Downloaded 18 times

This document provides an overview of financial accounting concepts including the definition of accounting, the types of accounts (personal, real, and nominal), journal entries, and key accounting transactions like purchases and sales of goods. It defines accounting as the process of identifying, measuring, recording, classifying, verifying, communicating, and interpreting financial information. Journal entries record transactions in chronological order with debits and credits, and involve personal accounts for individuals/entities, real accounts for assets/properties, and nominal accounts for income/expenses.

Presentation of financial accounts by Vikash Barnwal, highlighting the importance of accounting in business.

Accounting is defined as the language of business that captures financial performance, including profit/loss and assets/liabilities.

Discussion on the historical origins of accounting, tracing it back to its Italian roots.

Defining accounting according to experts and outlining its key components: recording, summarizing, reporting, analyzing, interpreting, and communicating.

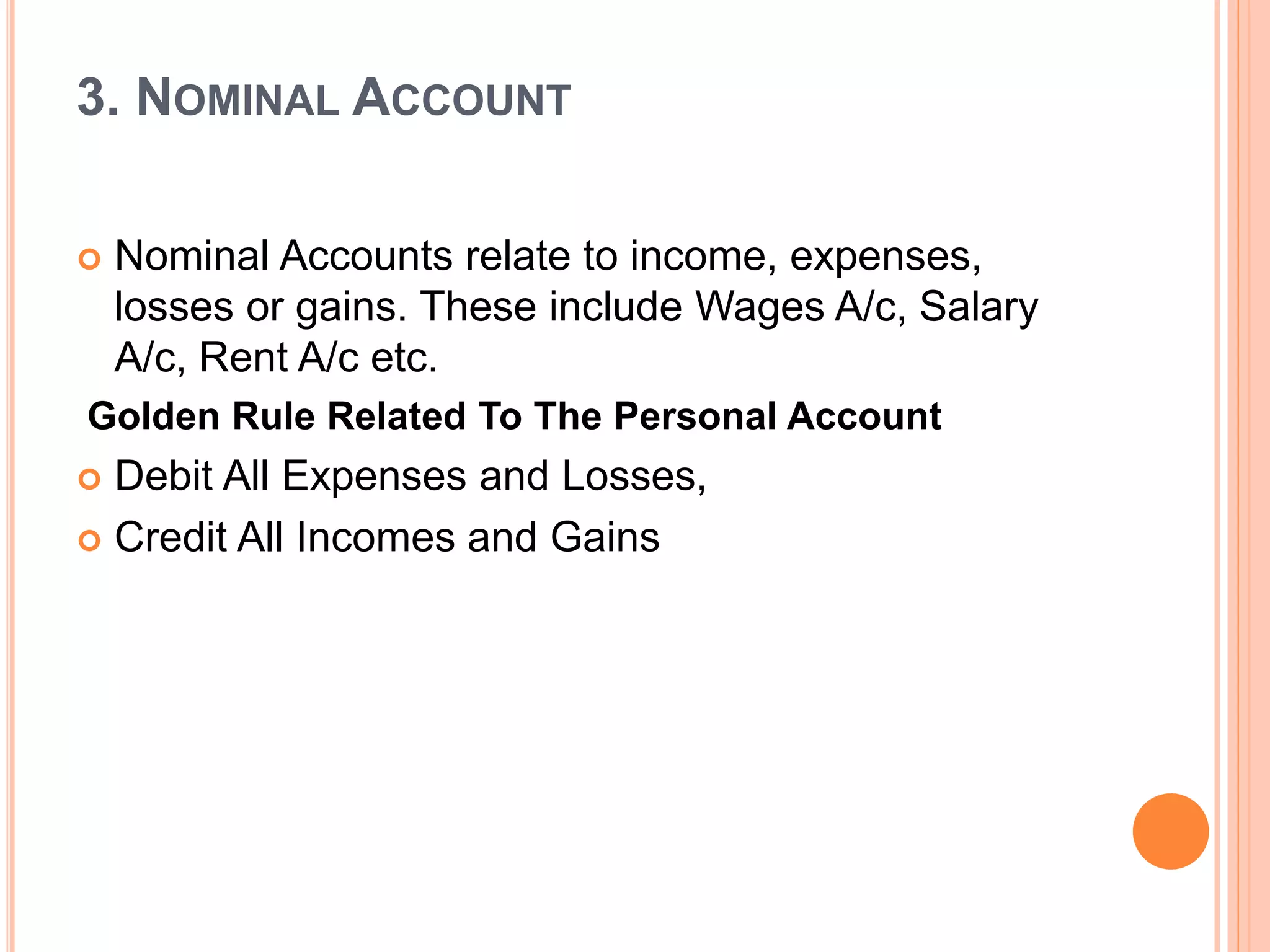

Overview of different account types: Personal, Real, and Nominal Accounts, and their characteristics and rules.

