Downloaded 203 times

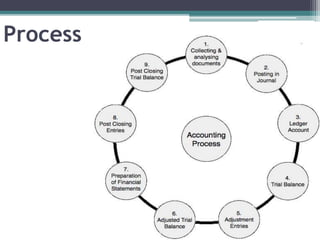

The accounting process involves collecting documents, posting journal entries, transferring balances to ledger accounts, preparing a trial balance, making adjustments, creating an adjusted trial balance, preparing financial statements, making post-closing entries, and generating a post-closing trial balance. Source documents are collected and analyzed throughout the accounting period. Journal entries are posted using double entry accounting. Ledger accounts track debit and credit balances. An initial trial balance is prepared, then adjustment entries are made and an adjusted trial balance is created to develop financial statements showing the firm's profits, losses, and financial health. Finally, revenue and expense accounts are closed out and balances transferred in post-closing entries.