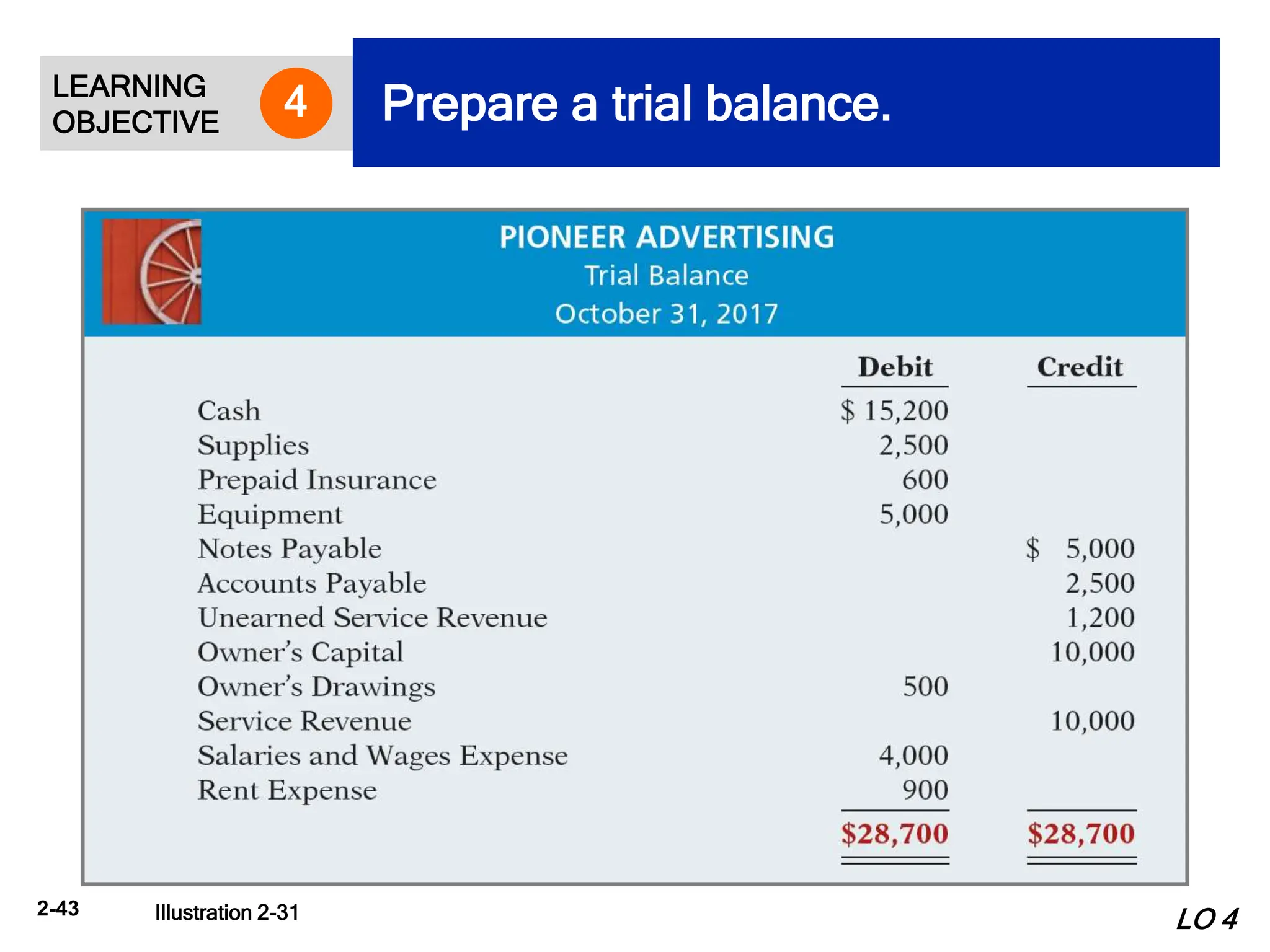

The document outlines the recording process in accounting, emphasizing the use of accounts, debits, and credits to accurately manage business transactions and maintain equilibrium in the accounting equation. It explains the double-entry system, detailing how each transaction affects multiple accounts and requires that total debits equal total credits. Additionally, it discusses the importance of journals and ledgers in recording and posting transactions, as well as preparing trial balances, while comparing procedures under GAAP and IFRS.