Introduction to journal entries, their importance in recording daily transactions, and the definition of a journal.

Key characteristics of journal entries, such as chronological recording and its advantages in providing complete accounting information.

Distinction between simple and compound journal entries based on the number of accounts affected.

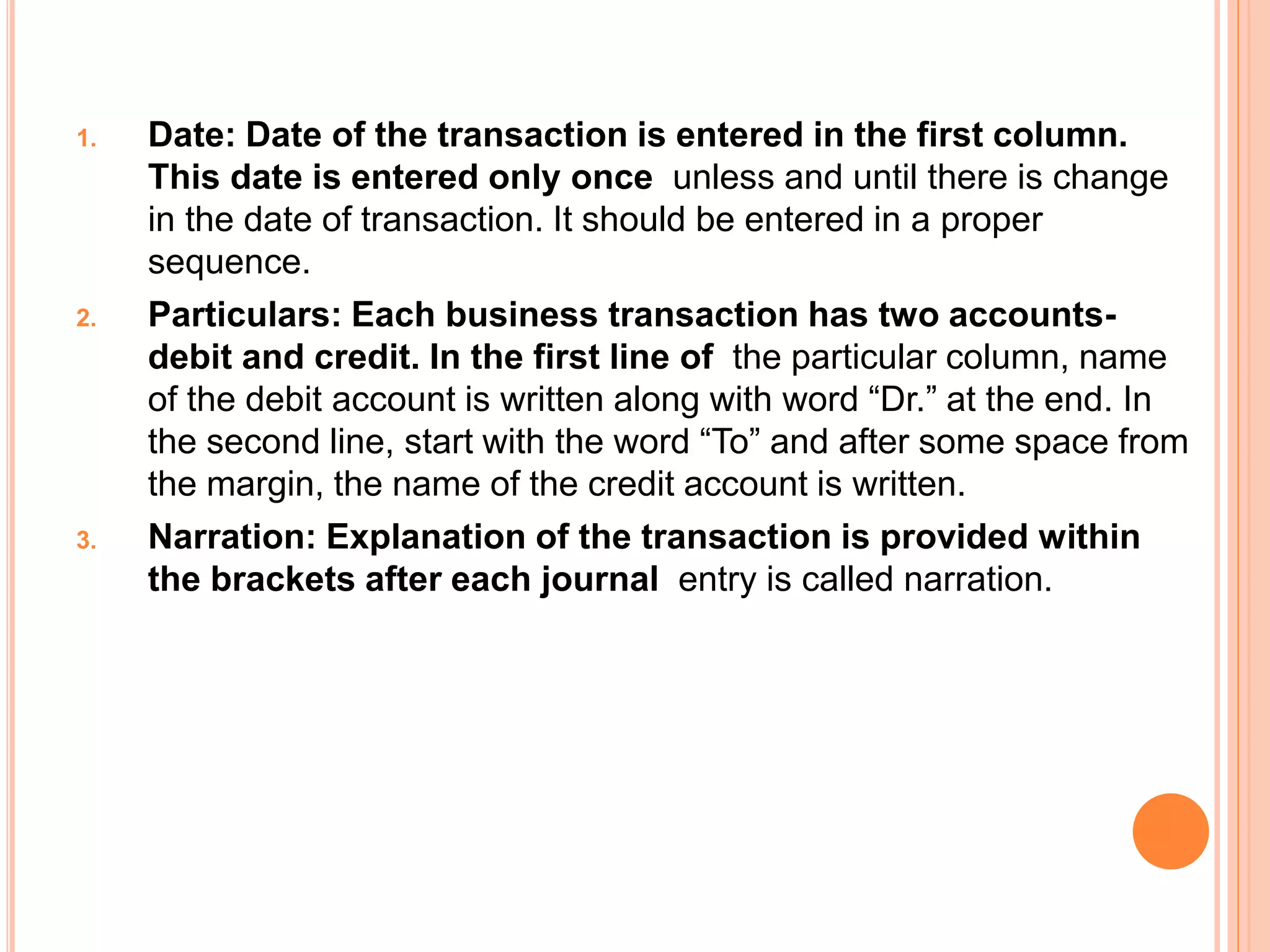

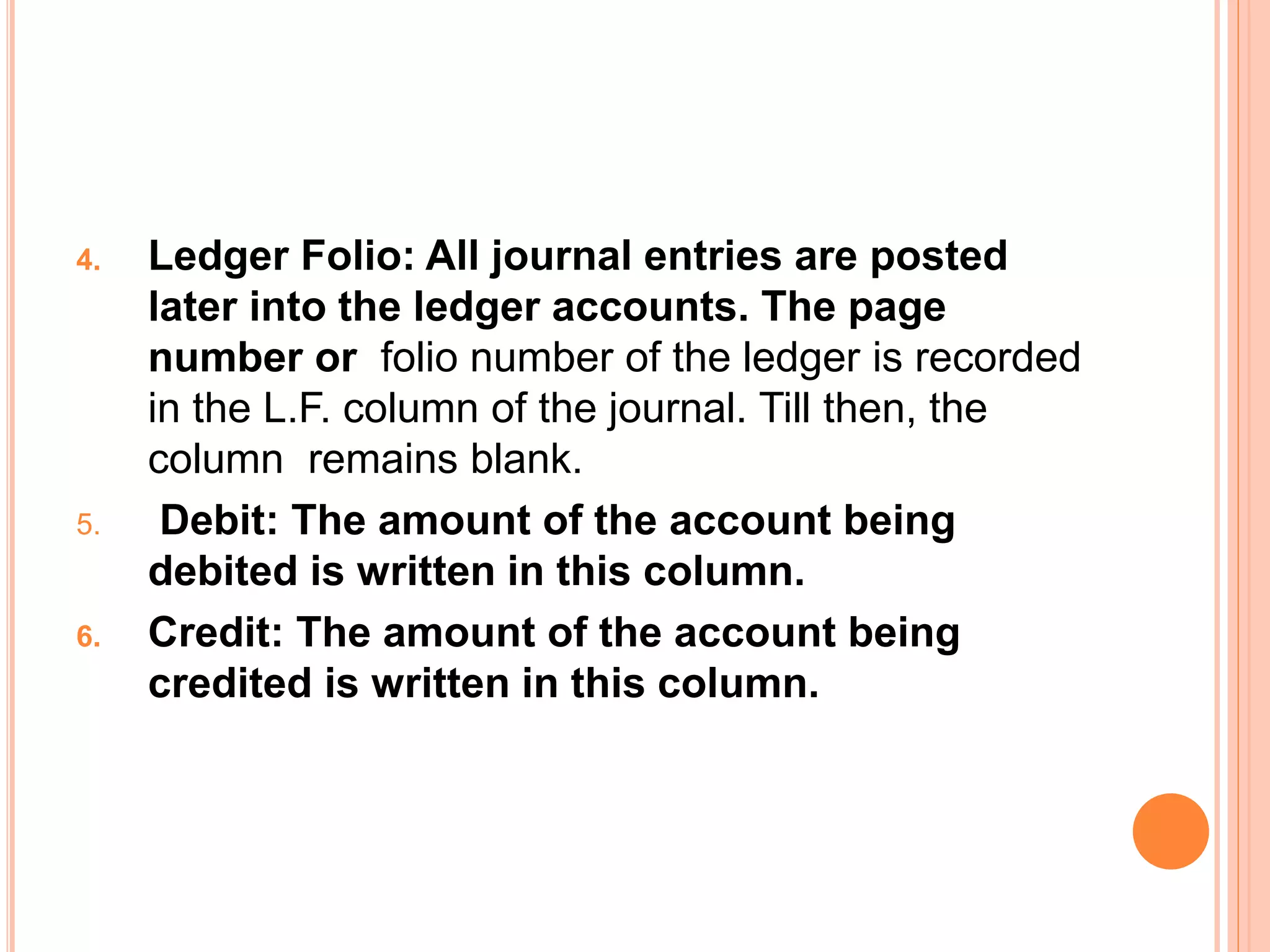

Details on how to structure journal entries, including date, particulars, narration, ledger folio, debit, and credit.

