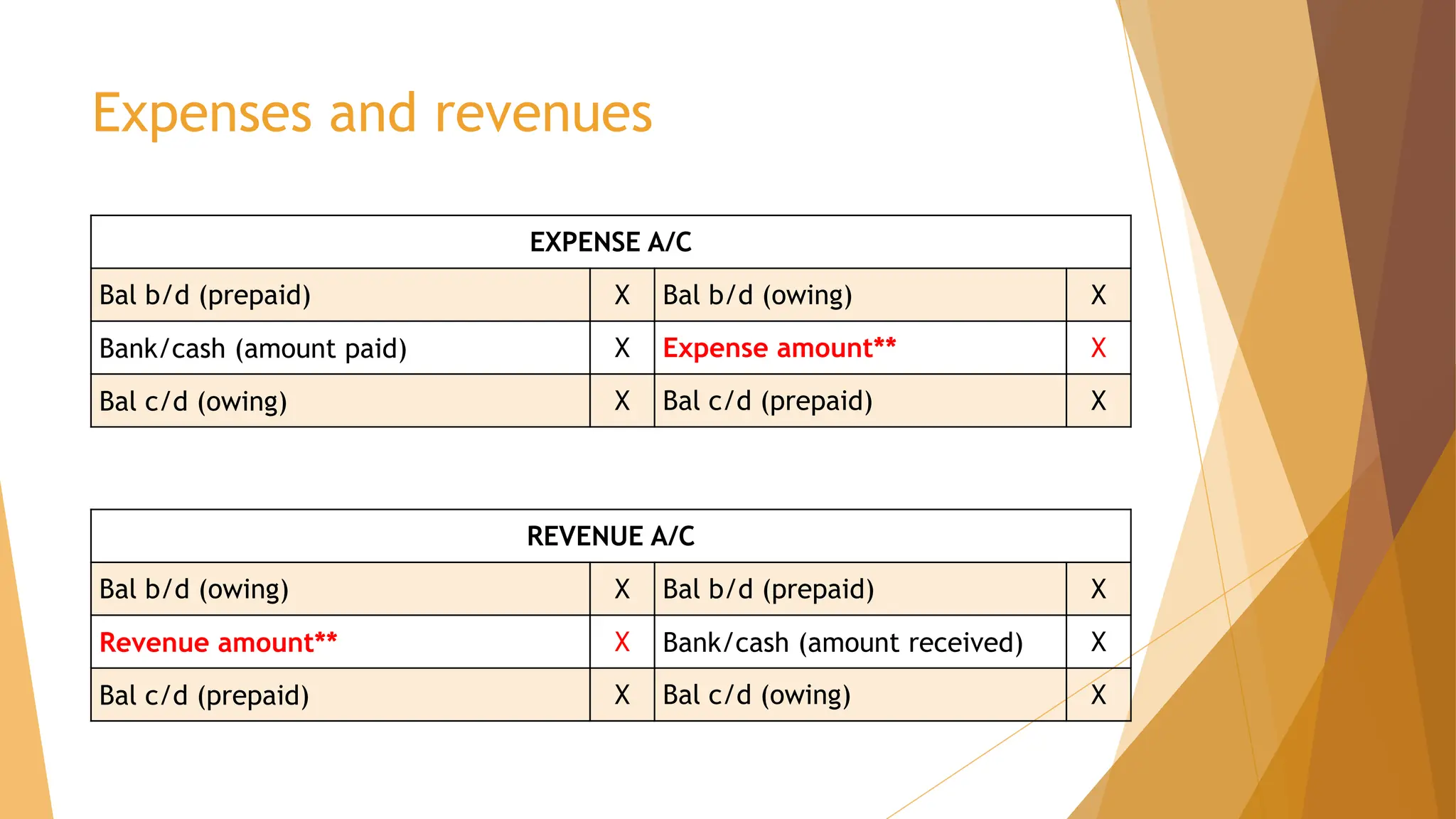

Expenses and revenues

EXPENSEA/C

Bal b/d (prepaid) X Bal b/d (owing) X

Bank/cash (amount paid) X Expense amount** X

Bal c/d (owing) X Bal c/d (prepaid) X

REVENUE A/C

Bal b/d (owing) X Bal b/d (prepaid) X

Revenue amount** X Bank/cash (amount received) X

Bal c/d (prepaid) X Bal c/d (owing) X

23.

