Download to read offline

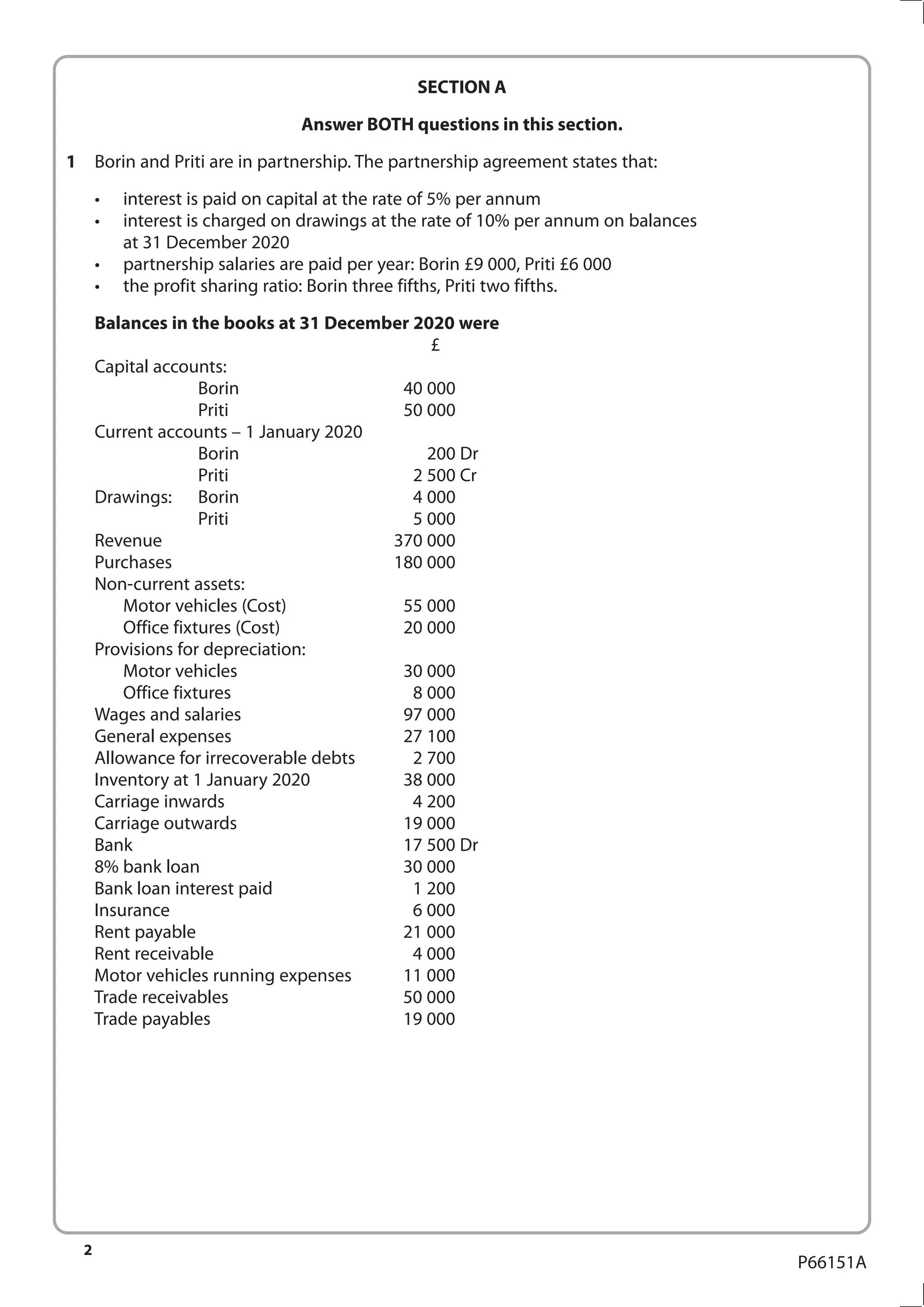

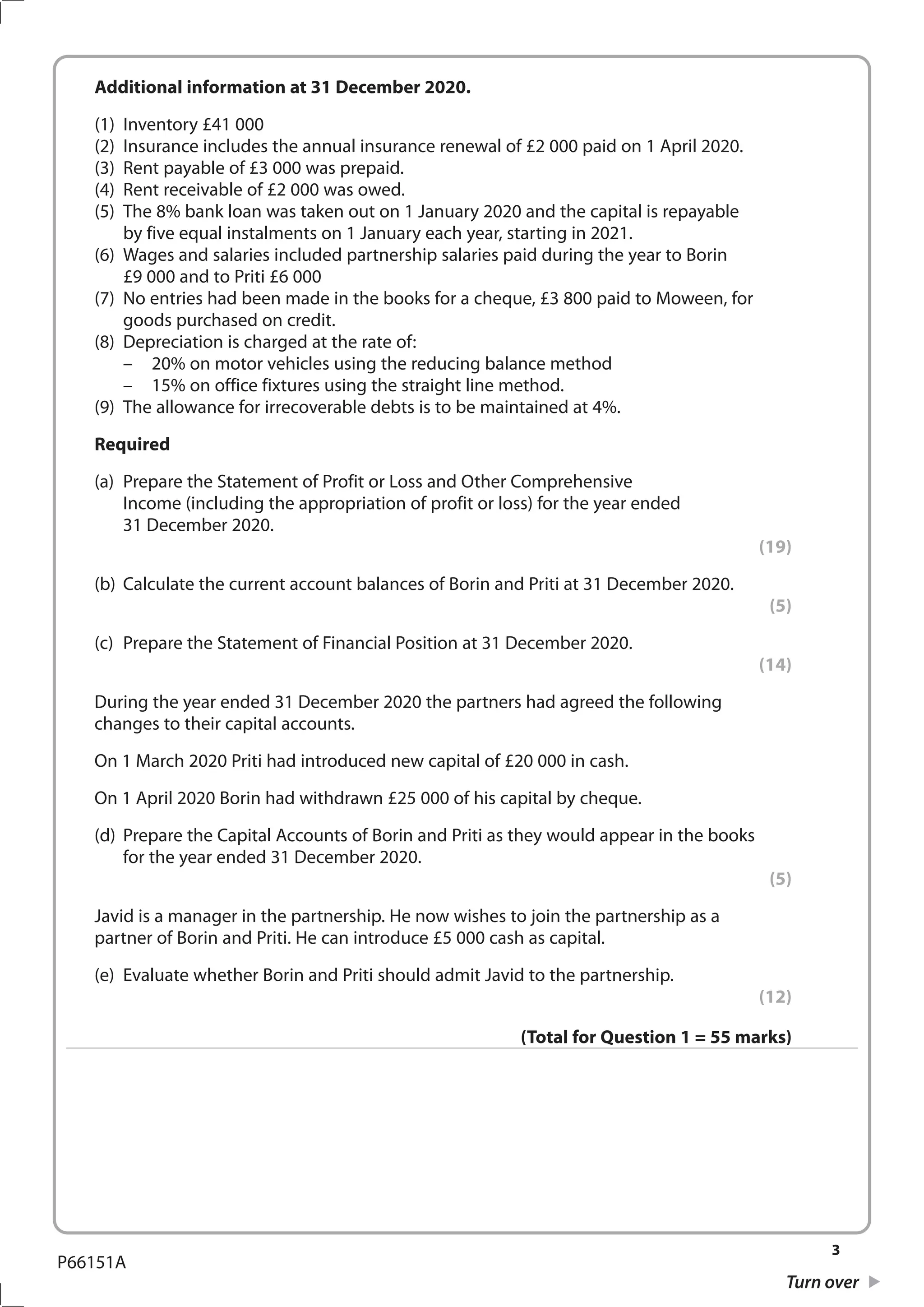