Discussion on the limitations of using journals for recording transactions, including bulkiness and challenges in compliance.

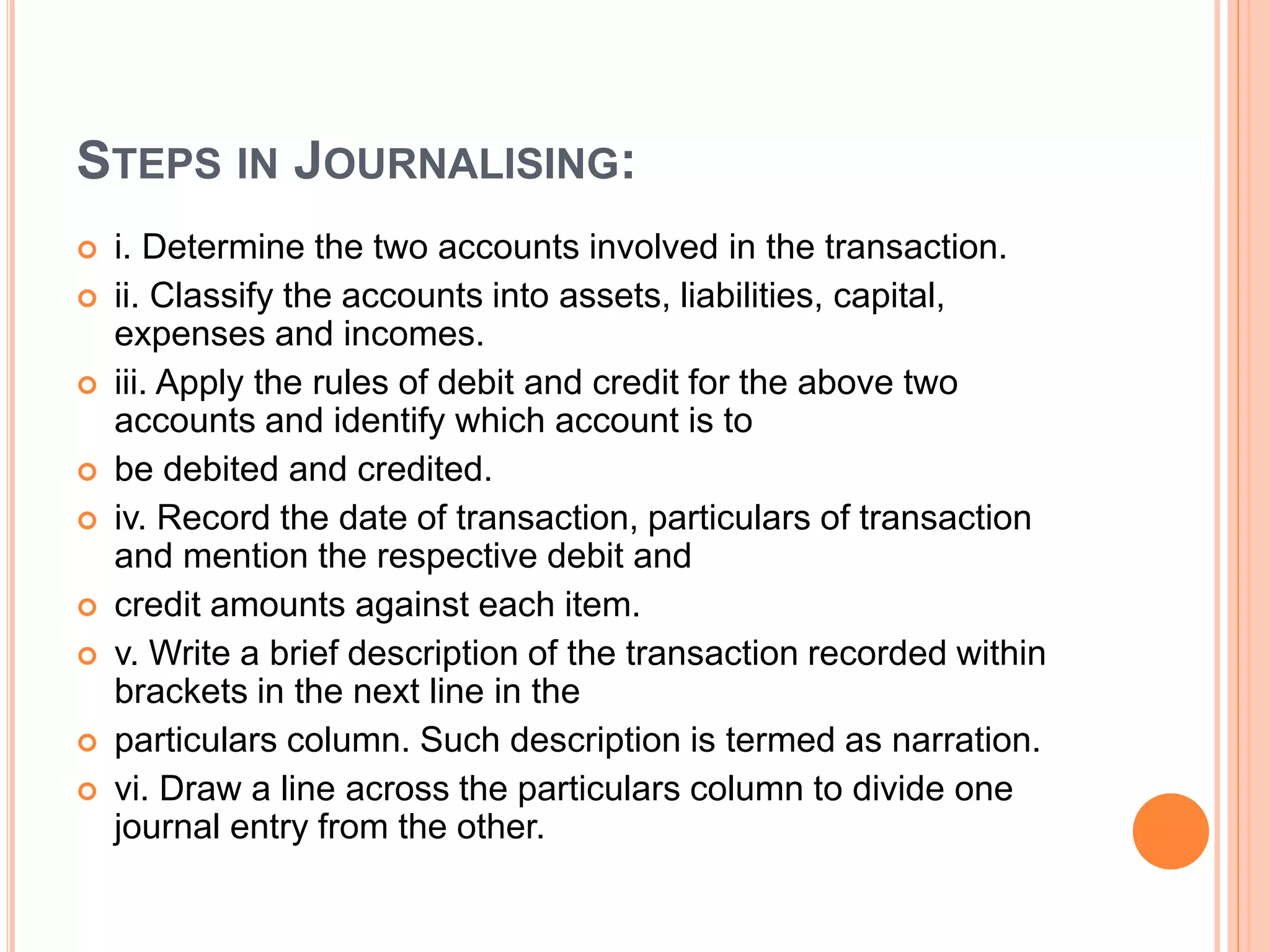

A step-by-step guide on how to journalise accounting transactions effectively.

Guidelines for identifying whether a transaction is cash or credit and the implications for accounting.

Clarity on purchase and sale transactions, including related accounts and how returns and closing stock are handled.

Definition of discount as a reduction in price and the types of discounts, including trade and cash discounts.