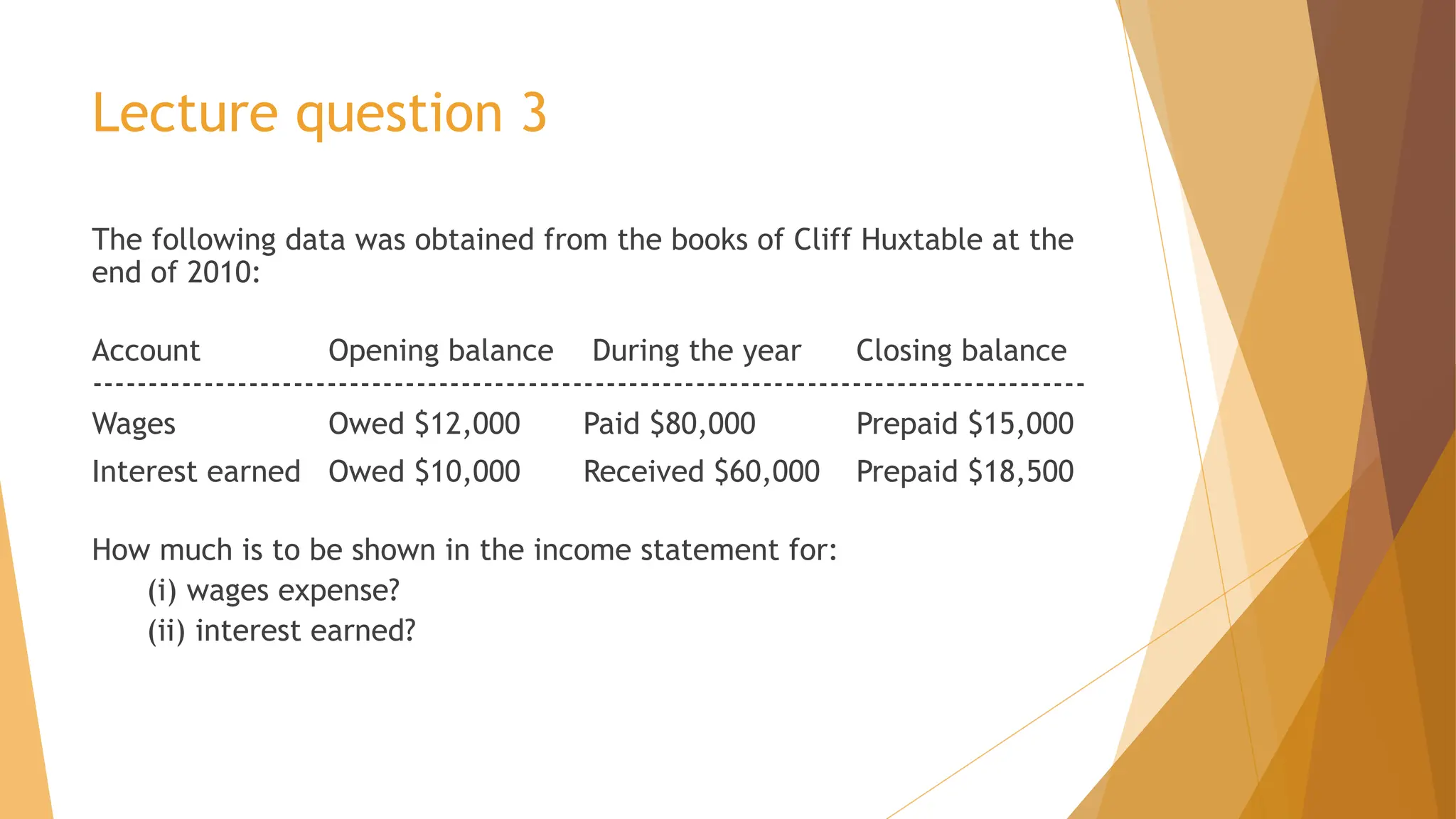

Lecture question 3

Thefollowing data was obtained from the books of Cliff Huxtable at the

end of 2010:

Account Opening balance During the year Closing balance

-----------------------------------------------------------------------------------------

Wages Owed $12,000 Paid $80,000 Prepaid $15,000

Interest earned Owed $10,000 Received $60,000 Prepaid $18,500

How much is to be shown in the income statement for:

(i) wages expense?