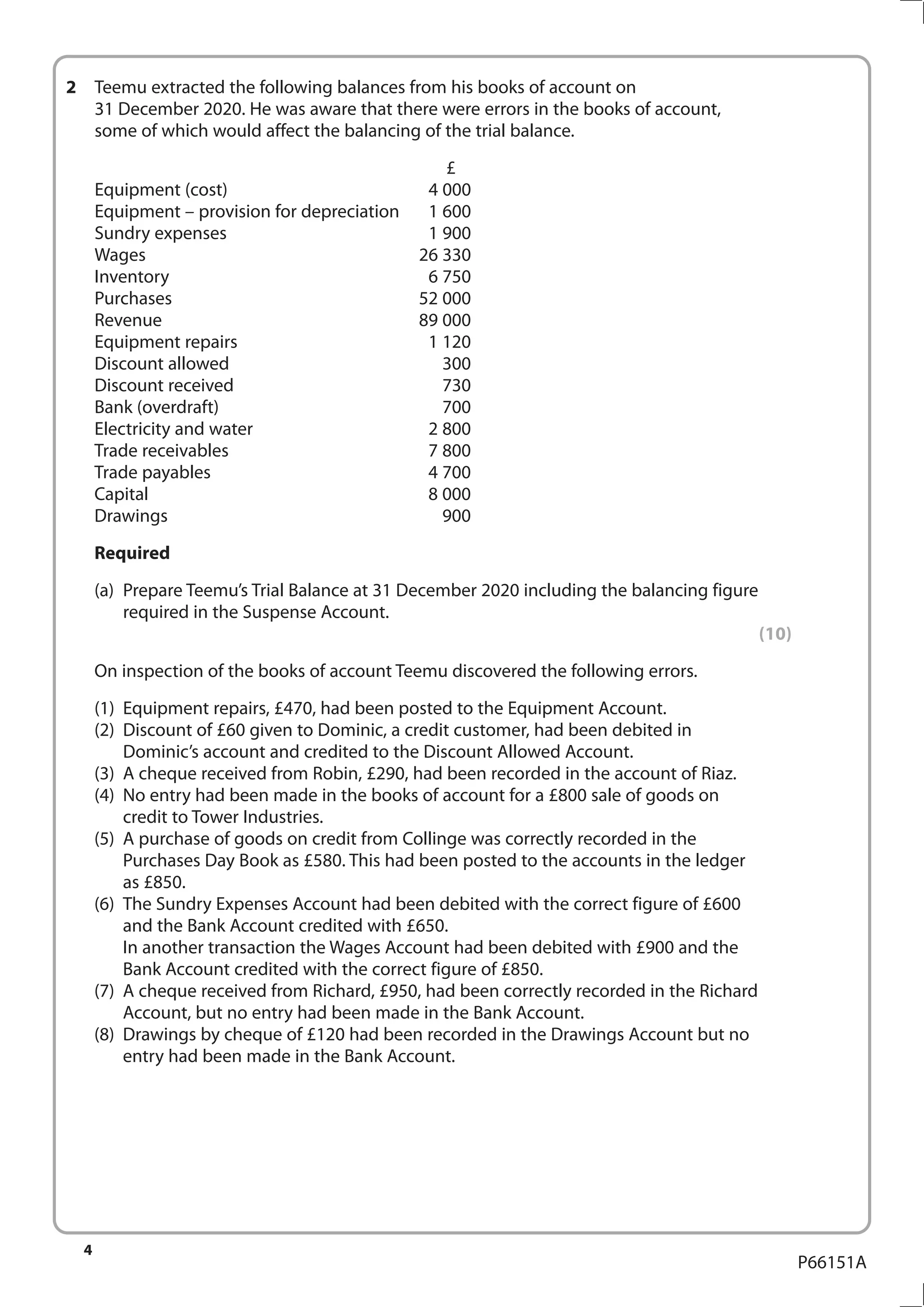

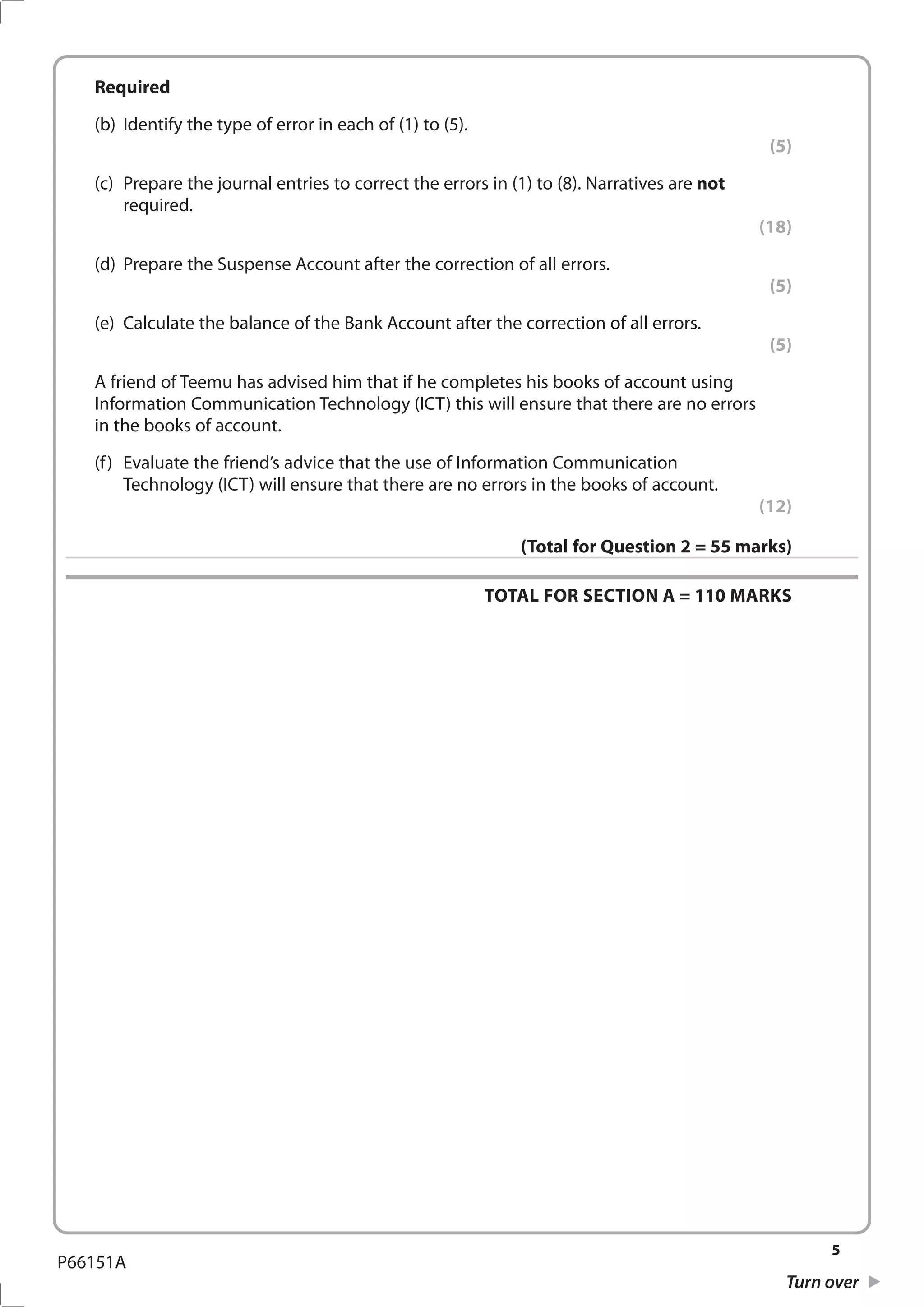

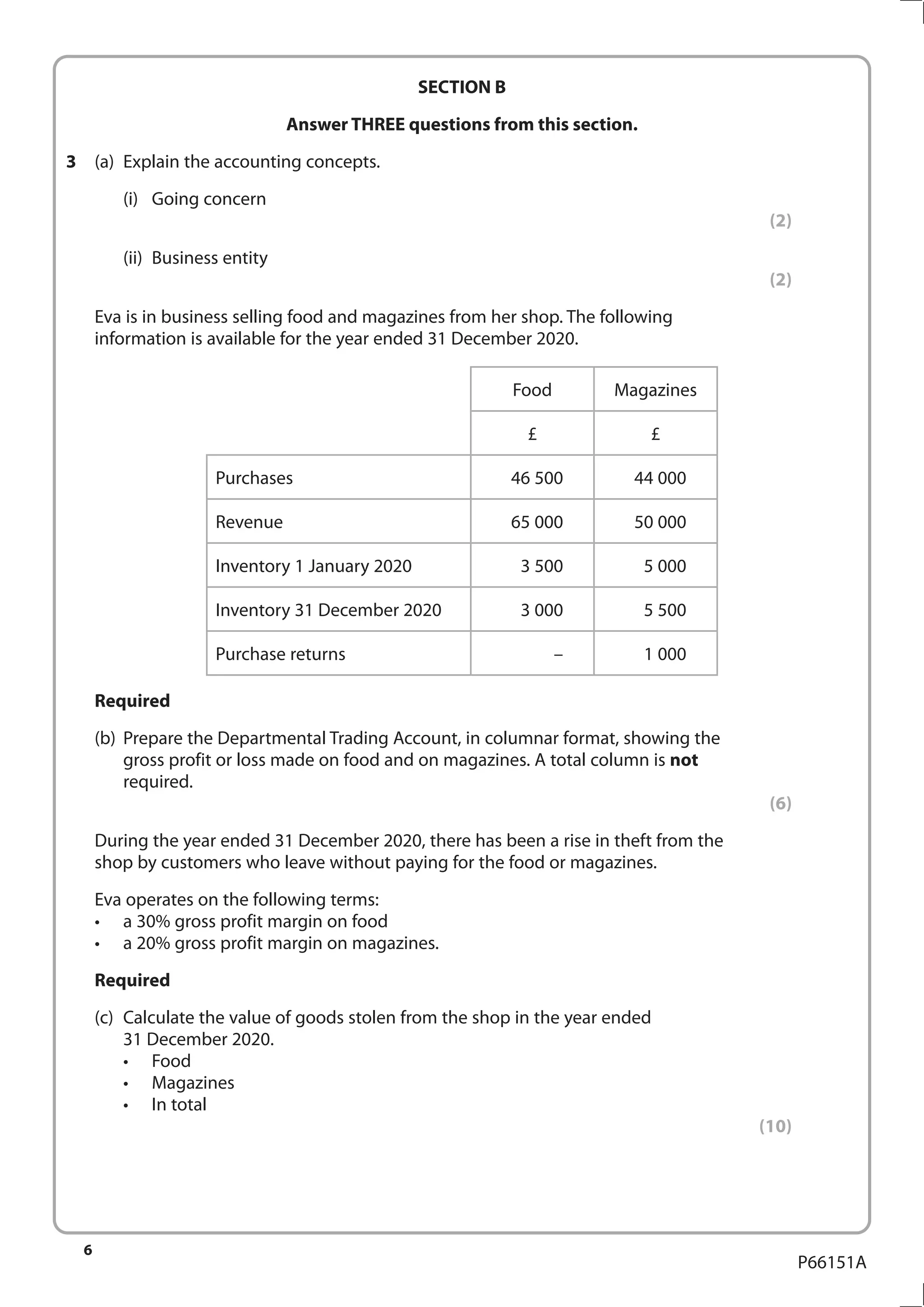

