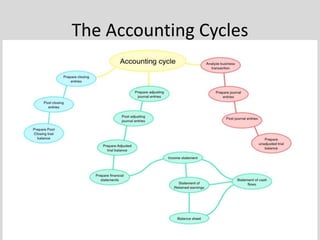

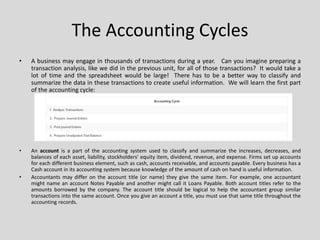

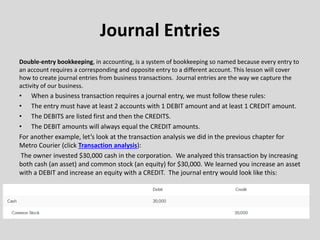

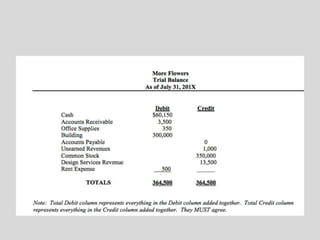

The document provides an overview of the accounting cycle, including defining key concepts like journals, ledgers, debits and credits, and the trial balance. It explains how transactions are recorded in journals using double-entry bookkeeping, then posted to ledger accounts. A trial balance is prepared by listing account balances to ensure total debits equal total credits. Errors may occur and need to be corrected by tracing transactions through to their source.