(ii) interest earned?

24.

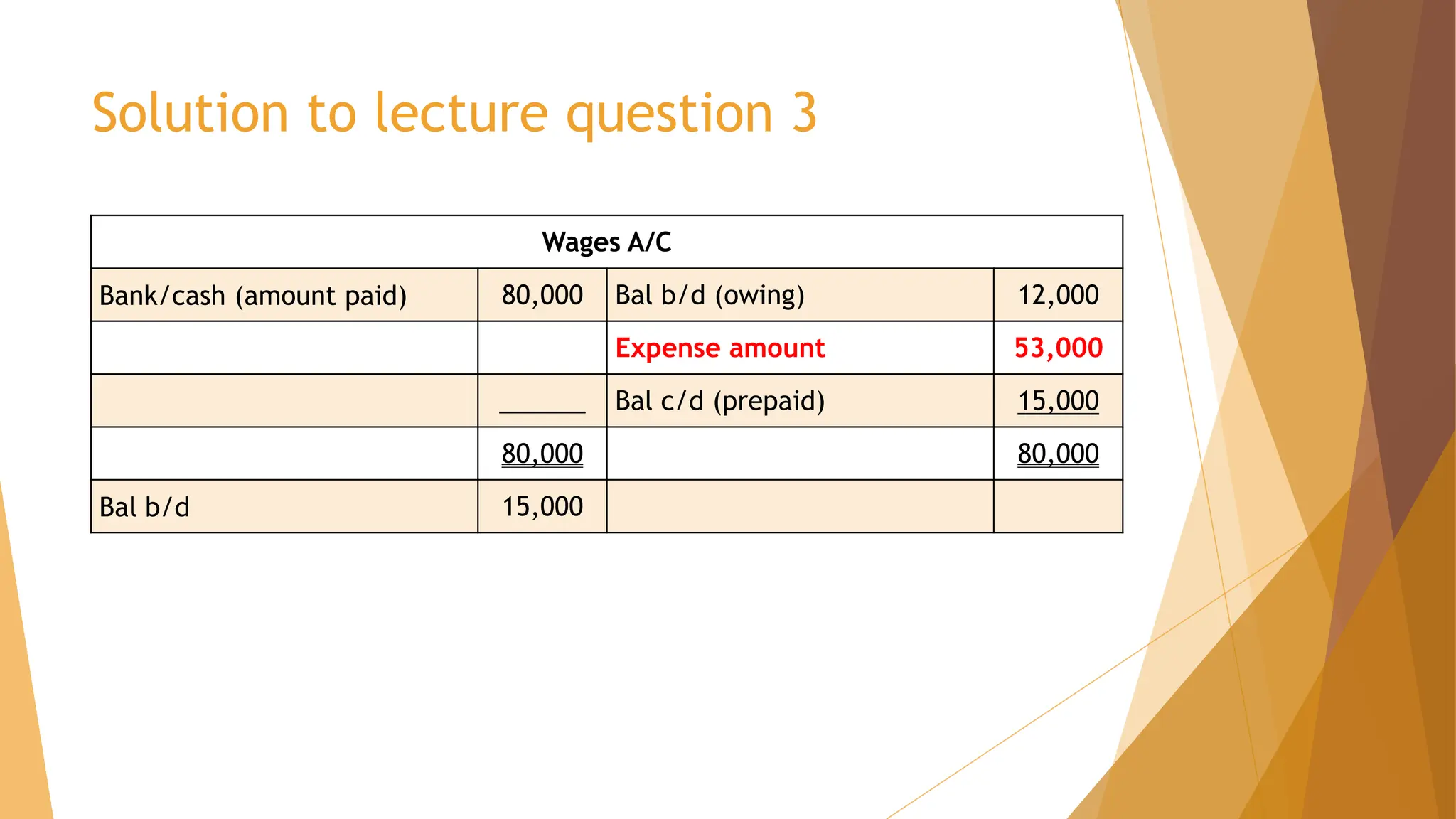

Solution to lecturequestion 3

Wages A/C

Bank/cash (amount paid) 80,000 Bal b/d (owing) 12,000

Expense amount 53,000

______ Bal c/d (prepaid) 15,000

80,000 80,000

Bal b/d 15,000

25.