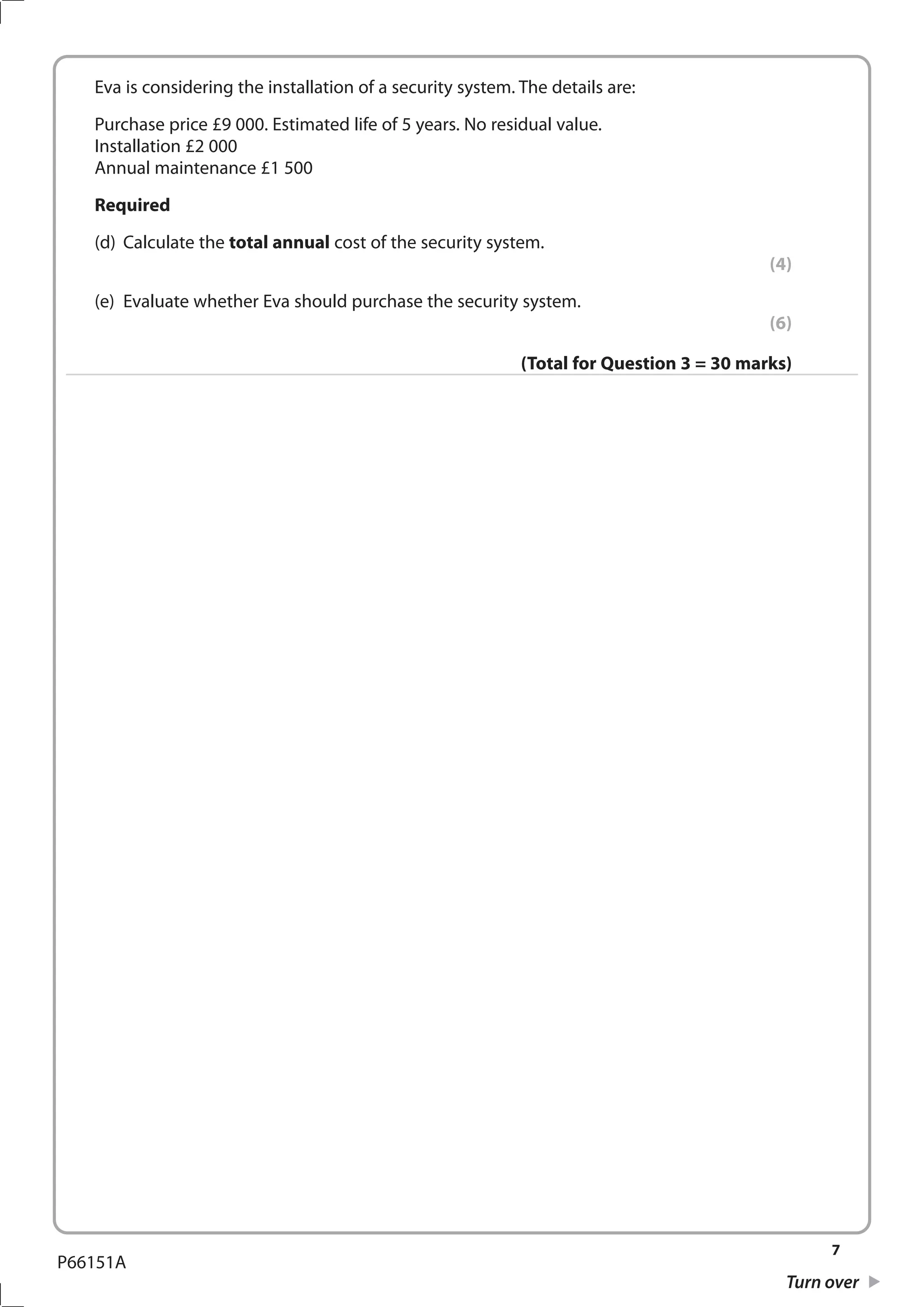

The document is an examination paper for the Pearson Edexcel International Advanced Level Accounting, containing instructions and questions for candidates. It includes sections on preparing financial statements, calculating account balances, and correcting errors, along with time constraints and materials required. Candidates must answer specific questions, demonstrating their accounting knowledge and skills.