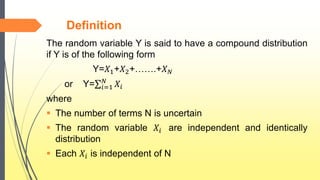

This document outlines the concept of compound distributions. It defines a compound distribution as a random variable Y that is the sum of random variables X1 + X2 + ... + XN, where N is a random variable representing the number of terms. The document discusses the assumptions about N and the Xi, provides an example, and outlines the key properties of compound distributions including distribution function, expected value, variance, and moment generating function. It also includes a numerical example to demonstrate calculating the expected value and variance of a compound distribution.

![1. Distribution function

By the total law of probability, the distribution function of Y

is given by

𝐹𝑌(y)= 𝑛=0

∞

𝐺 𝑛(y)P[N=n]

Where

For n=0 ,𝐺0(y) is the distribution function of the point

mass at y=0

For n ≥ 1 , 𝐺 𝑁 (y) is the distribution function of the

independent sum 𝑋1+𝑋2+…….+𝑋 𝑁](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-7-320.jpg)

![2. Expected value

The mean aggregate claim is :

E[Y]=E[N]E[X]

The expected value of the aggregate claims has a natural

interpretation .

It is the product of the expected number of claims and the

expected individual claim amount](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-8-320.jpg)

![Expected value (cont…)

proof: E[Y] = 𝐸 𝑁[E(Y|N=n)]

= 𝐸 𝑁[ E[ 𝑖=1

𝑁

𝑋𝑖]]

= 𝐸 𝑁[∑E[X]]

= 𝐸 𝑁[NE[X]]

= E[N]E[X]

The higher moments of the aggregate claims Y

do not have a intuitively clear formula as the

first moment .](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-9-320.jpg)

![3. Higher moment

We can obtain the higher moments by using the first

principle

E[𝑌 𝑛

] = 𝐸 𝑁[E(𝑌 𝑛

|N)]

= 𝐸 𝑁[E({𝑋1+𝑋2+…….+𝑋 𝑁} 𝑛|N)]

=E[𝑍1

𝑛

]P N = 1 +E[𝑍2

𝑛

]P N = 2 +…….

Where

𝑍 𝑛 = 𝑋1+𝑋2+…….+𝑋 𝑁](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-10-320.jpg)

![4. Variance

The variance of the aggregate claims var[Y] is:

var[Y] = E[N] var[X]+ var[N]𝐸[𝑋]2

The variance of the aggregate claims also has a

natural interpretation

It is the sum of two components such that the first

component stems from the variability of the individual

claim amount and the second component stems from

the variability of the number of claims](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-11-320.jpg)

![Variance (cont…)

The variance of the aggregate claims ,by using the total

variance formula

var[Y] = 𝐸 𝑁[𝑣𝑎𝑟(Y|N)]+𝑣𝑎𝑟 𝑁 [E(Y|N)]

= 𝐸 𝑁[𝑣𝑎𝑟(𝑋1+𝑋2+…….+𝑋 𝑁|N)]

+ 𝑣𝑎𝑟 𝑁 [E(𝑋1+𝑋2+…….+𝑋 𝑁|N)]

= 𝐸 𝑁[N𝑣𝑎𝑟(X)]+𝑣𝑎𝑟 𝑁 [NE(X)]

var[Y] = E N Var X + Var N 𝐸[𝑋]2](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-12-320.jpg)

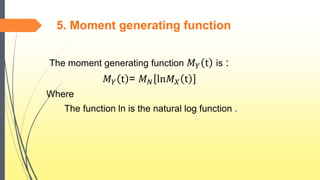

![Steps for m.g.f.

𝑀 𝑌 t = E[𝑒 𝑡𝑌 ]

= 𝐸 𝑁[E𝑒 𝑡( 𝑋1+ 𝑋2+…….+ 𝑋 𝑁) |N]

= 𝐸 𝑁[E(𝑒 𝑡𝑋1…….. 𝑒 𝑡𝑋 𝑁)|N]

= 𝐸 𝑁[E(𝑒 𝑡𝑋1)…….. E(𝑒 𝑡𝑋 𝑁)|N]

= 𝐸 𝑁[𝑀 𝑋(𝑡) 𝑁

]

= 𝐸 𝑁[𝑒 𝑁𝑙𝑛𝑀 𝑋(𝑡)

]

𝑀 𝑌 t = 𝑀 𝑁[ln𝑀 𝑋(t)]](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-14-320.jpg)

![Numerical Problem

𝑋𝑖 = Numbers of the 𝑖 𝑡ℎ patient has

𝑋𝑖 is distributed as a possion

E[𝑋𝑖] = 1.6

N = Number of patients seen by a doctor in an hour

N is also possion distributed

E[N] = 4.7

Problem :

1. What are the expected number of symptoms

diagnosed in an hour by a doctor ?](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-15-320.jpg)

![Numerical (cont…)

2. What are the variance value of symptoms

diagnose in an hour by a doctor

Solution

S= Number of symptoms diagnosed in an hour by a

doctor

S= 𝑋1+𝑋2+…….+𝑋 𝑁

1. E[S]=E[N]E[ 𝑋𝑖]

E[S]=7.52

2. var[S] = E[N] var[ 𝑋𝑖]+ var[N]𝐸[ 𝑋𝑖]2

var[S] = 19.552](https://image.slidesharecdn.com/finalpresentation-160918163750/85/compound-distribution-16-320.jpg)