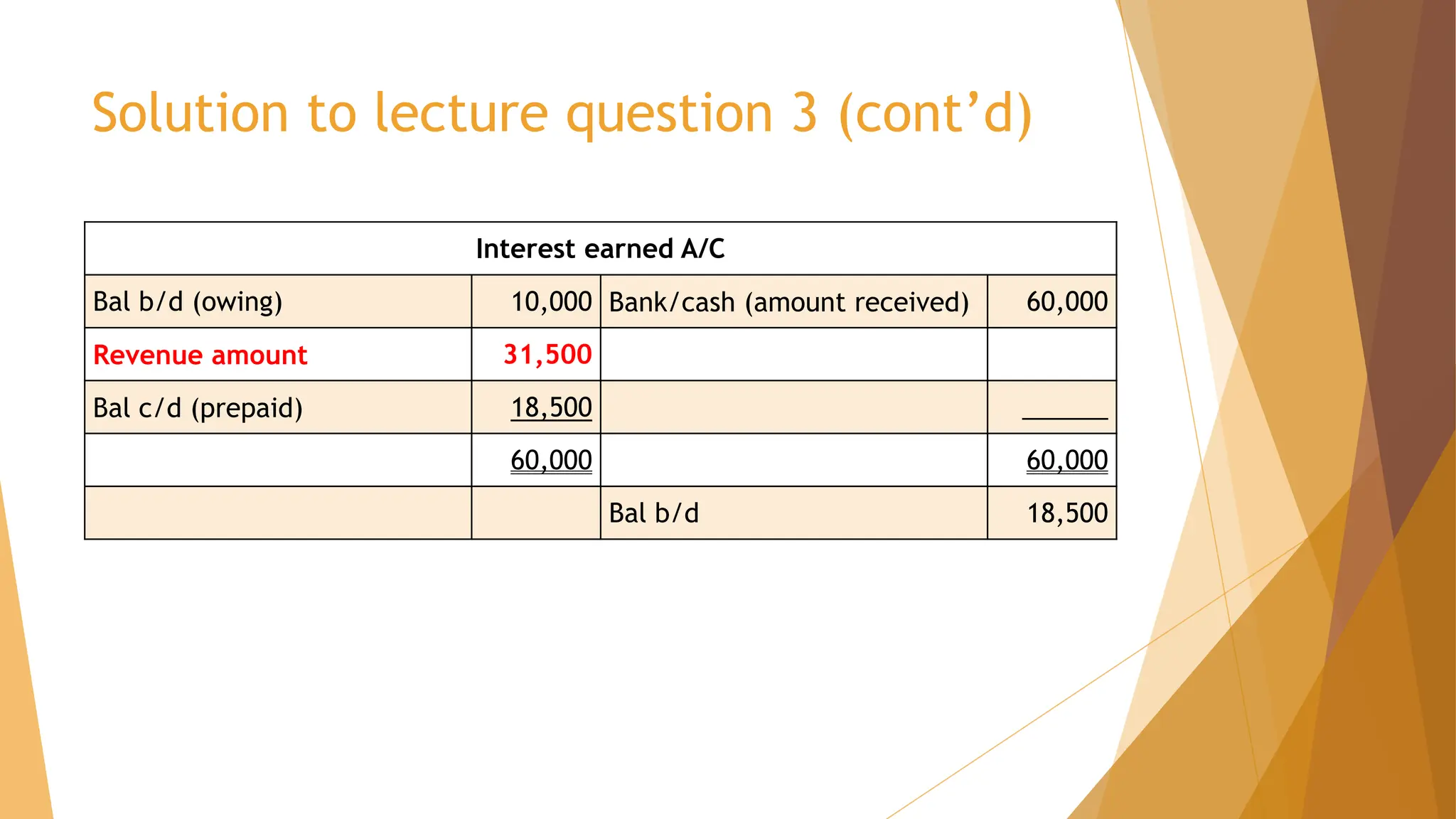

Solution to lecturequestion 3 (cont’d)

Interest earned A/C

Bal b/d (owing) 10,000 Bank/cash (amount received) 60,000

Revenue amount 31,500

Bal c/d (prepaid) 18,500 ______

60,000 60,000

Bal b/d 18,500